After mostly taking a hiatus from buying more of the “Fab5” in 2024 – Fab5 meaning ASML, Applied Materials, Lam Research, Tokyo Electron, and KLA Corp – we’ve been warming back up to this group of powerful semiconductor industry companies for 2025.

That said, Lam Research was our Fab5 exception last year. We’ve remained bullish on a gradual recovery of the memory chip market, though there have been some pockets of weakness (trailing-edge commodity memory manufacturing is still in the midst of a downturn, see our last video on SK hynix New Era For Memory Chips – What You Need to Know About SK hynix Stock). As memory chips rebound from the bear market, we took advantage of some periods of volatility to buy some more Lam – which historically derives much of its revenue from memory chipmakers.

After the Q4 calendar year 2024 earnings update, and initial guidance for 2025, is Lam Research stock (LRCX) a value?

As a little preview, Lam and the Fab5 are semiconductor wafer manufacturing equipment providers. But Lam is expanding in new areas. We’ll circle back to this later after reviewing the last quarter and outlook.

Lam updates expectations for the new year

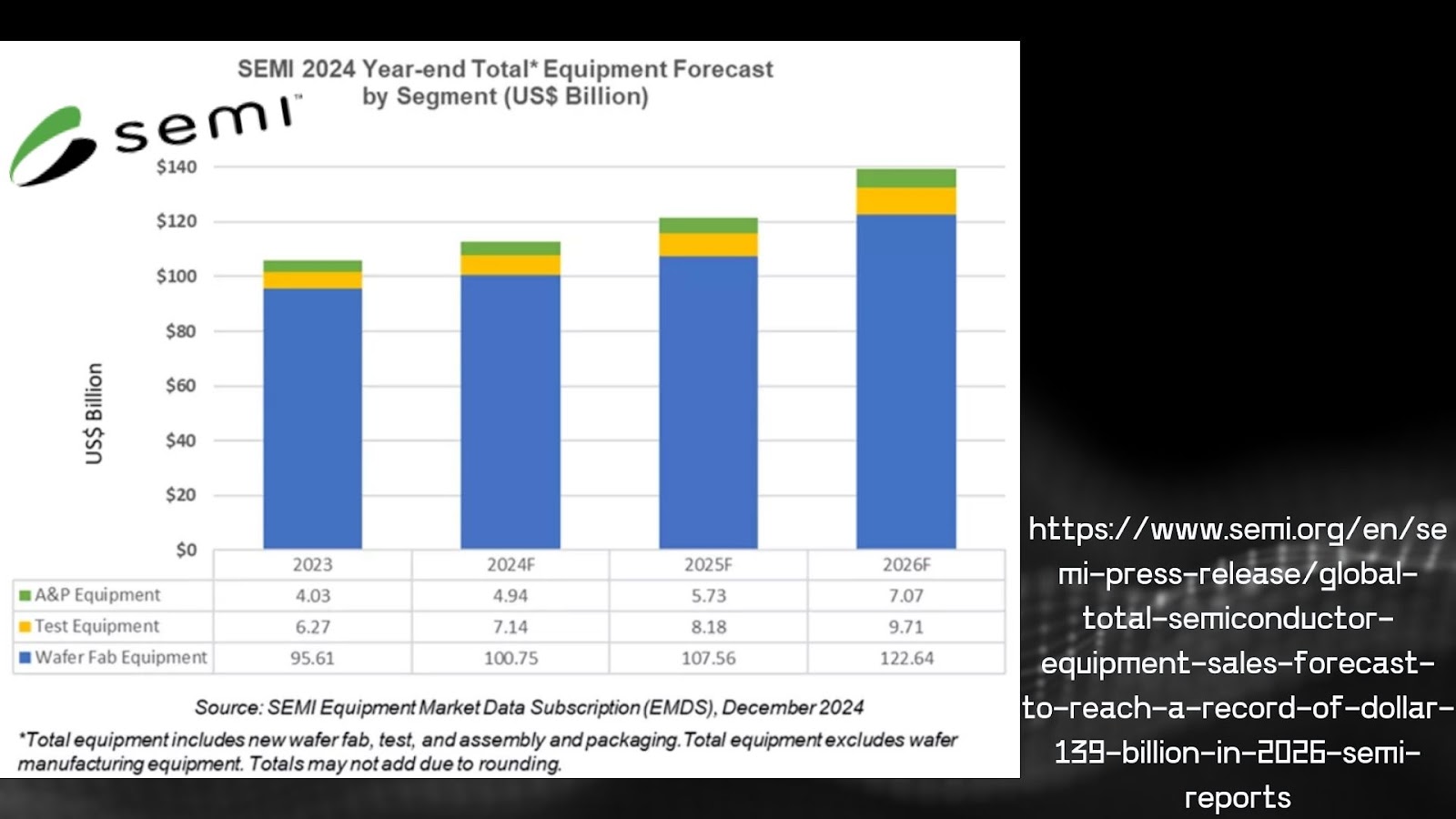

A couple weeks ago when discussing Aehr Test Systems, we showed this chart from SEMI.org on the expected ramp-up of semi fab equipment sales this year and into 2026 (the blue part of the bar chart). Note the expected tepid growth this year, but an expected acceleration of the blue bar’s growth in 2026. This jives with the “U-shaped recovery” we’ve been discussing in other parts of the semi industry supply chain too. Basically, first half of 2025 will be a bit more lackluster for industry sales overall before starting to heat up the second half of the year.

Lam Research management doused just a bit of cold water on the 2025 expectation for fab equipment, stating an expectation for equipment sales to be just a skosh above $100 billion, perhaps a few billion dollars less than SEMI.org’s previous outlook. Blame new U.S. restrictions on equipment sales to China that have extended to more legacy manufacturing processes.

No big deal, though. While Lam did acknowledge it lost a handful of customers in China as a result (it reports these under CSBG, customer service business group), leading-edge fabs are in need of a lot more equipment everywhere else in the world. Lam expects to outpace average growth of its peers in 2025 as a result.

Just one reason why, a few months ago we did a deep dive on Lam’s molybdenum (moly) technology. Closely related to that is the carbon fill process tech. Together, Lam’s moly and carbon processes are driving innovation in high-end NAND memory chips. ASML’s 2025 Outlook Blunder Gets A Bailout – Thanks Lam Research! (LRCX Stock)

Q1 2025 continues the slow-and-steady recovery trend

Lam has been steadily re-growing its sales base on a sequential basis for nearly two years now. Based on the midpoint of guidance for Q1, expect another modest (but still very much respectable) 6% quarter-over-quarter increase in revenue (revenue highlighted in yellow below). Operating margin (highlighted in orange), both on a GAAP and adjusted basis, should also increase a bit sequentially as well from some long-term cost optimization initiatives management has put in place.

Essentially, what we’re seeing here at CSI, is a very generalized guide from Lam management to expect something like mid-teens % (give or take a few percentage points) revenue growth this year, plus maybe a bit of profit margin stabilization or a bit of growth in 2025.

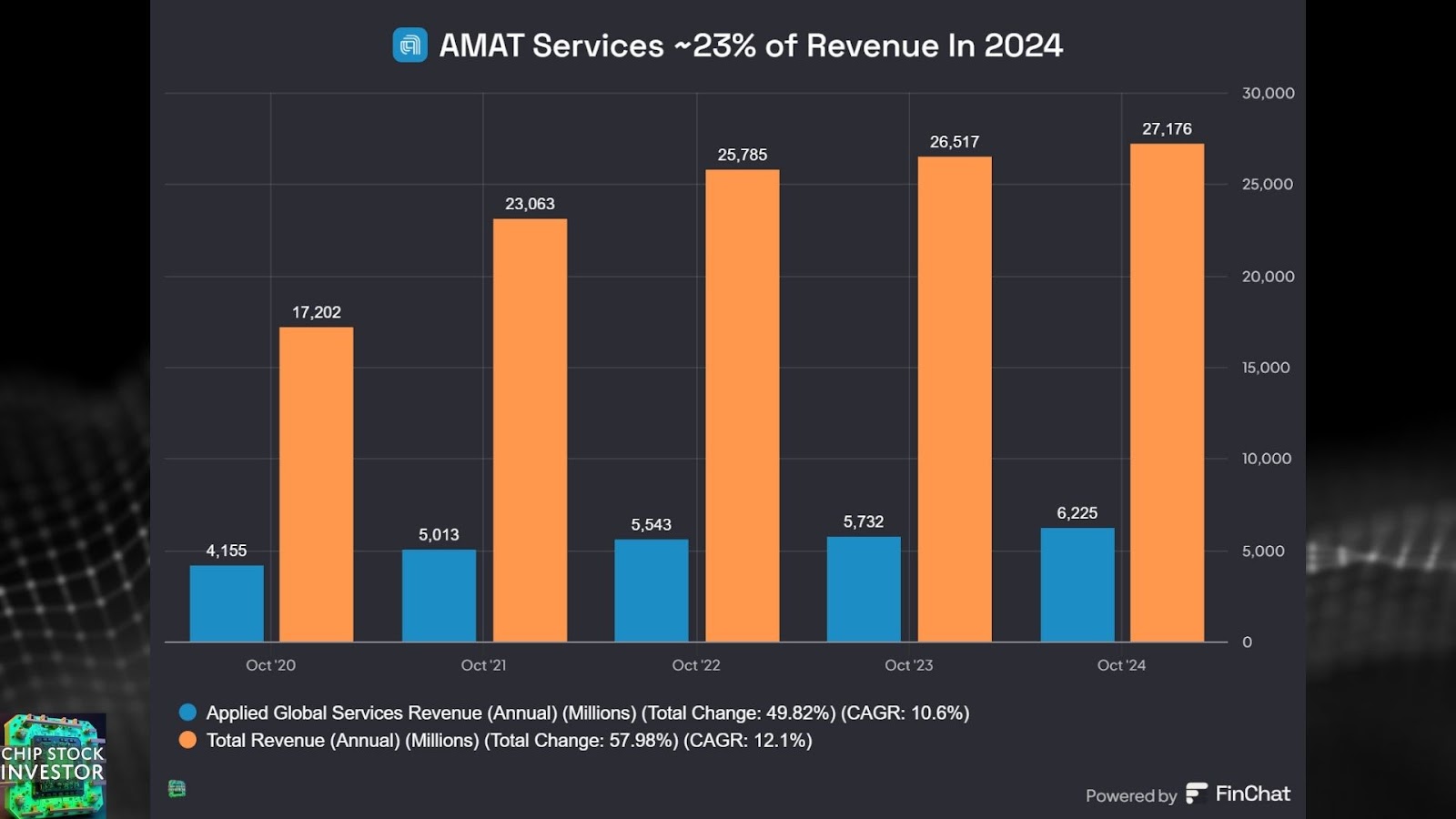

But what about the pink highlight above, correlated to the CSBG segment we mentioned earlier? Yes, there will be some headwinds there, like the loss of some customers in China. However, Lam has some unique things happening in this customer service segment. For the sake of comparison, Lam’s service segment was nearly 40% of revenue last quarter, to about 23% for peer Applied Materials’ service segment (called AGS, Applied Global Services).

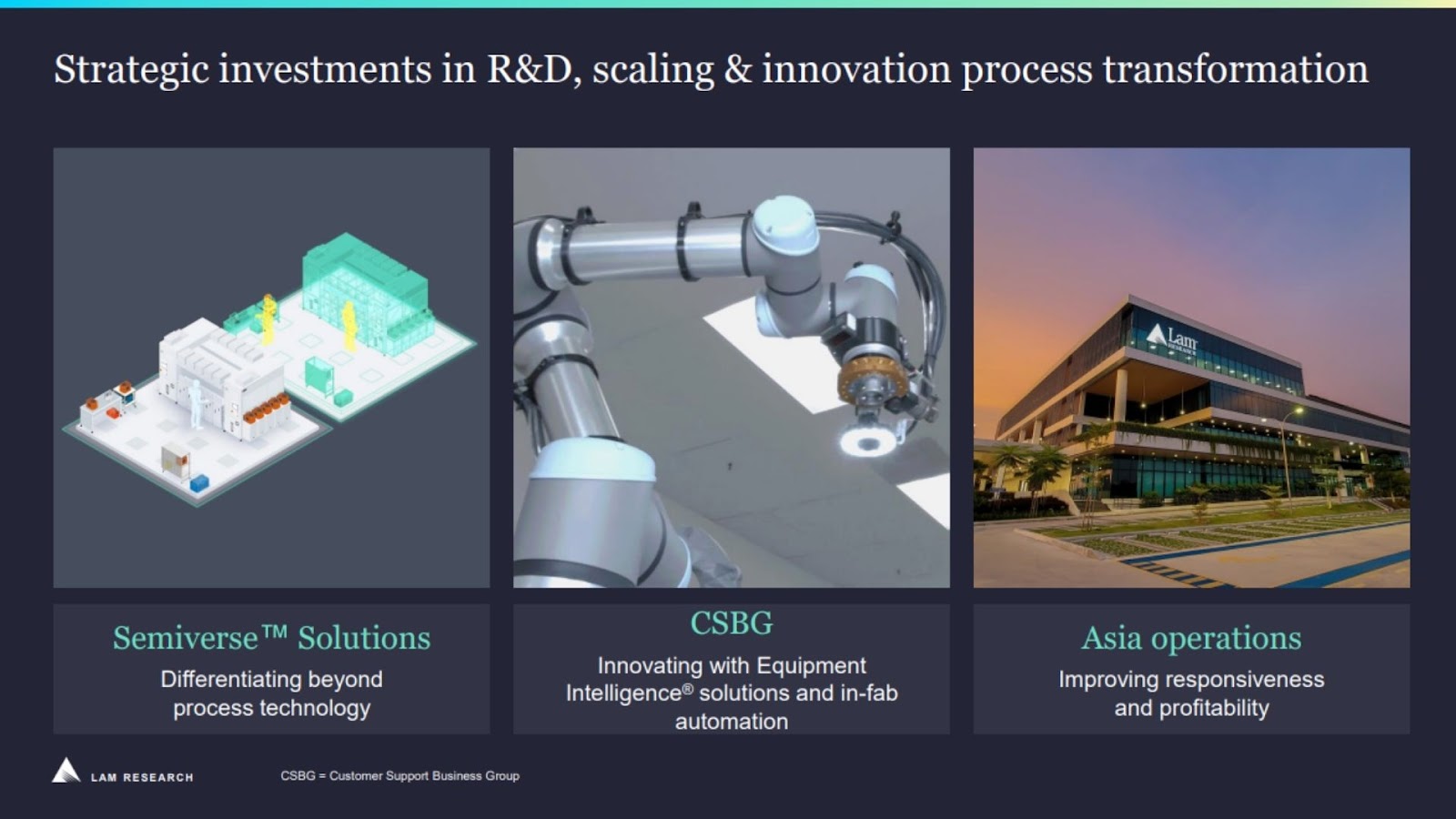

Lam’s next big batch of innovations in CSBG

In the last year or so, we did some work explaining how Lam stayed steady through the bear market (on the profitability front, anyways) thanks to CSBG services like helping memory chipmakers repurpose existing equipment. Not exactly sexy, but Lam has the goods to weather some severe downturns.

But now it’s time to look at some more exciting developments for its customer service segment: Physics simulation software and cobots.

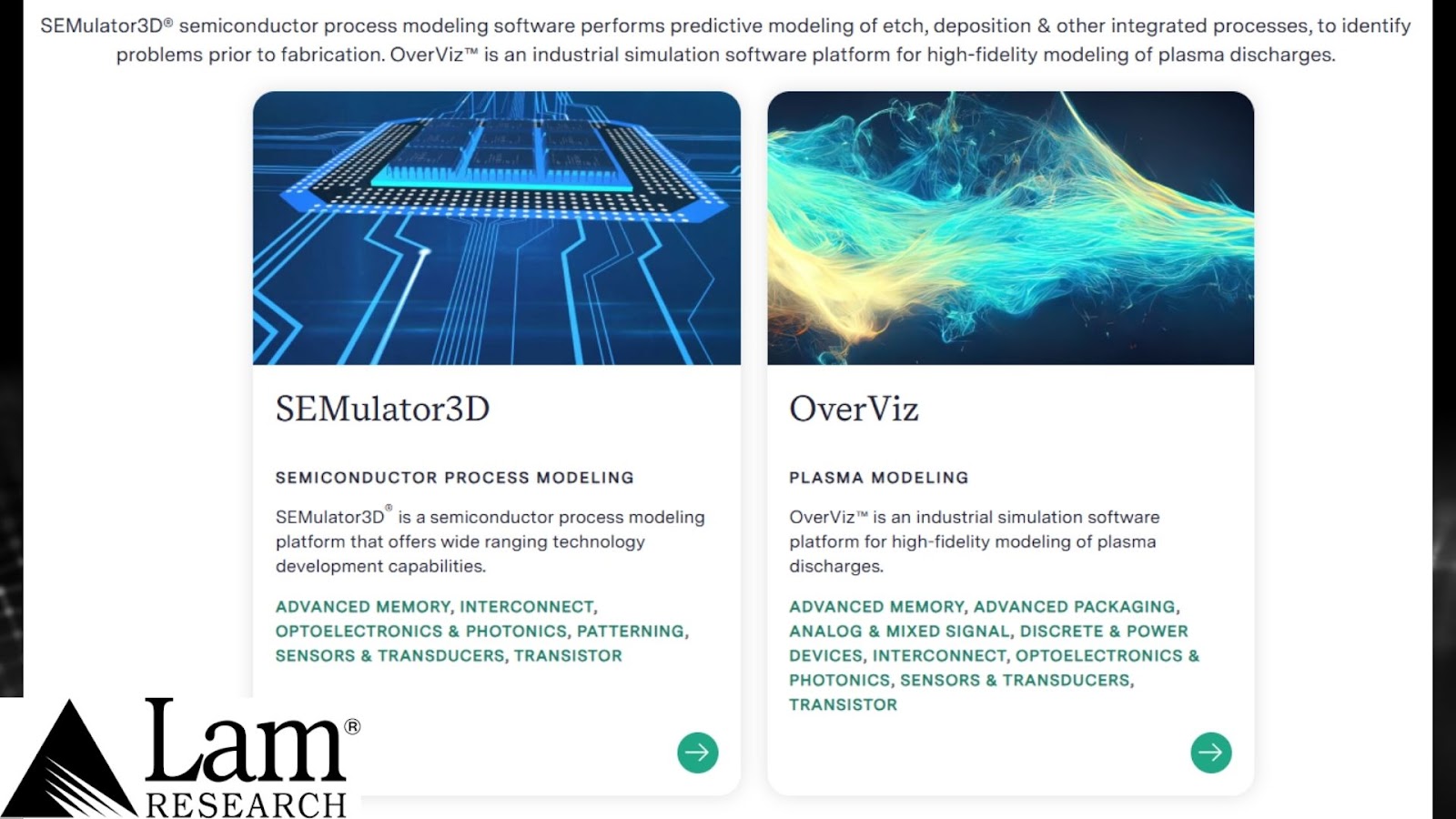

- “Semiverse” software solutions

First up, we have what Lam calls its “Semiverse Solutions.” Sort of sounds like Nvidia’s Omniverse, 3D graphics and digital twin simulation software used to build things virtually before building them in real life? Very possible Lam built these tools with some help from Nvidia Omniverse APIs.

But what are they? There are two primary solutions, SEMulator3D and OverViz.

SEMulator3D was designed to help early on in the development process for new semiconductor manufacturing processes. As process technology gets more complex – and expensive – this tool creates a virtual creation of what the microscopic 3D structures on a silicon wafer would look like after running them through a new manufacturing process. https://www.lamresearch.com/products/semulator3d/

As for OverViz, it’s a plasma (the “fourth state of matter”) physics simulation software suite. Plasma is, of course, used in various steps of wafer development, like deposition (PECVD, for example), “dry” etching, and ion implantation. OverViz helps with solving the complex physics problems involved in running these manufacturing processes using plasma. https://www.lamresearch.com/products/overviz/

These software tools illustrate how companies like Lam have been quietly expanding into enterprise software – in this case, software for semiconductor manufacturers. But there’s some overlap with EDA, especially when thinking about how the EDA software providers like Synopsys and Cadence Design have been acquiring physics simulation engines. Perhaps the Synopsys-ANSYS mega-merger comes to mind…

- “Dextro” fab cobots

The other big innovation going on at Lam’s CSBG is in relation to challenges with so many new fabs being built around the world. There are serious challenges involved in sourcing talent to operate these manufacturing facilities – talent that may not even be readily available to recruit (a challenge TSMC has been facing building its new fabs in Arizona, for example).

In December, Lam announced its “Dextro” cobot (a portmanteau of “collaborative” and “robot”). Dextro is essentially a robotic arm that can perform various tasks in a chip fab. Not as cool as a humanoid robot that can fully replace a human. But then again, we’re still a ways off from that horror story (or total liberation from all life monotony? We’re not sure yet) becoming a reality. Cobots are a nice happy compromise. You can see Dextro hard at work, under human supervision, here: https://www.lamresearch.com/product/dextro/

The point? Lam is breaking out of its fab equipment roots in another direction: End-market tech equipment and devices. Perhaps Dextro is just the beginning, like what fellow semi equipment company Teradyne has been trying to do with its small robotics segments (Teradyne owns Universal Robots and MiR).

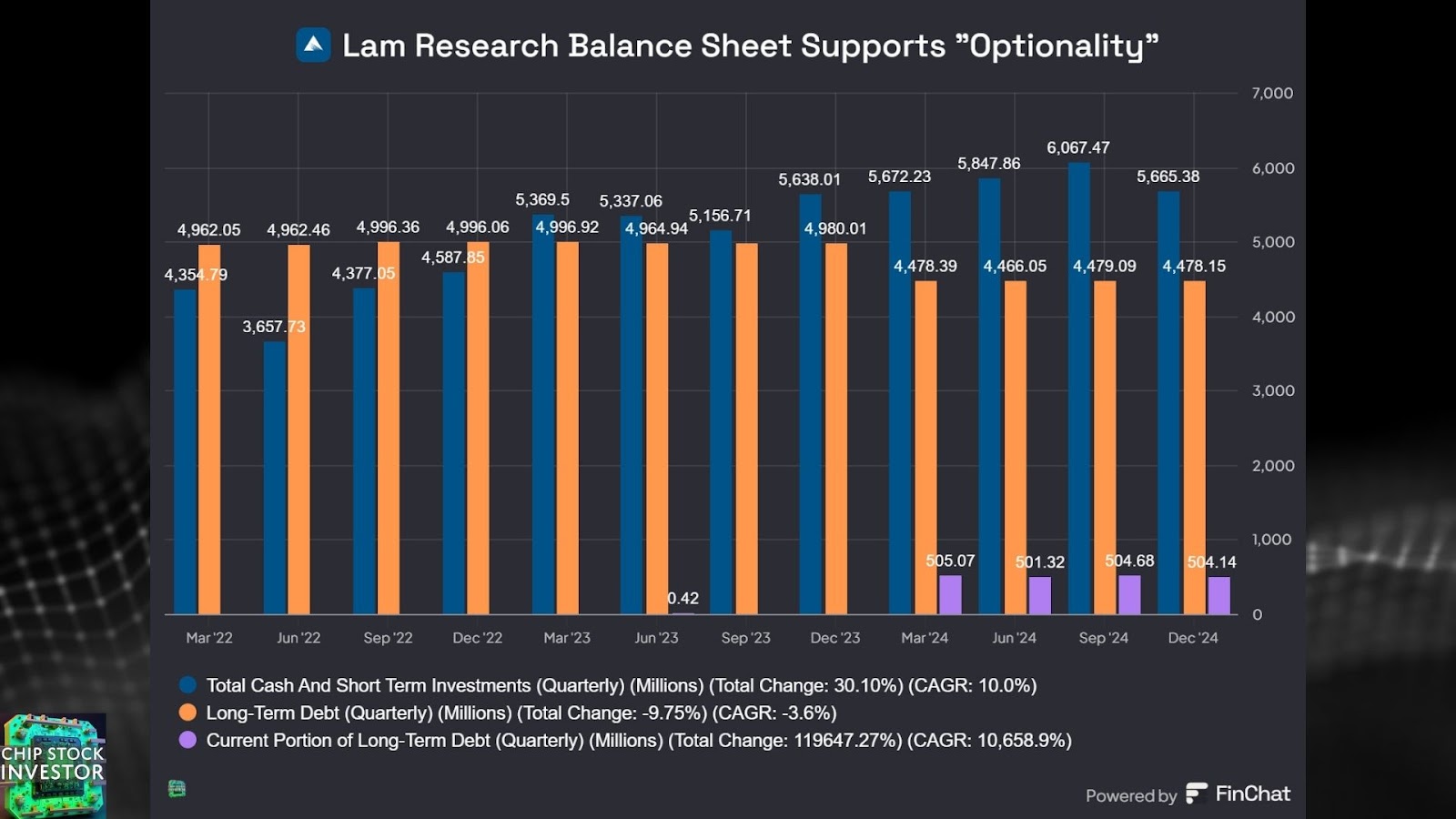

Be it more enterprise software, robotics, or something else, Lam has “optionality” built in with a solid balance sheet and more net cash flowing in every quarter. FYI, management said it will be paying off the ~$500 million in debt that matures this year with cash.

Some updates on valuation – is LRCX a value?

Ok, fun to take a stroll along innovation road, but the bulk of Lam’s financials today come from selling good-ole fashioned semiconductor manufacturing equipment. And that could be plenty good enough with revenue and profit forecasted to continue expanding through 2026 from the current fab growth cycle.

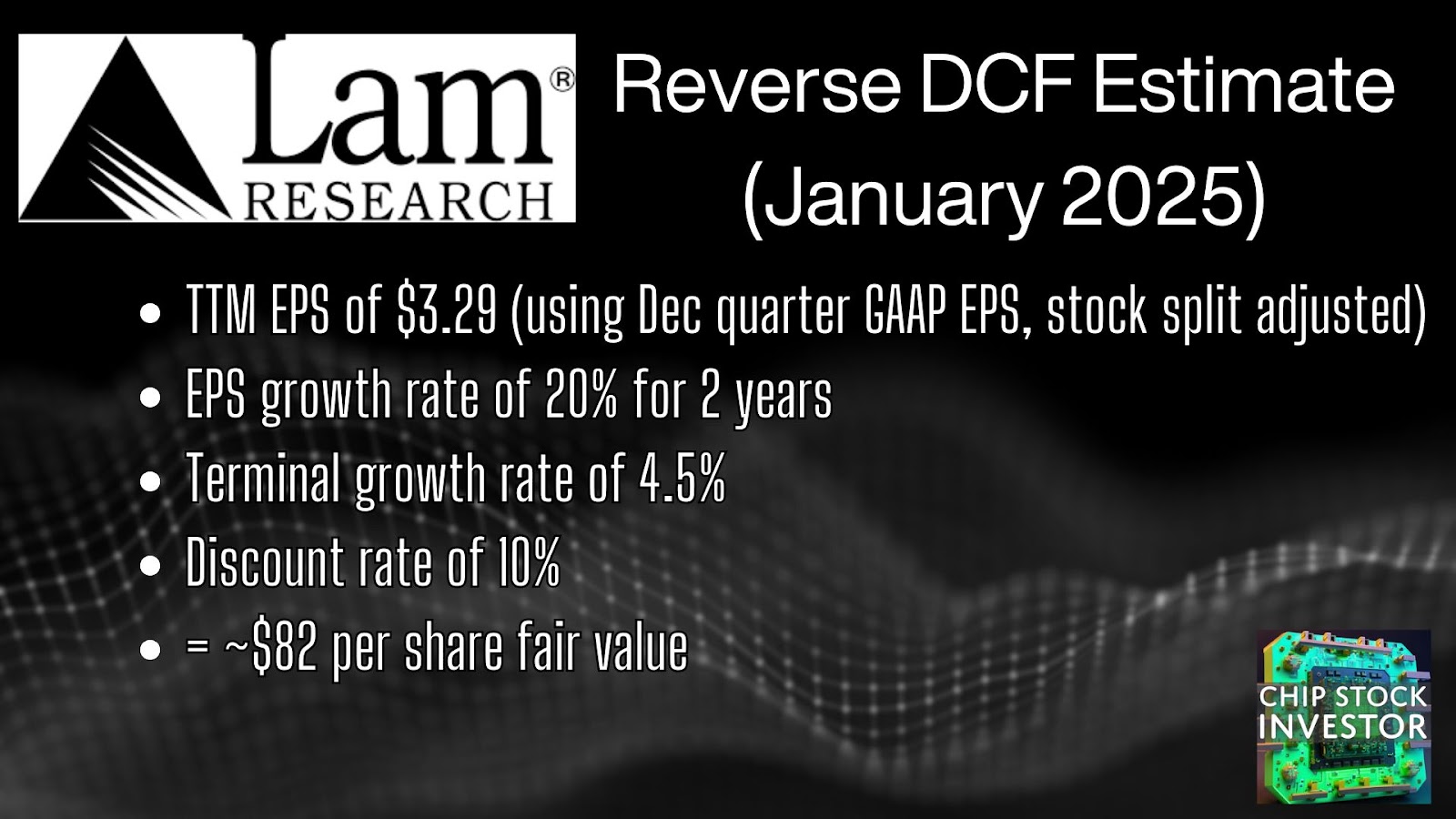

With that in mind, we plugged in a few updated numbers to our reverse DCF (discounted cash flow) from a few months ago. Not much has changed, but we continue to believe earnings (using GAAP earnings per share) are set to continue growing at a brisk pace for a couple years. We’ve kept the terminal growth rate beyond that at 4.5% to account for a period of temporary cyclical decline at some point (2027? 2028?).

Remember, this is a reverse DCF. It isn’t our prediction of Lam’s trajectory. Rather, it’s just one possible scenario we think is likely baked into the current stock price (currently at $81.50 for LRCX stock as we write). From here, it’s now up to each investor to decide if the above expectations (or a different scenario that gets the reverse DCF to current stock price) is a reasonable hurdle for Lam Research to meet or clear. If yes, it could indicate LRCX is a value – if the assumptions prove correct over the next two years and beyond.

As for us here at CSI, we are still very pleased with our position in Lam Research, and the rest of the Fab5 too. Signs point towards 2025 being a good year as advanced chip fabs need to install some upgrades. See our updates on TSMC (here: Investing In Chip Stocks? TSM Report Reveals the 2025 Winners) and SK hynix (same link as earlier, here: New Era For Memory Chips – What You Need to Know About SK hynix Stock) for more on the current state of advanced semiconductor fabrication.