Chatter about the “AI bubble” continues, and what it all means for Nvidia’s (NVDA) meteoric rise to one of the world’s most valuable and important companies.

Meanwhile, Alphabet (GOOGL/GOOG) – a top Nvidia customer – just had its Q2 2024 financial update. AI made a nearly every-other-sentence appearance on the earnings conference call. There’s serious confusion about all of this “AI spending” on AI, chatbots, LLMs, and such to the point that the cries this is a bubble are getting quite loud. Let us clear a few things up for you, dear reader/viewer.

Where did the AI bubble talk come from?

At least some of the AI bubble conversation circling right now can be traced back to an article originally published by venture capital firm Sequoia Capital last year, and updated in June 2024. A simple equation using Nvidia’s annualized data center revenue equates this revenue line item with AI, and makes the case that companies like Alphabet’s Google, Meta, Microsoft, Amazon, and others, need to earn $600 billion in revenue to justify the spending on Nvidia hardware. Other similar calculations have been made and used as evidence of a “bubble” forming.

You can read the assertion from Sequoia here: https://www.sequoiacap.com/article/ais-600b-question/

How did Sequoia get to the $90 billion in annual Nvidia data center revenue for Q1, and $150 billion for Q4? $22.5 billion in Q1 x4 was used, and estimating $37.5 billion in quarterly data center sales in Q4 this year x4, to get an annualized figure. See Nvidia’s revenue segments below.

We’ll talk about Google’s AI revenue in a bit, but suffice to say it’s currently minimal. So $600 billion in mostly non-existent revenue on data center AI surely sounds like a bubble, right???

Popping the bubble before it even truly starts

Wrong! There’s a massive fact that is omitted from the equation, and it’s simply this: Nvidia calls this revenue line item Data Center, NOT AI. There’s a good reason for that. Nvidia’s sales are going towards far more than AI applications. It’s going to data center operators in general. And according to just one estimate from tech researcher Gartner (IT), annual end-user cloud computing spend (a top revenue stream for the world’s data centers) IS ALREADY AT OR ABOVE $600 BILLION THIS YEAR.

In fact, end-user cloud spending (revenue for the tech giants like Google) is quickly headed towards $1 trillion a year, still a minority slice of the estimated $5 trillion in global IT spending right now. https://www.gartner.com/en/newsroom/press-releases/2024-05-20-gartner-forecasts-worldwide-public-cloud-end-user-spending-to-surpass-675-billion-in-2024 https://www.gartner.com/en/newsroom/press-releases/2024-07-16-gartner-forecasts-worldwide-it-spending-to-grow-7-point-5-percent-in-2024

In other words, there may not be much of an Nvidia bubble at all. Nvidia is simply supplying the necessary infrastructure for existing data center businesses that already generate ample and rising amounts of revenue and profit.

Let’s get a few terms straight

Viewed from this standpoint, the real bubble here isn’t AI infrastructure spending, but the conversation about an AI bubble.

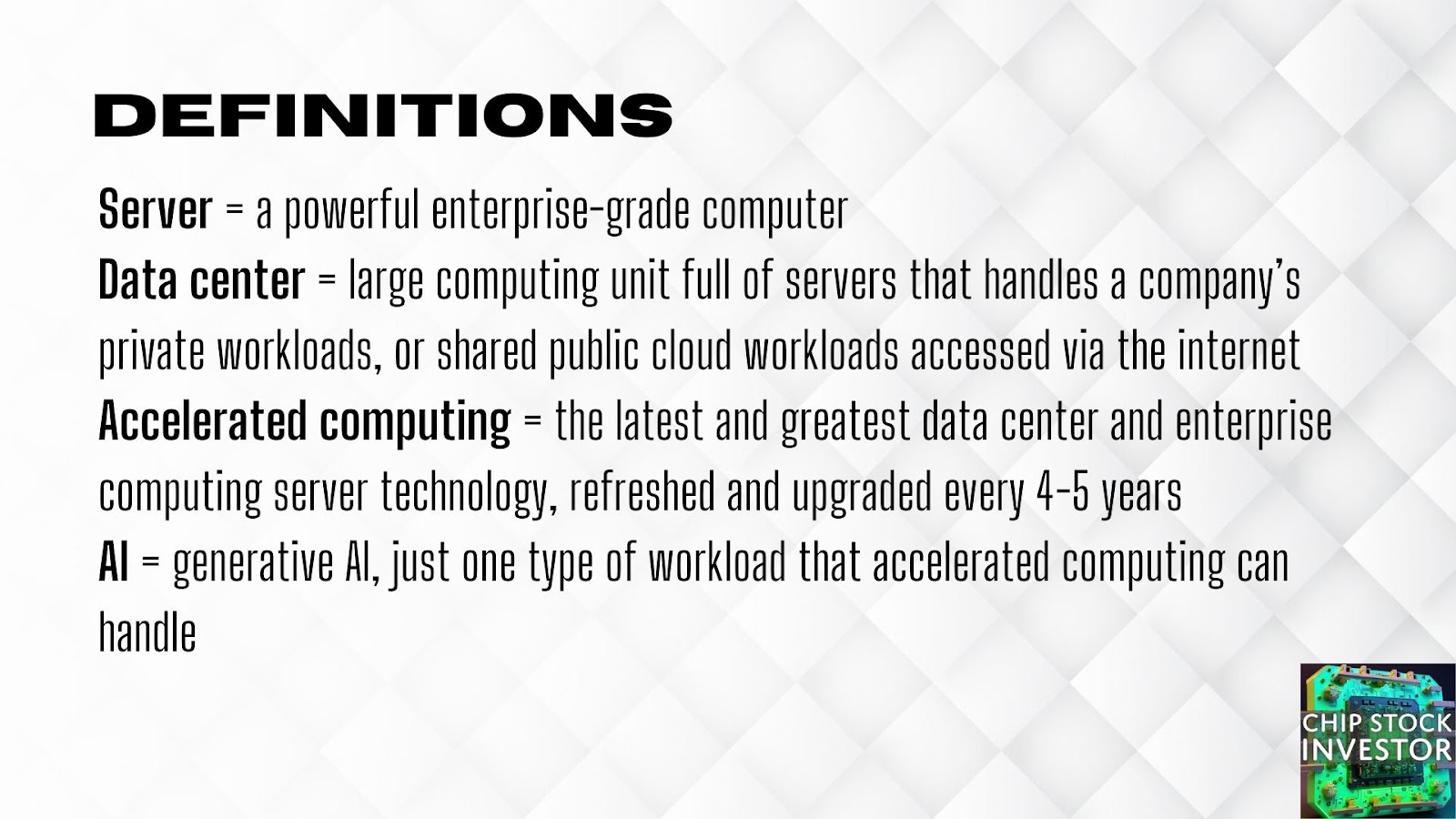

A few definitions may help explain why.

What’s really going on with the AI hype?

So, the existing global data center infrastructure that exists today (in support of private business data networks, the internet, and the cloud) is valued at ~$1 trillion. And like any infrastructure, the equipment in those data centers (like the servers) age and wear out. The equipment needs to be refreshed or upgraded every so often (4 to 5 years). An example of this is Google’s several dozen internet data center fleet, plus its growing Google Cloud data centers.

Put simply, Google (and other tech giants) are a type of modern-day utility company. They need to build and maintain infrastructure to deliver services. That means buying servers and related equipment for their data centers and global network of cables connecting the data centers together.

We wrote and recorded a video on how this situation developed over the last half-a-century or so here: Don’t Think About Investing In Cloudflare Until You Know About This Data Center Stock — NET Stock

Slide below showing the disaggregated timeline of events that got us to this point.

But what does this have to do with Nvidia? Simply this: We’ve reached a point where these computing infrastructure (utility) companies see financial benefit in ripping out their old CPU-powered servers (from the likes of Intel and AMD), and replacing it with Nvidia’s GPU-powered accelerated computing servers.

By now, everyone in the investment world has heard about the incredible price-to-performance of Nvidia’s latest-and-greatest GPU chips (computing accelerators). A small number of those are being purchased to build brand new AI-specific data centers, in addition to replacing the old existing infrastructure. Nvidia’s Blowout Victory Against AI Chip Competitors (Nvidia Unveils Blackwell and GTC) Everything You Need to Know About Nvidia (NVDA) Stock – Crucial Q1 Earnings Update

But didn’t Alphabet earnings just prove AI is a bubble?

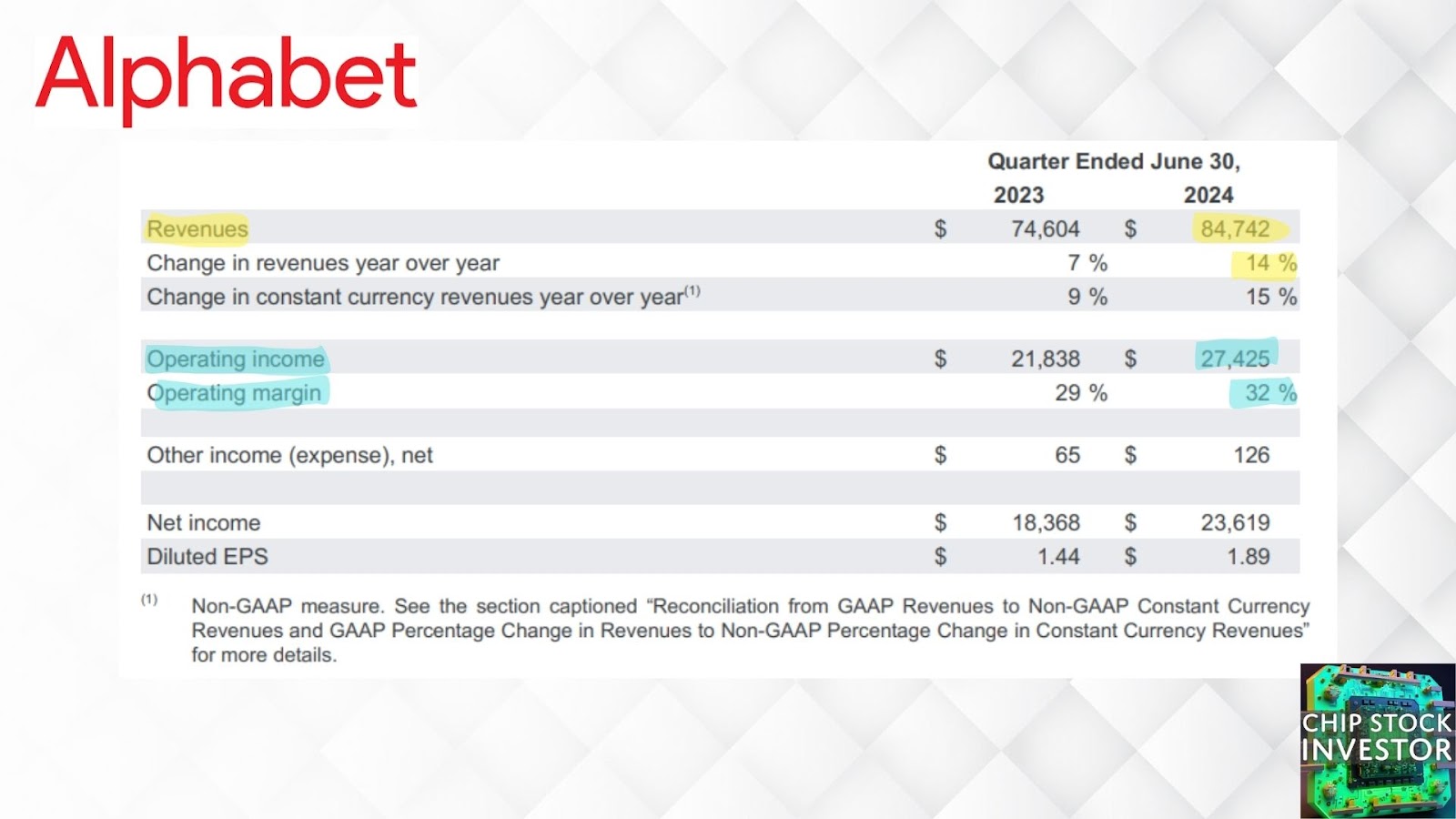

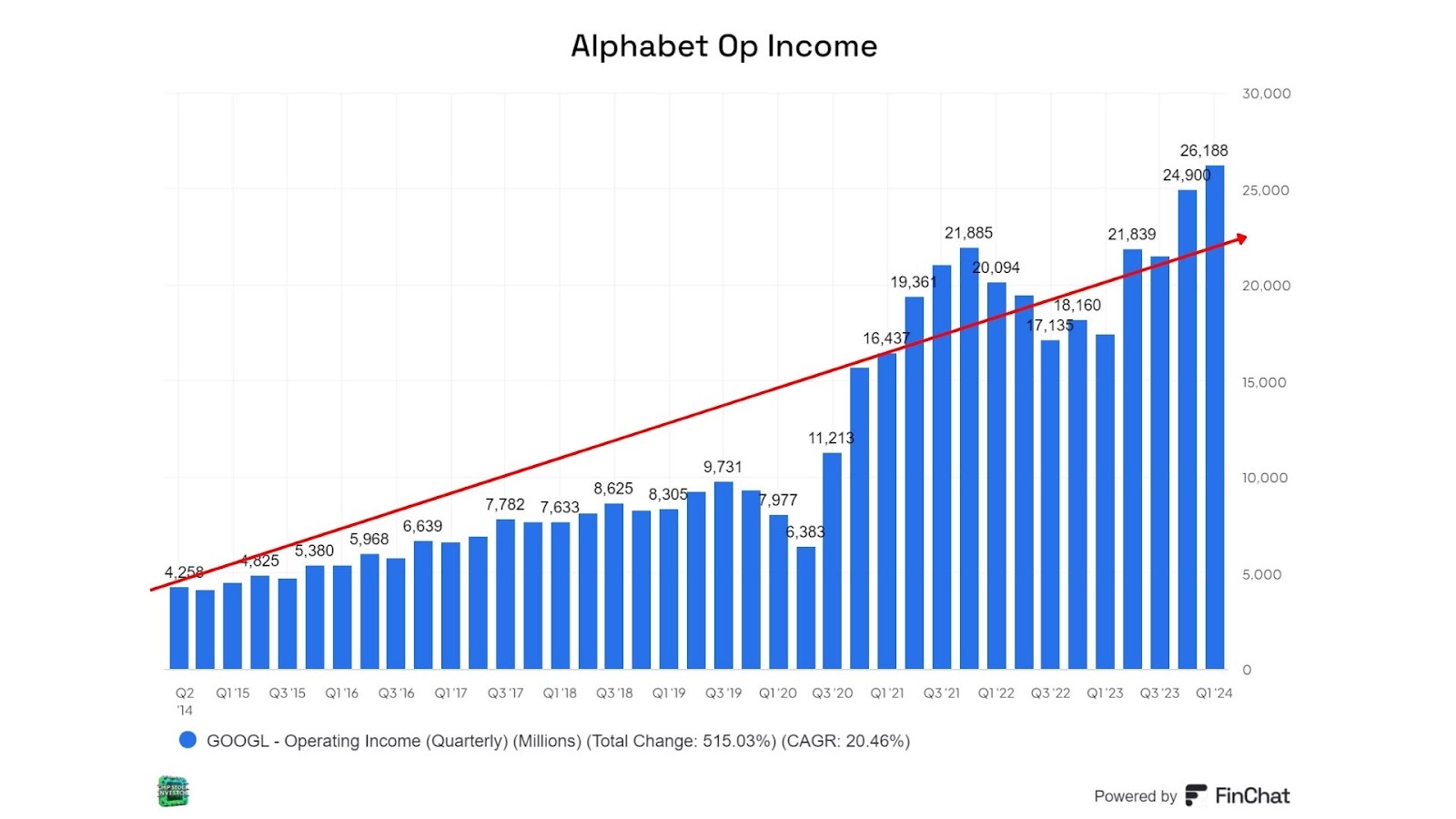

Ok, let’s pivot back to Alphabet (Google) for a moment, and its Q2 2024 update. Revenue and operating profit was significant, as you can see below. The old Google Search and other digital ads business is still growing, but Google Cloud is kicking in some serious growth and profitability too.

Important point above that we’ll circle back to, note one of the ways Google is boosting its operating margins this year compared with 2023 is by reducing employee count. This is the “re-engineering of the cost base” we’ll address momentarily.

But first, look at the pace of capital expenditures (CapEx, spending on property and equipment, like servers and data centers), nearly double what they were in the first half of 2023. CapEx isn’t used to calculate operating income, since CapEx is depreciated over time (depreciation goes into the GAAP operating profit calculation). Given this boom in CapEx, is Google headed for an AI-induced infrastructure crash?

A couple of items point to the answer being no.

- CapEx was low in 2023 because of the bear market, and Google and others were paring back expenses everywhere they could – including in infrastructure spend as they increased the useful lifespan (depreciation) of some of their existing equipment

- CapEx is now simply returning to normal levels after the bear market

- The current CapEx spend isn’t just for AI, its on data center and computing infrastructure in general, as Nvidia’s revenue line item again gives away

This is why we’ve sharing this semiconductor industry end-market cycle chart below. Not only in generative AI infrastructure a brand new market, with an unknown current or future value; existing infrastructure (cloud and enterprise) is just now returning to growth mode after a prolonged drought. Nvidia is gobbling up market share of both of these markets.

This doesn’t mean AI spending is non-existent

Of course, Google and others are spending some (undisclosed) amount of CapEx on AI infrastructure. Alphabet CEO Sundar Pichai mentioned this at the start of the earnings conference call. At $1 billion in AI revenue, but over two million developers and counting working on use cases (at Google Cloud and at its customers), AI revenue is going to keep growing from here. It will be reported as part of the Google Cloud revenue line item.

However, besides just generating new revenue, AI infrastructure is having an effect on operating margins of existing businesses. SVP Philipp Schindler gave but one example of a Google marketing team using AI to get more done with less on the earnings call. The financial community has a tough time grasping follow-on effects of new tech like this.

CFO Ruth Porat (Q2 is her last call as the company’s CFO) hammered the point home by discussing the “re-engineering of the cost base” with higher CapEx for “technical infrastructure” (not just AI infrastructure). This extra CapEx cost is partially being offset by the lower employee count mentioned earlier.

Proof this is just another data center refresh cycle

If you still aren’t convinced this is just yet another data center refresh and upgrade cycle, albeit one heavily favoring Nvidia, take a look at some historic financial metrics below. (Score your own finchat.io subscription with 15% here: https://finchat.io/csi/)

In the first slide, you can see that current CapEx as a percentage of revenue is well within historic norms.

During these periods of higher CapEx, free cash flow (FCF, a non-GAAP metric, not the same as operating income) does take a hit. FCF margin was 21% in Q1 2024, and dipped to 16% in Q2.

Remember, though, that FCF will rally as Google finishes this current data center refresh cycle. Later, as the CapEx is depreciated over time, GAAP operating profit will balance out with the higher depreciation expense from all of the computing infrastructure purchases.

Alphabet is a core position in our portfolio. It knows how to manage its data centers for its big digital ads and fast-growing Google Cloud businesses. This isn’t a data center or AI bubble – at least not yet. Things can change in the future. For now, this is just Google being Google, setting itself up for more future growth and profitability. We’re more than happy to continue holding our position.

What does it mean for Nvidia stock???

As for Nvidia, it’s a new era in which accelerated computing (AI being but one use case for accelerated computing) is front-and-center. Nvidia is going to accrue lots more market share of the existing data center market for the remainder of 2024, and perhaps well into 2025 too.

This risk isn’t an AI bubble. This risk is, and always has been, the inherent cyclicality of infrastructure spending from customers like Google. The difference this time is Nvidia’s tech is hastening the demise of the old CPU server order of things. Based on recent commentary from Google, and chip supplier peers like Micron (MU), this current growth cycle still has legs. Micron’s (MU) Epic Good News For AI Chip Stocks – Time to Buy Now?

Given all the talk about AI, we’re entering a phase of the cycle when the stock price can continue going up detached from any future financial reality. When will the cycle end, and bring the stock price back down? That remains to be seen. Perhaps in 2025, or maybe 2026. It’s too soon to tell. Below is a very general timeline of our predictions for the next 5 to 7 years, for Nvidia, and the semiconductor and computing tech industries at large. We’ll have plenty more analysis along the way.