In our previous video, 3 Great Stocks to Buy For the Long-Term – What’s Good For GOOGL Is Good For NVDA and AVGO, we highlighted Alphabet (GOOGL) as a core holding, alongside Nvidia (NVDA) and Broadcom (AVGO), in what we see as the burgeoning “accelerated computing bull market of the 2020s.”

We laid out the compelling reasons for our conviction then, emphasizing Google’s AI leadership, profitable cloud growth, and foundational infrastructure for all things internet and connected world.

But after Q4 earnings, the market seems to have been a bit… unenthusiastic about Google. The stock price has seen some fluctuations.

But zooming out and looking at the bigger picture, we still remain confident in Google’s long-term trajectory. Let’s talk about why.

Why was the market so glum after Q4 earnings?

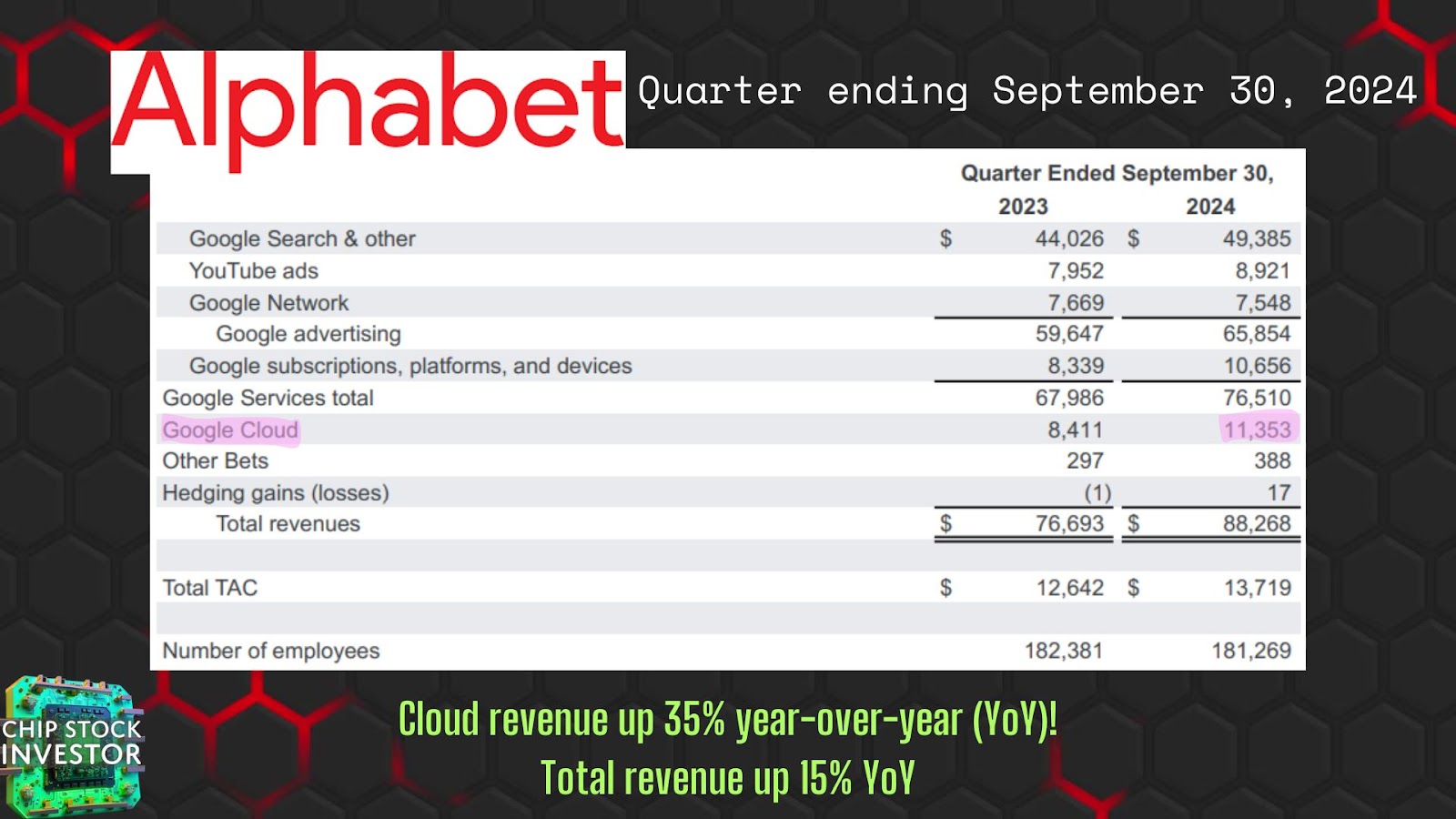

It seems the market was a little unhappy with the deceleration in growth for cloud revenue. This is from that last update we did after Q3 2024:

Google Cloud revenue was up a whopping 35% year-over-year (YoY) in Q3, 2024.

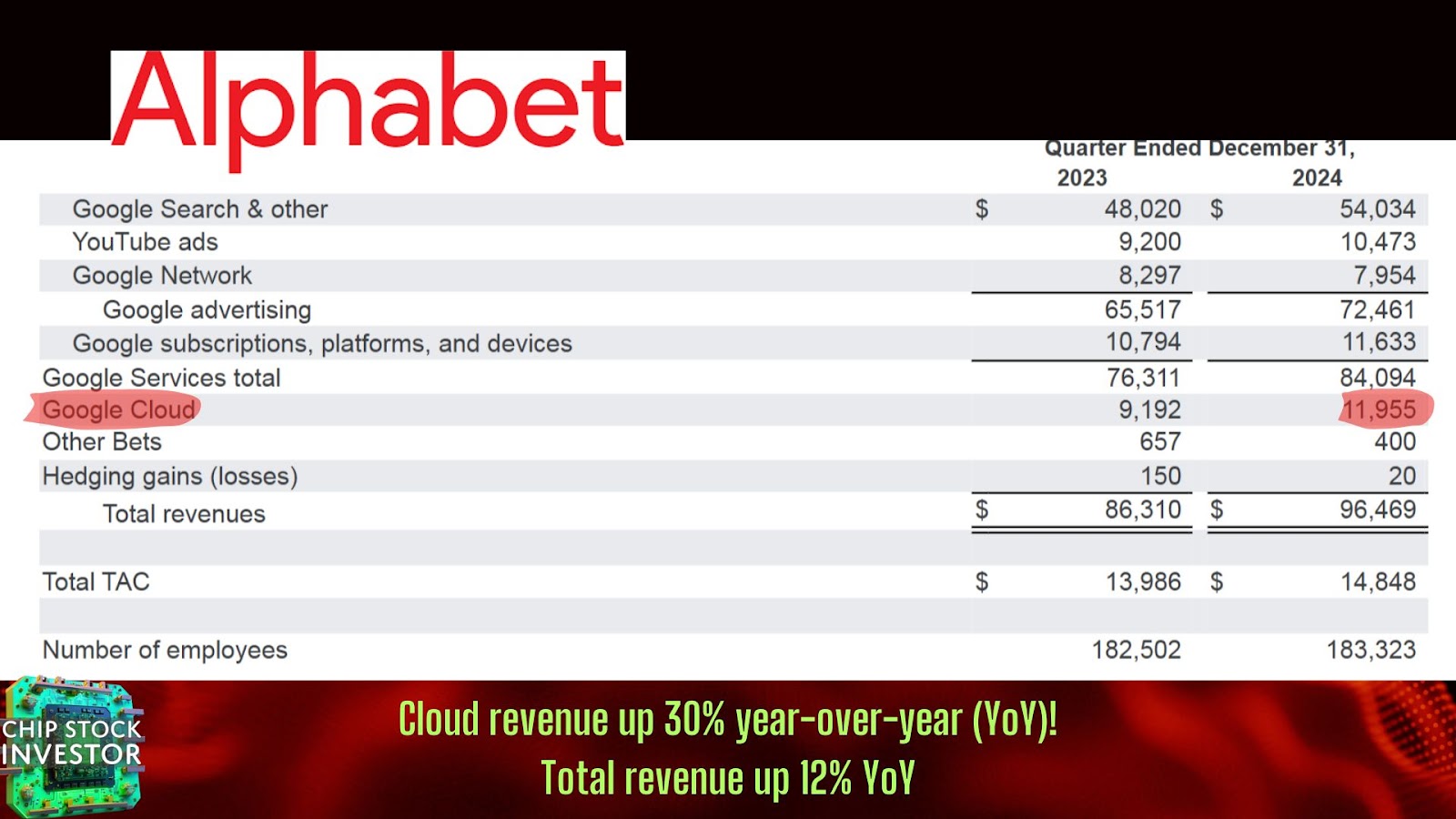

Now fast-forward to Q4, and Google Cloud revenue came in at just under $12 billion and is only up 30% YoY! Gasp!

For reference, in past years, the market was ecstatic about 20%+ cloud growth. We investors can be so fickle…

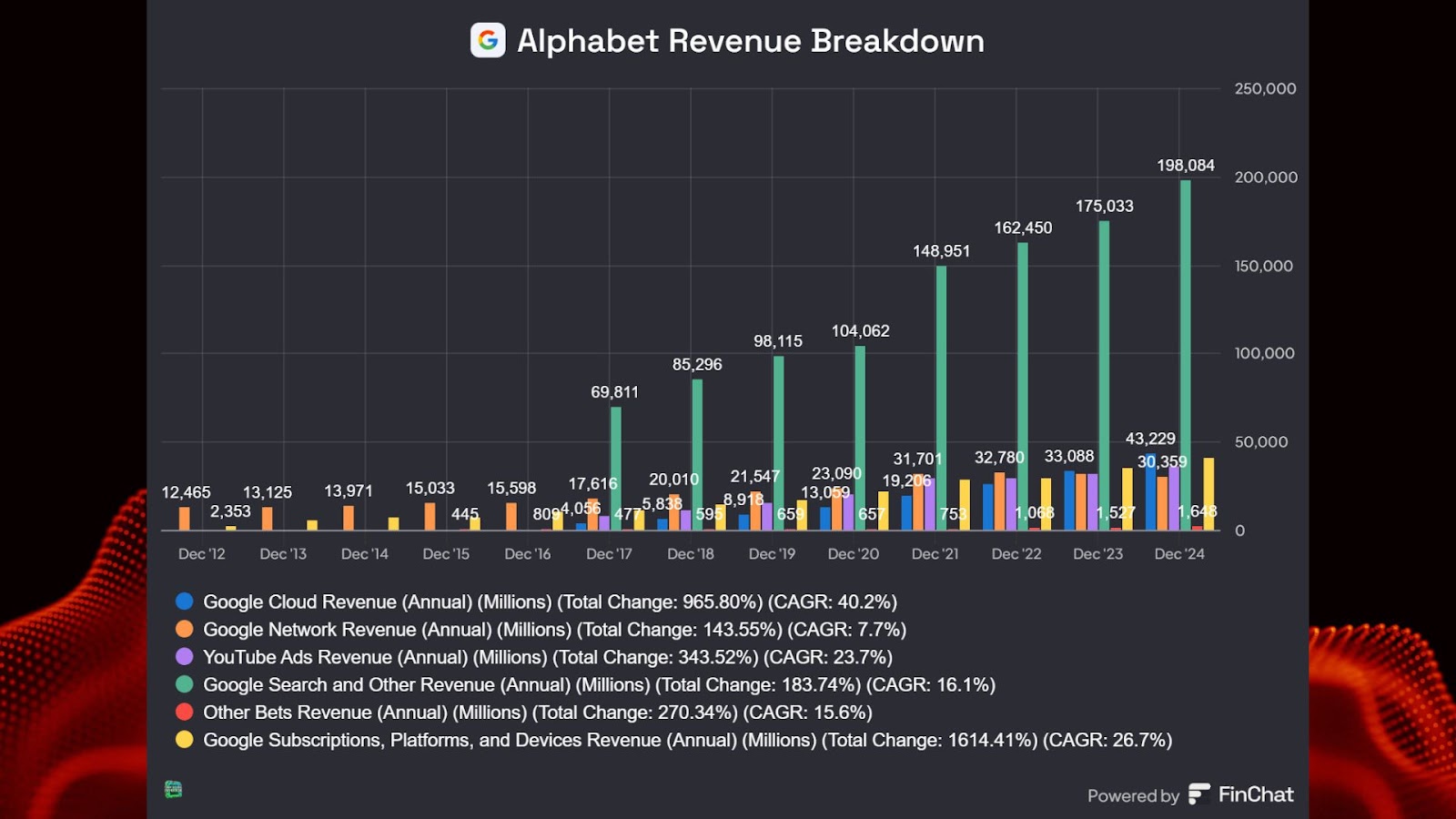

Where is Alphabet’s cloud growth headed?

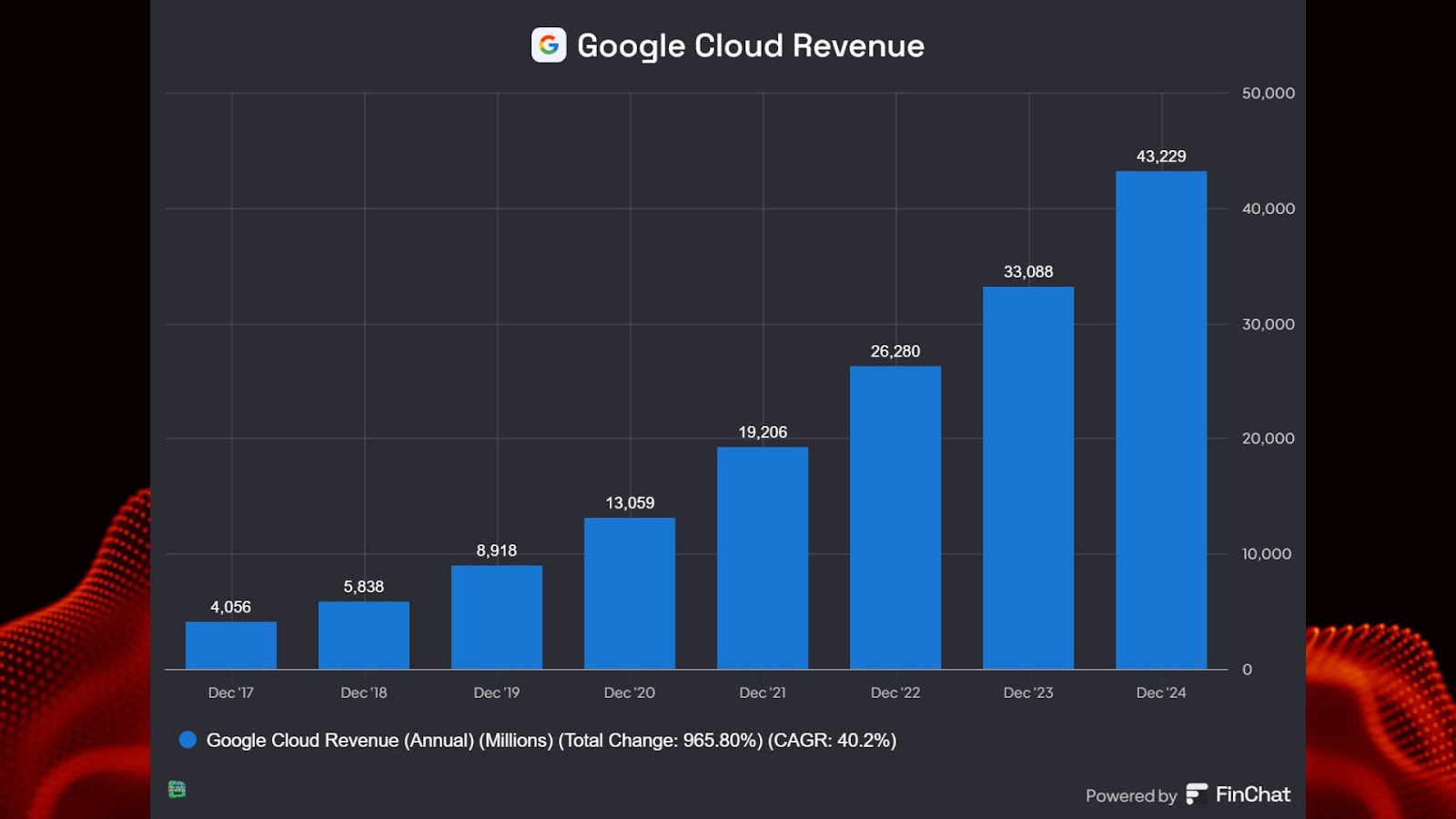

Just for a little perspective, look at the yearly breakdown of Google Cloud revenue. If this is what slow-down looks like, we certainly don’t see a need to panic.

If you want to make cool financial charts and models, check out FinChat.io. Here’s a link that gets you 15% off a membership: https://finchat.io/csi/

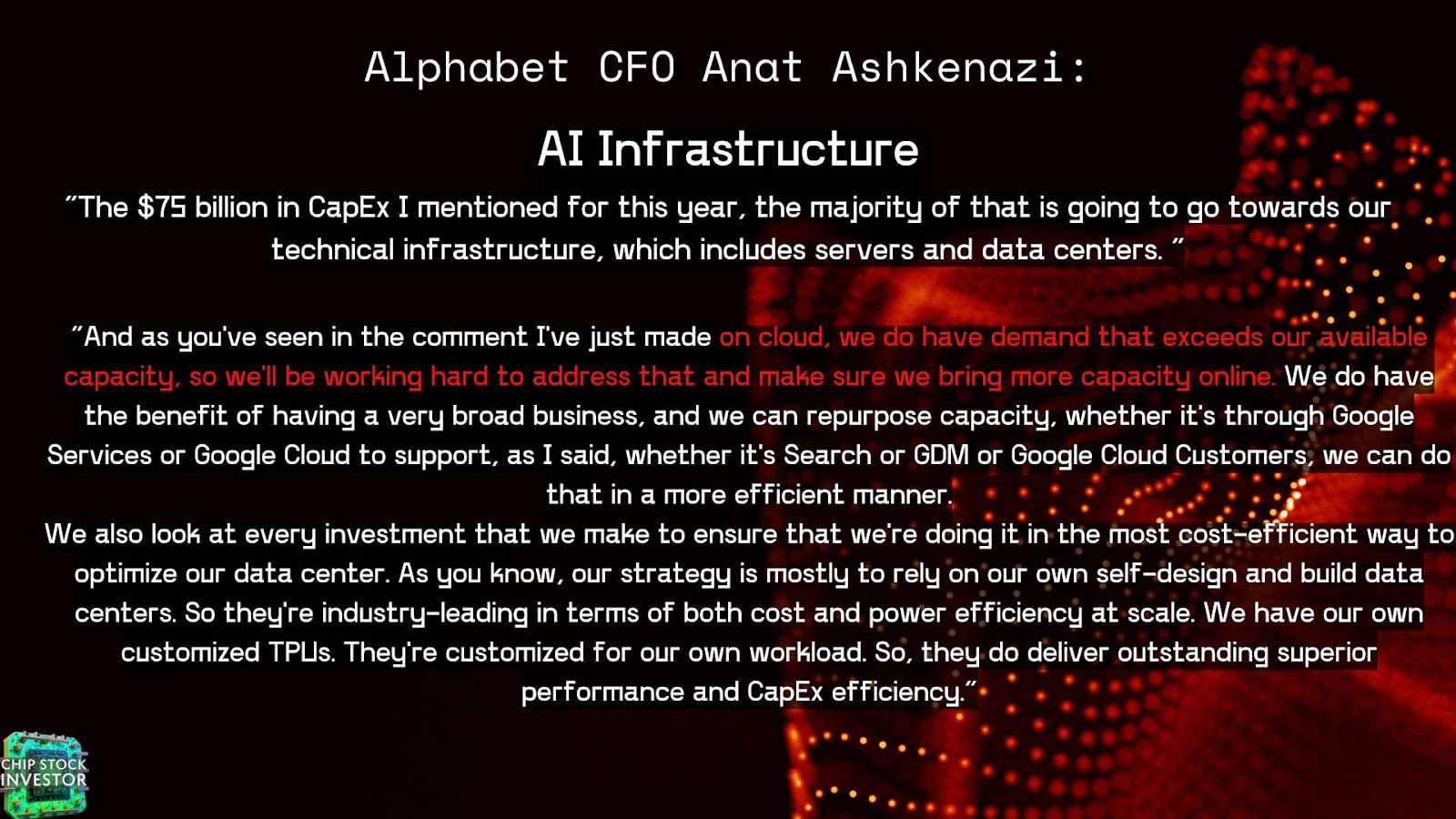

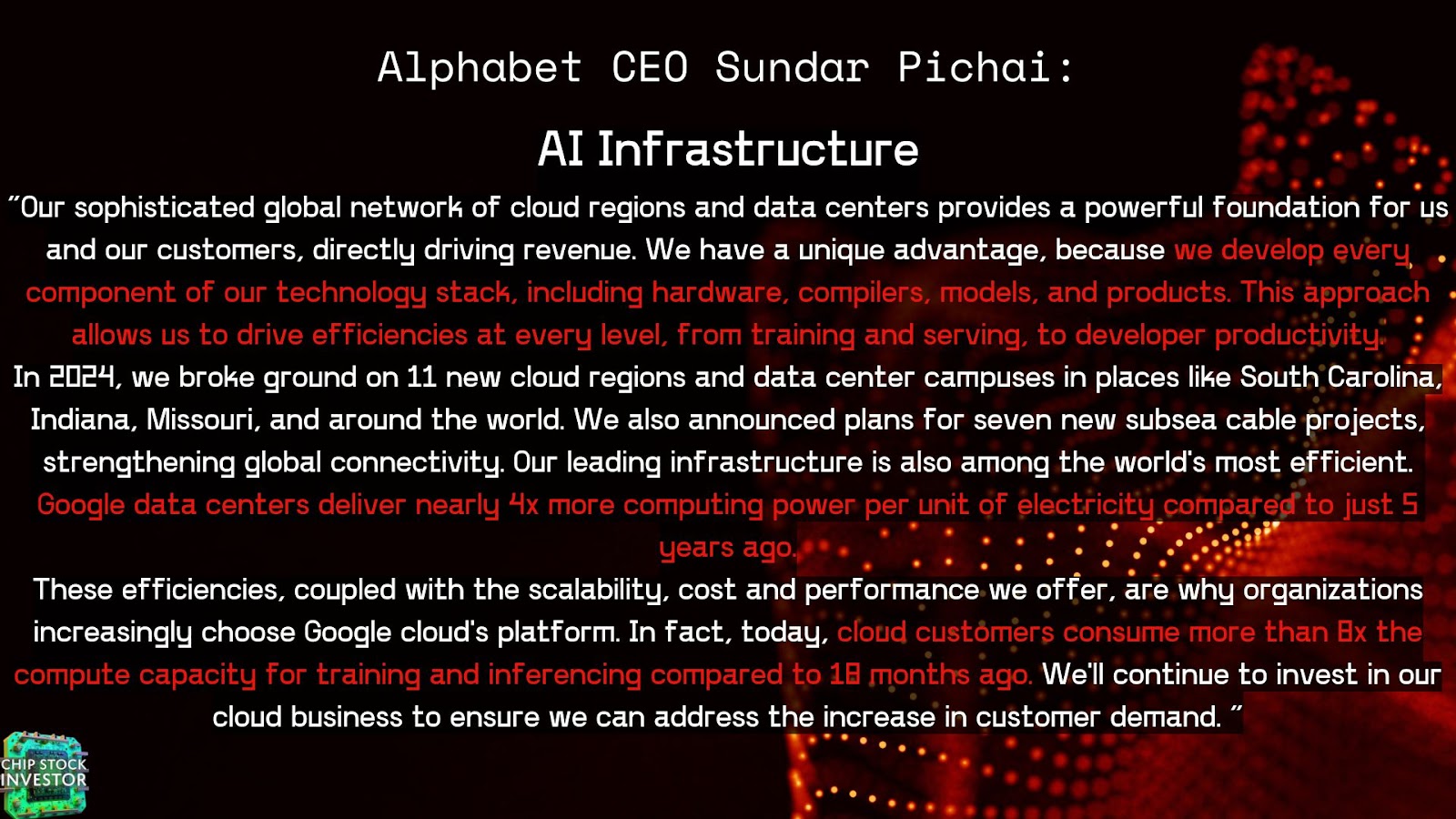

Notice what Google CFO Anat Ashkenazi had to say about cloud growth and demand:

We will get to the CapEx spend here in just a moment, but you may wonder, what happens if they bring too much capacity online?

Again, don’t panic. Ashkenazi continued:

“We do have the benefit of having a very broad business, and we can repurpose capacity, whether it’s through Google Services or Google Cloud to support, as I said, whether it’s Search or GDM or Google Cloud Customers, we can do that in a more efficient manner.”

That computing capacity that Google is spending $75 billion on in 2025, can be used for a plethora of Google’s services — Search, YouTube, Google Business, Cloud, etc.

As for the cloud revenue itself, this momentum likely continues, making Google Cloud an increasingly significant and profitable growth engine for Alphabet.

And what about Alphabet’s other revenues? Here’s a look at the breakdown of all the others (excluding hedging gains for currency conversion purposes).

Google’s CFO stated that the $75 billion in CapEx is going to be primarily used for “technical infrastructure” — much like former CFO Ruth Porat had astutely stated last year.

Alphabet’s technical infrastructure spending

What does that mean exactly? Primarily servers, followed by data center and networking equipment, and probably a bit for building construction.

Included in this is of course custom chips. Google has been busy, developing their own proprietary TPU’s (or Tensor processing units), purpose built for their data center workloads. Those TPU’s are designed in partnership with Broadcom IP. Here’s our video from January about the importance of IP in the tech world: https://youtu.be/FiRACIRhTXc

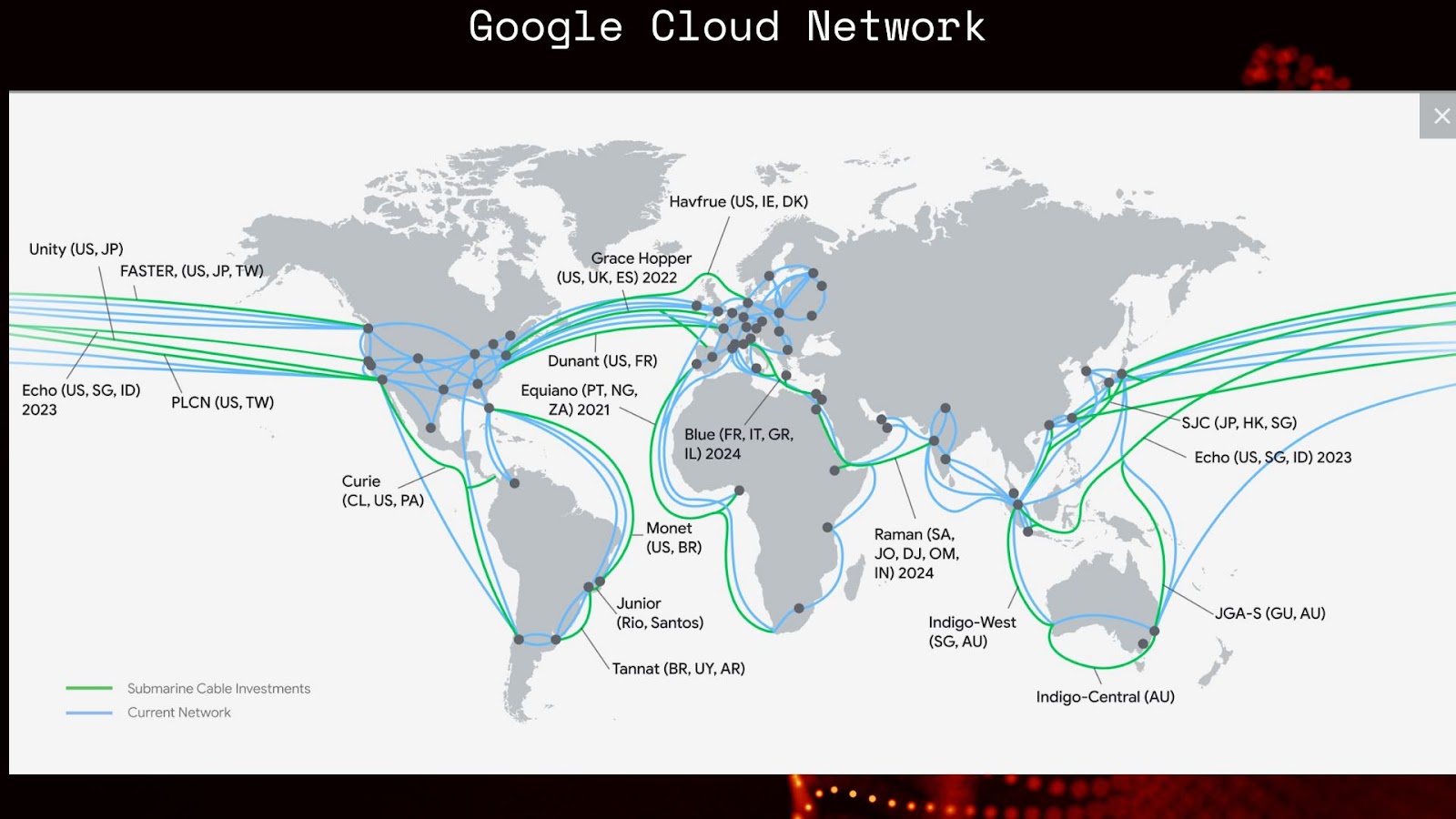

Here is a global snapshot of where Google has been spending some of that CapEx.

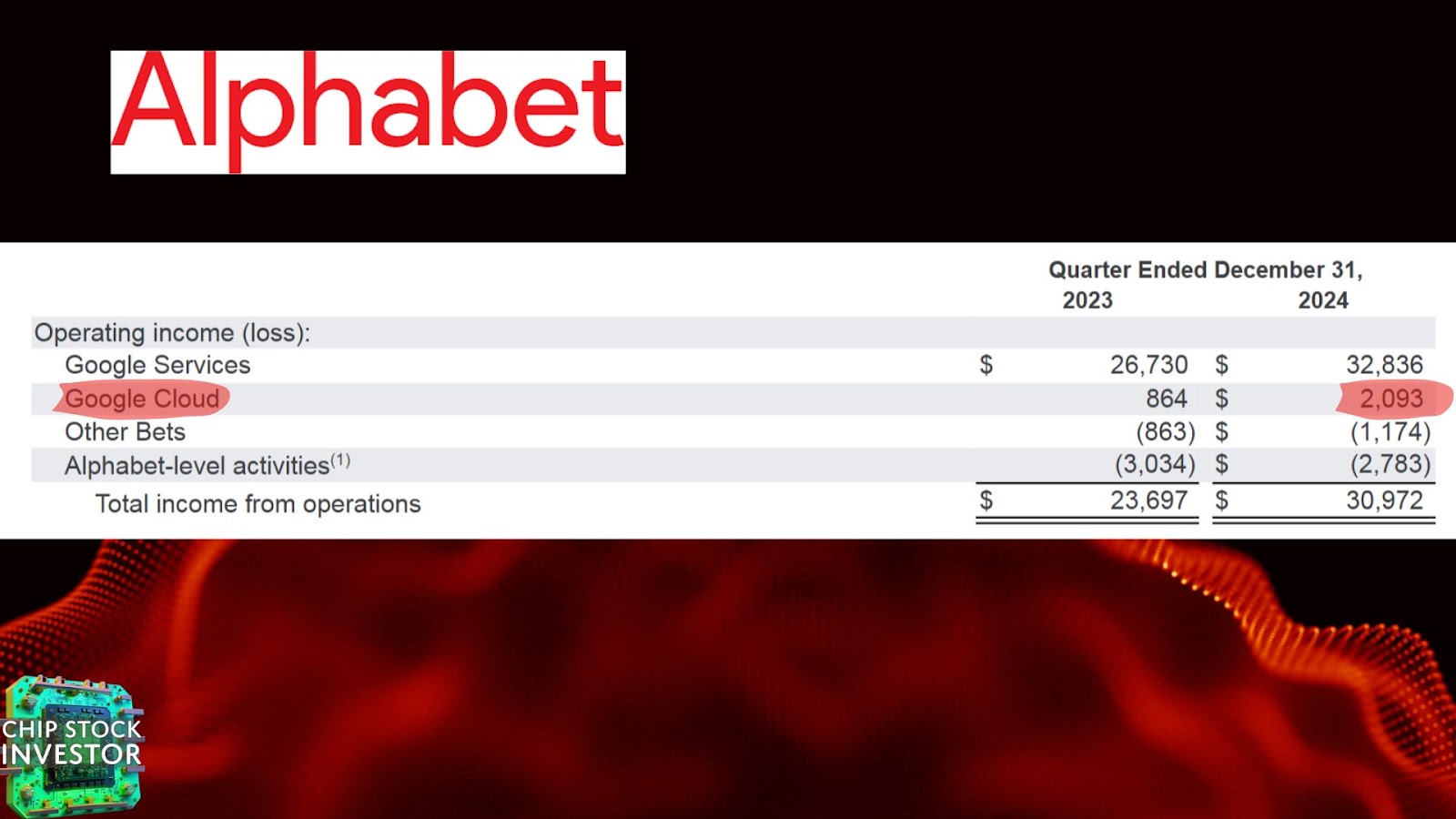

Even with all that spending, Google Cloud is becoming a top driver, not of growth, but of PROFITABLE GROWTH.

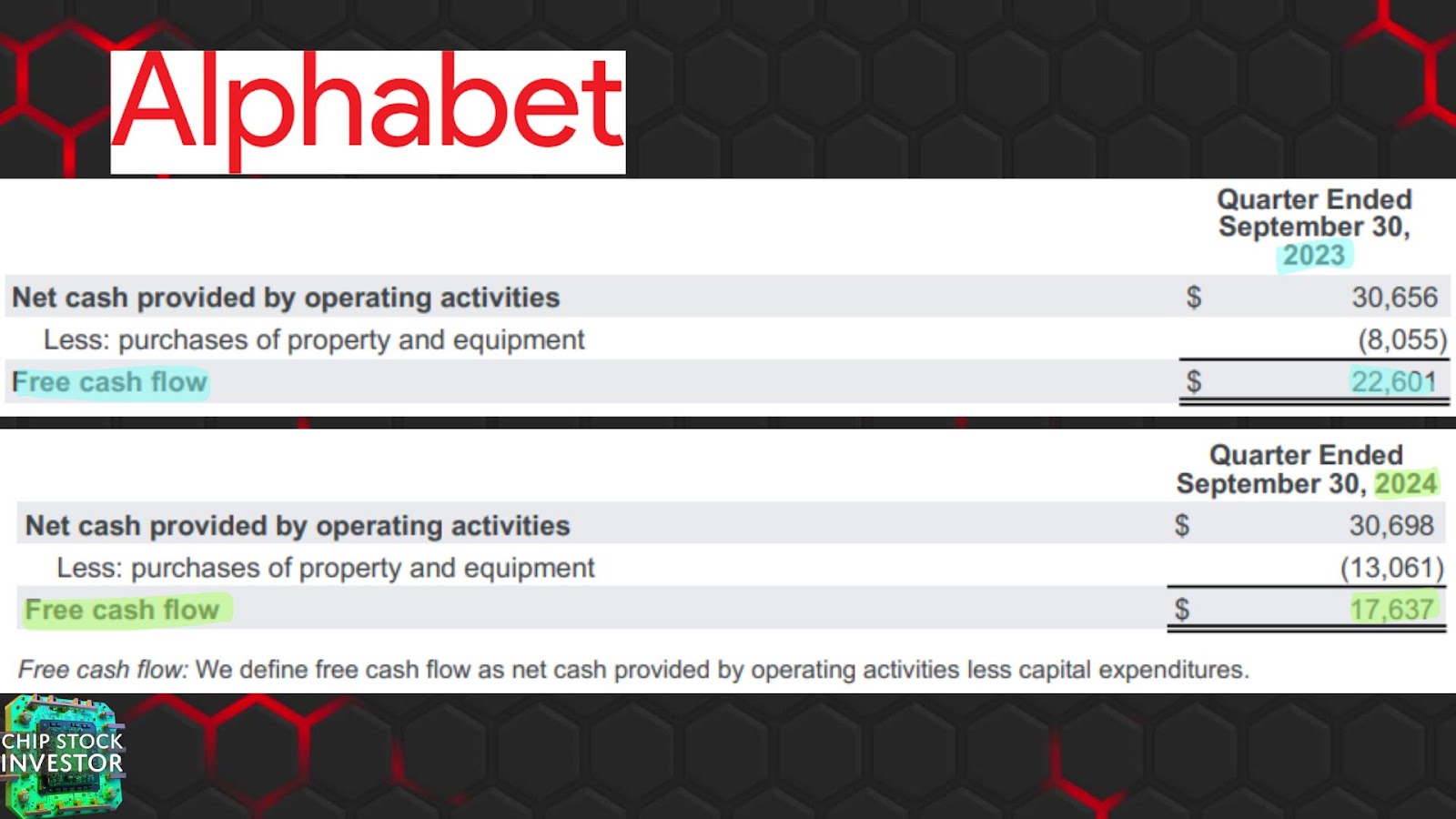

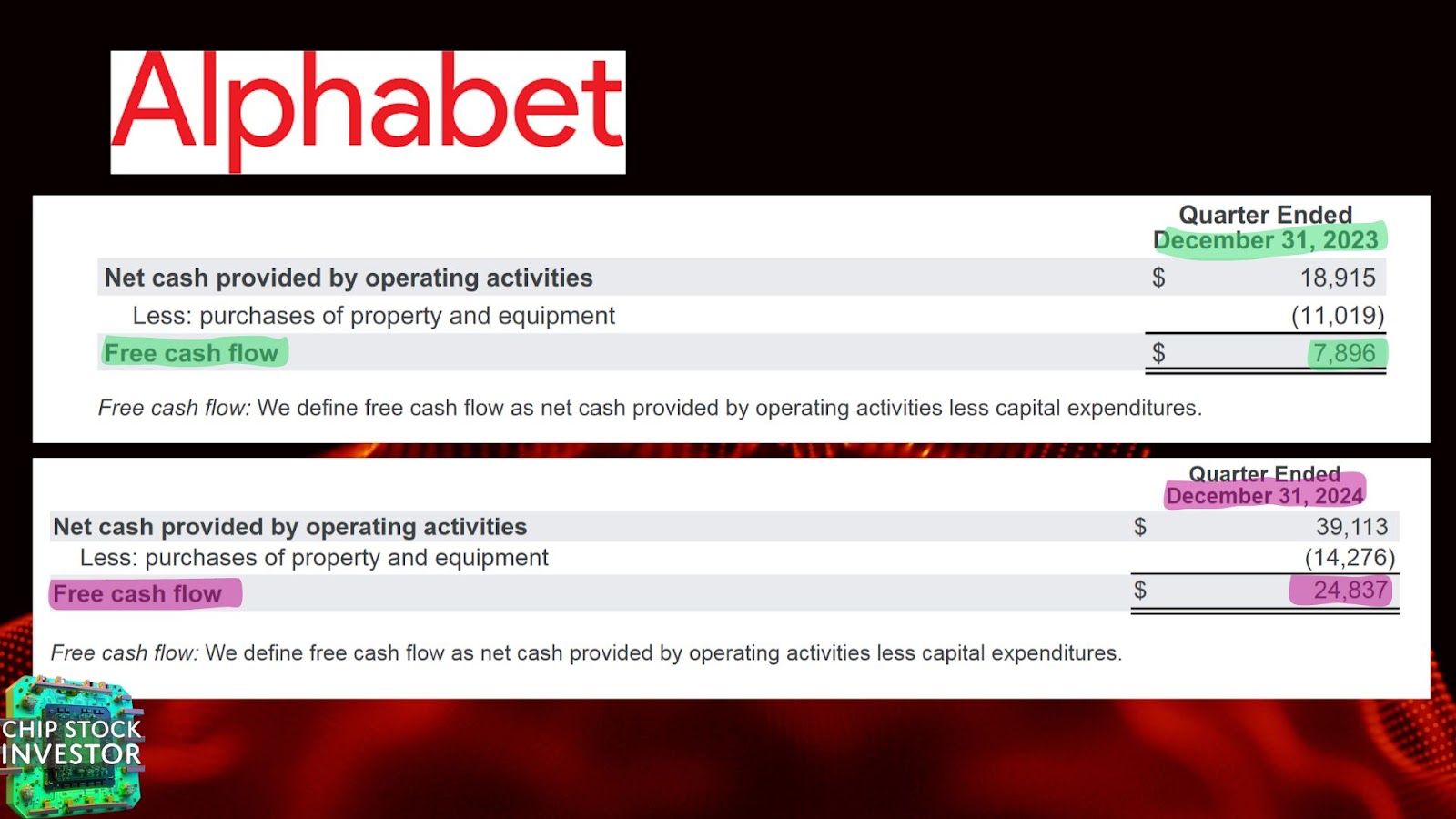

Cash flows

In Q3, we highlighted that free cash flow (FCF) was down YoY, in large part due to CapEx spend.

In Q4, we see a spike in FCF sequentially and YOY.

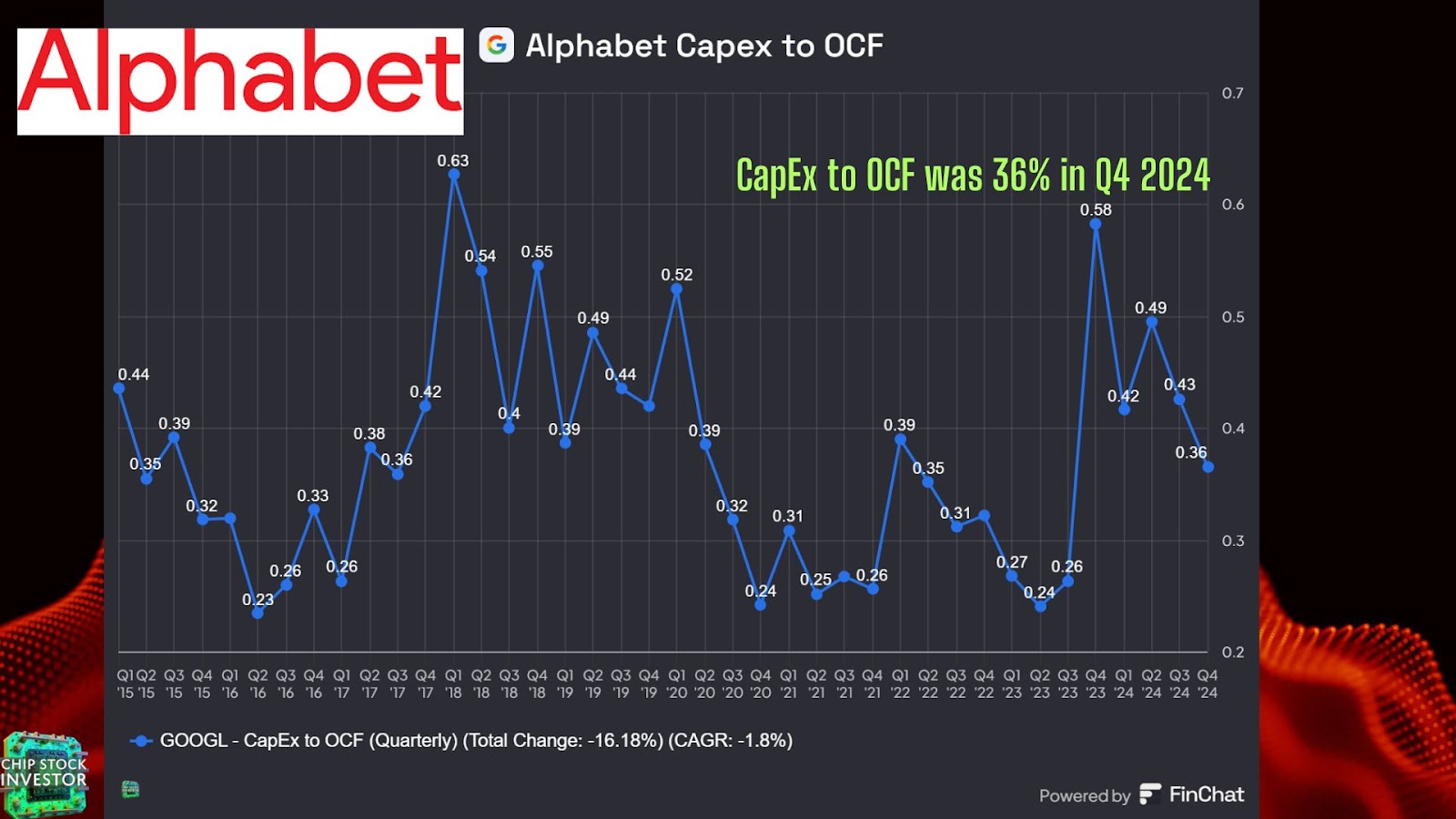

Alphabet’s CapEx to operating cash flow was 36%. This is an incredible figure given how many checks the company has been writing to Nvidia and Broadcom for accelerated computing.

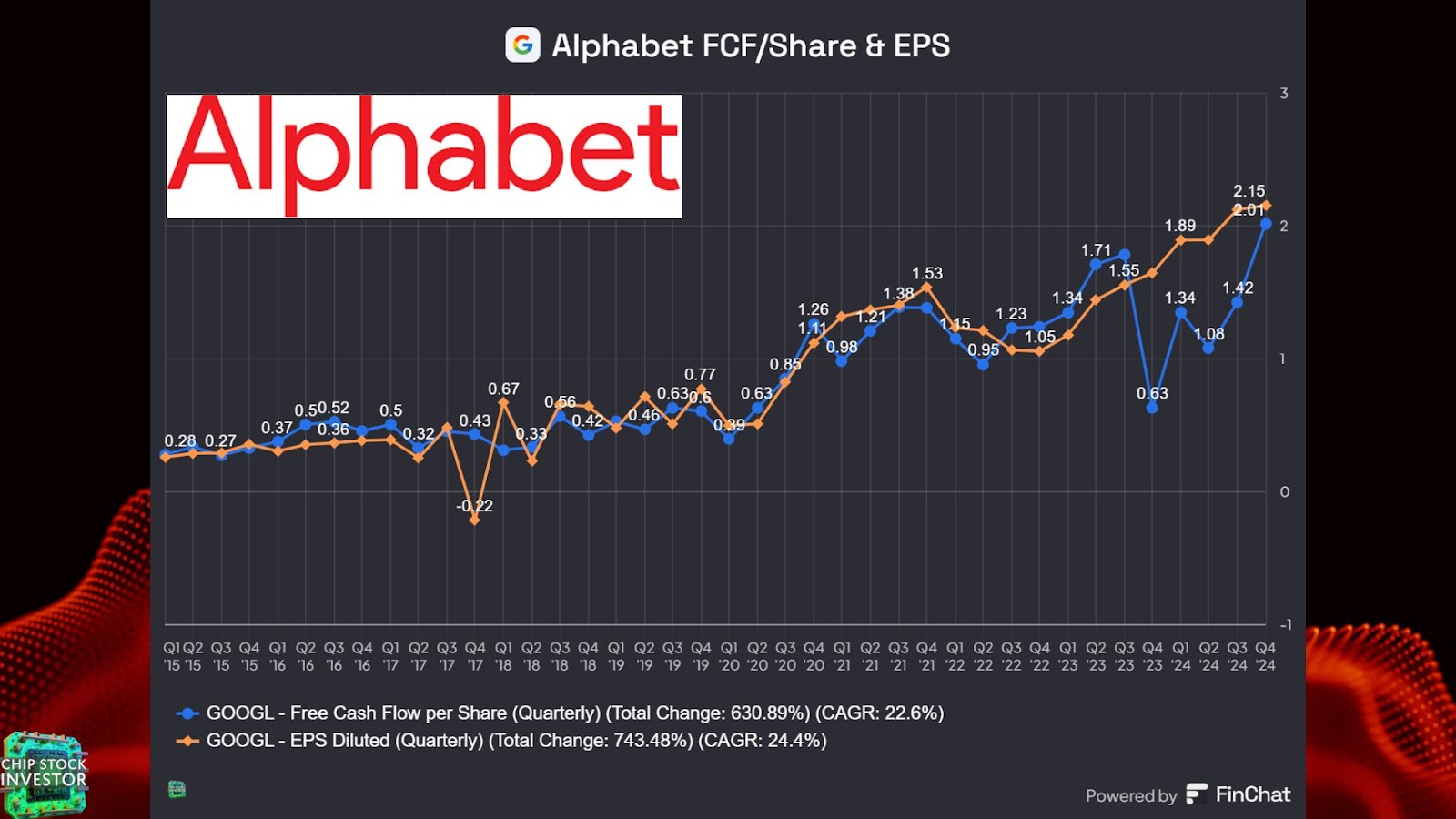

Notice FCF per share and earnings per share (EPS) reached all time highs too.

In all, there’s “nothing to see here” if you’re looking for CapEx spending gone wrong. Alphabet has customers in need for more computing power, and they’re simply spending to expand their supply of said computing power — and turning an incredible profit in the process.

This remains one of our core positions (top 5 at the start of the year, as you may recall) and we’re more than happy to keep it that way.