Table of contents:

Cadence completes its big acquisition

Q2 financial highlights and updated 2024 guidance

Cadence is foundational to AI

Why was Q2 guidance “light?”

A best bet on big chip and big tech custom AI designs

Updated valuation notes for July 2024

Just to make a point, this opening paragraph will read almost identical to the one we wrote in April 2024: Media outlets have flooded Google Search with headlines stating that Cadence Design Systems’ (NASDAQ:CDNS) second quarter 2024 earnings were good, but guidance is light for Q3. Yes, that’s true. But it was always to be expected. This is a second half team (more sports analogies!), slower in the first half of the year, busier in the second.

It seems that the market is still unhappy with the slower-but-steadier nature of this growth business. Let’s break it down again.

Cadence completes its big acquisition

We’ve stated before that the leader in electronic design automation (EDA) Synopsys (NASDAQ:SNPS) has been more willing to make big acquisitions in recent years, while Cadence has preferred smaller tuck-in purchases of smaller software companies.

However, after Synopsys announced its intent to mega-merge with Ansys (NASDAQ:ANSS) early this year to accelerate the “convergence of mechanical and electrical systems,” Cadence made its own move, announcing the purchase of BETA CAE. Our last full Cadence video: AI’s Biggest Customers So Far May Be the AI Developers Themselves: Cadence Design Systems

Here’s the video on Synopsys + Ansys: Massive Software Merger Wants to Bring AI to the World — Synopsys Acquires Ansys

And the March 2024 video explaining the “AI war” going on as companies consolidate the EDA market a bit more: The Secret AI War, and Japan’s Renesas A Top Stock For 2024?

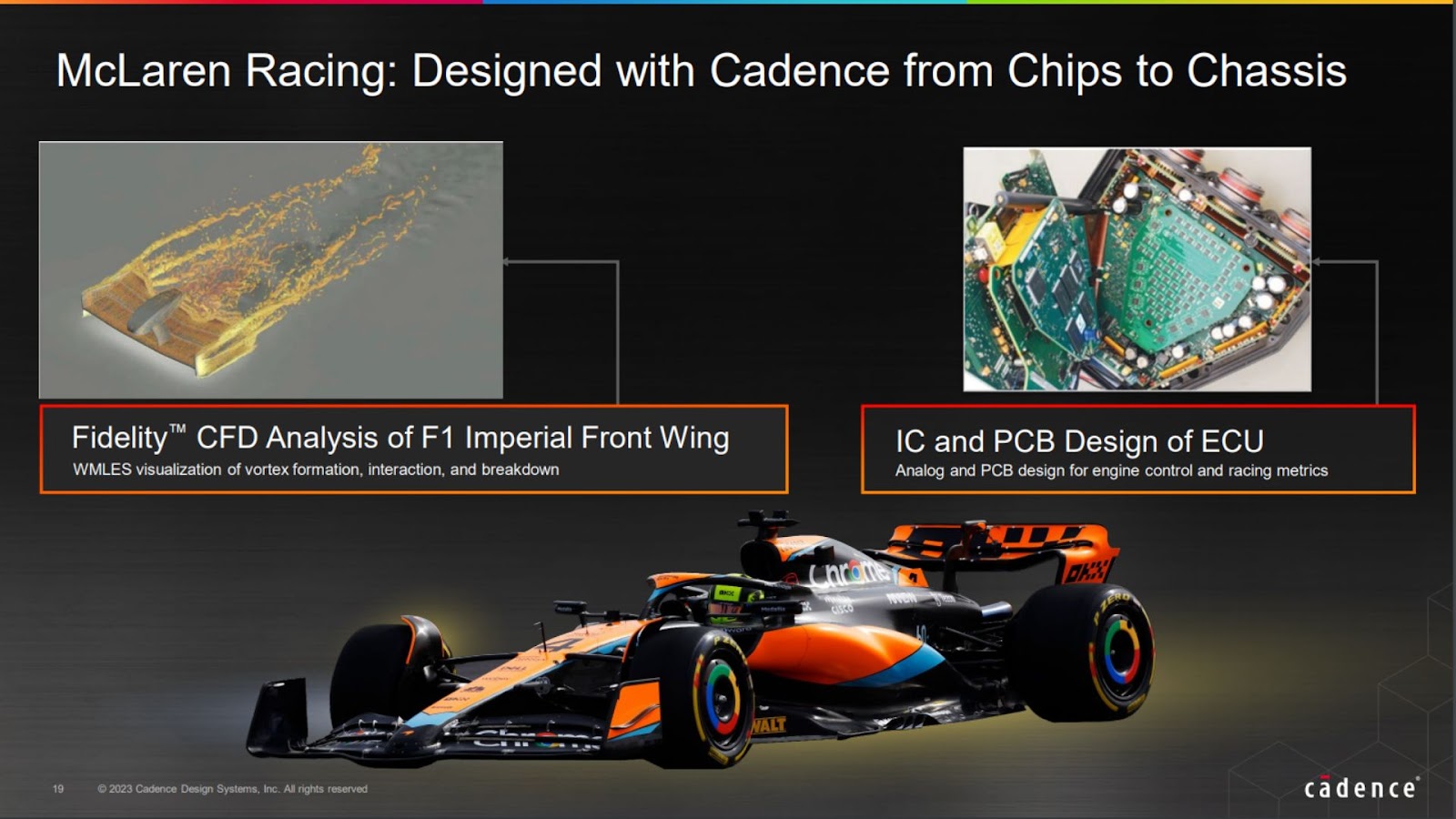

In March, Cadence announced the $1.24 billion acquisition of BETA CAE (60% paid in cash, 40% in issuance of new Cadence stock). BETA CAE’s software does simulation analysis of mechanical and structural designs, especially used by automakers. That acquisition is now complete, and is complementary not just to Cadence’s electronics software, but also the computational fluid dynamics (CFD) and multi-physics simulation software suite. https://www.cadence.com/en_US/home/company/newsroom/press-releases/pr/2024/cadence-to-acquire-beta-cae-expanding-into-structural-analysis.html

Here’s an example of what that looks like, via the partnership with McLaren’s F1 team. Cadence is probably pleased with the team’s current #2 ranking in the Constructors Championship standings.

The end result is more growth and higher free cash flow, but the balance sheet doesn’t look as pretty at the moment due to the debt Cadence took out to complete the purchase. We’ll see how this convergence between EDA and more mechanical systems design works out. But Cadence and Synopsys are still battling it out on multiple fronts.

We expect the Cadence balance sheet to clean up nicely in just a few quarters as debt is paid down. Along the way, Cadence still generates ample free cash flow (FCF) to keep repurchasing stock, completely offsetting stock-based comp and then some (~$125 million repurchased in each of the last four quarters).

Also, we frequently talk about our belief that there are very few moats in software. True competitive advantages are built over time by expanding breadth and depth of product offerings. To illustrate how wild software markets can be, Asianometry just put out a great video on the history of Cadence and Synopsys, and how they became the duopoly of EDA. The Semiconductor Design Software Duopoly: Cadence & Synopsys

Q2 financial highlights and updated 2024 guidance

So why the lackluster Q2 and light Q3? As we discussed a few months ago, much of this is regarding the big backlog of hardware (usually FPGAs, used to verify and emulate a chip before a customer sends the final design to the foundry for manufacturing) that Cadence filled for its customers this time last year. It’s lapping those elevated hardware sales now, before the next wave of growth expected later in 2024. (Yup, even this software business has some cyclicality to it.)

Guidance is still looking solid, though. Revenue guidance got lifted just a bit to an expected 13% YoY growth to $4.60 billion to $4.66 billion ($4.56 billion to $4.62 billion before). Some of this increase is thanks to the addition of BETA CAE. Also bear in mind that as the next semi industry growth cycle heats up, Cadence revenue growth will lag behind a bit (it outpaced the industry the last couple of years) because EDA and related revenue is tied to semi industry R&D spending, not final chip sales.

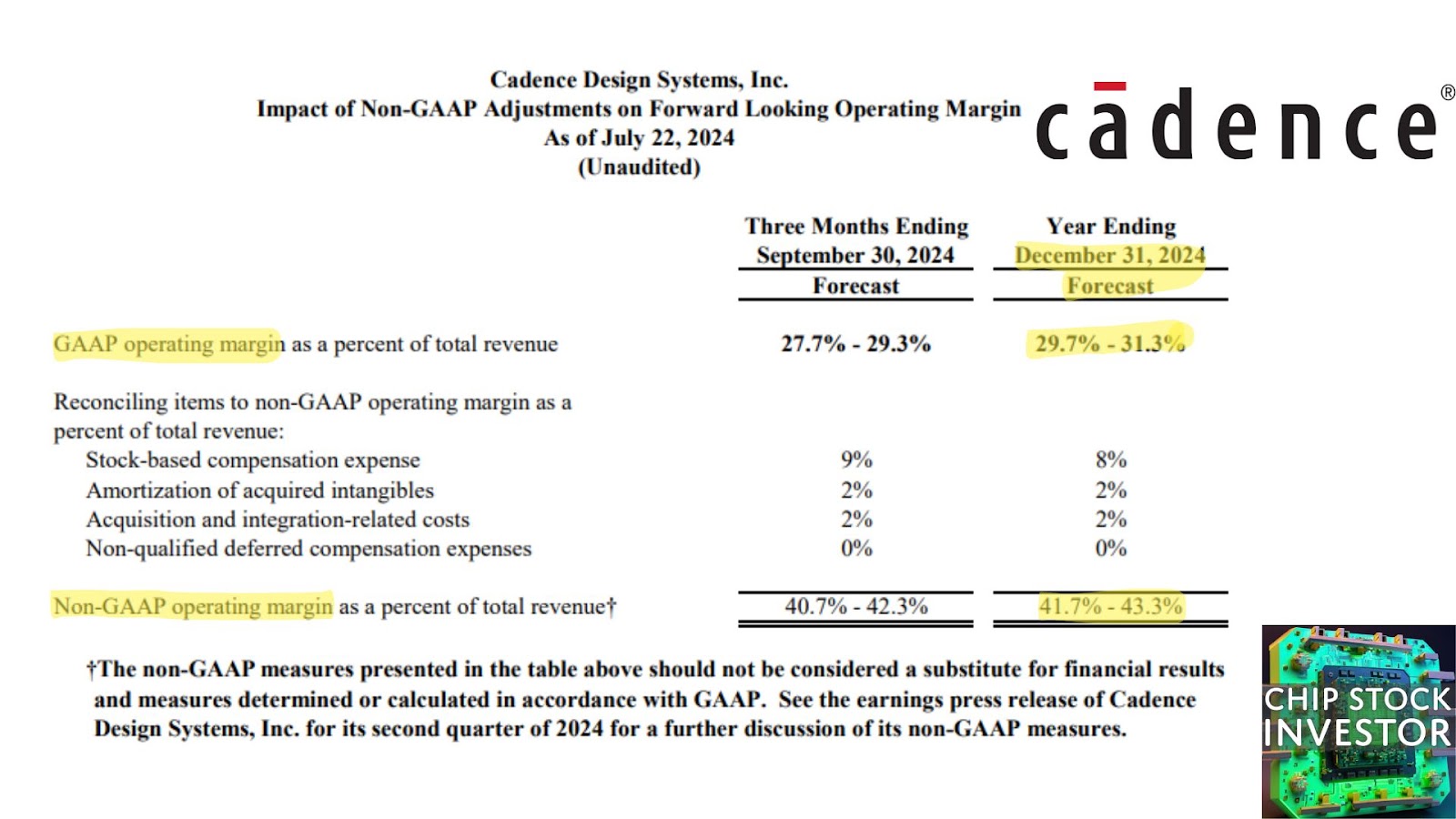

Additionally, due to the BETA CAE acquisition, GAAP operating margins are likely to dip this year. But on an adjusted basis, Cadence still expects operating profit margin expansion over 2023. Here’s what 2023 looked like for comparison:

And the updated 2024 guidance:

The sections that follow are our notes and discussion on Cadence from three months ago, which is still relevant after the Q2 financial results. Our final thoughts on valuation are in the conclusion.

Cadence is foundational to AI

Whether it’s chip design to hardware needed to sign off on those designs to entire AI system development, Cadence has built itself into a foundational powerhouse. Its services have percolated to every level of the semiconductor industry, and leading AI systems are now being recycled directly back into Cadence’s software and computing platform to immediately begin work on the next generation of AI chips and software.

A few of those foundational AI developments were discussed on the last call, which help with understanding the direction the business financials will take later in 2024 and into 2025.

CEO Anirudh Devgan on Cadence’s work on LLMs (large language models):

“Our Cadence.AI portfolio provides customers with the most comprehensive and impactful solutions for chip-to-systems intelligent design acceleration. Built upon AI-enhanced core design engine, our GenAI solution boosted by foundational LLM copilot are delivering unparalleled productivity, quality of results and time-to-market benefits for our customers. Last week, at Cadence Live Silicon Valley, several customers, including Intel, Broadcom, Qualcomm, Juniper and Arm shared their remarkable successes with solutions in our Cadence.AI portfolio.”

Devgan on the emulation (Palladium series, including Z3) and prototyping/simulation (for early software development later in the development process, Protium X3) hardware compute platform: https://www.cadence.com/en_US/home/tools/system-design-and-verification/emulation-and-prototyping/palladium.html https://www.cadence.com/en_US/home/tools/system-design-and-verification/emulation-and-prototyping/protium.html

“Palladium Z3 is powered by our next-generation custom processor and was designed with Cadence.AI tools and IP. The Z3 system is future-proof with its massive 48 billion gate capacity, enabling emulation of the industry’s largest design for the next several generations. The Z3 X3 systems have been deployed at select customers and were endorsed by NVIDIA, ARM and AMD at launch. We also introduced the Cadence Reality Digital Twin Platform, which virtualizes the entire data center and uses AI, high-performance computing and physics-based simulation to significantly improve data center energy efficiency by up to 30%.”

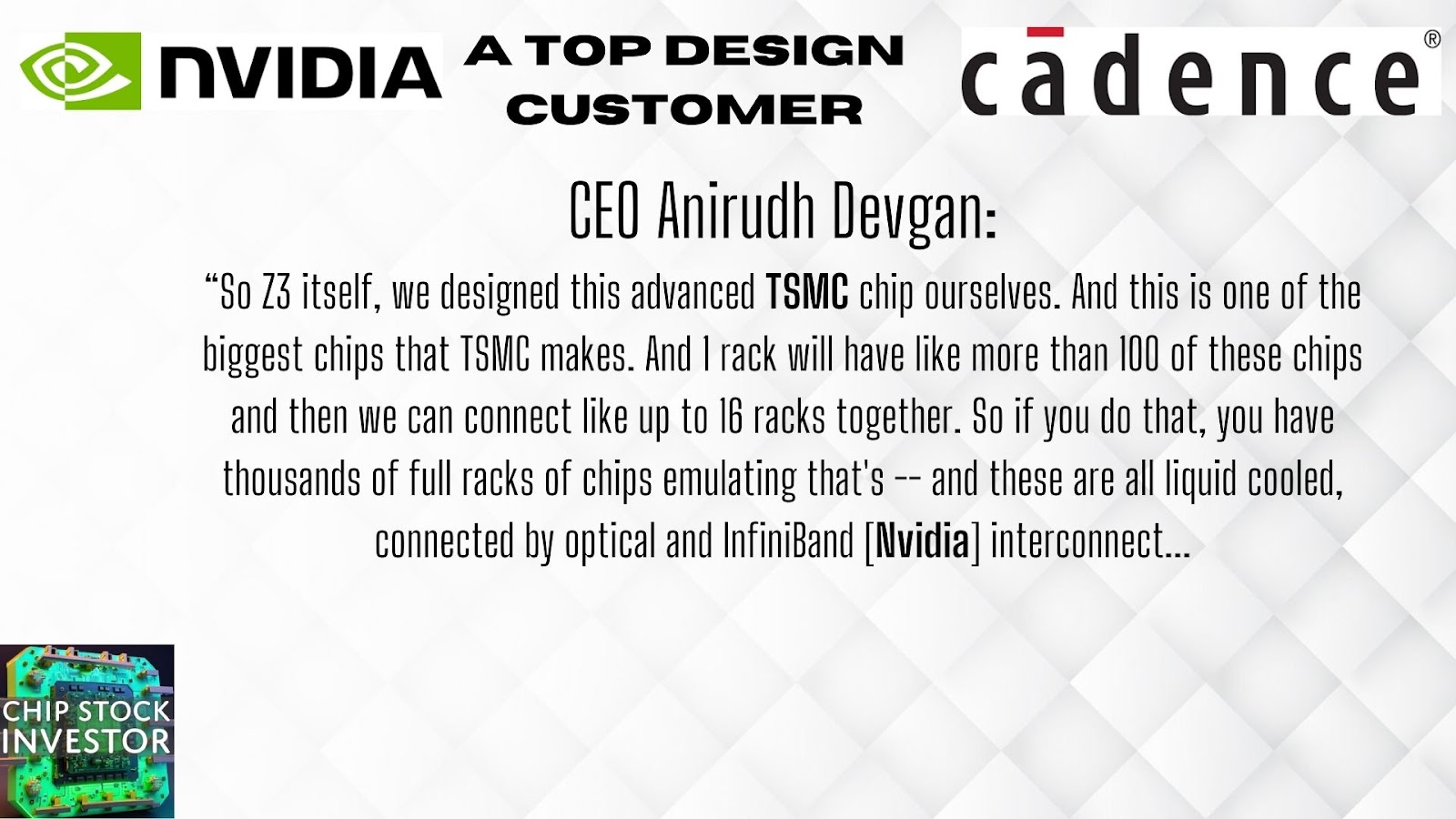

Devgan later on the custom Cadence chip (using its own IP, as well as BlueField DPUs and InfiniBand from Nvidia):

“So let’s take Z3, for example. So Z3 itself, we designed this advanced TSMC chip ourselves. And this is one of the biggest chips that TSMC makes. And 1 rack will have like more than 100 of these chips and then we can connect like up to 16 racks together. So if you do that, you have thousands of full racks of chips emulating that’s — and these are all liquid cooled, connected by optical and InfiniBand [Nvidia] interconnect. (Our video on InfiniBand: https://youtu.be/wLQzaelC5PA )

So this is like a truly a multi-rack supercomputer. And what it can do is just emulate very, very large systems, very, very efficient. So even Z2 like NVIDIA talked about it last week, even Blackwell, which is the biggest chip in the world right now with 200 billion transistors was emulated on fewer racks of Z2, okay? So now with 16 racks of Z3, we can emulate chips, which are like 5x bigger than Blackwell, which is already the biggest chips in the world, right?

So that gives a lot of runway for our customers because with AI, the key thing is that the capacity of the chip needs to keep going up, not just a single ship, look at Blackwell, they have 2 full radical ships chips on a package. So as you know, you will see more and more, not just big chips on a single node, but multiple chips in a package for this AI workload and also 3D stacking of those chips.

So what this allows is not just emulating a single large chip but multiple chips, which is super critical for AI, okay? So I think this is what I feel that this puts us in a very good position for all this AI boom that is happening, not just with our partners like NVIDIA and AMD, but also all the hyperscaler companies, okay?

And so that will be the primary demand as more capacity chips require more hardware, okay? And then X3 will go for that with software prototyping, which is used on FPGA [field programmable gate arrays, like from AMD’s Xilinx].” (We explained how that works last summer: https://www.fool.com/investing/2023/07/21/amds-best-bet-on-ai-may-not-be-what-you-think/ )

Why was Q2 guidance “light?”

CFO John Wall:

“Given the recent launch of our new hardware systems, we expect the shape of hardware revenue in 2024 to weigh more towards the second half as our team works to build inventory of the new system. Our updated outlook does not include the impact of our pending BETA CAE acquisition, and it contains the usual assumption that export control regulations that exist today remain substantially similar for the remainder of the year.”

It was also added later that the Rambus HBM memory IP acquisition will also begin contributing to revenue more meaningfully in the 2nd half of this year too. Intel IFS (Foundry Services) is also steadily ramping up use of Cadence IP.

Wall later expounded that this year, hardware-based up-front revenue is expected to be about $800 million (up from $650 million last year) – but with $250 million of that in the first half of the year but $550 million in the second half.

Q2 may have been light, but management actually raised full-year revenue guidance by about $10 million, and EPS by $0.01. Cadence is just fine.

A best bet on big chip and big tech custom AI designs

Devgan on any perceived change in acquisition strategy:

“And a lot of times, there are a lot of reports, and we normally don’t comment on these reports and people get very creative on these reporting.”

Touche, Mr. Devgan. That said, he explains further, validating our past analysis of the Cadence strategy:

“But what I would like to say is that our strategy hasn’t changed, okay? It’s the same strategy from 2018. First of all, I want to make sure you know that we are focused in our core business, which is EDA and IP. But what is one thing that I even mentioned last time, what is different from 2018 to now is that EDA and IP is much more valuable to the industry. Our core business itself has become much more valuable because of AI, okay? So our first focus is in our core business. So we are leading in our core business. Our first focus is on organic development, okay? That’s what we like. We always say that’s the best way forward.”

Devgan on big tech colliding with “big chip” designers, as the cloud and internet companies design more of their own silicon (using chip industry IP, of course):

“And the pace of AI innovation like is increasing and not just in the big semi companies, but of course, in these system companies. And I think several announcements did come out, right, including, I think now Meta is public that Meta is designing a lot of silicon for AI. And of course, Google, Microsoft, Amazon. So all the big, really hyperscaler companies, along with NVIDIA, AMD, Qualcomm, all the other kind of Samsung had AI phone this year.

So I mean, there is a lot of acceleration both on the semi side and on the system side. And we are involved with all the major players there, and we’re glad to provide our solutions.

And I do think — and this is the other thesis we have talked about for years now, right, 5, 7 years that the system companies will do silicon because of a lot of reasons for customization, for schedule and supply chain control for cost benefits, if there is enough scale. And I think the workload of AI, like if you look at I think some of the big hyperscaler and social media companies, they’re talking about using like 20,000, 24,000 GPUs to train these new models. I mean this is immense amount.

And then the size of the model and the number of models increased, so that could go to a much, much higher number than right now that is required to train these models and of course, to do inference on these models. So I think we are still in the early innings in terms of system companies developing their own chips and at the same time, working with the semi companies. So I expect that to grow and those — and our business with the system companies doing silicon, I would like to say is growing faster than Cadence average. But the good thing is the semi guys are also doing a lot of business. So I don’t know if that 45% will — because that’s a combination of a lot of companies. But overall, the AI and hyperscalers, they are doing a lot more and so are the big semi companies.”

Updated valuation notes for July 2024

Just like in April, we are now getting a summertime chip stock selloff during earnings season. Even with that selloff, Cadence stock still isn’t a “cheap” investment. The earnings multiple expansion opportunity looks played out, and could be a drag on stock performance in the coming years.

Let’s do a reverse discounted cash flow calculation (we use this simple calculator: http://www.moneychimp.com/articles/valuation/dcf.htm ) to see what the market is now factoring for, assuming ~$280 a share is fair value:

Same as in April, we still think this is the closest Cadence stock has been to fair value in at least a year. The stretched valuation is why we put our DCA of it and Synopsys on hold late in 2023. We like where our portfolio is at right now, and so aren’t adding at this time, but we’ll be watching carefully. However, bear in mind the cyclicality of this software business. That cyclicality doesn’t show up so much in revenue, but in the lumpy profitability. At some point, as new hardware sales kick in, there could be a dramatic uptick in earnings that balance out the expensive looking valuation. That next run higher should start to kick in in 2025. This shows up in the lower (but still elevated) expected one-year-forward valuation:

Earnings could improve more than expected, but it’s too soon to tell. We’re still only in the early innings of the new growth cycle for most of the semiconductor industry (excluding accelerated computing and AI).

As per usual, we think a dollar-cost average (DCA) plan is appropriate for a stock like this, for those investors that want to build a position in Cadence (and Synopsys) over time. Or, if that doesn’t sound so appealing, there’s nothing wrong with getting EDA duopoly exposure via one of the industry ETFs, iShares Semiconductor ETF (SOXX) or VanEck Semiconductor ETF (SMH).