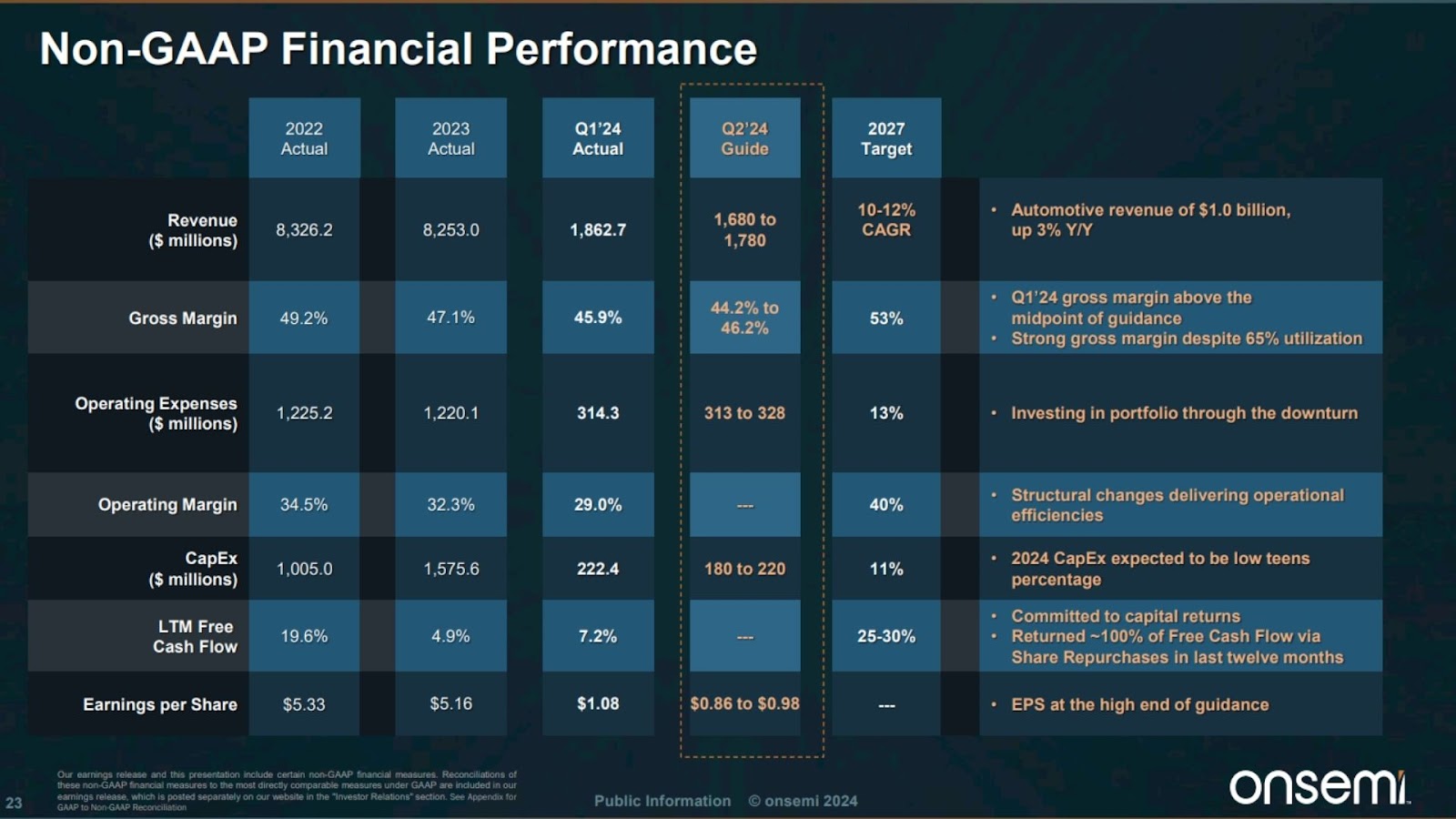

ON Semiconductor (ON) came out the last two weeks with some big announcements for silicon carbide (SiC), including a new supply agreement with several Volkswagen brands in Europe. No word on how much this could affect the growth trajectory to the upside, so let’s keep it at management’s stated goal through 2027 (10% to 12% CAGR, see later in the article).

In light of this, we thought we’d share this post we made for our Semiconductor Insider members on Discord. Onsemi is making moves to keep its high-end industrial and auto chip fabs full with work to do for the next few years.

Originally posted July 9, 2024

The world is in the midst of a semiconductor manufacturing boom. A traditionally conservative industry that (out of necessity due to the high-and-rising cost of semis) only expands manufacturing capacity until it has customer commitments.

But fueled by nearly every industrialized nation funneling cash into onshoring or friendshoring initiatives, new semi manufacturing capacity is being built at a frenzied pace.

Some companies are being thoughtful about their expansion plans, though. A few months ago, we wrote an article about Microchip’s (MCHP) “AI acquisition” to help fill up some of its current excess fab capacity. https://www.fool.com/investing/2024/04/22/1-top-chip-stock-goes-on-the-ai-acquisition-hunt/

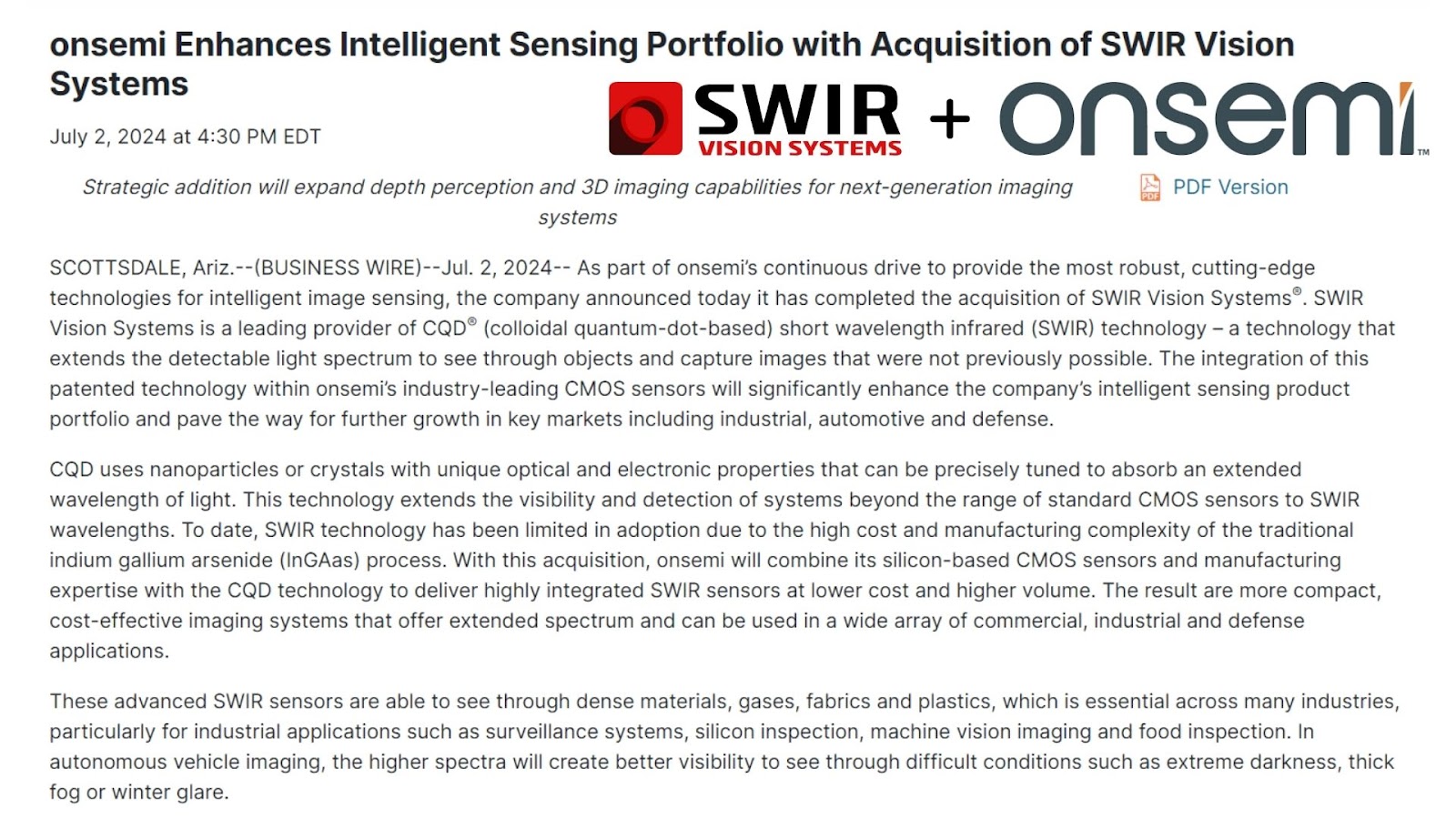

Now it’s ON Semiconductor’s turn to do the same. In early July, Onsemi announced an acquisition (it didn’t provide financial transaction details, which almost always means the price paid was very small) of a potentially revolutionary semiconductor technology – CQD SWIR. https://investor.onsemi.com/news-releases/news-release-details/onsemi-enhances-intelligent-sensing-portfolio-acquisition-swir

The acronym soup sounds cool, what is it?

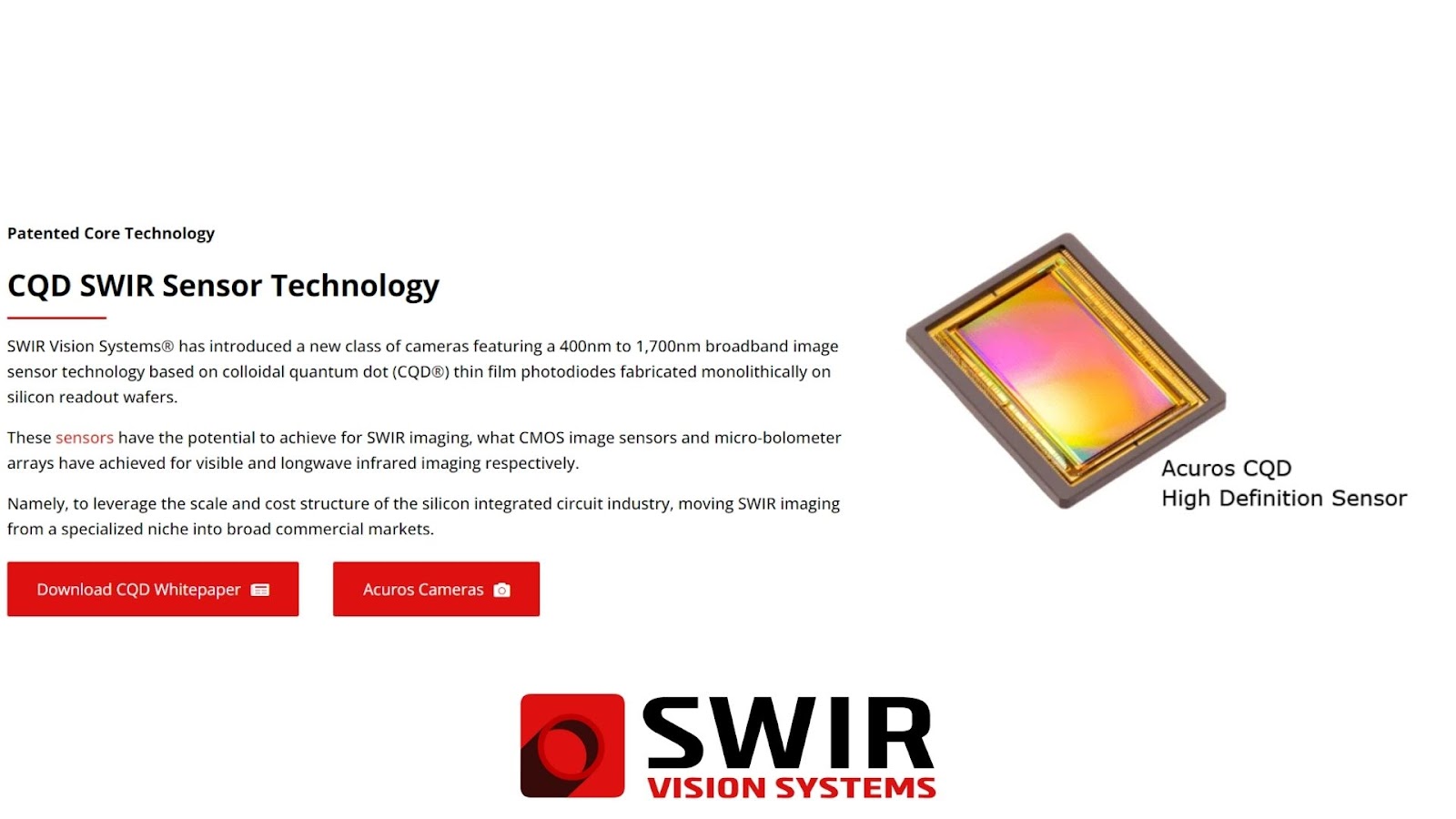

The CQD® (colloidal quantum-dot-based) short wavelength infrared (SWIR) technology that Onsemi just purchased is via the small startup business called SWIR Vision Systems. SWIR (pronounced “sweer,” according to the company) was founded in 2018 on a new tech that “extends” the spectrum of visible light into the infrared part of the spectrum.

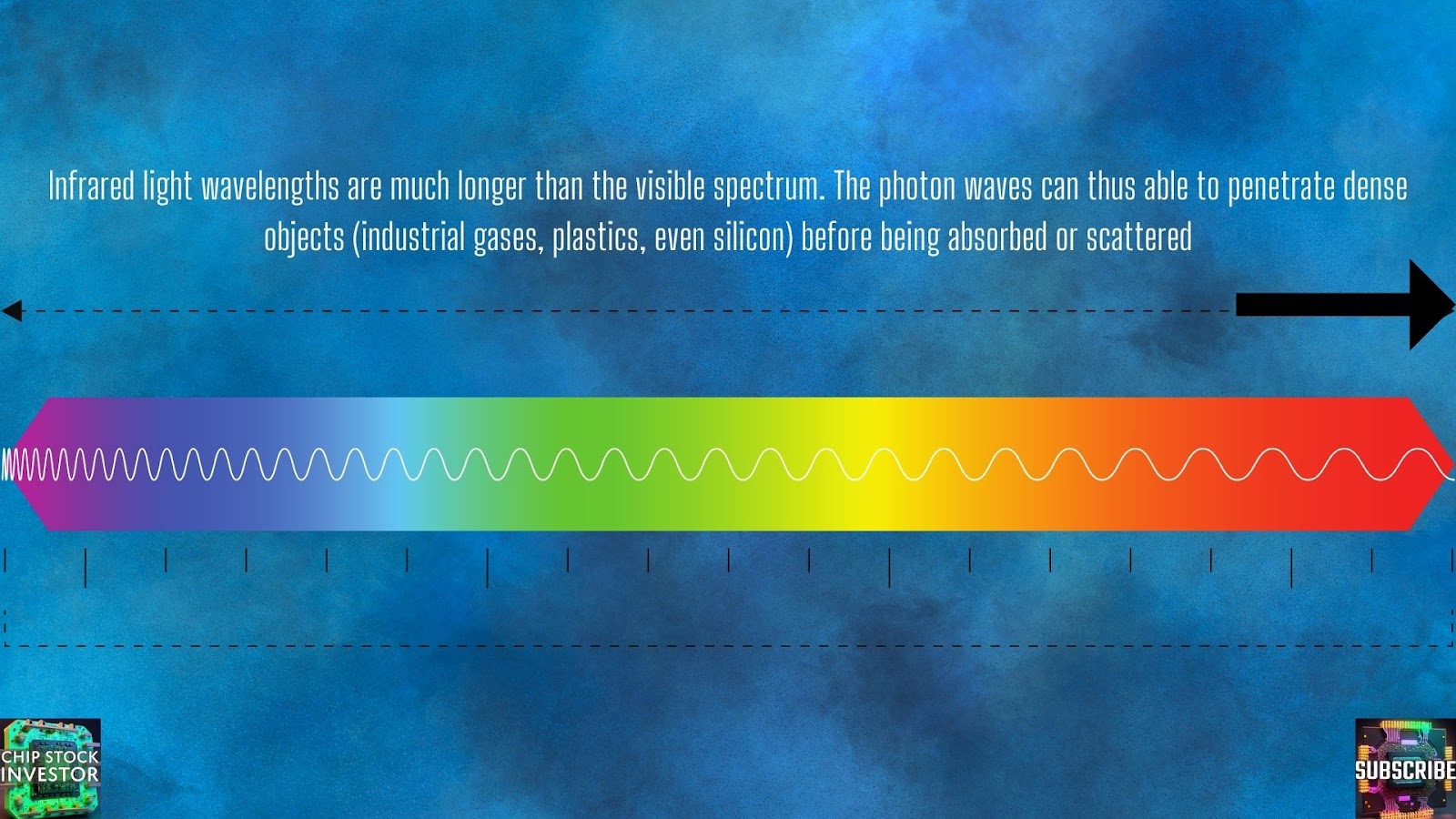

Why is that a big deal? Well, CQD SWIR apparently combines the benefits of high-resolution imaging from cameras that operate in the visible spectrum of light, with the power of the infrared spectrum to penetrate dense objects and substances – from industrial gases to plastics to silicon.

How does this iteration of SWIR work?

Why can infrared light penetrate dense objects? We’ll borrow a slide we made a few months ago when explaining ASML’s (ASML) ultraviolet light, which also lies just beyond the visible spectrum, but opposite infrared. These wavelengths are very short, which means they are easily absorbed or scattered when passing through some gases, plastics, silicas, etc.

By contrast, infrared has a much longer wavelength, so it can penetrate denser objects before being absorbed or scattered.

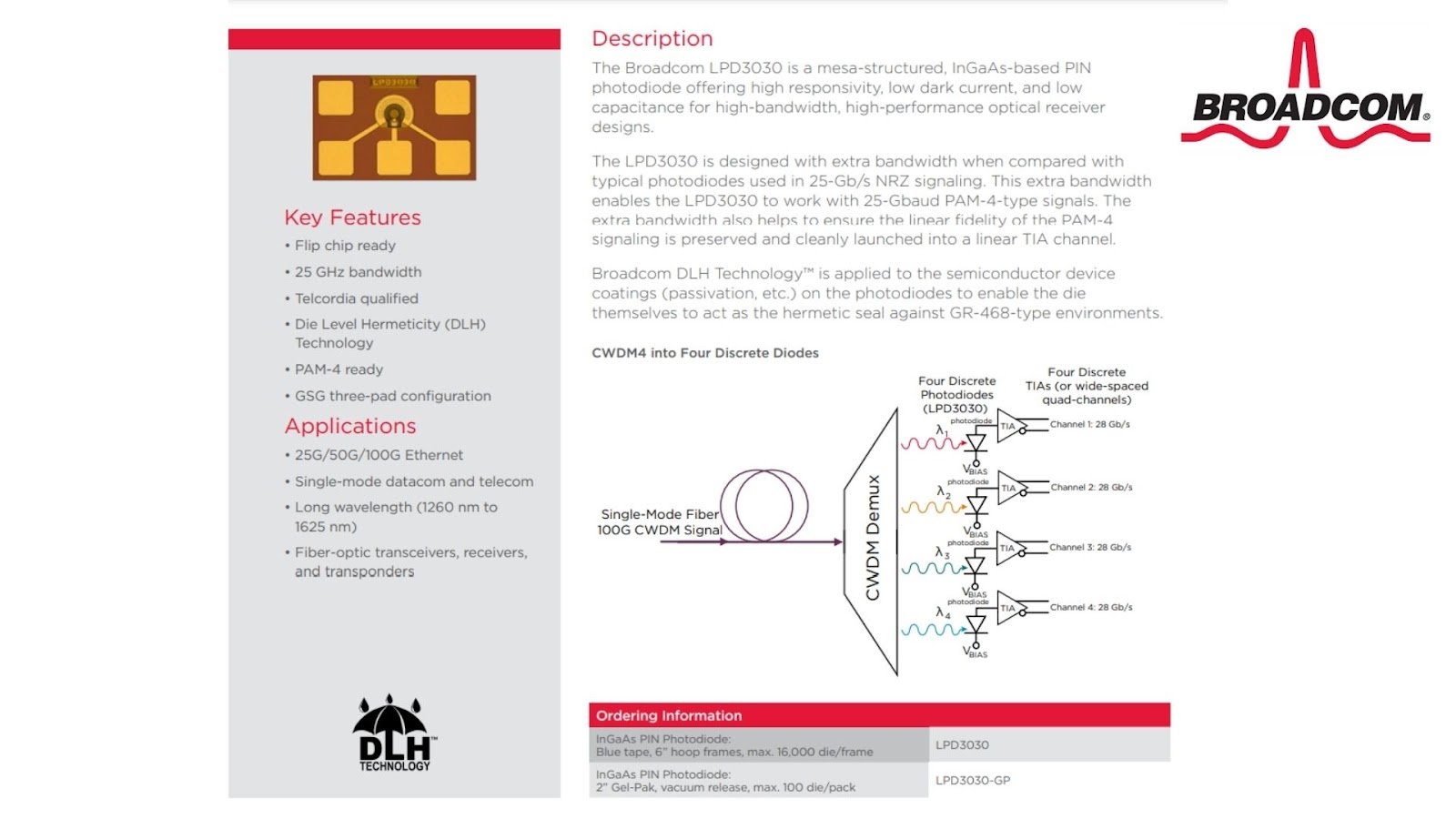

SWIR Vision Systems notes on its website and marketing materials that traditional infrared devices and cameras are really expensive. That’s because short-wavelength infrared light semiconductor detectors are traditionally made with the complicated compound material InGaAs (indium gallium arsenide). Perhaps you’ve seen InGaAs devices used in industrial cameras from Coherent (COHR), or similar from the likes of Hamamatsu Photonics (TYO:6965) displayed below. Here’s our last video on Coherent. Or there’s Broadcom (AVGO), which also has an InGaAs portfolio for its portfolio of fiber-optic networking components. Where Would AI Chip Stocks Be (Nvidia Included) Without Lasers? Coherent Scores A Top AI Chip CEO https://docs.broadcom.com/doc/LPD3030-PB100 https://www.coherent.com/laser-power-energy-measurement/photodetectors

The research hub IMEC (or Interuniversity Microelectronics Center, a privately-owned organization based in Belgium) has been working on making InGaAs manufacturing more efficient for years. But SWIR Vision Systems’ CQD SWIR technology gets the high-resolution of the visible spectrum (using silicon devices) by extending camera technology into the near-infrared (NIR) realm – all using a non-InGaAs process, instead leveraging good old-fashioned CMOS manufacturing techniques on silicon substrates. https://www.imec-int.com/en/articles/imec-demonstrates-shortwave-infrared-swir-range-hyperspectral-imaging-camera https://www.imec-int.com/en/articles/imec-reports-monolithic-thin-film-image-sensor-for-the-swir-range-with-record-pixel-density

But, according to SWIR Vision Systems:

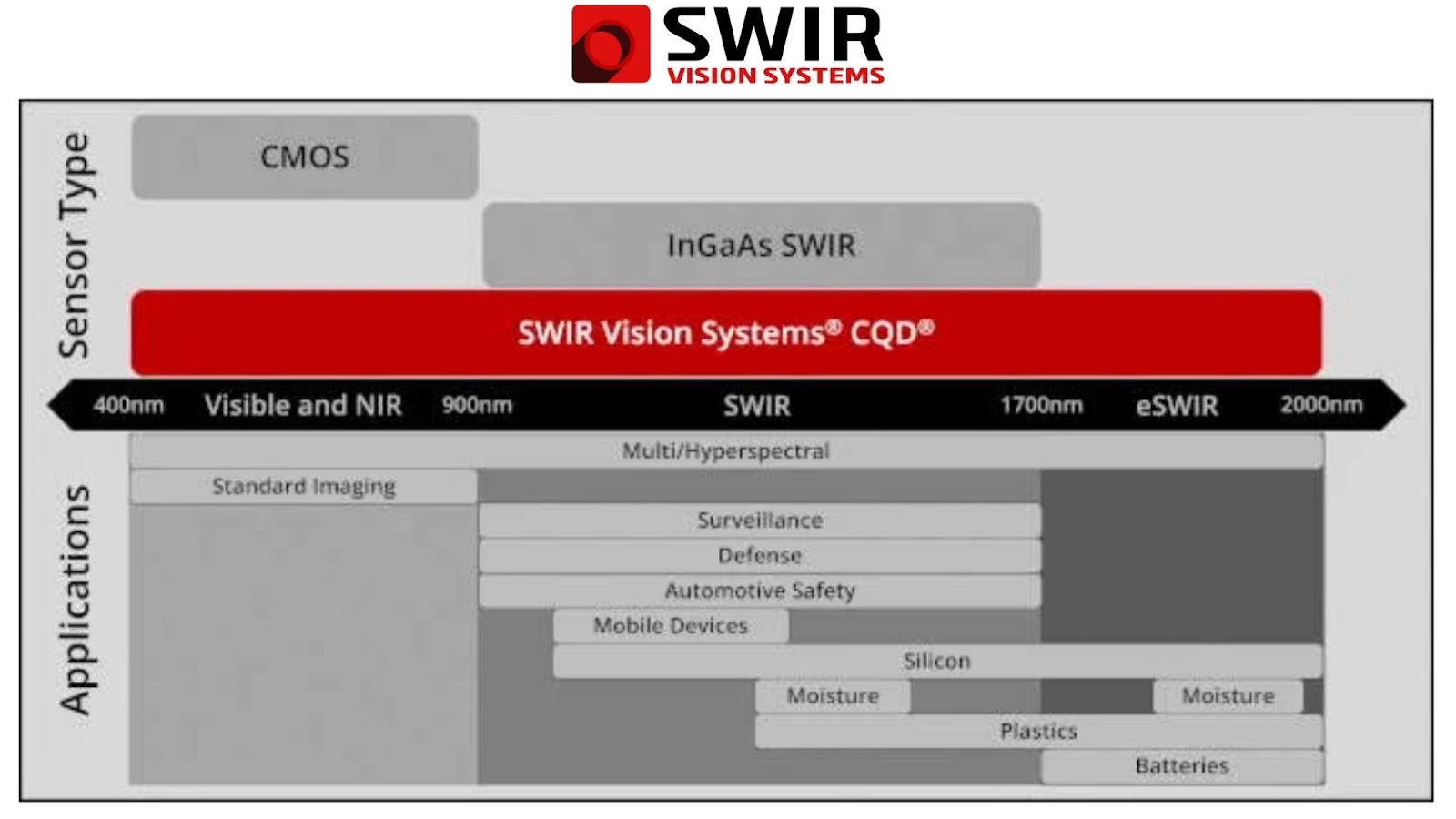

“SWIR generally refers to the wavelength band of light between 900nm and 2500nm.

Since standard silicon sensors have an upper limit of approximately 1000nm, SWIR imaging requires sensors and SWIR camera components capable of operation in the shortwave infrared range, which exceeds the upper limit of silicon. Indium gallium arsenide (InGaAs) sensors are commonly used in SWIR imaging, typically covering the 900nm to 1700nm range. But InGaAs devices are inherently expensive and face challenges in scaling to smaller pixel pitches and higher resolution arrays.

Unlike Long Wave Infrared (LWIR) light, which is emitted from the object itself, SWIR or shortwave infrared light is similar to visible light in that photons are reflected or absorbed by an object, providing the strong contrast needed for high-resolution imaging. While LWIR imagers give off more poorly defined thermal images, SWIR imagers deliver high-resolution images, much like visible light cameras.” https://www.swirvisionsystems.com/about/what-is-swir/

What will CQD SWIR be used for?

According to Onsemi:

“With this acquisition, onsemi will combine its silicon-based CMOS sensors and manufacturing expertise with the CQD technology to deliver highly integrated SWIR sensors at lower cost and higher volume. The result are more compact, cost-effective imaging systems that offer extended spectrum and can be used in a wide array of commercial, industrial and defense applications.”

So Onsemi’s hope is that SWIR Vision System’s CQD can be plugged into its existing silicon sensors business, and turned from niche industrial product to large-scale solution for many applications. Per the Onsemi press release:

“These advanced SWIR sensors are able to see through dense materials, gases, fabrics and plastics, which is essential across many industries, particularly for industrial applications such as surveillance systems, silicon inspection, machine vision imaging and food inspection. In autonomous vehicle imaging, the higher spectra will create better visibility to see through difficult conditions such as extreme darkness, thick fog or winter glare.”

An important chip market, addressing big secular trends

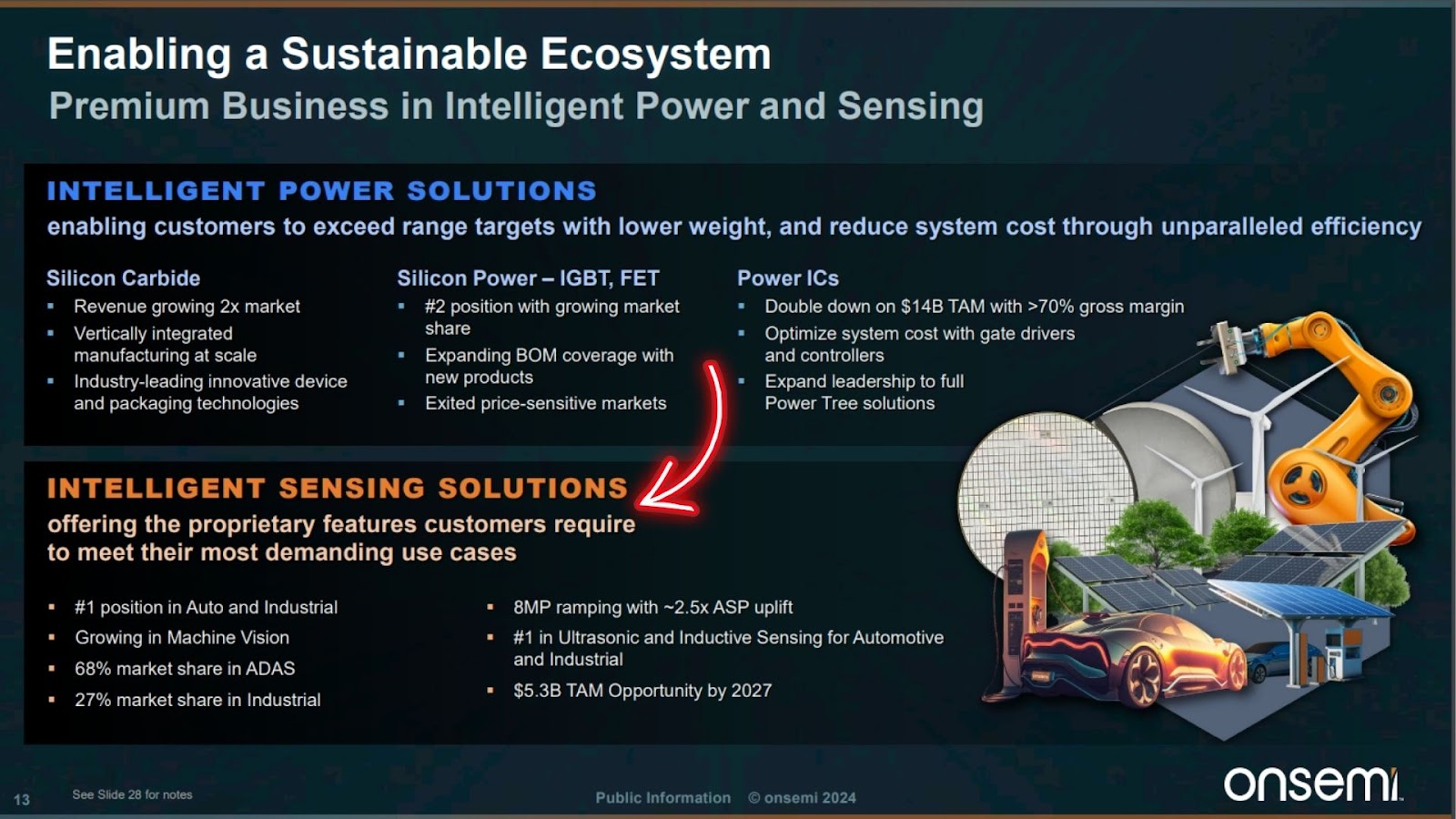

Onsemi management recently reorganized its revenue reporting segments into “Automotive,” “Industrial” (which is further segmented in two: “power tools” or industrial goods closer to the consumer, and “secular growth industrial” or megatrends like renewable energy/next-gen power grid solutions and factory automation), and “Other.”

Before this shuffle, though, Onsemi used to report revenues per the following methodology. The smallest of those old segments, “Intelligent Sensing,” is where SWIR Vision Systems will be filed.

You may have heard CEO Hassane El-Khoury talk about some of these sensors in recent earnings calls. Onsemi is actually a leader in high-resolution imaging sensors, a secular growth trend particularly suited to industrial processes and manufacturing – including semiconductor manufacturing, where high-resolution cameras are needed in inspection equipment. (Onsemi thus helps complete the virtuous cycle of chipmaking, see our last metrology video: The Secret Stocks Powering the Future of AI – What Investors Need to Know Right Now)

The small acquisition (we should know a bit more detail in the Q3 2024 earnings report this autumn from the statement of cash flows, which is where acquisition expense is reported) of SWIR Vision Systems could thus be a small price to pay so Onsemi can continue to increase sales from this potentially high-growth industrial automation trend. Or, it could help speed up Onsemi’s leadership share of that part of the industry.

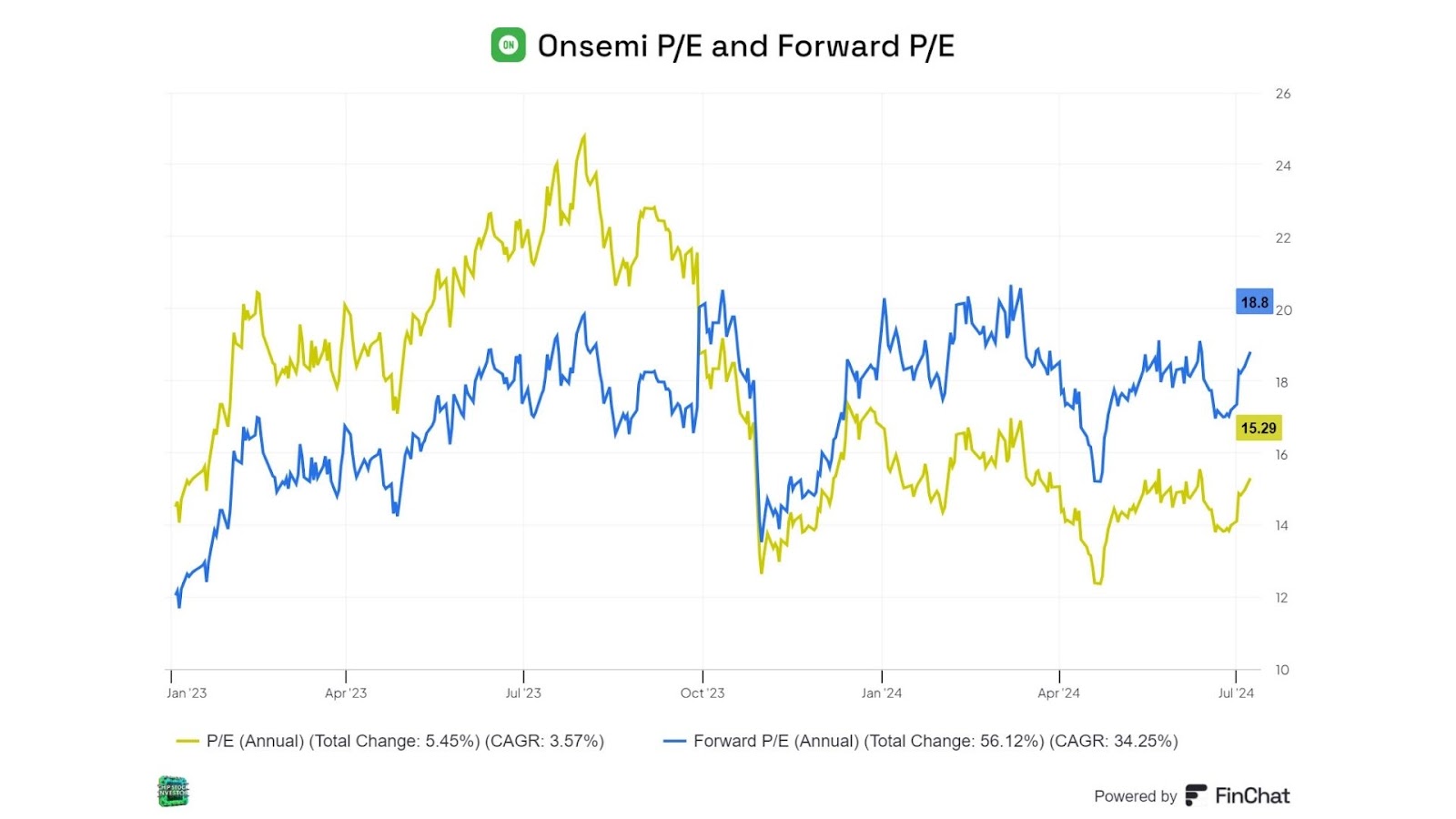

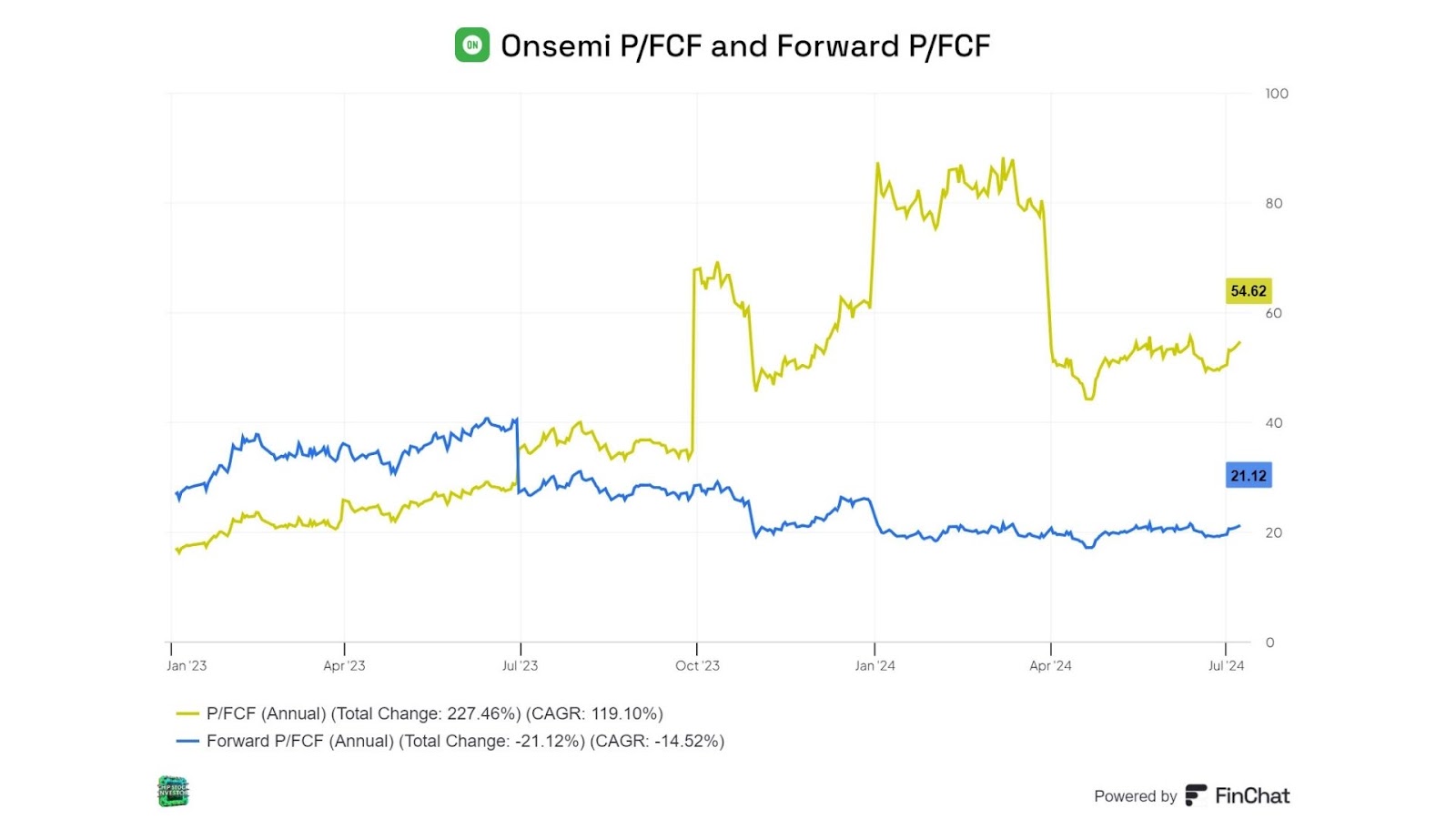

Onsemi’s path to even higher profitability

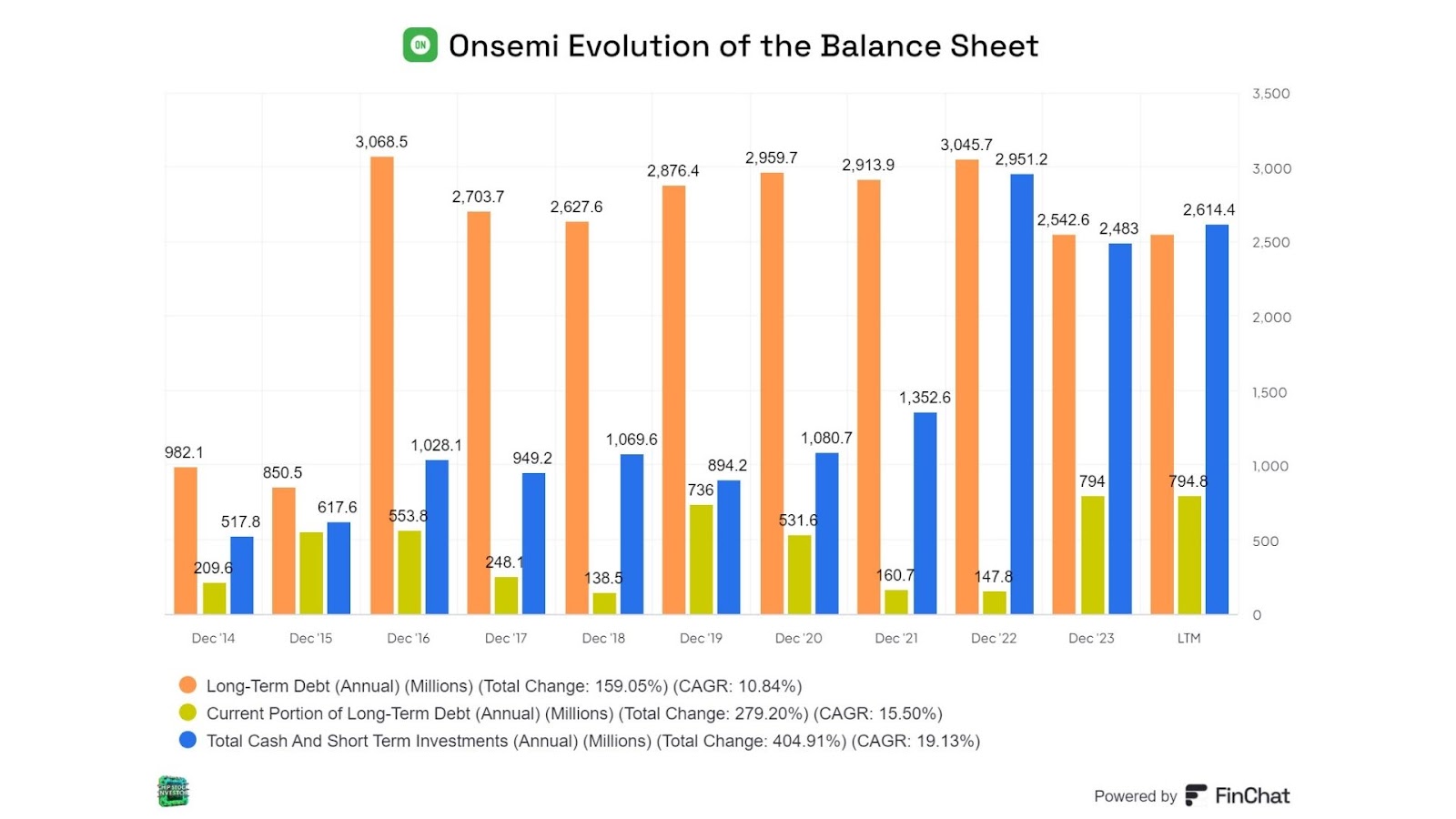

Up until let’s say about 2016, when Onsemi acquired the old and storied remnants of Fairchild Semiconductor for $2.4 billion in cash, the company operated in highly commoditized markets. Profitability was good, though not impressive, in good years. And during semi industry downturns, things could get a bit dicey. https://www.businesswire.com/news/home/20160919005796/en/ON-Semiconductor-Successfully-Completes-Acquisition-of-Fairchild-Semiconductor-for-2.4-Billion-in-Cash

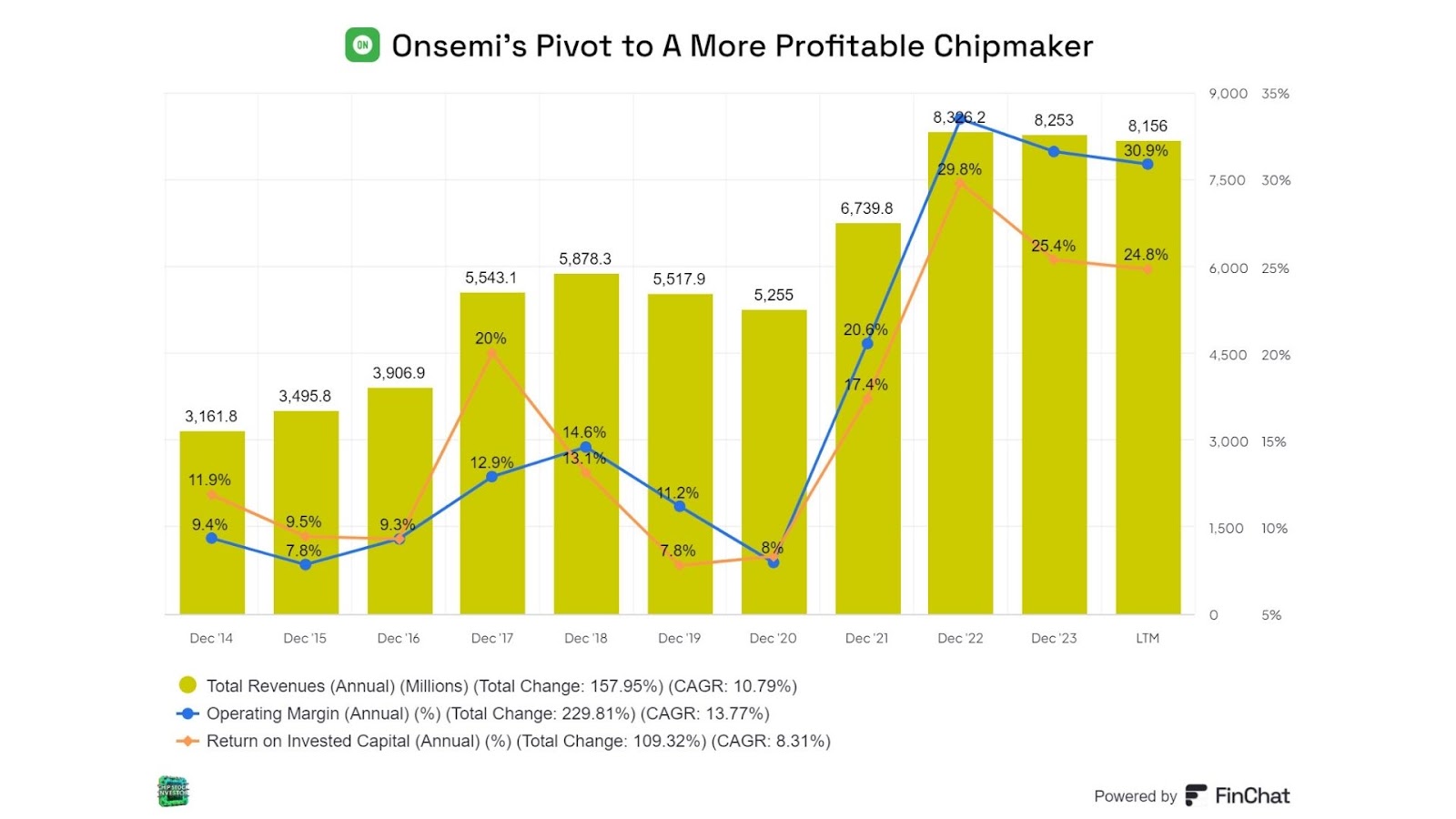

However, since CEO El-Khoury and CFO Thad Trent were brought in a few years ago (after leading Cypress Semiconductor to getting acquired by Infineon in early 2020), Onsemi’s story has centered less on revenue growth, more on profit margin expansion and increasing capital efficiency (in the chart above, measured by ROIC, or return on invested capital).

To pull it off, management has been employing a similar strategy as it did at Cypress:

1. Exit low-margin highly-commoditized (lots of competition) products

2. Sell fabs it doesn’t need

3. Revamp the existing fab base with higher-end chipmaking equipment and fill them with products addressing secular growth markets

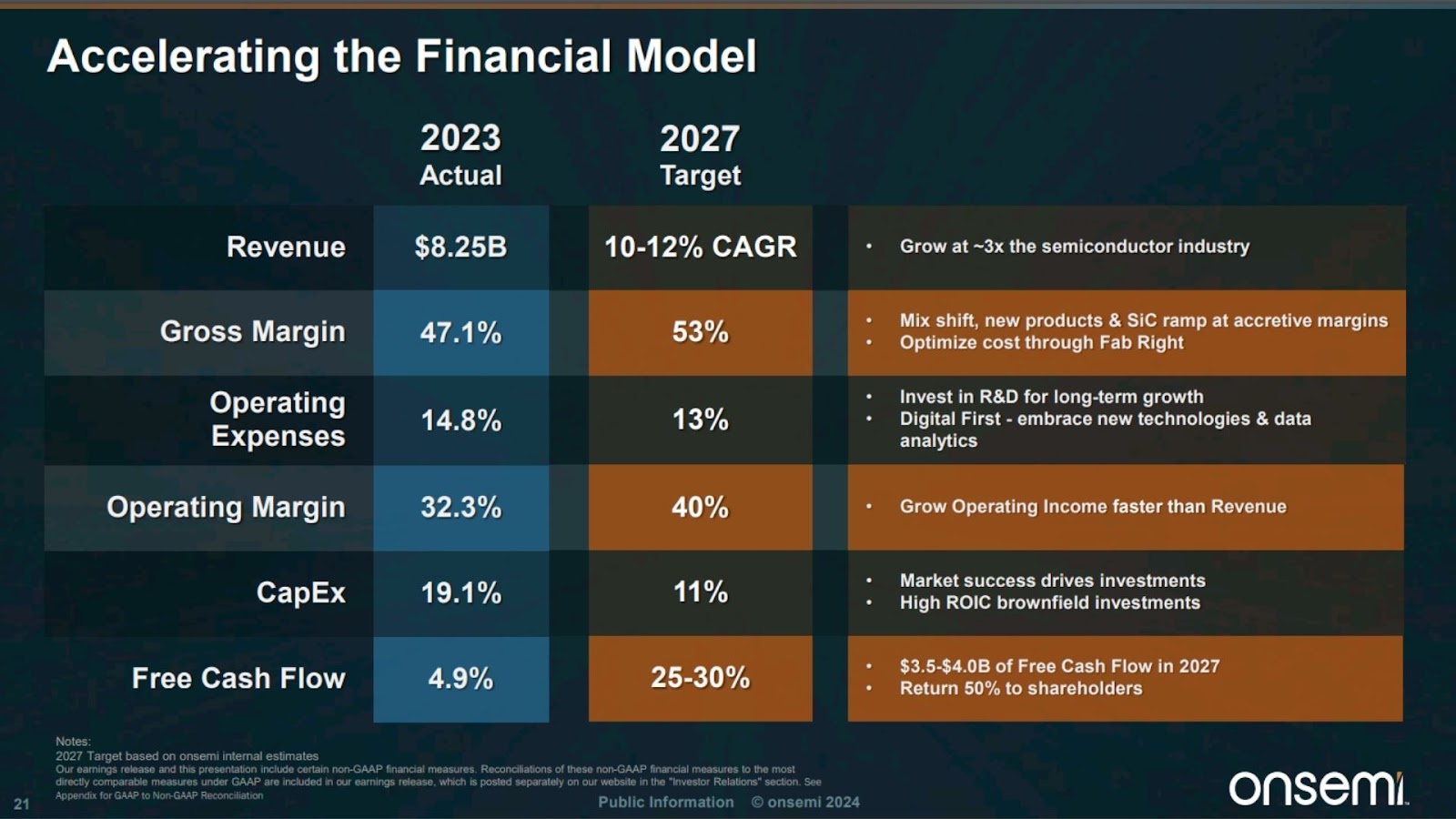

The top team believes it has lots more work to do as it tries to home in on 40% operating margins by 2027 – an ambitious goal, especially while simultaneously trying to enter new growth markets.

To get to this point, the top team sold four of its fabs in 2022 (at the last semi industry cyclical peak, fetching it top dollar). https://investor.onsemi.com/news-releases/news-release-details/onsemi-divests-wafer-manufacturing-sites-part-fab-liter-strategy https://investor.onsemi.com/news-releases/news-release-details/onsemi-divests-wafer-manufacturing-sites-part-fab-liter-strategy https://www.businesswire.com/news/home/20221209005487/en/LA-Semiconductor-Purchases-Fabrication-Plant-From-onsemi https://investor.onsemi.com/news-releases/news-release-details/onsemi-divests-niigata-japan-fab

That helped get the balance sheet back in good shape, so that it could do things like acquire the East Fishkill, New York fab from GlobalFoundries, which is now the home of Onsemi’s 300mm advanced power chip wafer production, and move its SiC business to its existing South Korea facilities. It also gave Onsemi the ability to ditch ~$475 million in low-margin highly cyclical products the last few years; plan SiC R&D and advanced packaging for its facilities in the Czech Republic; and make acquisitions like SWIR Vision Systems. https://investor.onsemi.com/news-releases/news-release-details/onsemi-selects-czech-republic-establish-end-end-silicon-carbide

And now here we are, at a cycle bottom (or close to one). El-Khoury and Trent believe a simple rebound in sales will provide the bulk of margin improvement through 2027. Currently, its smaller but more nimble and advanced manufacturing footprint is sitting at about 65% utilization. 80% or higher is the “sweet spot.” According to recent interview commentary from El-Khoury and Trent (from the BofA 2024 Global Technology Conference on June 5), for every 1 percentage point (pp) increase in fab utilization, margins go up about 20 basis points (0.2%). Increasing fab utilization to 80% minimum, then, gets Onsemi to about 3 pp or more in improvement from this point forward.

Now add in ongoing margin improvements as final separation of the four sold off fabs completes in 2025 and 2026, and getting the new East Fishkill fab more efficient along the way, gets Onsemi to that ~40% operating margin.

A best-bet on power and sensor manufacturing?

The small investment in SWIR technology illustrates the position of strength Onsemi is operating from right now. The balance sheet is in good shape, the company remains profitable even in the midst of a nasty downturn, and there’s significant upside ahead even if a semi industry recovery is muted.

In a recent video on the fabless power chip design Monolithic Power Systems (MPWR), Nick lamented having picked the wrong power chip stock for the last few years. The NVIDIA of Data Center Power Chip Stocks? And Next 10-For-1 Stock Split Candidate? MPWR Analysis

But that hardly means we’ve given up on Onsemi. Based on the company’s earnings power (GAAP earnings per share, as well as free cash flow), the stock could be mighty cheap right now. We’re happy to keep holding what we have, and will continue to nibble from time to time as 2024 progresses.