Lot’s of wild volatility in July, and it’s continued in August. Chip stocks got hit especially hard, some of them even after posting solid earnings.

And so we’re going to revamp our thesis that we started on Advanced Micro Devices (AMD) late last year: AMD AI is never going to create an “Nvidia moment,” but the chip designer can still be a winner with a focus on profit margin expansion.

First, some additional commentary on the “AI bubble” that we addressed last week through the lens of Alphabet (GOOGL), but this time pulling some comments from Microsoft’s (MSFT) latest earnings update. The TRUTH About the AI Bubble, Alphabet GOOGL Stock, and What It Means For Nvidia

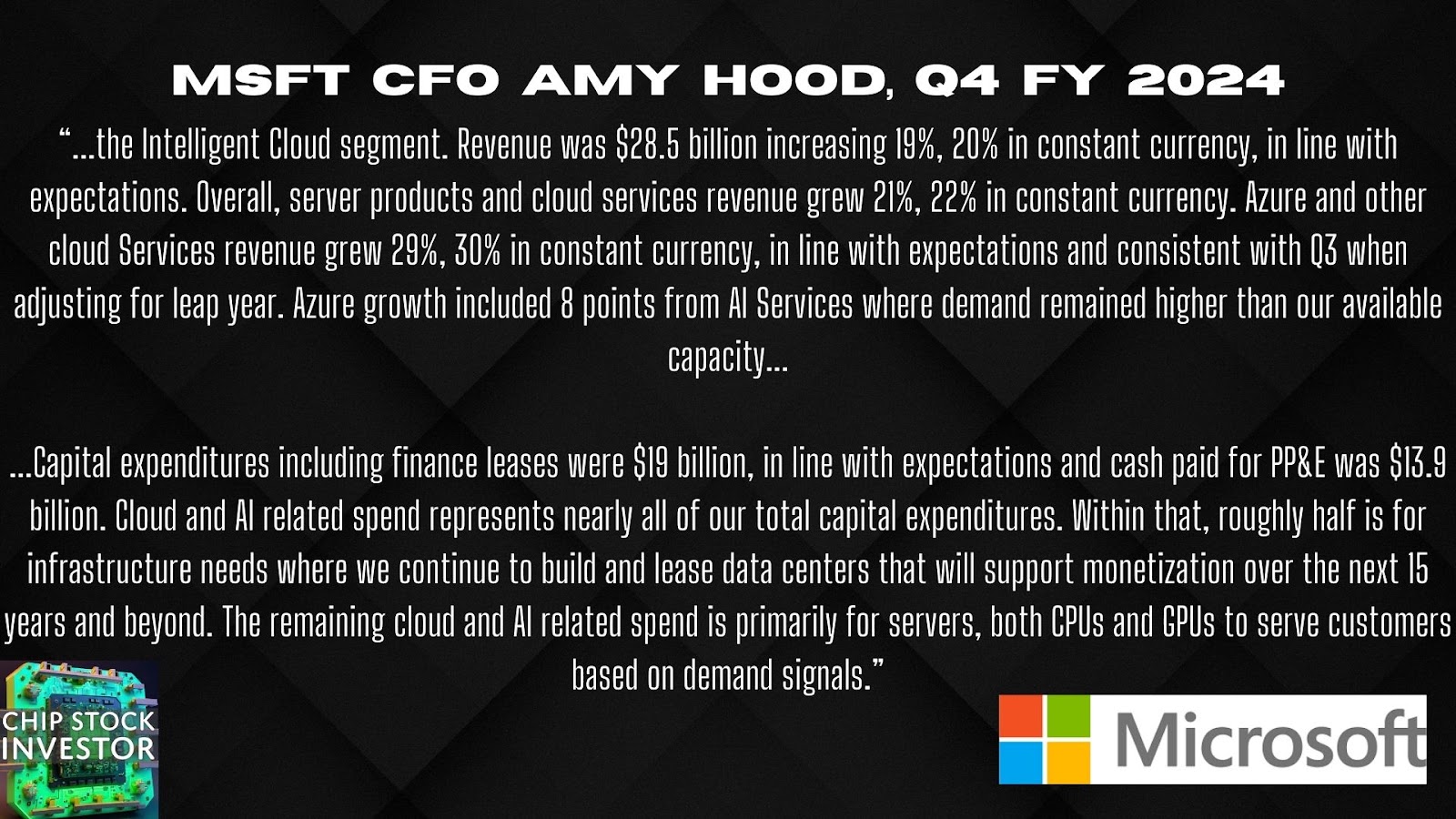

What is Microsoft spending all that money on?

Microsoft’s enterprise computing and cloud infrastructure business (including Azure Cloud) is a top user of AMD chips. And so, any update in Microsoft’s capital expenditures (CapEx, spending on property and equipment) is highly relevant to chip suppliers.

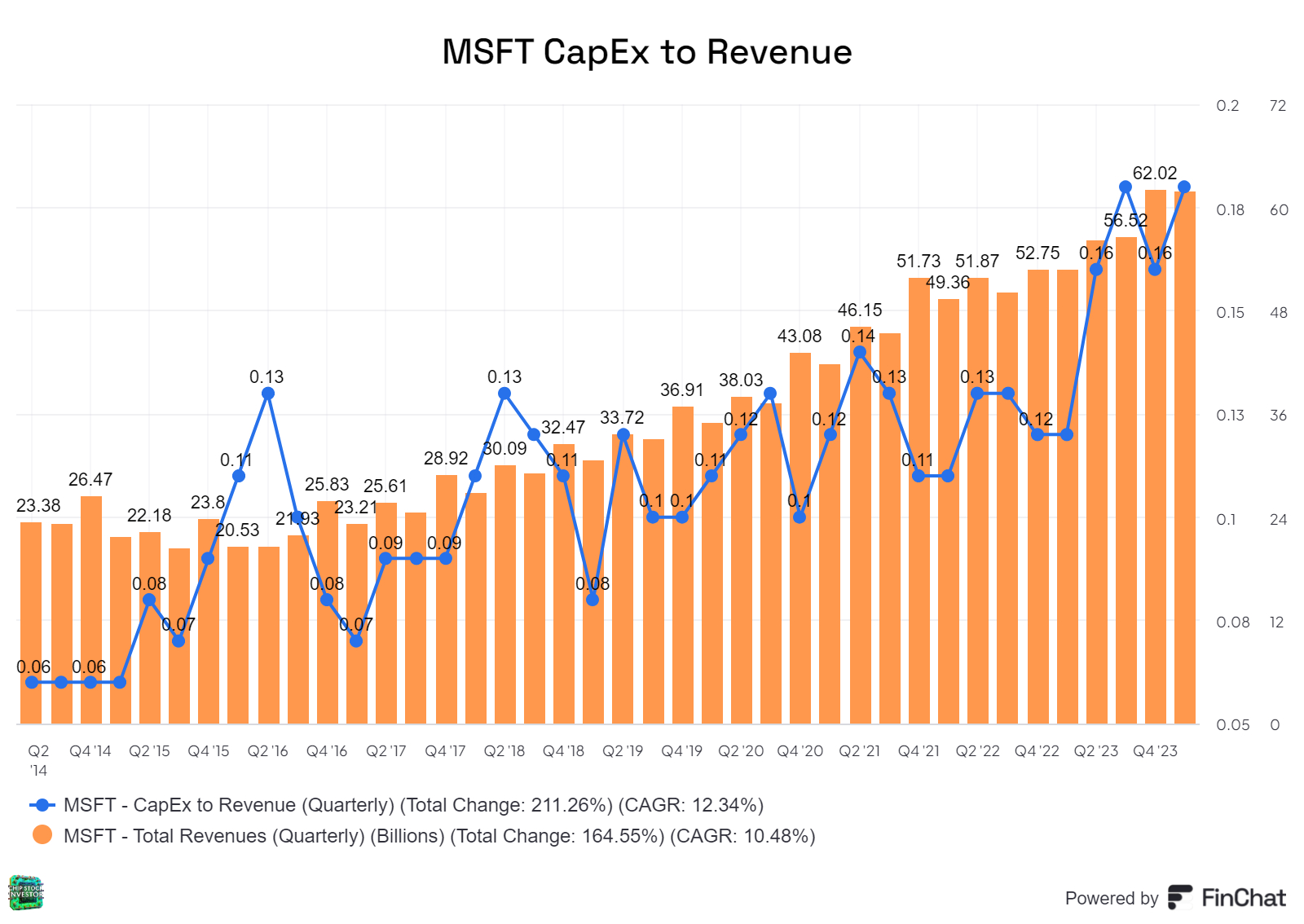

CapEx to revenue did rise to 21% in the last quarter (based on property and equipment spend, PPE in quote above), an elevated amount as MSFT continues to keep pace with the big data center leaders Amazon AWS, Google, Meta, and the other historically software-turned-cloud infrastructure-upstart Oracle.

However, as MSFT commented, this CapEx is in line with revenue growth for its cloud and Azure customers, and doesn’t represent an AI bubble – at least not yet. Time will tell how long the trend can last.

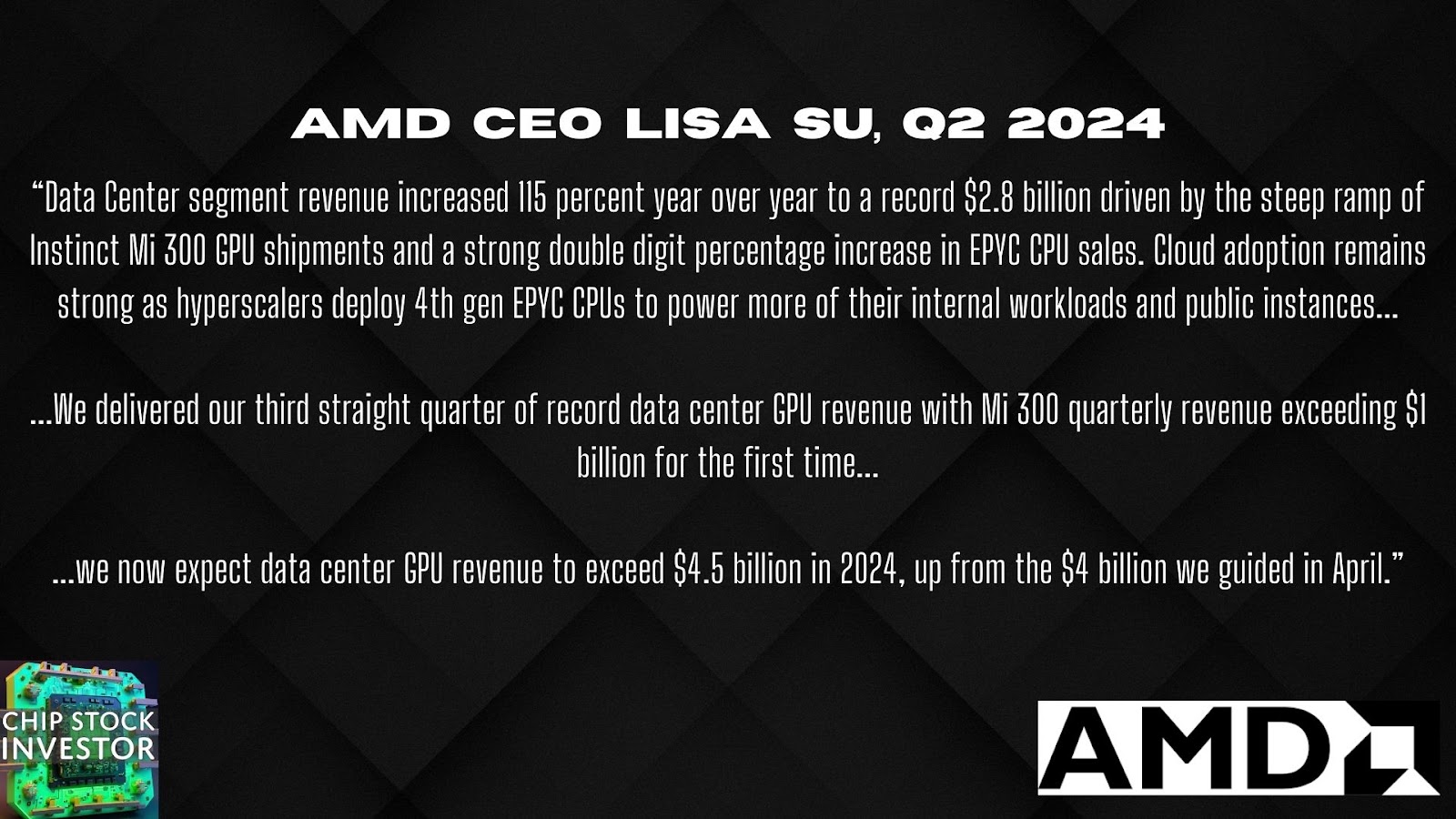

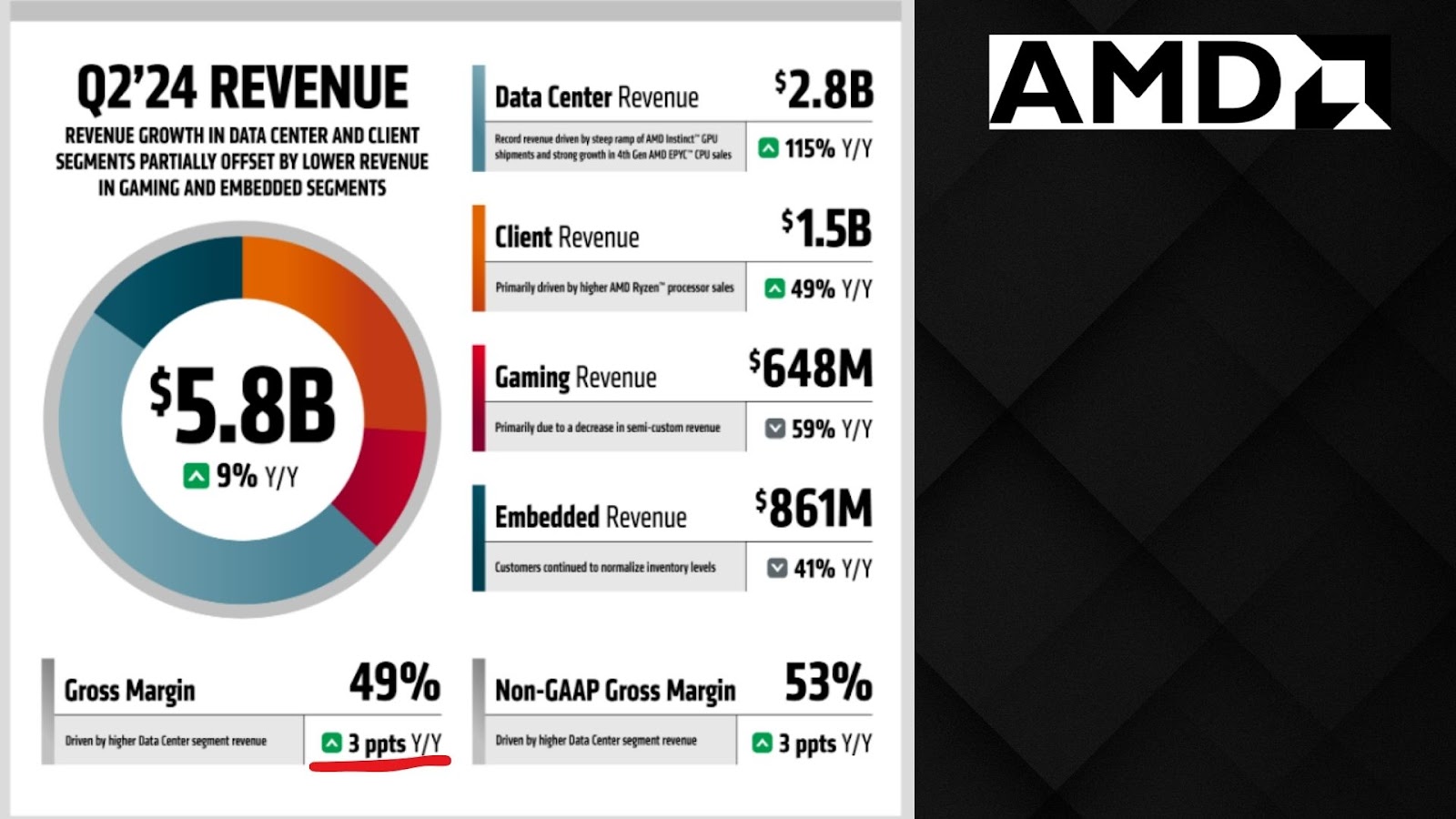

Onwards to AMD’s Q2 2024 update

In line with mega-tech CapEx spending, AMD’s data center segment (including accelerated computing and AI chips like the MI300X) had another good quarter of sales in Q2. CEO Lisa Su and company again raised the guidance a bit for accelerator sales (for cloud, not just AI) for full-year 2024.

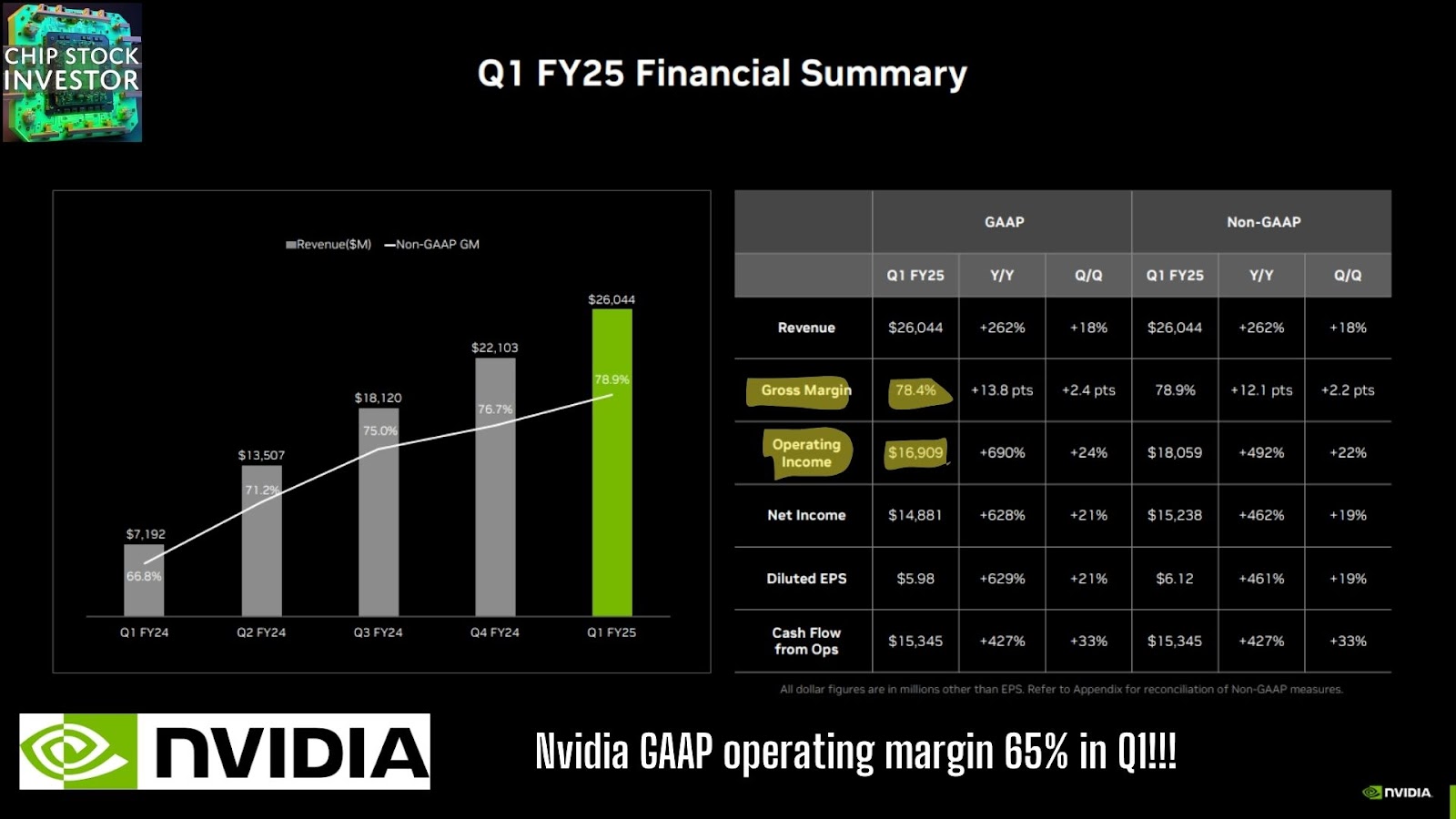

This bodes well for other fabless (outsourced manufacturing) chip designers, including Nvidia (NVDA), when they report Q2 numbers.

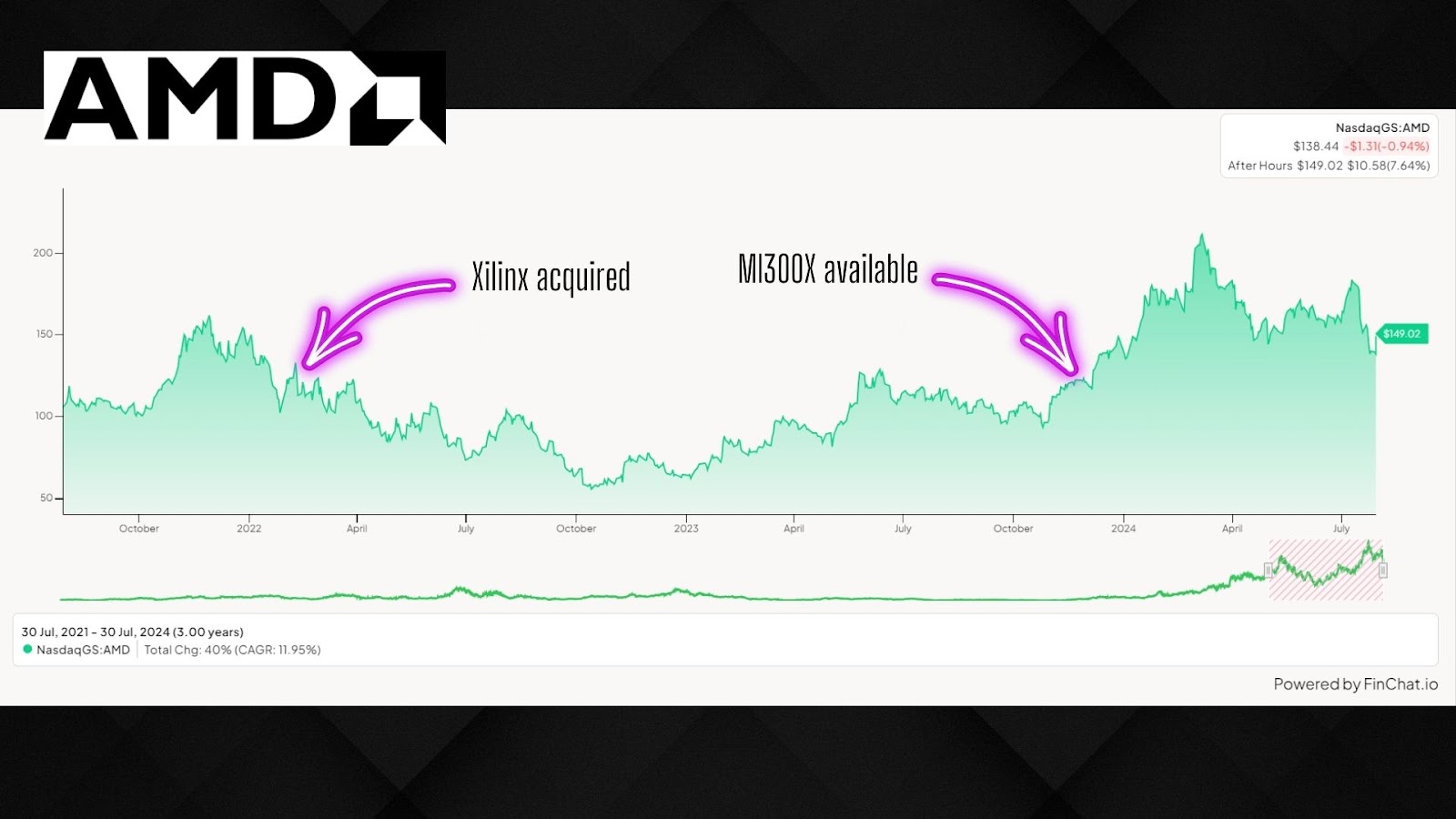

However, as an old company with a broad portfolio of products spanning multiple end markets, AMD just isn’t getting the triple-digit-% overall revenue growth Nvidia is. Legacy segments like Client and Gaming, as well as Embedded (from the Xilinx acquisition in early 2022), are diluting the data center growth.

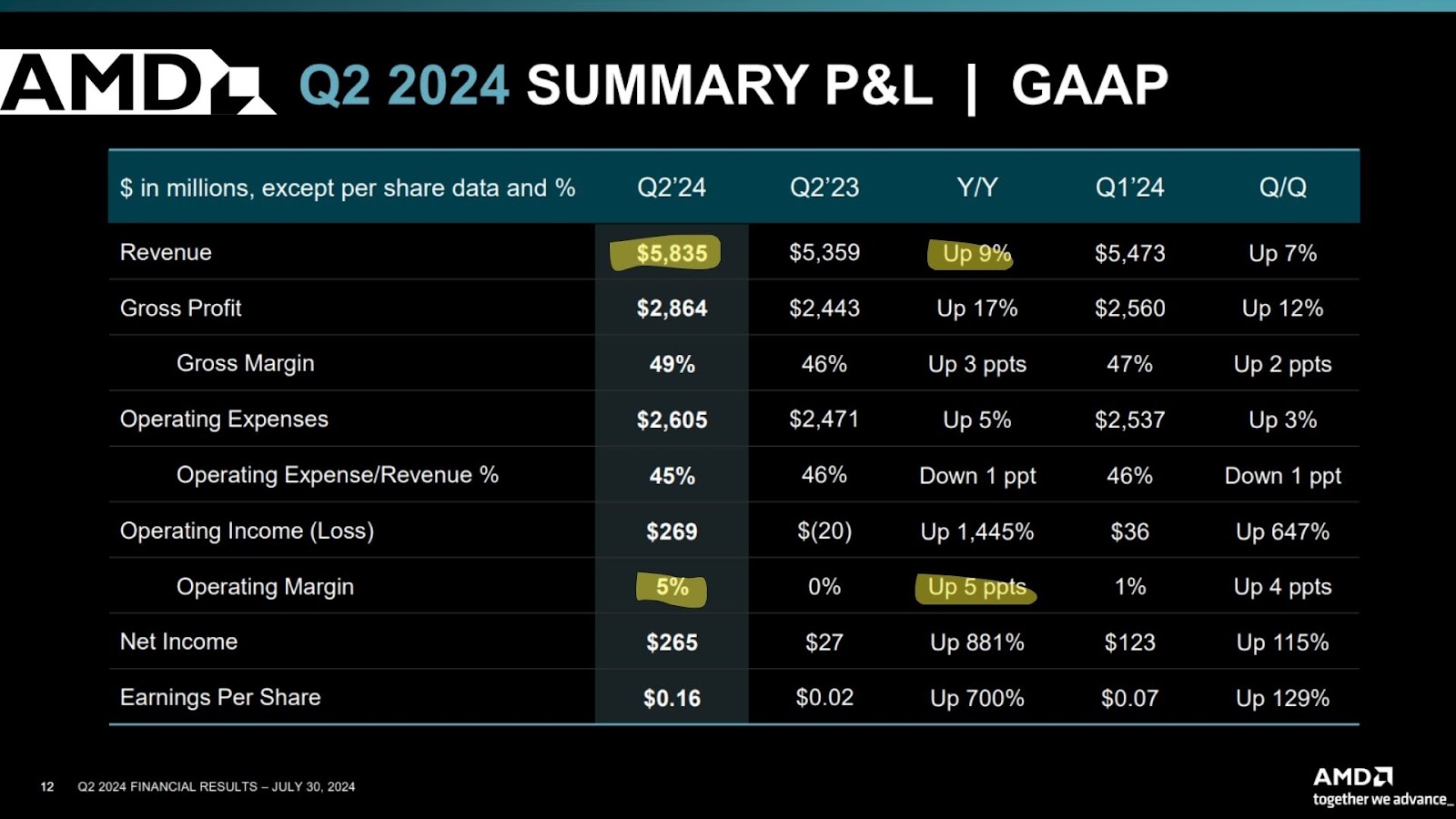

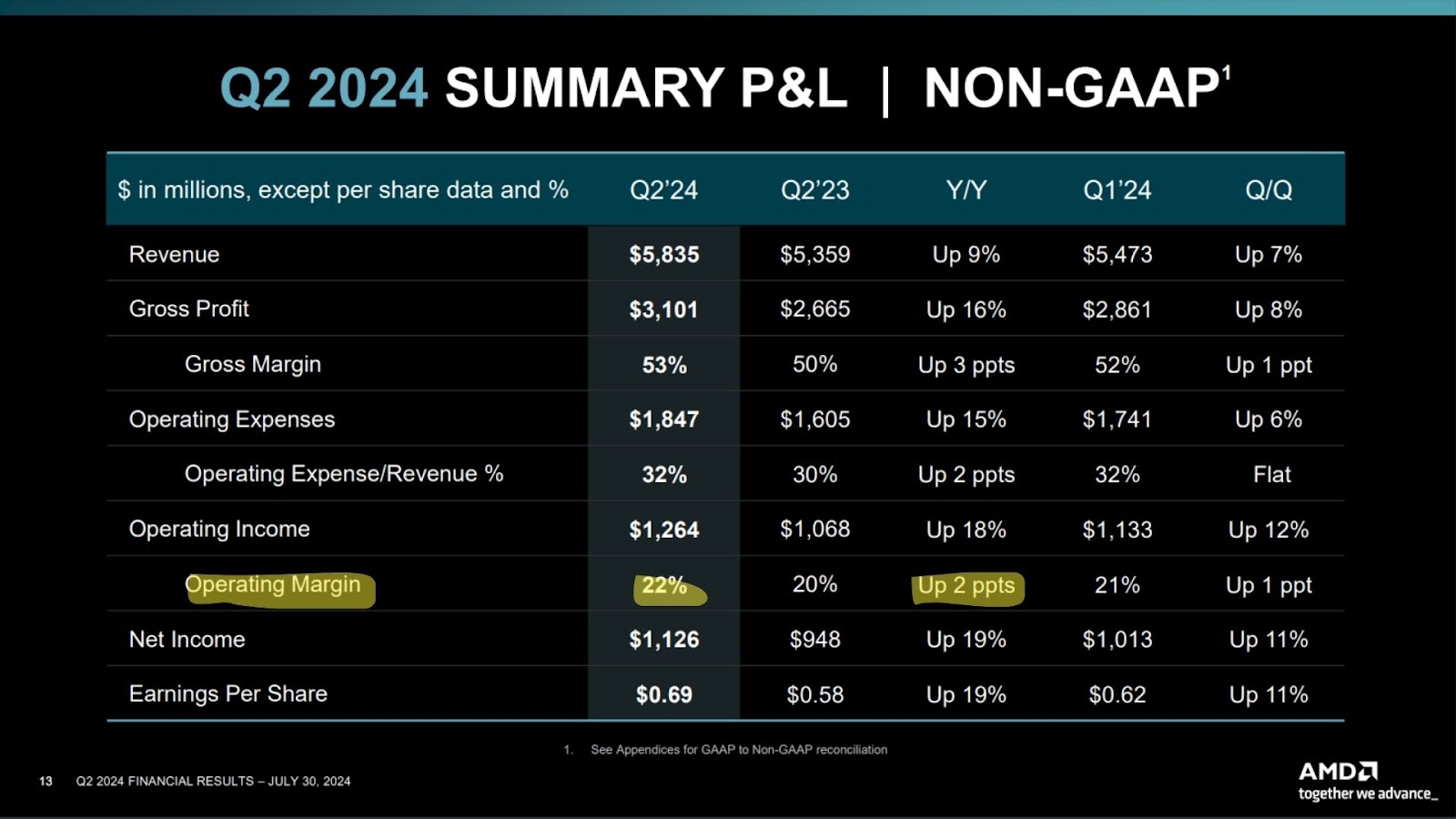

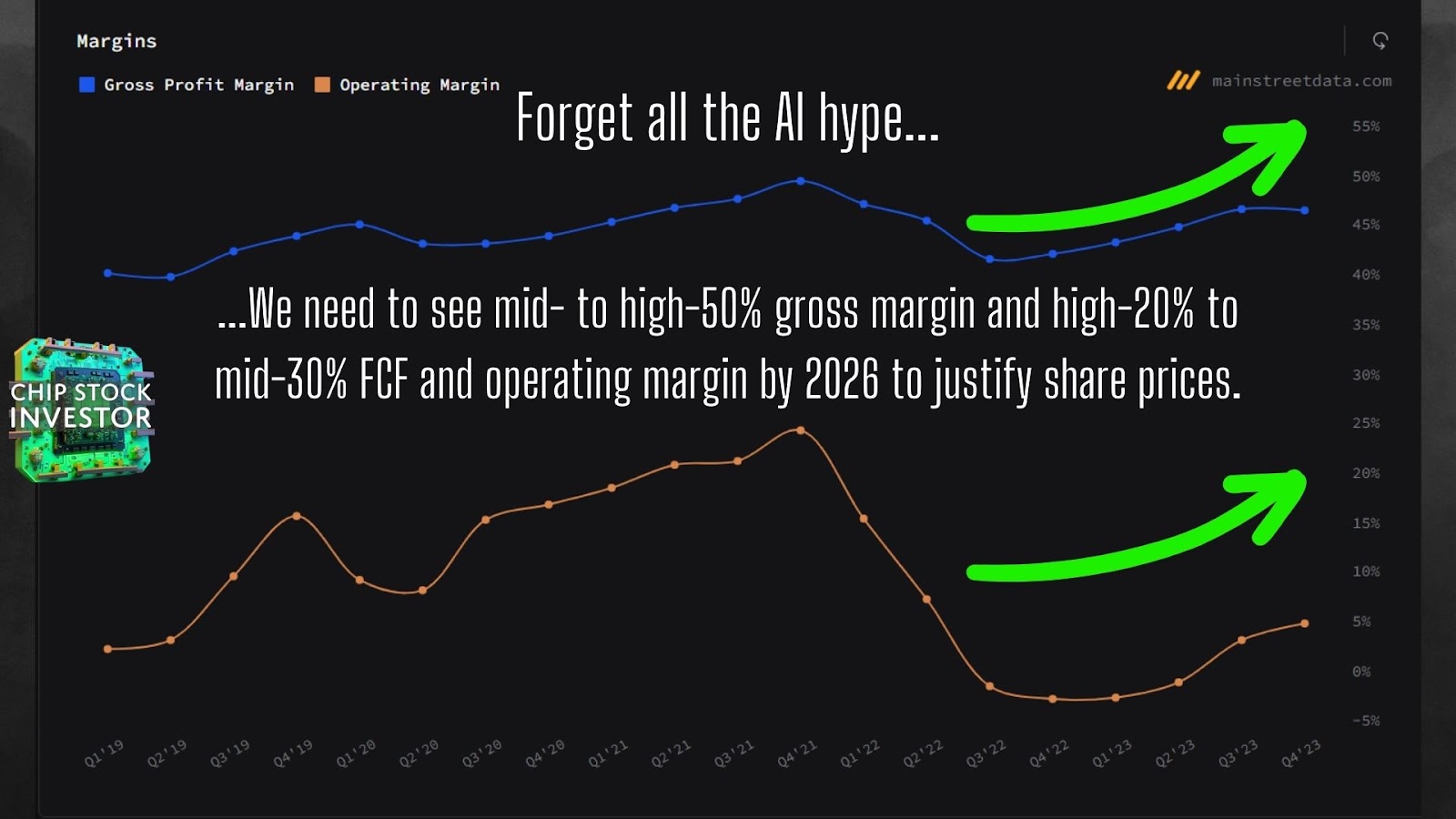

Thus, while investors have been hyper-focused on the MI300X “AI chip” (really a computing system), AMD’s most important metric continues to go ignored: Profit margin expansion following the chip market implosion of 2022 and 2023. Progress continues at a slow-but-steady pace on this front, both on a GAAP and adjusted basis.

However, as you can see above, AMD still has plenty of work to do in the profit margin department.

Drilling down into the margin nitty-gritty

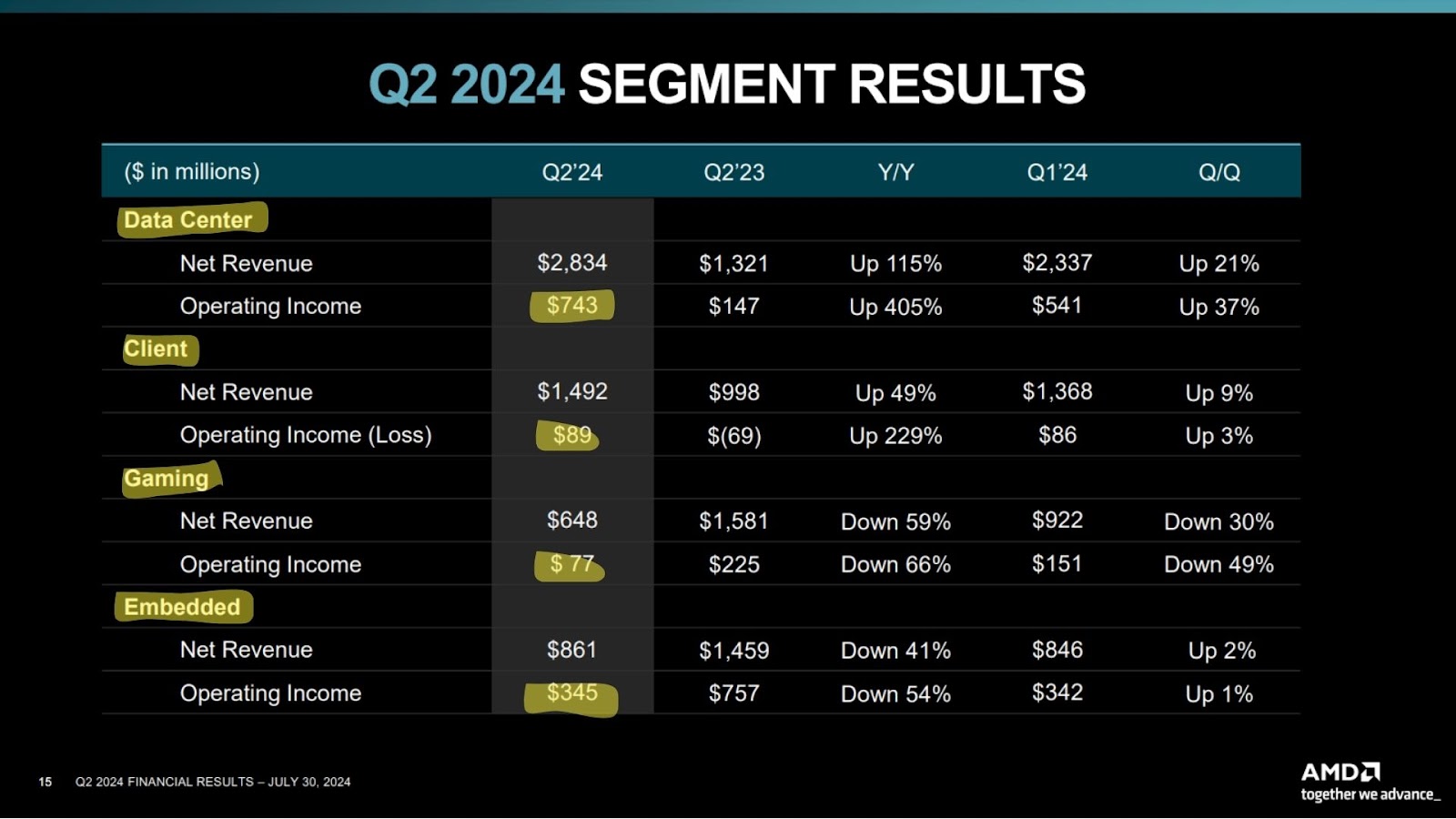

Again removing the AI hype, you can see below that AMD’s data center segment is starting to reach a healthy margin profile, though still not as good as Embedded (the old Xilinx FPGA biz). But this progress remains diluted by under-performing Client and Gaming margins.

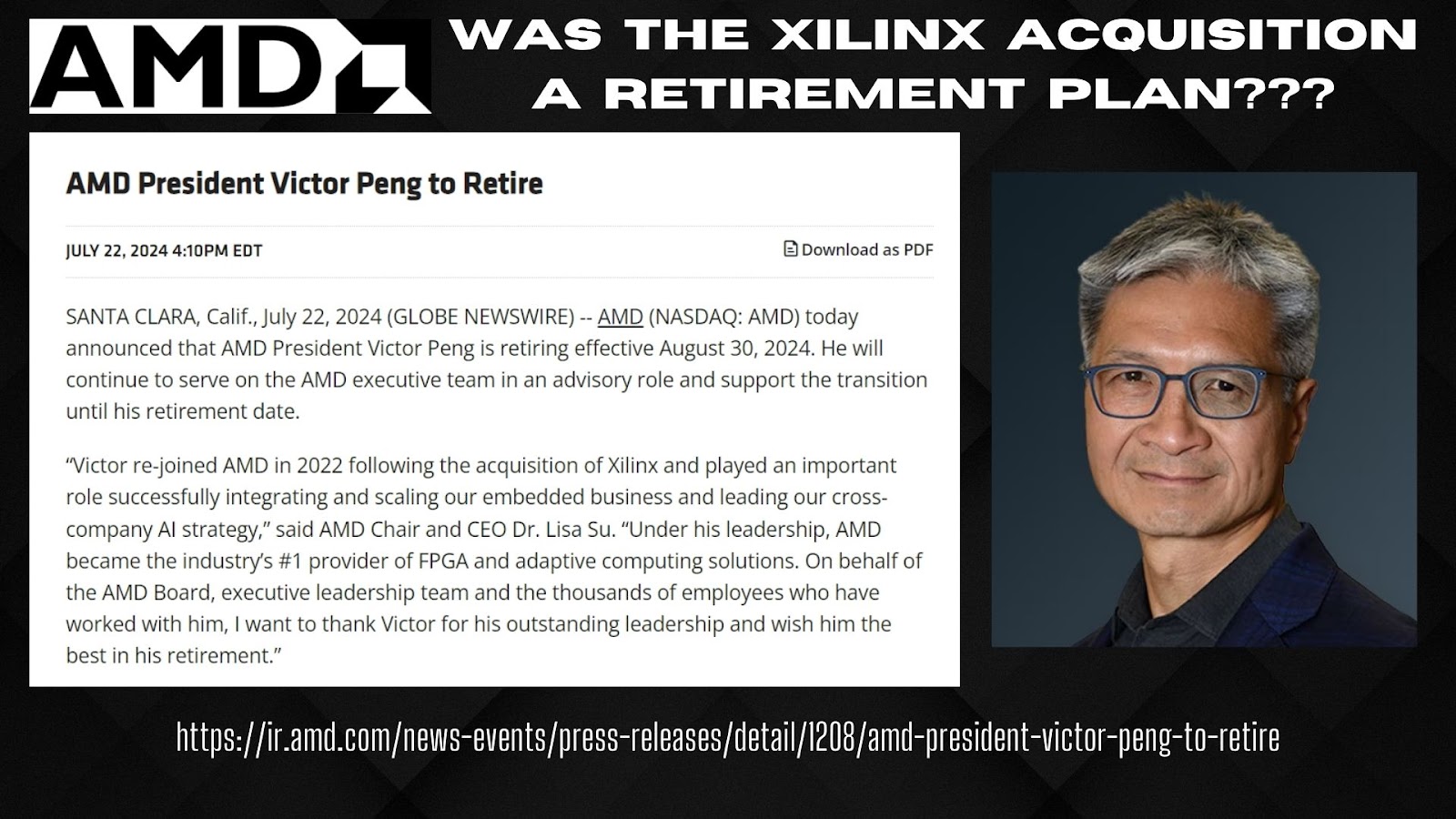

Just a quick side note on Embedded, former Xilinx co-founder and CEO Victor Peng, tasked with heading AMD’s AI endeavors – including the ROCm software suite to make AMD chips more comparable to Nvidia’s offerings – is retiring. Keep an eye on this management shake-up.

Mr. Peng, thank you for your fantastic work! Much of our current AMD stock position came via Xilinx when our shares in that company converted after the merger was completed a couple years ago. We were happy Xilinx shareholders!

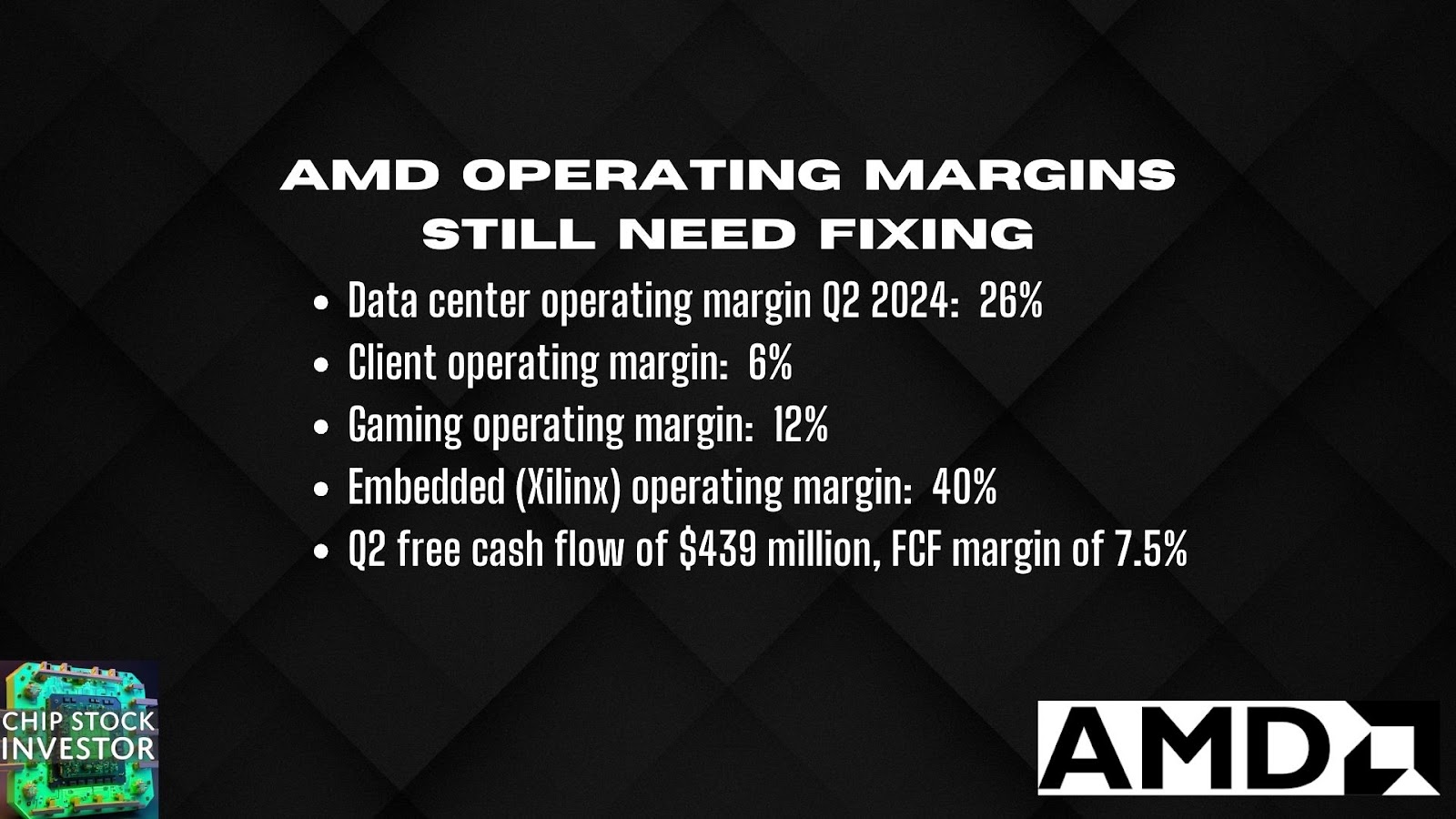

But back to AMD’s margin profile. Here’s another look at the performance in Q2, as well as the free cash flow (FCF) generation:

An unfair comparison

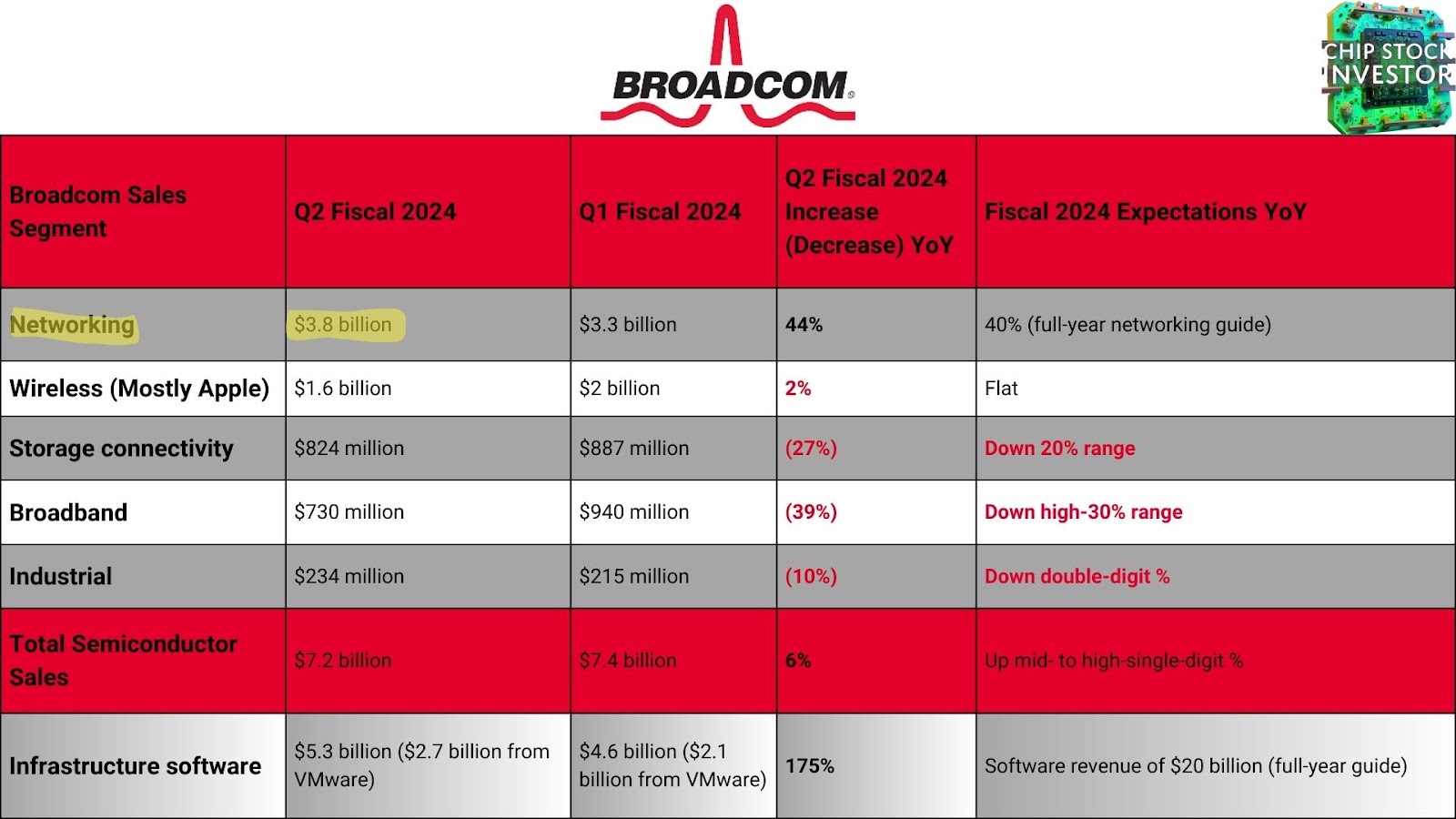

To help illustrate the work that still lays ahead of AMD, compare its data center segment revenue last quarter ($2.8 billion) to leaders Nvidia and Broadcom (which reports data center under “Networking”).

Remember, Broadcom is the company quietly behind custom silicon like Google’s TPU data center accelerators. AMD isn’t in second place in terms of data center revenue, it’s more like third – and that’s not even speaking to the disparity in profit margin profile.

Check out our last video on Broadcom’s status as an AI infrastructure and software leader: Move Over Nvidia, There’s Another AI 10-For-1 Stock Split Happening – Is Broadcom Stock A Buy Now?

AMD still has good stuff going for it

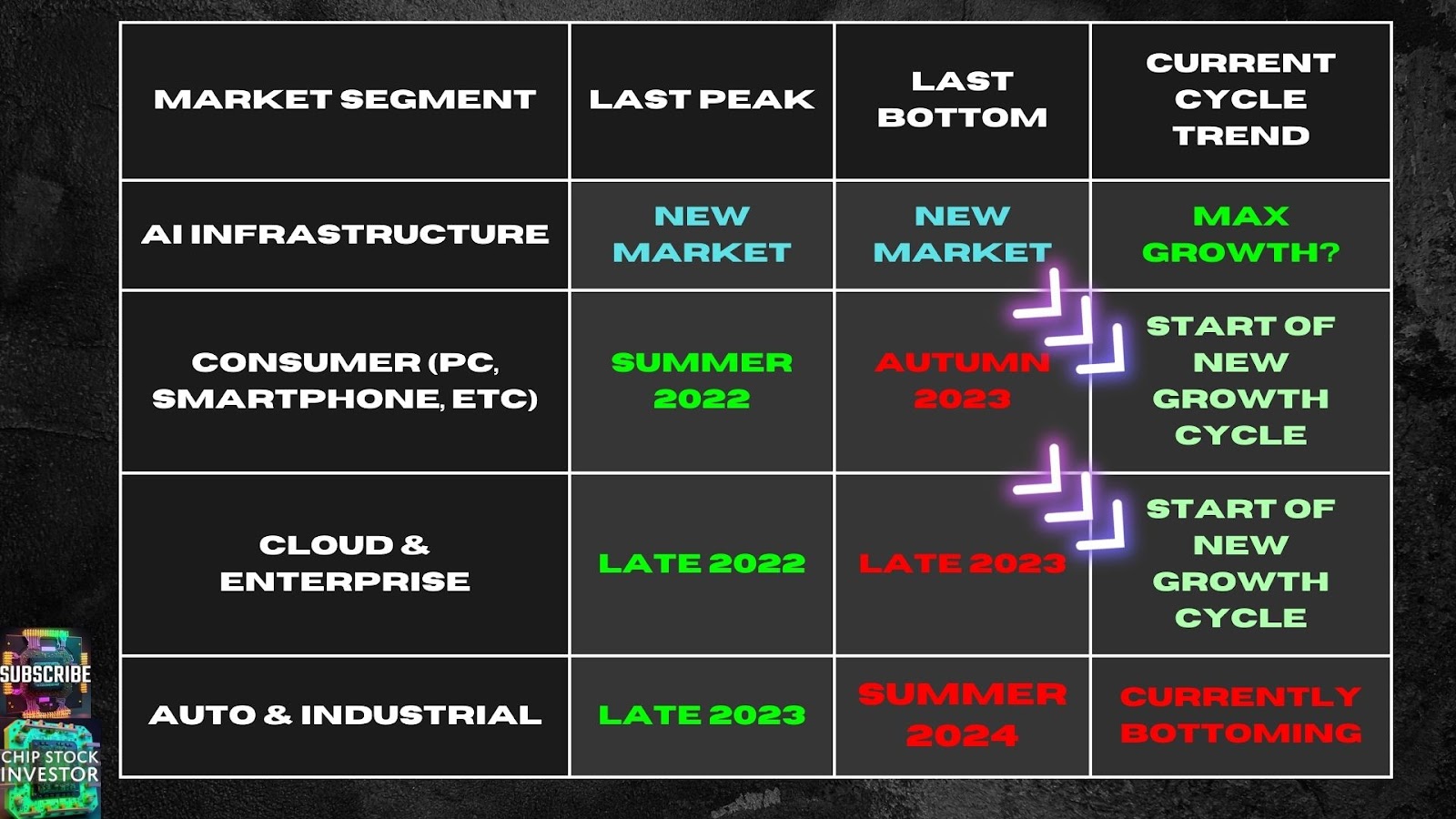

The good news is that AMD doesn’t need to rely just on data center and AI chip sales to drive profitability higher. As we’ve been discussing, the consumer and traditional enterprise compute markets have stabilized. Also see our last video on Onsemi (ON) and the possible bottoming in the auto and industrial market (which helps AMD Embedded/Xilinx, though it doesn’t compete with ON). The EV and Auto Chip Recovery Is Here – Time to Buy Top Semiconductor Stocks? Onsemi ON Stock

Higher sales should help with operating leverage (more revenue means more profit, and vice versa) for what are now AMD’s small Client and Gaming units. This operating leverage improvement is what will ultimately drive the volatile stock price higher over time.

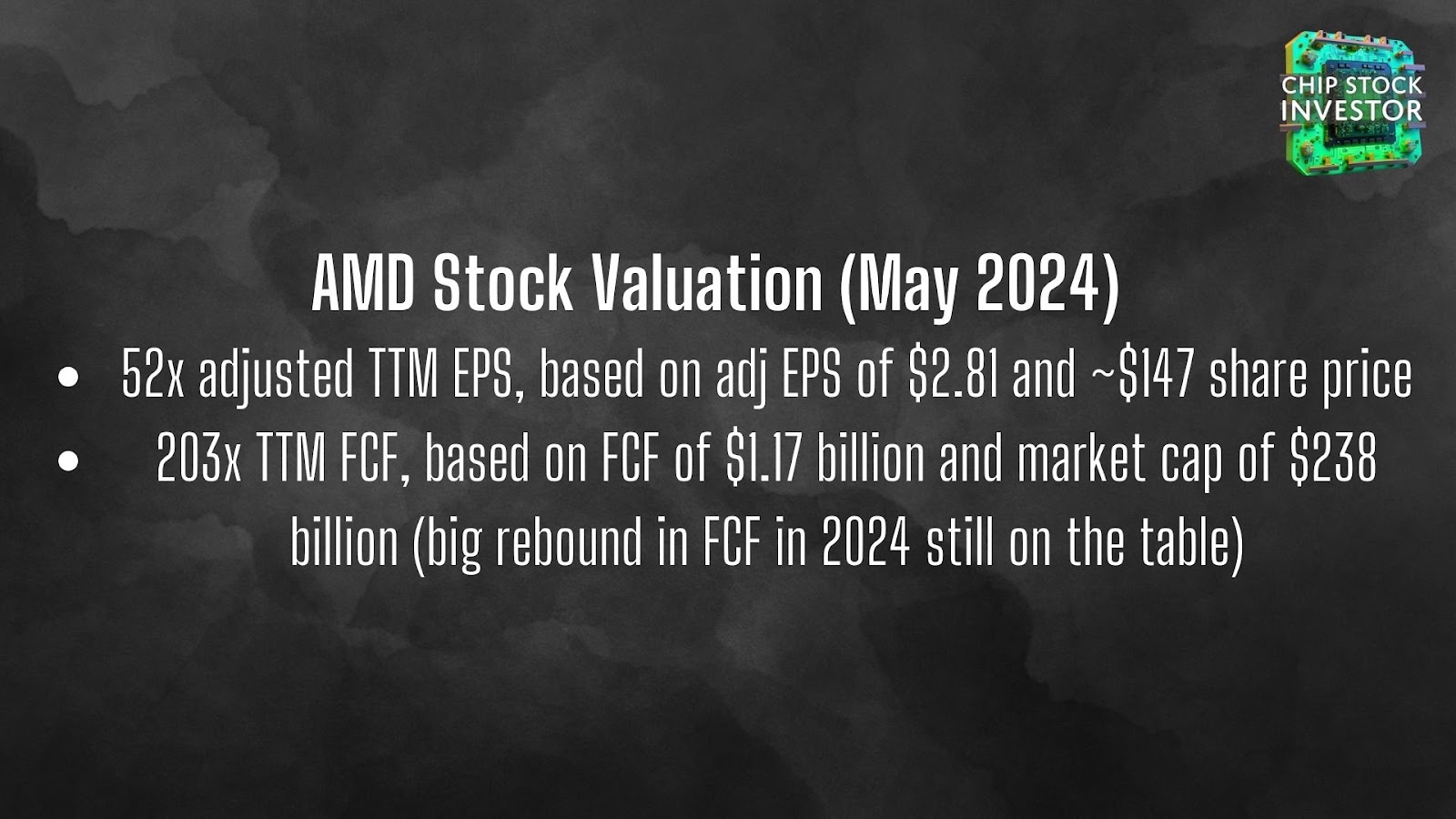

This is the same effect we called out for a few quarters now, and indeed, AMD’s CFO emphasized this point back in May. Here’s our last video on that, which is when we made the following slides (including the elevated looking valuation three months ago). Forget AI, This Is (Still) the Best Reason to Own AMD Stock

An update on AMD’s valuation

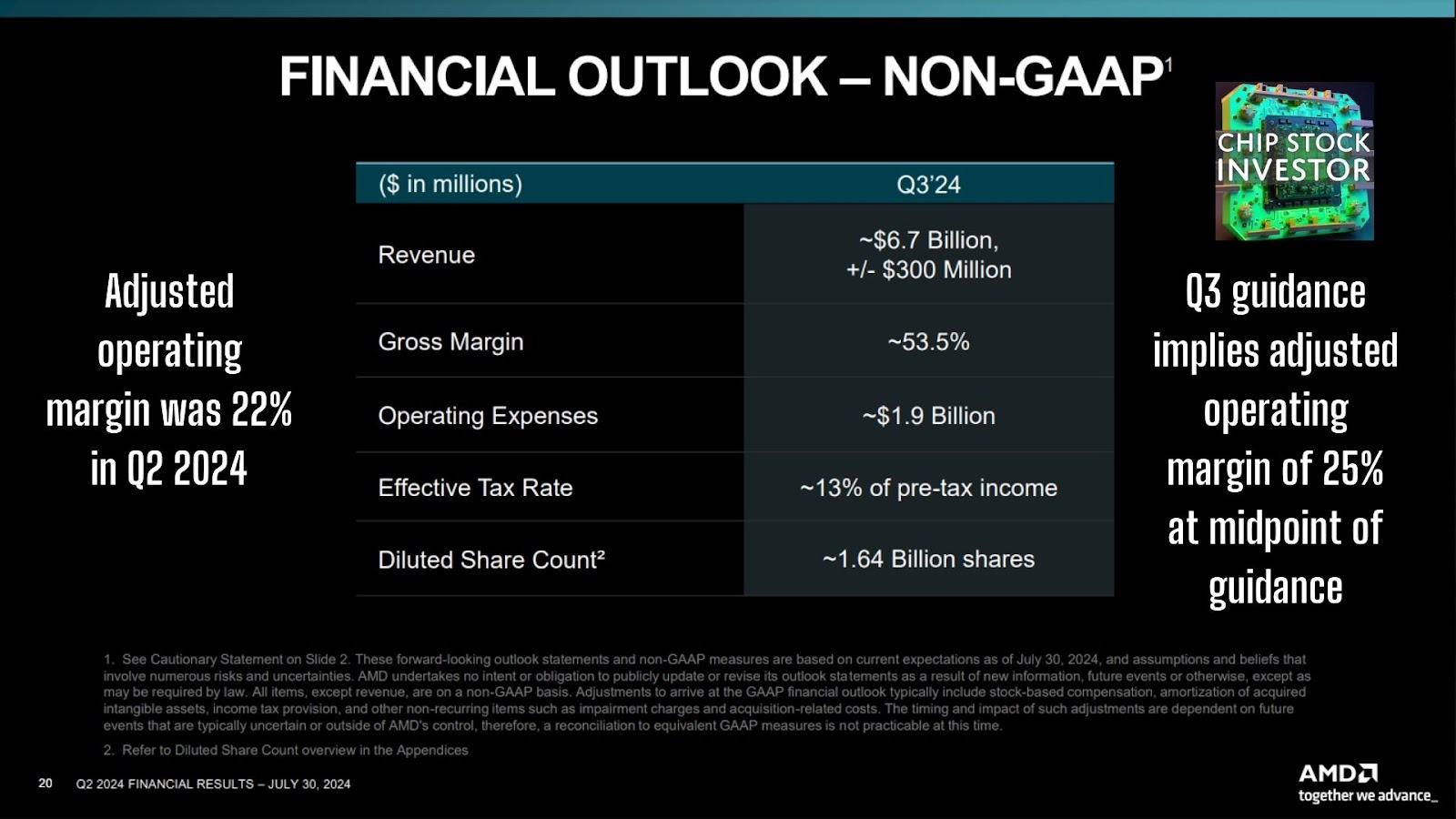

We are thus reiterating our outlook on what we need to see to justify AMD’s stock price today: Steady progress towards mid- to high-50% gross margins on product sold, and high-20% to mid-30% FCF and adjusted operating margins.

Based on the Q3 2024 guidance, AMD is continuing to make such progress.

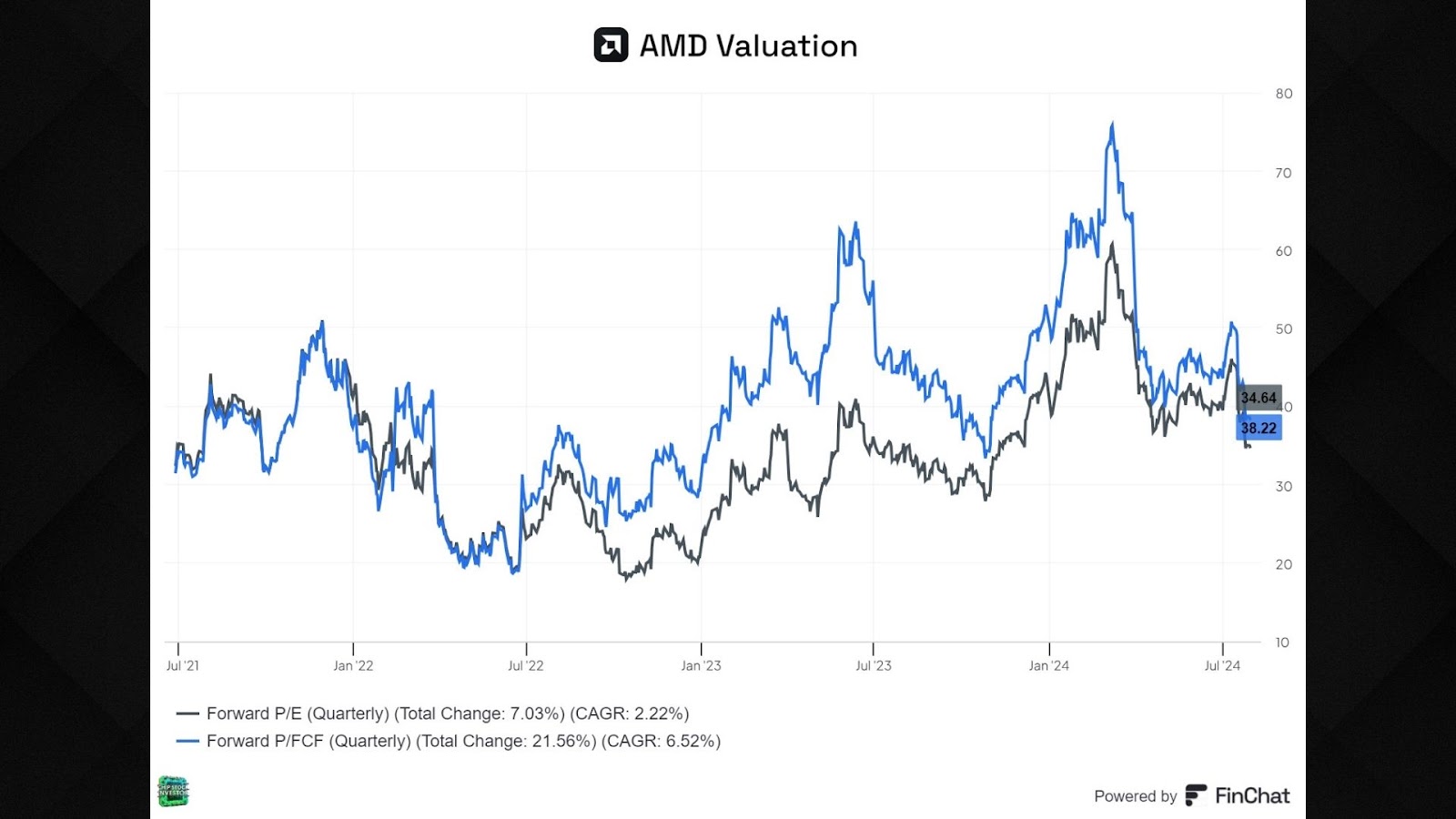

After the update, AMD stock now trades for about a mid-30x expected next-12-months earnings and FCF per share. This still seems about right for where AMD is at in the cycle.

We are happy to continue holding our position in AMD, but are not adding at this time. Especially with the chip stock and tech stock pullback in July, there are plenty of deals to be had. Nevertheless, if AMD can keep cranking out higher margins (AI will help, but it’s not the real story as this is not Nvidia), we’re happy to remain shareholders.