Up to this point, we haven’t had much to say about Apple‘s (AAPL) lack of play in the artificial intelligence (AI) race. AI isn’t an imminent threat to Apple’s business. However, the going narrative was that, with companies like OpenAI and Apple services partner Google making rapid advances in intelligent consumer-facing software, Apple would lose relevancy over time.

And yet, the market hasn’t cared much as Apple stock has soared higher this year. Once again, media narrative and storytelling, and what investors really want, aren’t the same thing.

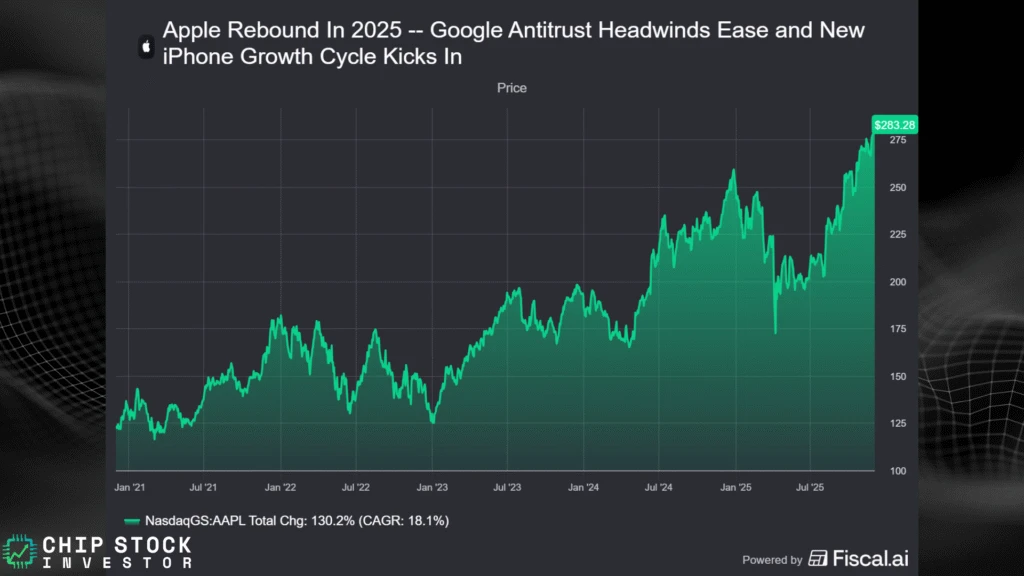

What’s actually behind Apple’s rebound to new all-time-highs in 2025? The answer is quite simple.

1. Alphabet gets some reprieve in the courtroom

We’ve done a series of videos the last few years on Apple’s reliance on Alphabet’s Google Search as a source of revenue growth — and the tight relationship between the two (Google pays Apple to be the default search engine on the Safari web browser) has been in the spotlight during Alphabet’s antitrust trial.

See the video linked at the top of this article for more on Apple’s revenue from Google. Here’s the time stamp link on the relevant part of the discussion: https://youtu.be/1Y5Yo0vwd5c?t=451

So the first reason Apple has rallied this year? Google didn’t get an all-out win on its Search and Ads antitrust, but investors now have some clarity on future changes that may need to occur between the two tech giants. Thus, just as Alphabet stock has rallied on this clarity, so has Apple. Google Stock: The Real Reason It’s Doubled (It’s Not Just AI)

2. A new iPhone cycle has begun

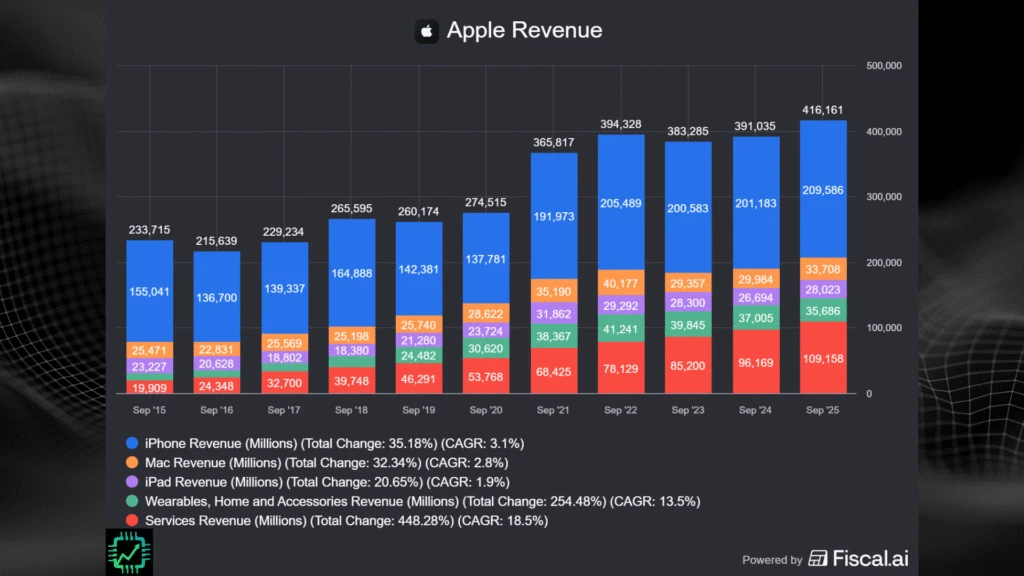

Apple’s recently wrapped fiscal 2025 (12 months ended every September) was the start of a more earnest iPhone upgrade cycle. Apple Intelligence may not be much of a hit, but the 17th generation iPhones are selling very well. There could be more upside in the company’s biggest revenue segment as a result ($210 billion in iPhone revenue in fiscal 2025, the highest since the $205 billion reported in fiscal 2022).

And as we discussed a few weeks ago in the chip supplier blog post (2 Apple Chip Suppliers Are Merging — Key Investing Lessons), Apple wields incredible control over its supply chain. The result is big increases in earnings per share (EPS) when Apple hits a new hardware growth cycle. Fiscal 2025 EPS increased 22%, though revenue was up only a modest 6.4%.

With EPS back in double-digit expansion, Apple has once again proven why it deserves a premium valuation — even if the extent of that premium is up for debate (one-year forward P/E and P/FCF both around 33x expected fiscal 2026 EPS and free cash flow).

Read all our analysis, access a growing library of technology supply chain tools, and join a community of like-minded long-term investors! Just $10 a month if paid annually. Chipstockinvestor.com/membership

3. Apple has time to figure out AI monetization (services)

To be clear, Apple’s limited AI feature set could crop up as a future problem. Consumer-facing software companies like OpenAI are moving fast and deepening engagement with users, which could “abstract” (to borrow the software dev term) the importance of hardware — Apple’s real bread-and-butter.

But companies like OpenAI themselves prove the limited economic viability of AI assistants for investors, at least in their current form of monetization. Even as OpenAI approaches 1 billion monthly active users by the end of 2025, it’s the business use cases for AI that hold real promise. OpenAI recently announced it had reached 1 million business customers in November, a sign that monetization beyond free-to-use and consumer subscriptions is heating up. https://openai.com/index/1-million-businesses-putting-ai-to-work/

Apple is primarily a consumer-facing company. Its services segment continues to be a top source of more consistent growth, one that could face some headwinds from the Google Ad revenue sharing at some point in the future. But Apple could have time to figure out how its own AI could be unlocked for the millions of businesses that also use Apple hardware — adding a valuable and much-needed enterprise revenue stream to Apple’s service segment.

This is no doubt part of the behind-the-scenes discussion at Apple. The company just announced Amar Subramanya (previously VP of AI at Microsoft, and head of engineering Google Gemini before that) will be taking over Apple’s AI efforts. Rumor has it “Tim Apple” Cook himself might also be retiring. If so, a more pronounced strategic shift could begin.

In the meantime, we’re happy Apple investors via its inclusion as a top holding in a couple of Vanguard tech ETFs.

See you over on Semi Insider for more!

One Response

great report, thank you