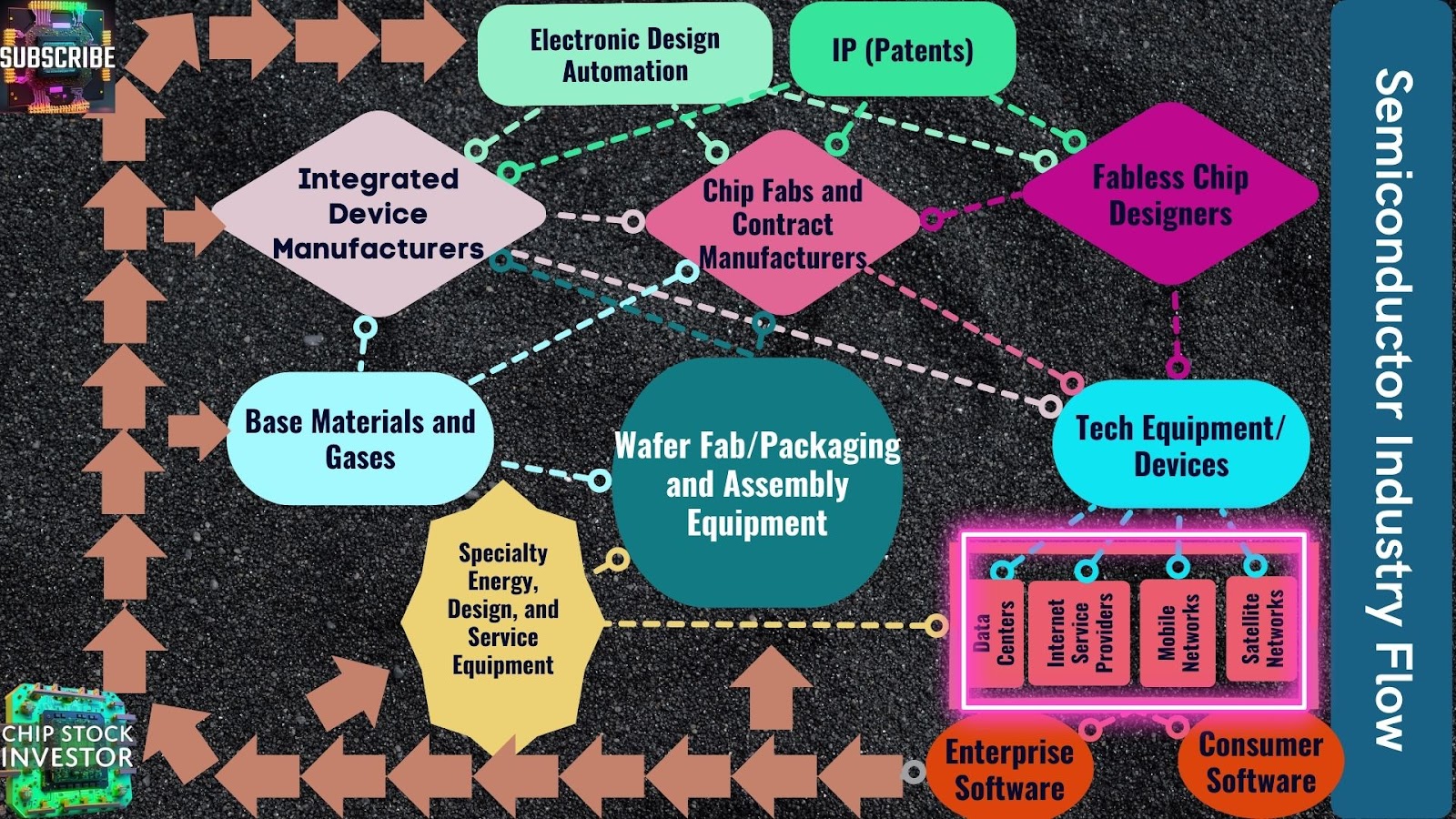

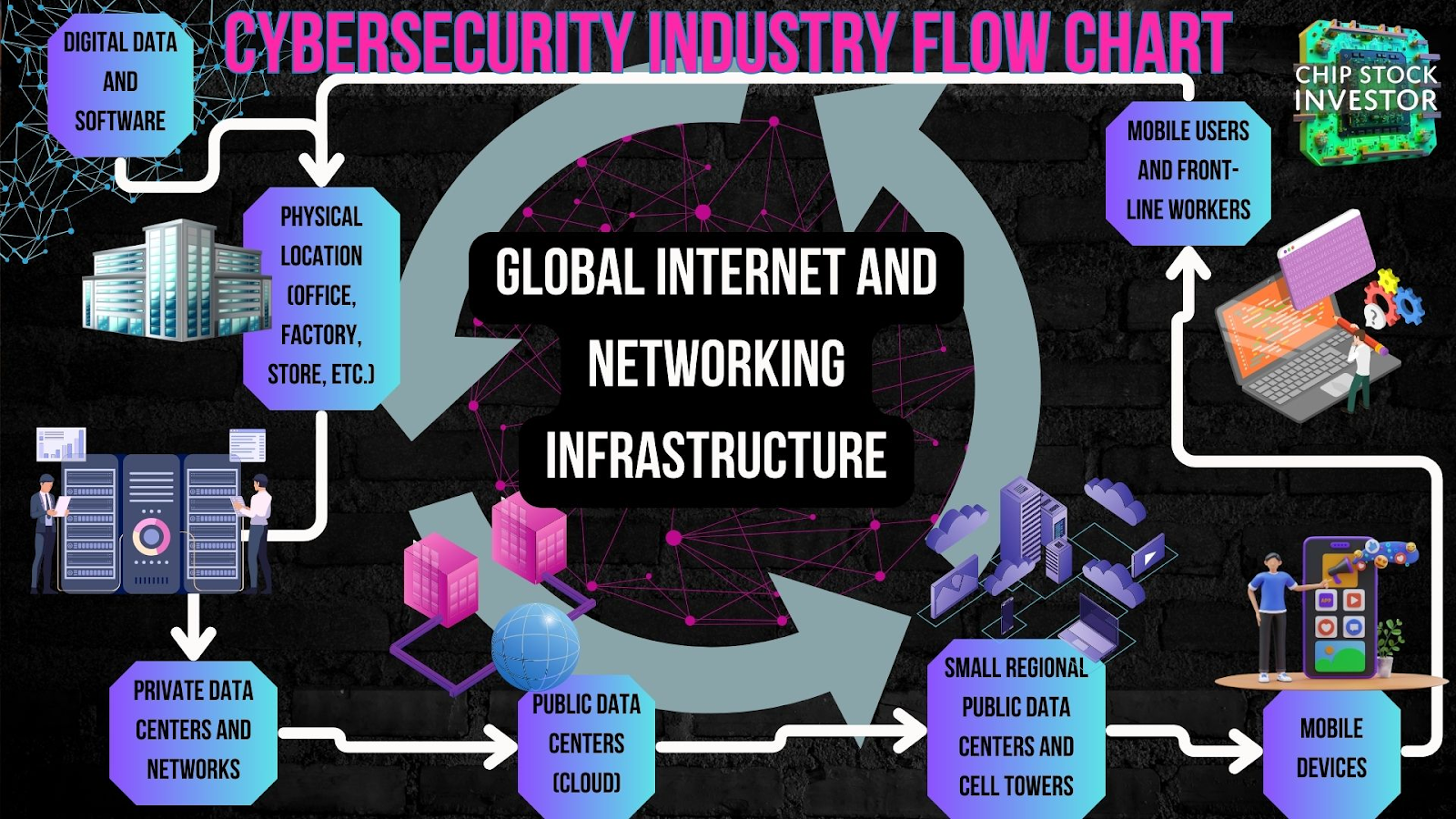

Let’s talk about the internet and global IT infrastructure. It’s a complicated mess. The globe is criss-crossed with undersea and subterranean cables, connecting regional and major data center hubs, businesses, and consumers. It’s the bottom right box we illustrate in our Semiconductor Industry Flow chart, the behind-the-scenes network that powers all the devices we rely on every day.

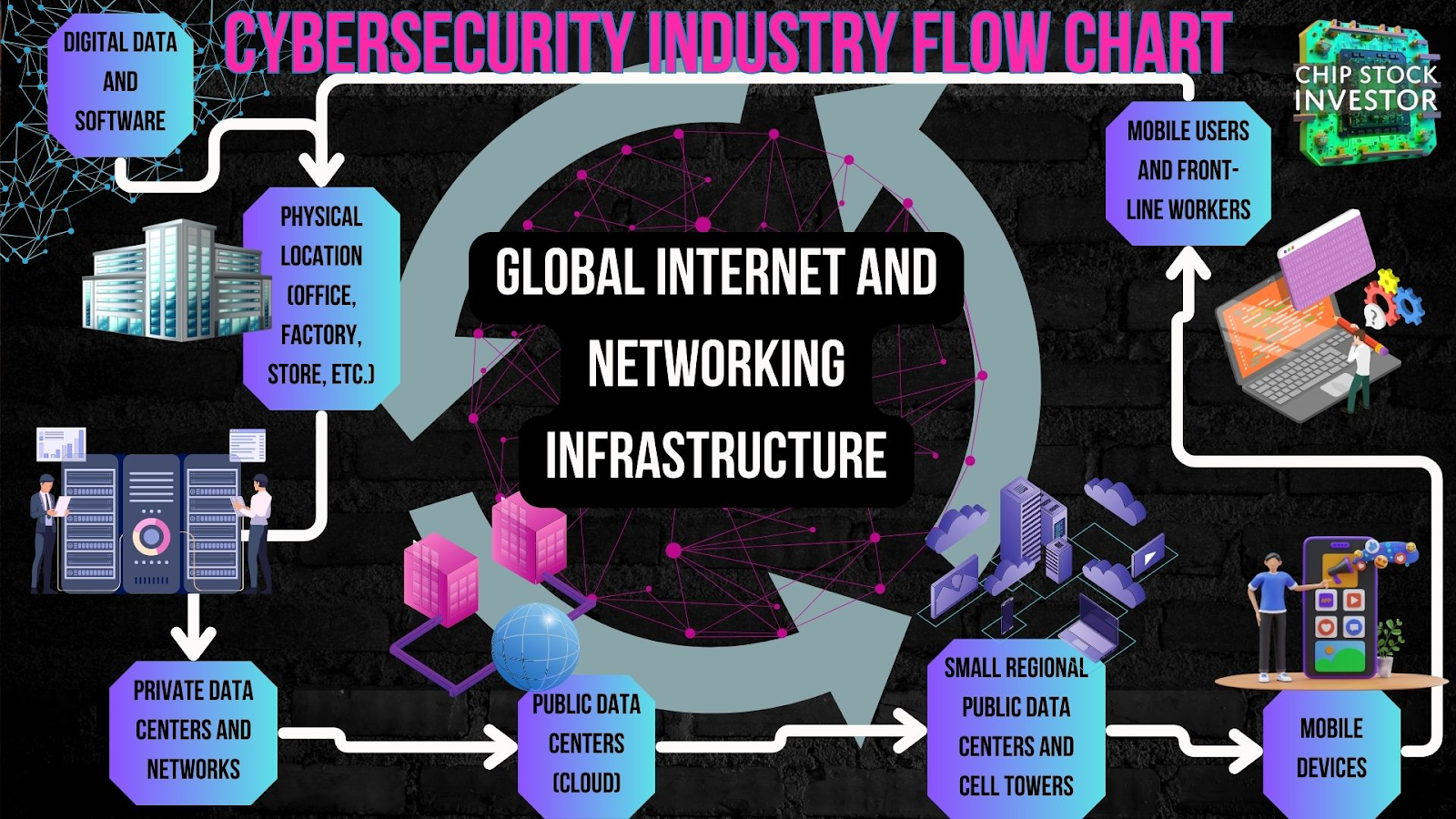

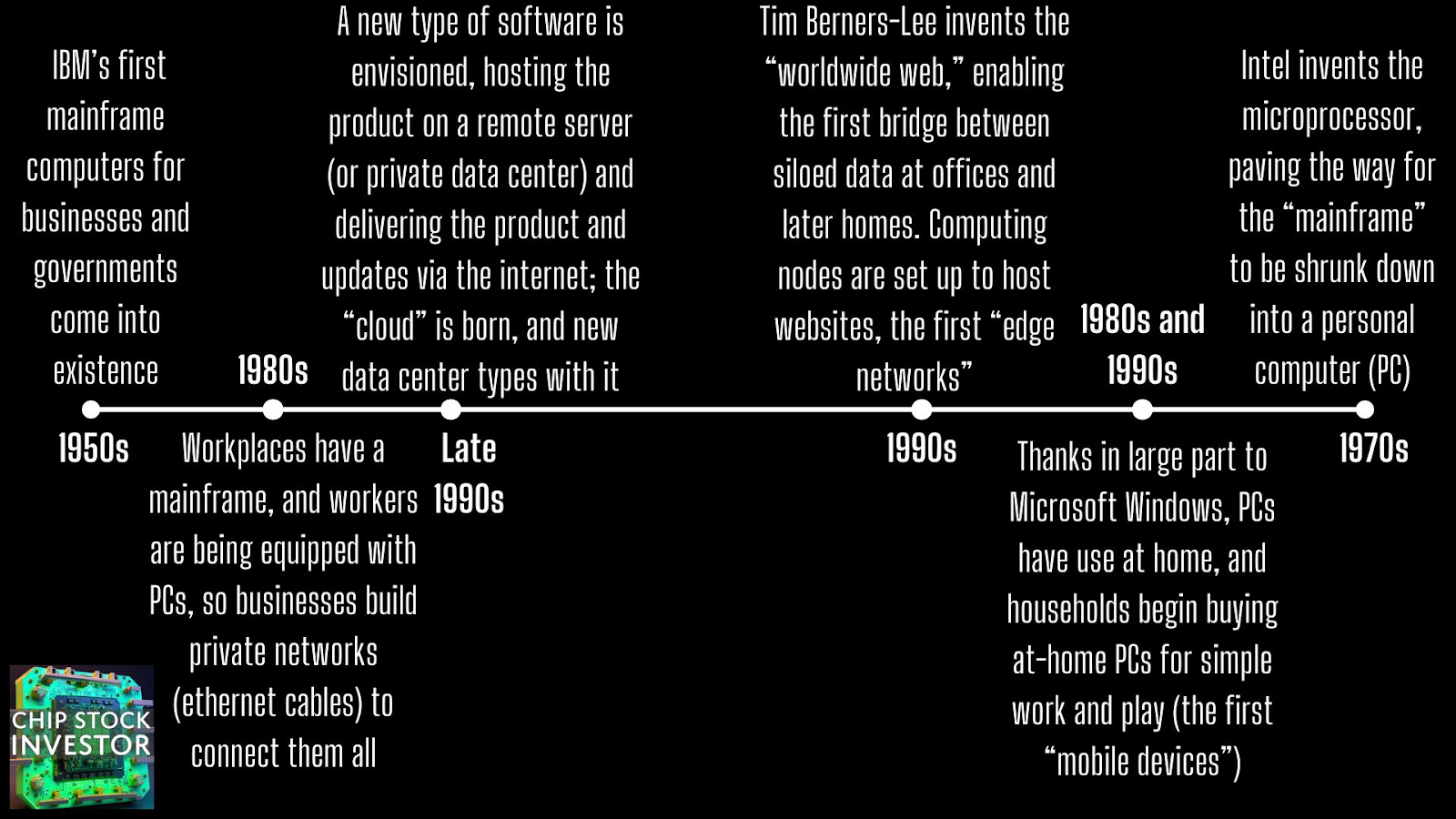

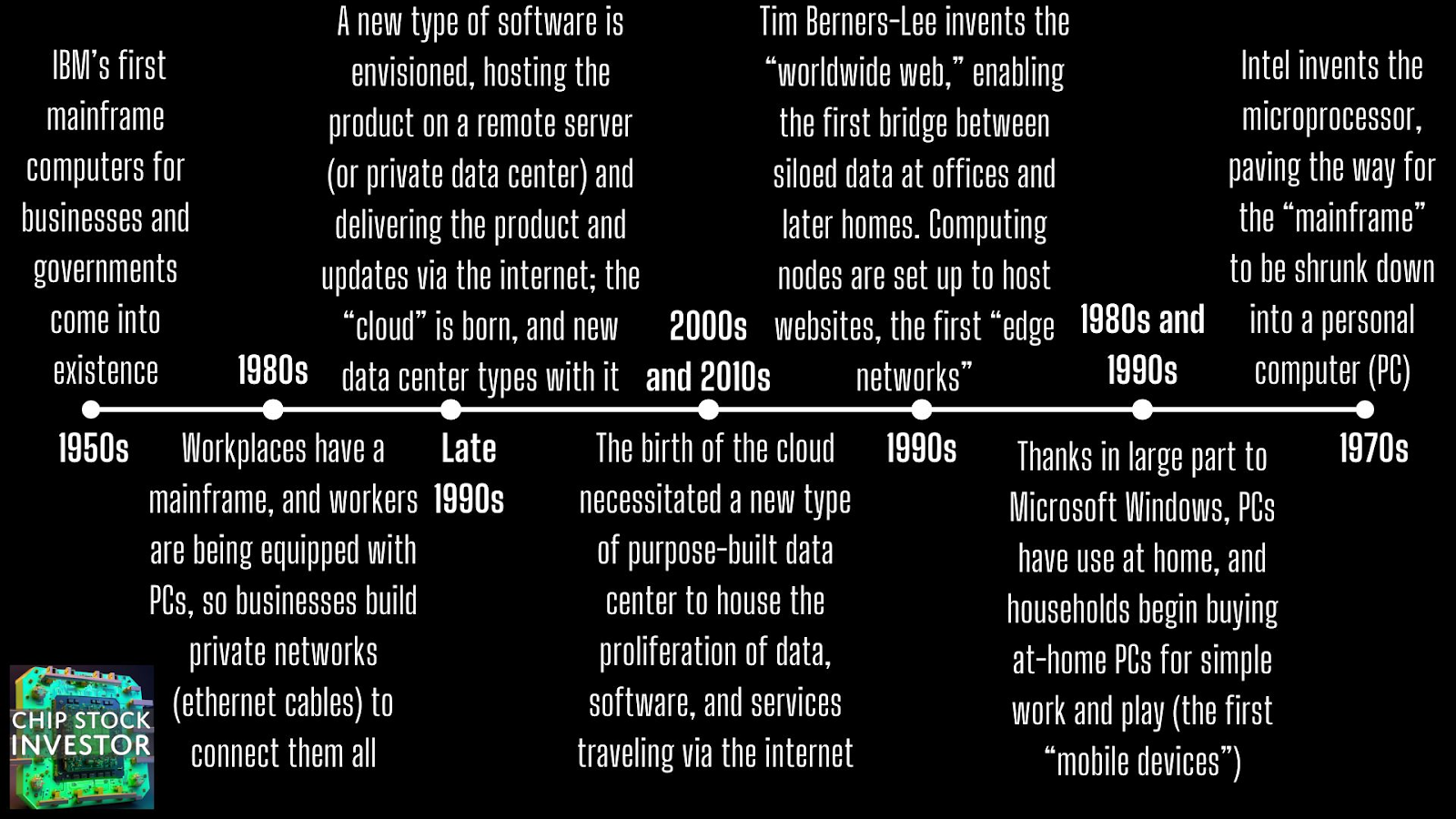

This is where Akamai (NASDAQ:AKAM) and Cloudflare (NYSE:NET) fit into the global IT industry. But before we jump in, let’s build a timeline. But maybe not just any old timeline. I thought we’d build out a linear representation of the “Flow Chart” Kasey made for the Cybersecurity Industry a few months ago. Here’s what it looks like today, the IT and internet (digital economy) infrastructure, and how data moves around it.

Charting IT and internet infrastructure buildout up to the AI era

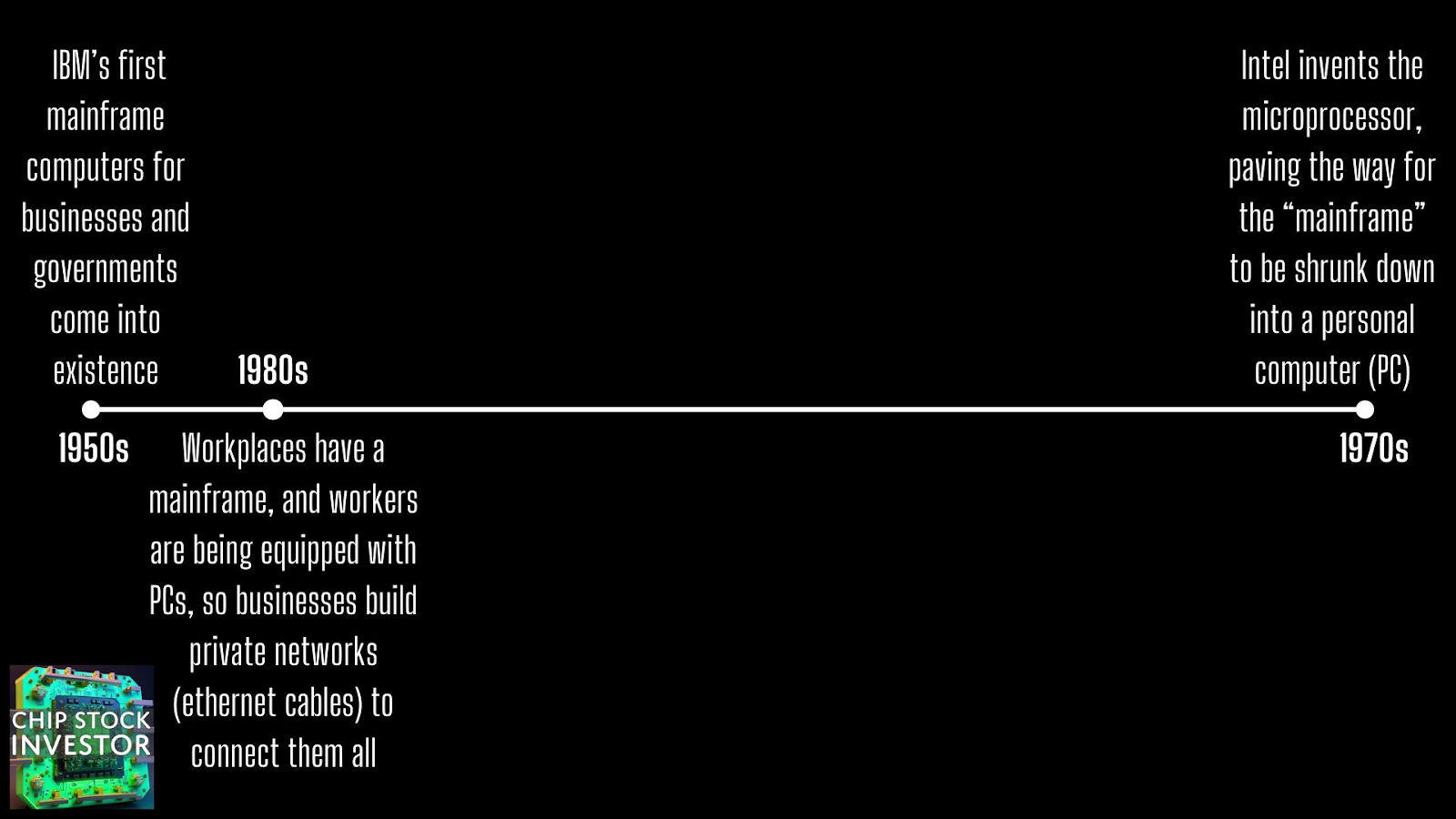

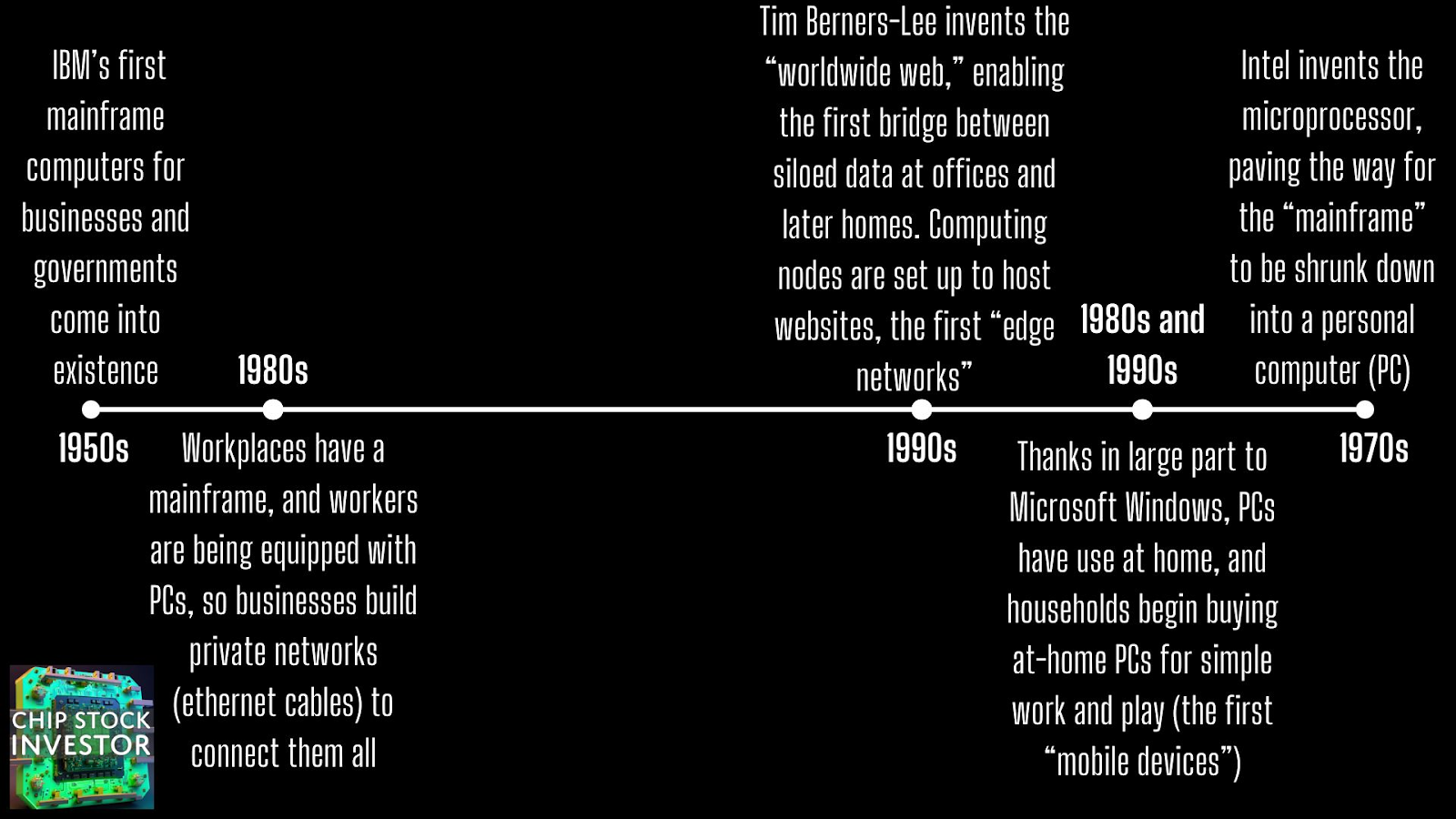

But how did we get here? Well, in the beginning, there were big business computers, mainframes (like what IBM made/still makes) in the 1950s.

We’re now going to flatten our flow chart into a straight line, but keep the positioning of the infrastructure in place with a date of its arrival onto the global scene. So, “digital data” and “physical locations/offices” start first on the left, which got their start in the 1950s.

After a couple decades of R&D into the nascent world of semiconductors, a little business known as Intel had a breakthrough and was first to invent/commercialize the microprocessor. Suddenly, big mainframes could be shrunk down into a personal computer (PC) that individuals could use at a desk. The first “front-line digital worker” was born.

Not long after the invention of the PC, a way to connect all of them inside the workplace and to the office mainframe needed to be devised. Ethernet was thus invented as an open connectivity standard in 1973. The first “private networks” were created not long after, a big trend as PC adoption picked up pace in the late 1970s and 1980s.

Suddenly, digital data was getting to be a phenomenal business and organizational breakthrough. There was only one problem. The data was siloed in individual locations: office mainframes and PCs. How could those silos be broken down so that data could be shared between remote locations? Tim Berners-Lee, a researcher at CERN, invented the worldwide web (WWW) in 1989. In the ensuing years, the internet would get commercialized, and internet service providers would pop up around the globe to help interconnect business data, and later on, make it a consumer product for people to use at home. This necessitated the creation of the first “edge networks” (remember that buzz phrase a few years ago?), data storage computing nodes (data centers) located close to end-users.

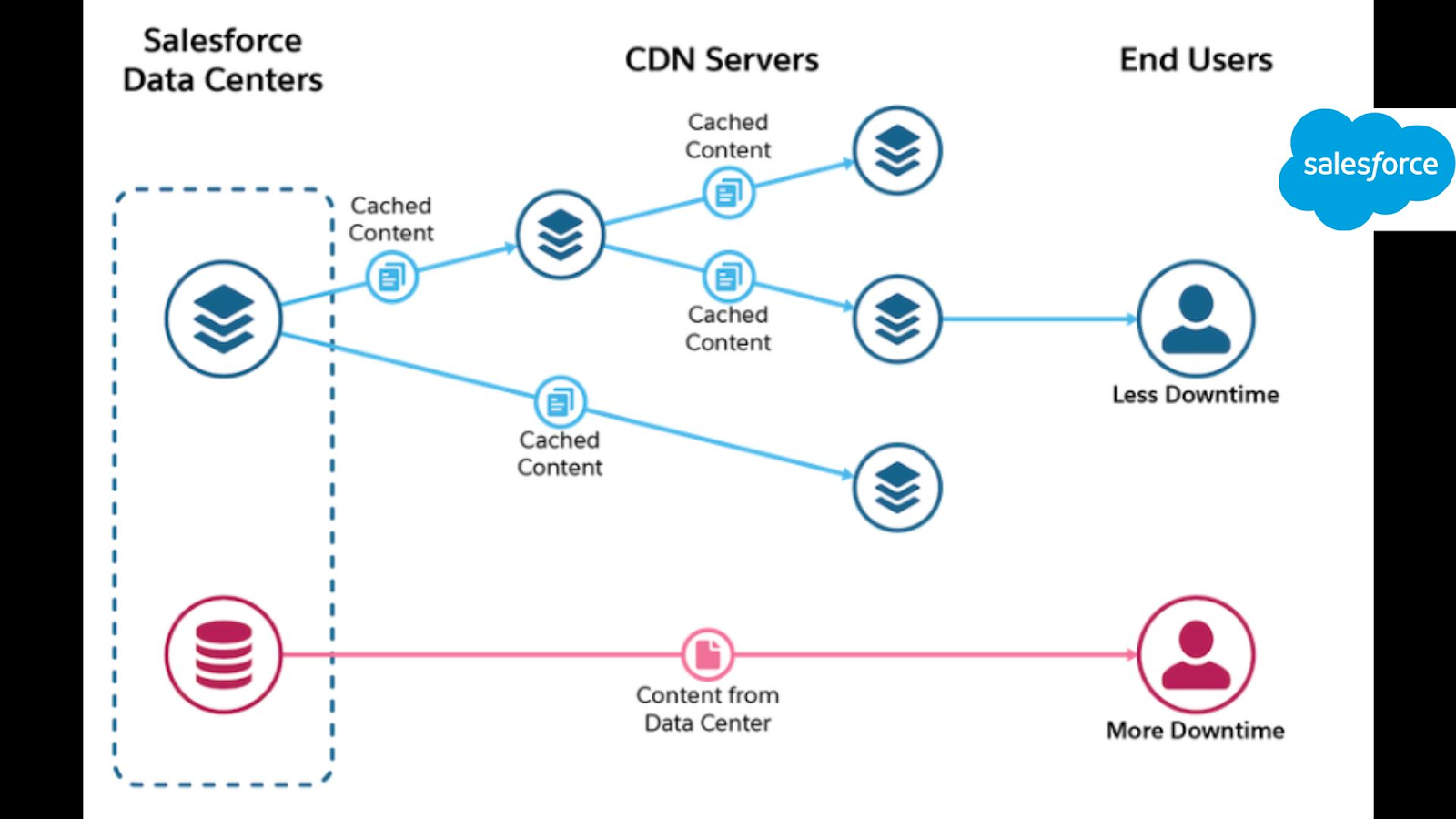

It’s at this point in time, 1999, that Akamai is founded, the first “content delivery network,” or CDN — a business purpose-built to help consistently and securely deliver internet data to web users. Not only was Akamai the first CDN, it still facilitates by some estimates the majority of global web traffic via its network of regional data centers and many miles of fiber-optic cable.

Also at this time, a boisterous and obnoxious executive at old mainframe database software company Oracle named Marc Benioff helps pioneer a new type of software, products hosted in a remote data center and delivered (along with continuous updates) via the internet. The “cloud” is born. Few realize it, but a new type of data center will be needed. The simple CDN that delivers static websites is almost dead on arrival. Legacy IT networks built to handle simple voice, messages, and text-based data are also going to get their last leg of growth before flatlining, then beginning a slow death spiral (at least, as far as a viable investment goes).

For our purposes here, let’s now skip the dot-com bubble, an economic event.

The development of internet-delivered software (later known as the cloud, and hosted data centers for rent that Amazon Web Services pioneered) is what leads to the eventual Mark Andreesen quote that “software is eating the world.” While meant to be a statement of how software is transforming business as we knew it, in all actuality the quote is quite literal. The explosion of data traveling via the web quickly overwhelms CDNs like Akamai. More high-powered infrastructure built with more advanced chips is needed. It led to a proliferation of CDN services, and prescient companies (what we now call the tech giants, including Google) recognized early on that the CDN business model was merely a commodity, a piece of infrastructure to own and control, with real monetization taking place via software, ads on content itself, etc.

Which brings us to the final cog in the “global internet infrastructure,” the middle of the Flow Chart, and really one of the last pieces of IT infrastructure to be built (up to the current new AI data centers being built today).

Content delivery has become a commodity

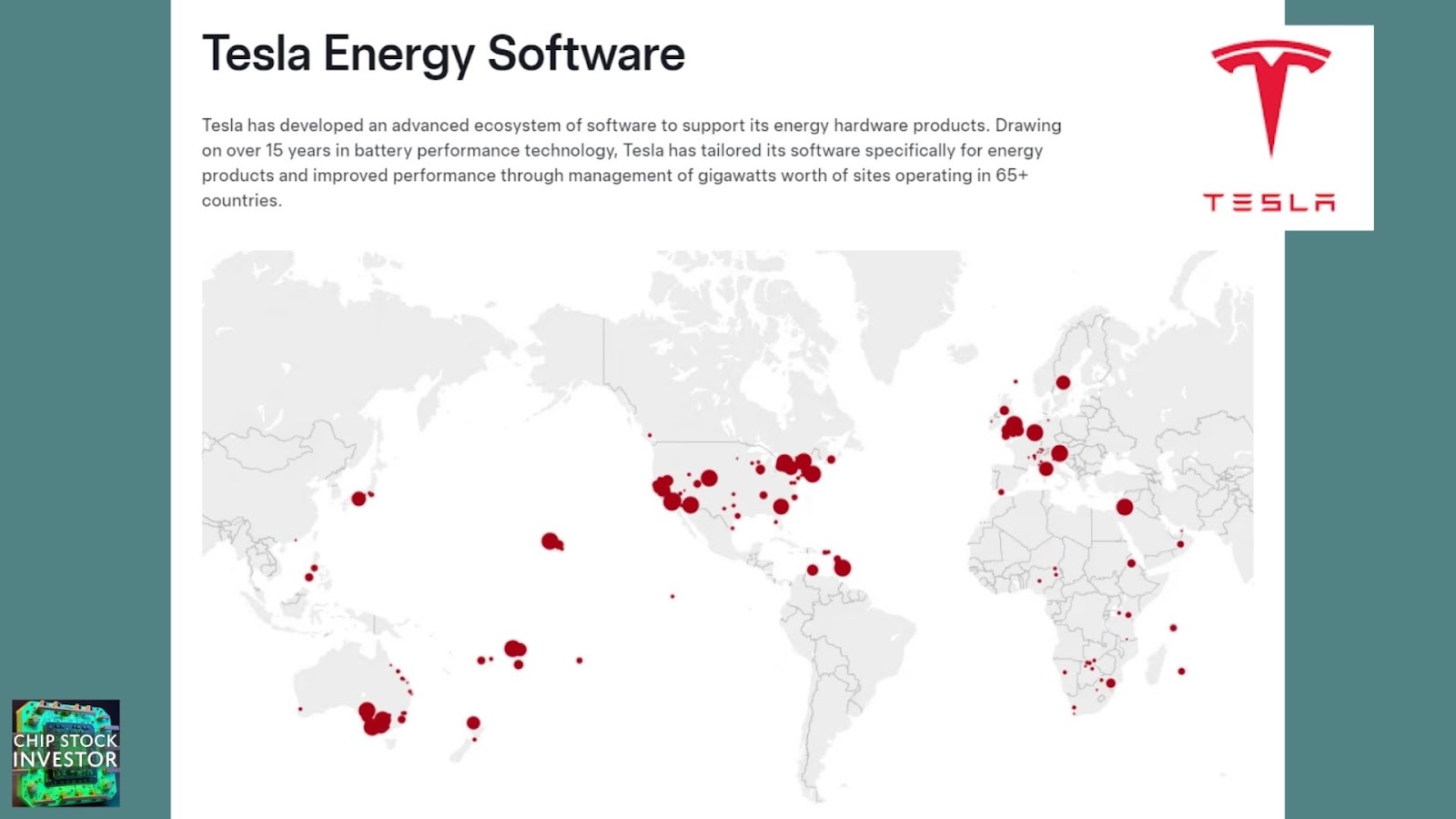

These days, the tech giants continue to gobble up data using various types of “content” delivery networks. Nvidia put a spin on it with its Graphics Delivery Network handling 3D and high-end graphics content. And Tesla, one could argue, is building a “power” delivery network with its software installed in data centers around the globe.

Which now begs the question: With regional data centers (edge networks) and IT infrastructure getting commoditized — the middle section squeezed on one end by chip companies charging ever-higher prices for ever-higher performance hardware, and squeezed at the other by software and big internet service provider customers demanding infrastructure providers facilitate ever-more data at lower prices — how did we get to this point where a company like Cloudflare, Fastly, and others would ever dream of “disrupting” a legacy business like Akamai? After all, it’s not like the original CDN is sitting atop some sort of financial empire.

A note on how a CDN works, and why rising data demands are a constant burden

Let’s use a brand name business, Domino’s Pizza. Back in the day, the internet allowed you to look at a menu, look up a phone number, call to place an order, and tell them your address for delivery. The legacy CDN helped host the website that got you the info you needed.

But with the advent of the cloud, the amount of data, and thus the value of the next-gen CDN shot higher. Now when you visit the Domino’s Pizza site, you can look at the menu and review dynamic offers, place the order and pay directly online, and have Domino’s save all of your personal info for later (if you want, but they’re gathering some basic data on you anyways via cookies), and your address from your digital payment provider can automatically be ported over so the driver knows where to make the delivery.

Which CDN requires more data bandwidth? And which CDN provider can thus charge the bigger premium? The newer cloud CDN, of course.

Managing the internet presents a financial challenge

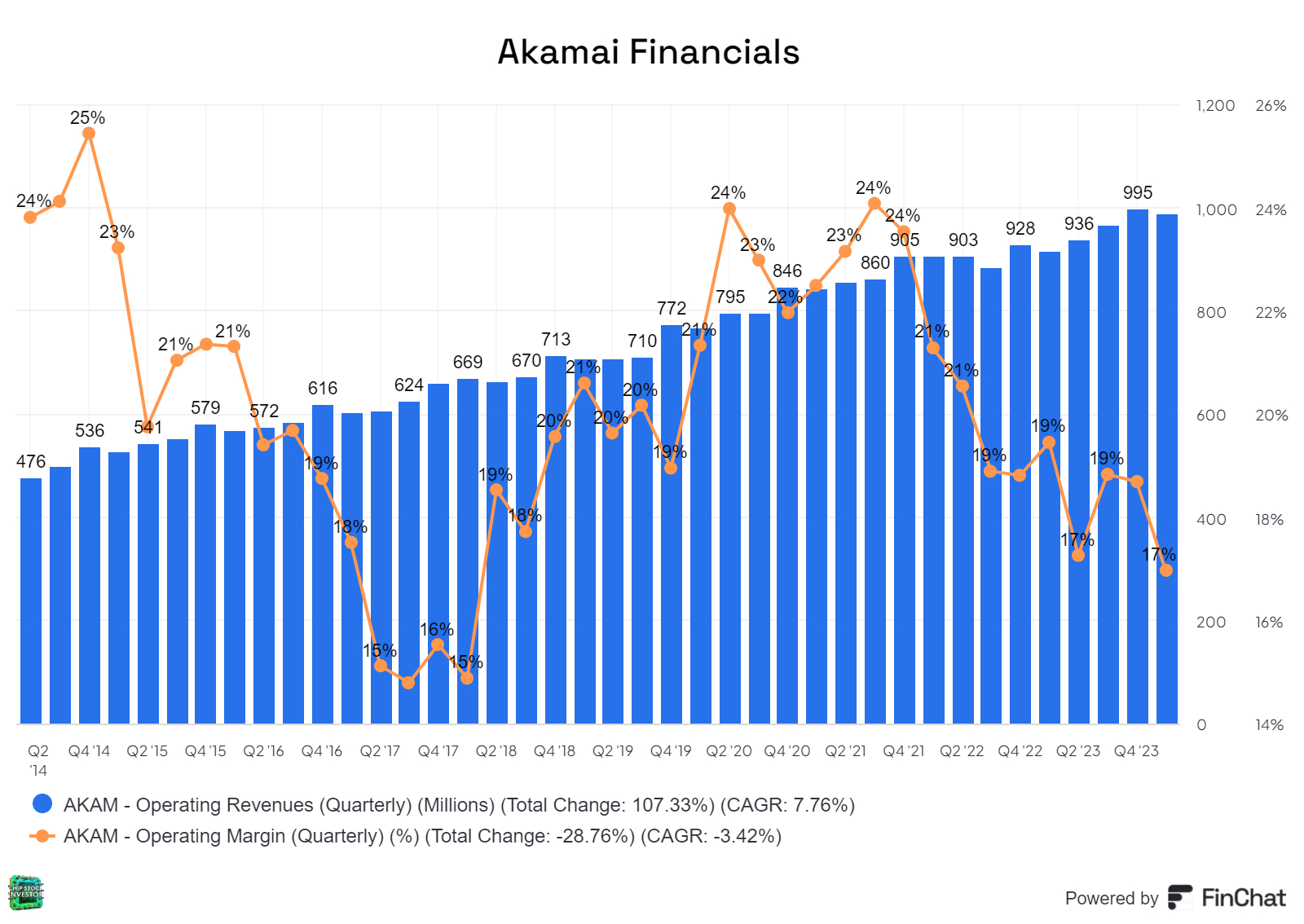

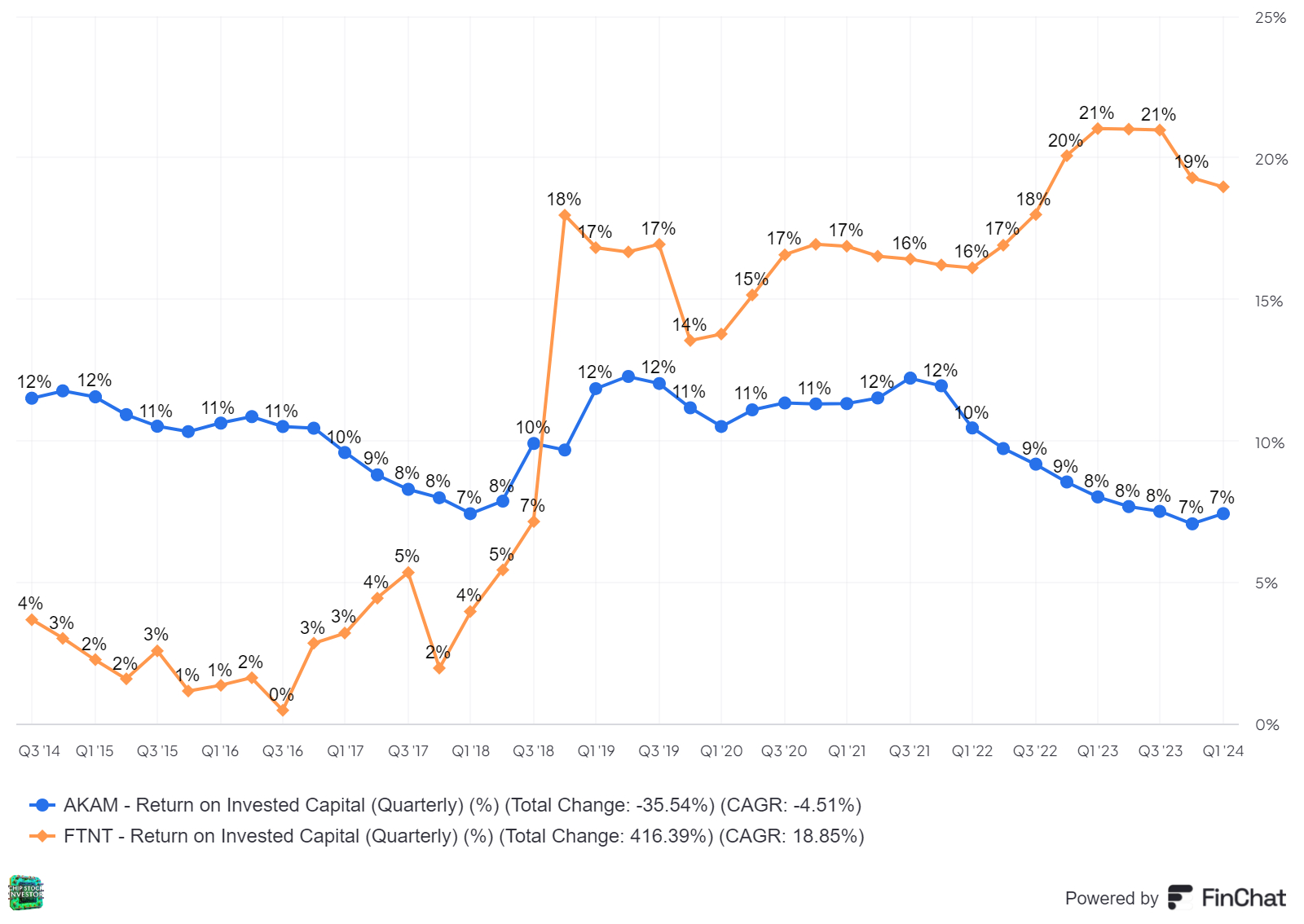

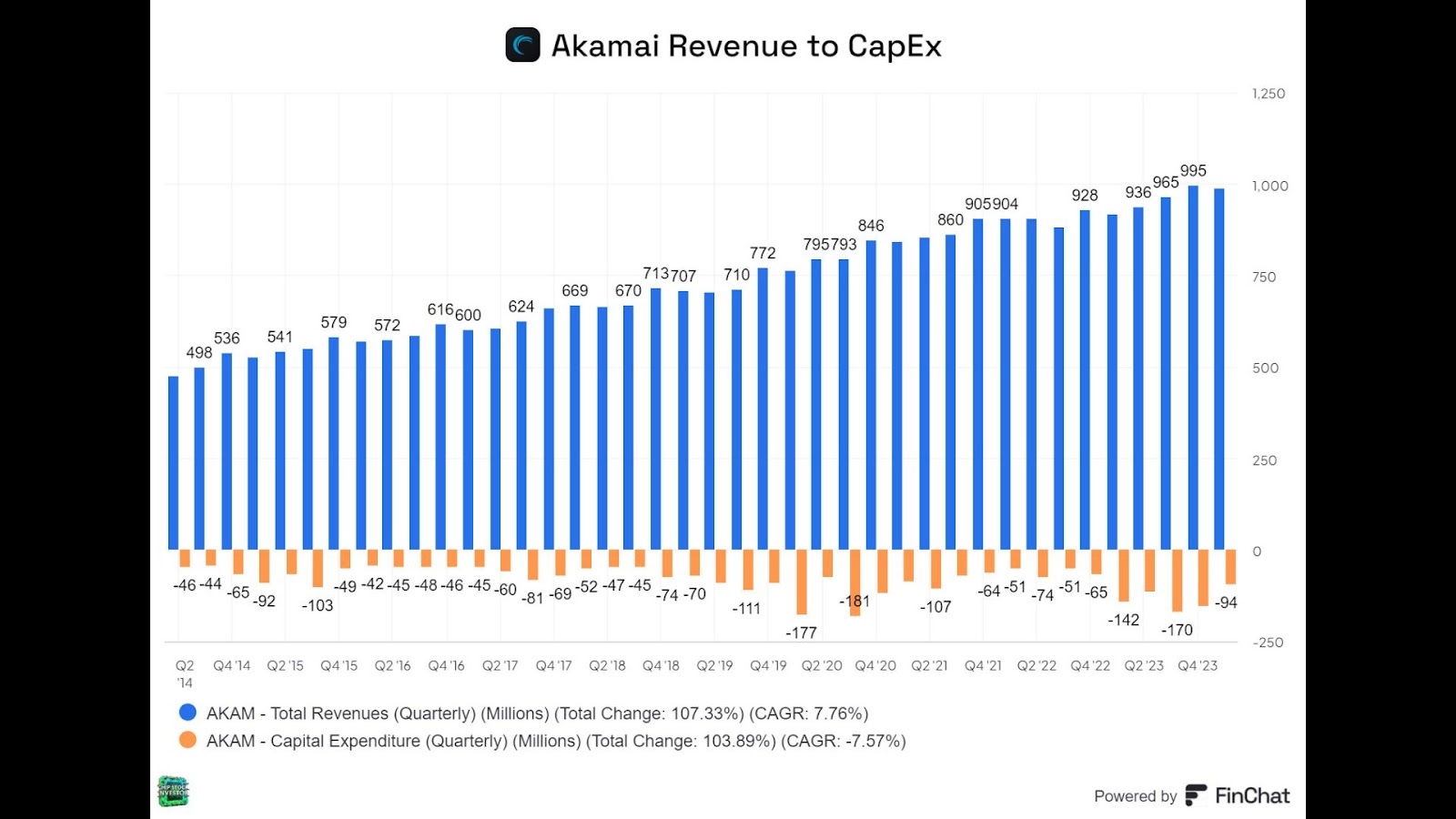

This following Akamai financials chart reflects numerous acquisitions made over the years to help it stay in growth mode.

Infrastructure businesses like Akamai (and other comms infrastructure, including Verizon, AT&T, Vodafone, etc.) have been in a pickle — from an investment POV — for a long time. Now, knowing that the cloud titans (Amazon, Google, Meta, etc.) are also a type of infrastructure business, how did they crack the code? As we frequently say, we love businesses that do both hardware (infrastructure) and software.

There are a lot of terms floating around for this combo: Software defined networks, serverless computing, platformization, full-stack computing, etc. At the end of the day, though, the idea is to combine the defensive moat of hardware (it’s expensive to build and maintain infrastructure of some sort) with the differentiation and scalability of software (pick you end market, from cybersecurity to e-commerce).

It’s often talked about that new technologists have a first mover advantage. Akamai, as an early entrant to the CDN space during the early days of the internet and the cloud (internet delivered software), is exactly the opposite: It had a first-mover disadvantage. It helped pioneer what publicly shared (infrastructure available for rent) internet infrastructure looked like, but the cloud giants went on to prove the real money-making ability was building a full software stack atop that infrastructure. Since coming to this realization, Akamai has been in a constant frenzy to acquire software to add to its very extensive (if not the most extensive, most widely distributed) edge network data centers.

For example, early this year, it announced the acquisition of another cybersecurity startup called Noname, which helps secure APIs. https://www.akamai.com/newsroom/press-release/akamai-announces-intent-to-acquire-api-security-company-noname

And in 2022, it spent $900 million to acquire Linode, turning its data centers into hubs for web developers (in a way, like Cloudflare Workers platform). https://www.akamai.com/newsroom/press-release/akamai-completes-acquisition-of-linode

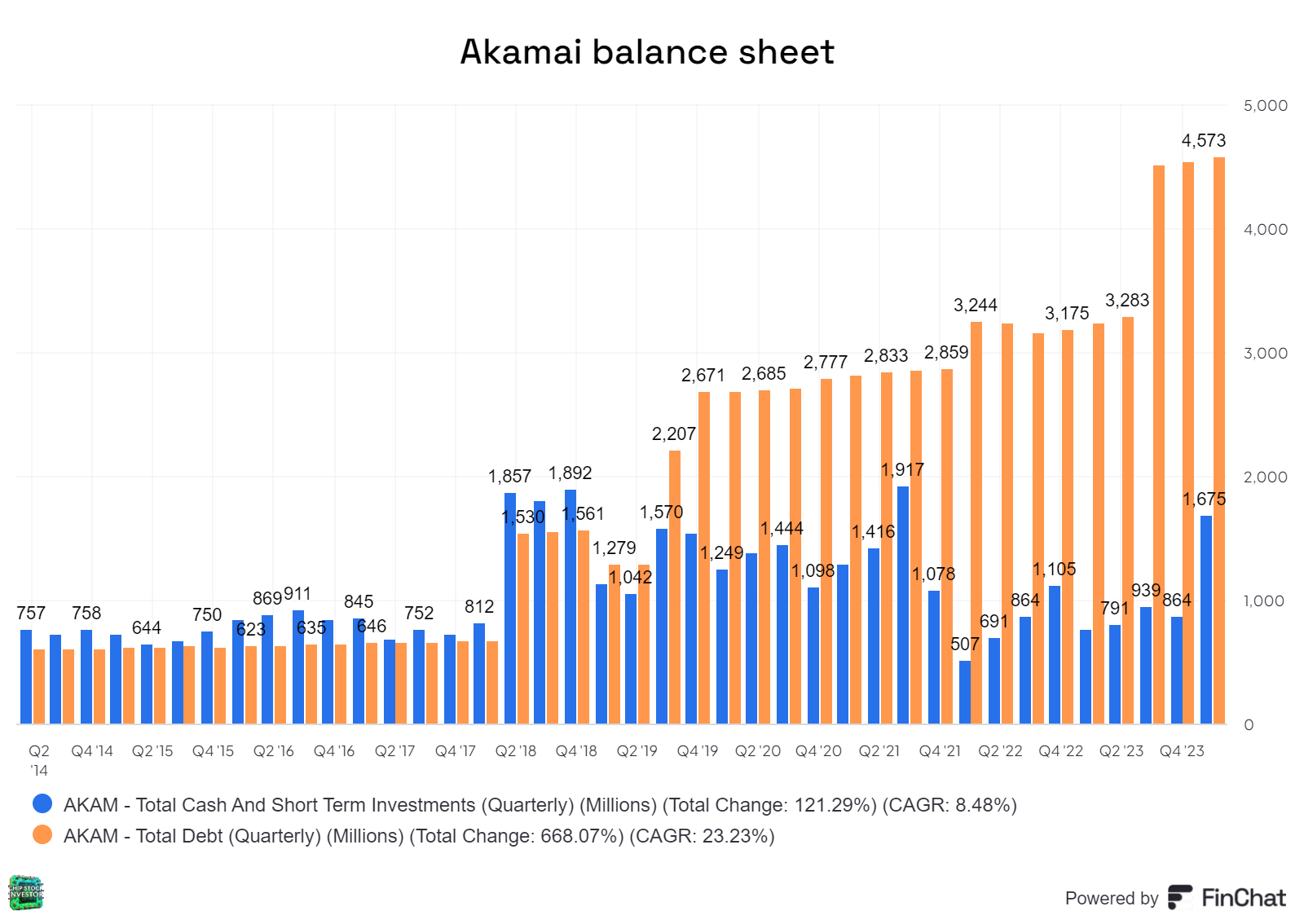

The downside is, it’s been a little late to the party. Constant purchases have left the balance sheet inverted with more debt than cash, and operating profit margins in steady decline for years as more nimble infrastructure with heavier software service offerings (Cloudflare) have entered the fray.

What’s really bad about this is it makes Akamai look like a mini version of the old telecom giants, again like Verizon, AT&T, Vodafone, etc. And to make matters worse, bolting on software of some sort to existing infrastructure that may or may not have been optimized for that workload can be extremely difficult. For example, take Verizon’s push into media during the 2010s. It took us some time to come to this realization, but the reason the purchase of AOL and Yahoo! was doomed to failure (among other reasons) was that the Verizon infrastructure (mobile networks) were never built to handle media. Put another way, it was just a bad fit. It was a colossal waste of shareholder capital in the end. Here’s a write-up Nick did all the way back in 2018 as I was finally starting to realize how bad of a deal it all actually had been. https://www.fool.com/investing/2018/11/04/why-verizon-might-be-conceding-defeat-on-its-aol-a.aspx

So what’s this to Akamai? Well, acquisitions to be bolted onto old infrastructure can be problematic. So far, Akamai has made an ok living off of this model. And its CDN core is a perfect fit for various types of cybersecurity, as you all know by now, a very high-growth market given the highly fragmented nature of IT infrastructure, how disjointedly it was built, and how terribly bad non-tech businesses (which is to say, most businesses) are at securing the digital data they unintentionally created by adopting IT infrastructure in the first place.

But the preferred methodology is organic development, with small incremental acquisitions that can immediately be accretive to a company’s tech, and thus financials. That’s why, as an example, we like Fortinet so much. Purpose-built network hardware, unified OS for all the software services, and smaller purchases of startups that can easily be folded into what has already been built without much need to re-write code to match the installed hardware.

Akamai’s hodge-podge strategy, by contrast, shows up in the financials.

What about Cloudflare?

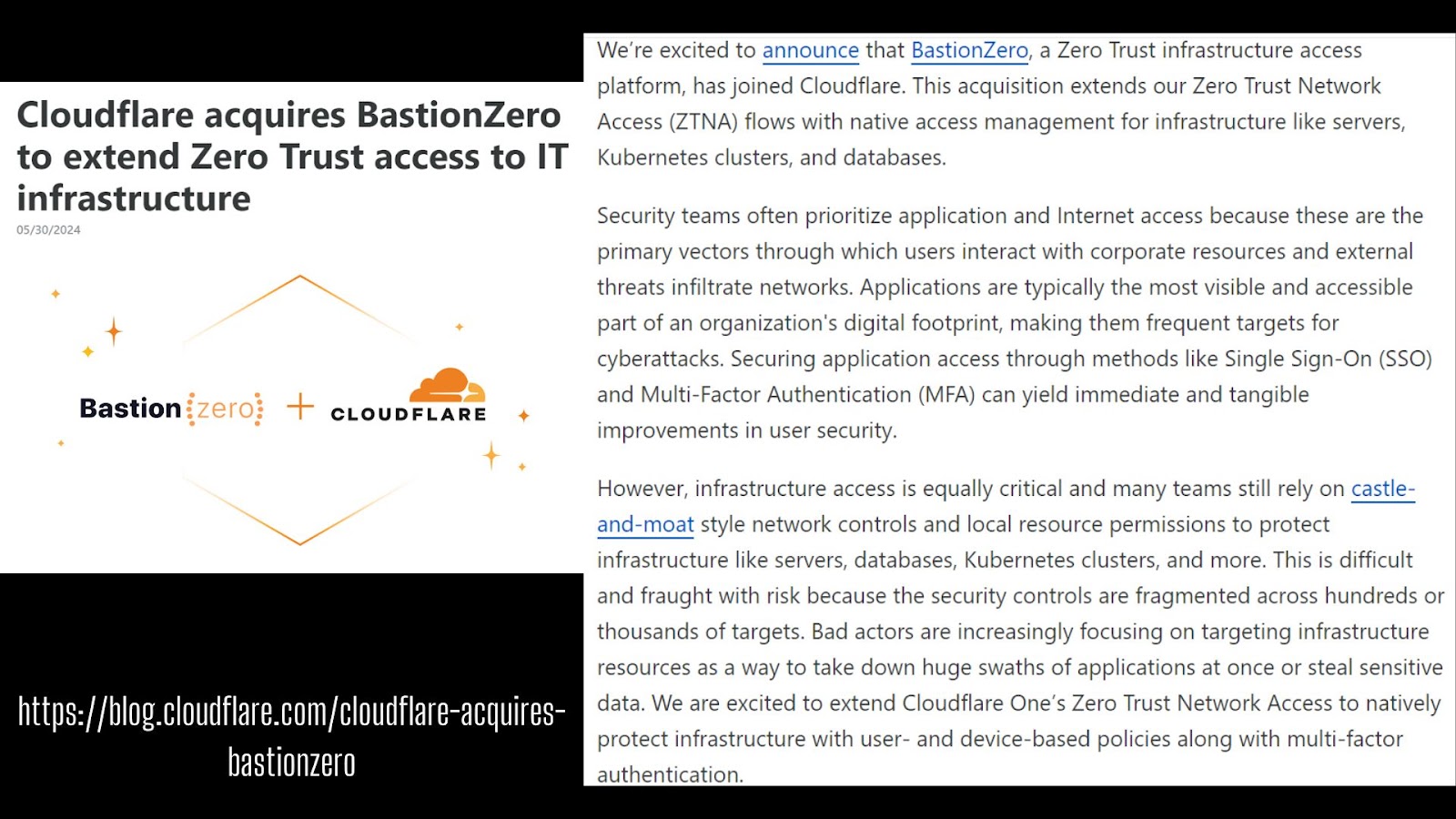

Now, this is all supposed to be about Cloudflare, a top upstart competitor to Akamai, and trying to build itself into a type of platform (infrastructure plus software services). It’s trying to do this from scratch, in an era where the infrastructure is getting much more expensive (thanks, Nvidia accelerated computing systems). As Cloudflare has grown in size, and revenue growth naturally tapers off, more acquisitions might become key to sustaining growth. The negative trade-off is, will the acquired be a good fit and be accretive? For example, you may know that Cloudflare has itself also been making a go of things in cybersecurity. It recently purchased a startup called BastionZero to boost its SASE (secure access service edge, a combo of security networking and software service that addresses the ridiculous complexities of modern IT infrastructure). https://blog.cloudflare.com/cloudflare-acquires-bastionzero

The question is, will these acquisitions pay off? Or is Cloudflare headed towards a similar fate as Akamai, squeezed by both chip suppliers from one end, and by bigger software service providers on the other demanding more data handling for the same or less money?

Hint: The trend isn’t looking as good as it did a few years ago. From the 2019 IPO through 2022, we remained highly optimistic. Some of the shine on our optimism has worn off.

The problem, as we see it, given the current tenuous state of the economy, Wall St is no longer (at least for now) rewarding businesses for no-profit expansion of customer bases and raw revenue growth. Wall St wants to see (again, at least for now, as long as the Fed exercises economic austerity with shrinking or flat monetary supply and higher interest rates) higher profit margins, and ASAP. The problem with this is it robs companies like Cloudflare from the opportunity of disrupting (in a true free market manner) the cloud giants.

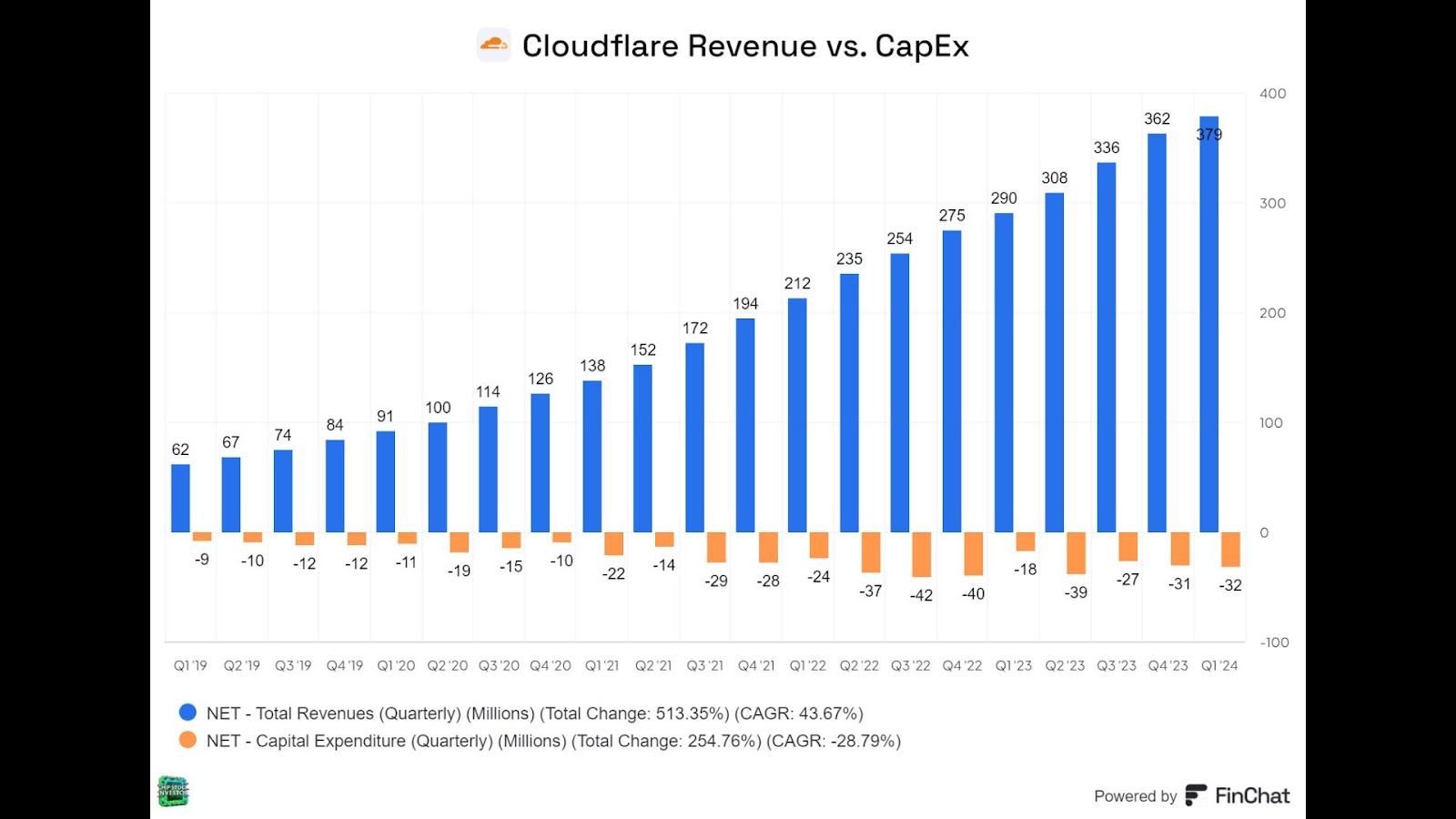

Additionally, with a new tech upgrade cycle in full force driven by AI, Cloudflare is having to spend cash on network upgrades. You can see capital expenditures (CapEx) climbing a bit and keeping pace with revenue, much like what has happened to Akamai over the years.

A financial checklist for investing in disruptive tech

And so, when it comes to investing in businesses like this, given where the economy is at, here’s our checklist of what to look for in core holdings in software businesses:

- a robust combo of tightly integrated hardware and software

- big and well-established business with breadth and depth to service offerings

- highly profitable, or rapidly rising profit margins

- strong balance sheets with more cash than debt

- if not #4, at the very least plenty of cash generation (free cash flow) to fund share buybacks and keep shares outstanding on the decrease

We hope these notes are educational in helping you whittle down where to focus your investment dollars. This is not the 2010s, it’s the 2020s, and for better or worse, current economic conditions are only strengthening the financial stranglehold winners of the 2010s were able to build against would-be competitors.