It would seem the answer to the title question is “yes” considering the compressed valuations paired with enduring growth for many enterprise SaaS stocks in 2025.

Yet the threat of new AI agent startups, vibe coding, and pricing pressure has many investors feeling like enterprise SaaS is still a pass. The massive underlying technology shift that Nvidia (NVDA) kicked off (accelerated computing) has put a lot of pressure on software companies to keep up, limiting the visibility on future software profit growth.

Perhaps the biggest indication, though, is from enterprise software companies themselves — from data management to cybersecurity to digital ads and entertainment. Just this last month, a handful of new acquisitions have been announced (and more rumored). A few examples might help inform portfolio decisions as we head into 2026.

Hint: The market still likes broad scale and revenue growth, but also promise of future profitable growth. And a deal… investors really want deep value in software.

IBM’s spending spree on consulting makes a pivot to more SaaS

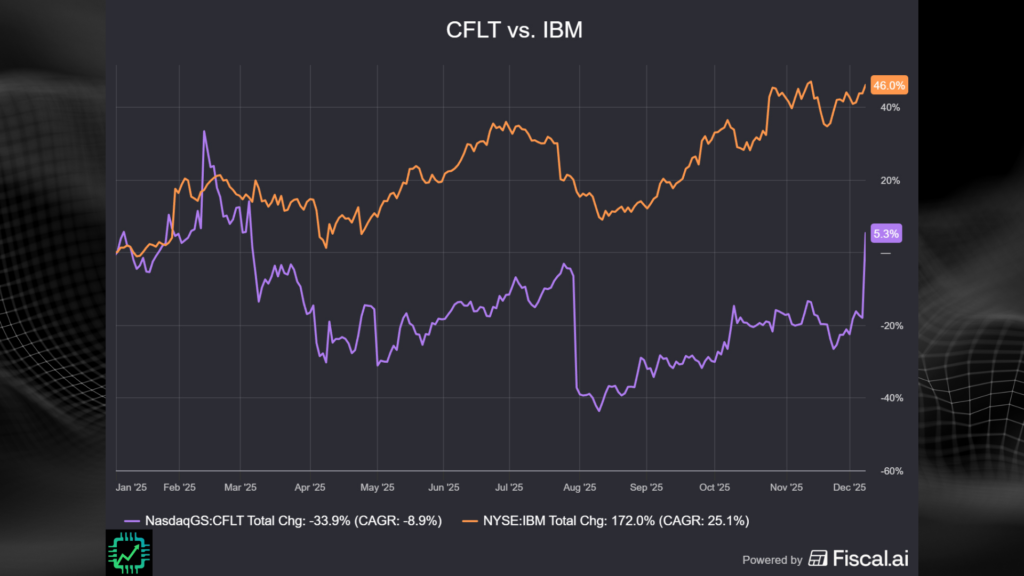

The latest enterprise SaaS M&A deal to be announced was by none other than ancient tech conglomerate International Business Machines (IBM). “Big Blue” is acquiring Confluent (CFLT), one of the 2021 IPO class of SaaS stocks that helps with real-time data storage and processing. Think of this like a software infrastructure play akin to what Salesforce (CRM) just did with its Informatica acquisition. IBM will be paying $11 billion in cash for the purchase.

IBM’s strategy under CEO Arvind Krishna (took over in 2020) has shifted the company from heavy on managed hardware infrastructure (Kyndryl (KD) spin-off in 2021) to asset light software and IT consulting services (a very long string of small consultancy and cloud software acquisitions, see here).

But the acquisition strategy might be pivoting. Early in 2025, it completed to purchase of cloud automation company Hashicorp for $6.4 billion, and now Confluent. IBM wants to capture more companies at the cusp of their own IT and data transformation for the AI era. Now that it has that “top of the economic hierarchy” piece in place, it’s rebuilding its cloud software plumbing to help its customers execute on needed changes it has consulted them on.

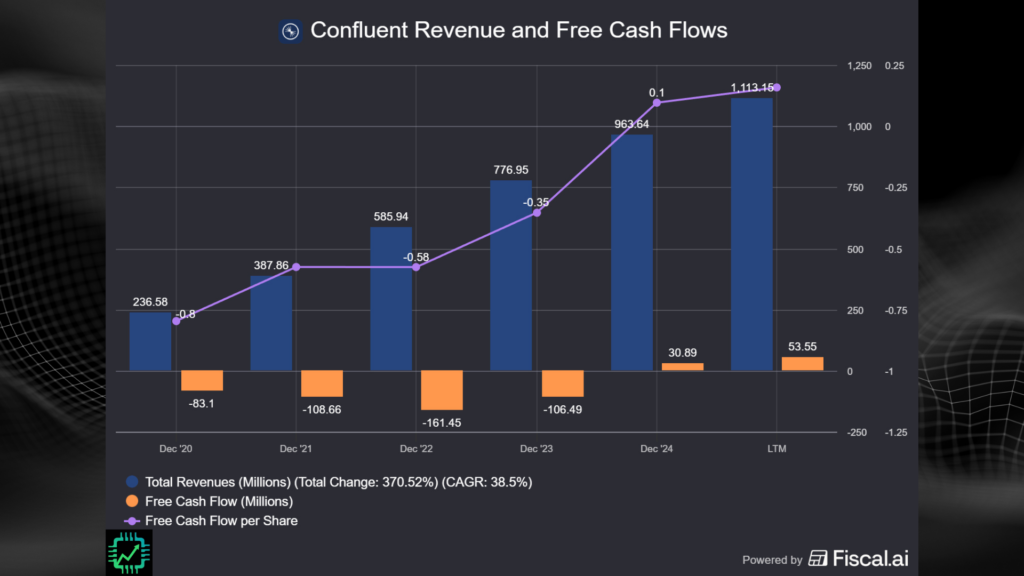

Wall St. has awarded IBM a higher earnings metric on this increased breadth and depth on cloud and AI consultancy. Confluent, essentially a point product without a lot of breadth and depth, has not been rewarded at all. Worry has been persistent about Confluent’s crowded market, disruption, as well as slowing free cash flow growth (on a per-share basis shown below, as is our norm here at Chip Stock Investor). IBM’s offer provides an exit for this struggling SaaS’s investors.

Want to dive deep into company analysis and make financial visuals like these? Check out Fiscal.ai, and get 15% using our link! Fiscal.ai/csi/

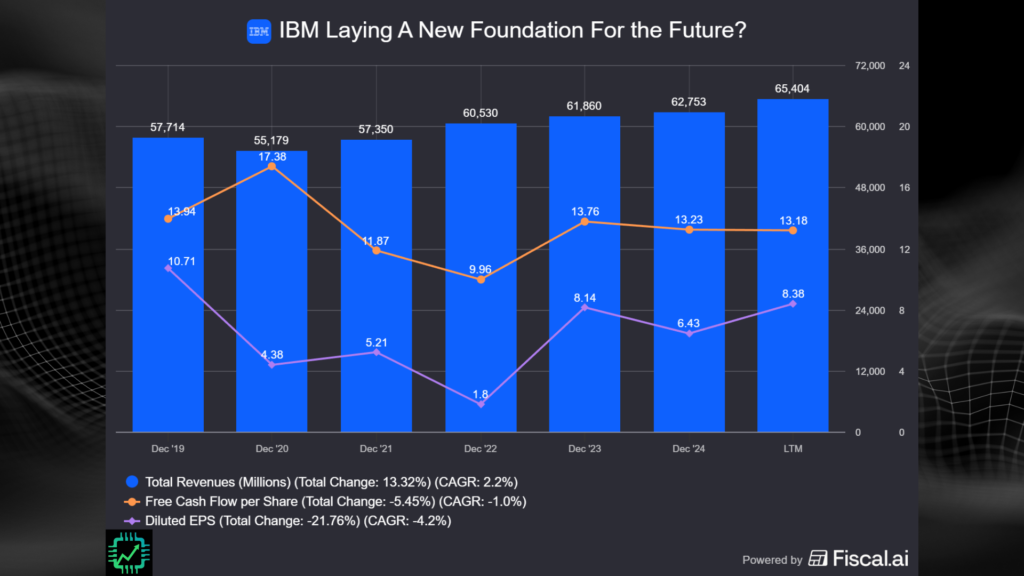

Now by contrast, it’s not as if IBM’s profit growth has taken off. On the contrary, AI and the development cycle it has kicked off has put pressure on this old stalwart — really, a pesky problem that’s been plaguing IBM for nearly two decades now as it has fallen behind younger peers.

Nevertheless, scale and durability of business (real or perceived) during the shift to accelerated computing is what investors want right now. While IBM doesn’t meet our personal needs, it appears the company is laying a foundation that should keep it in moderate growth mode for years to come.

ServiceNow more than a SaaS stock split story

ServiceNow‘s (NOW) 5-for-1 stock split will be completed after market close on December 17th. Investors haven’t cared. ServiceNow has been sold off this last year. But is it worry about AI disruption, or something more fundamental like a high valuation that needs to moderate?

ServiceNow has also chosen to go on the acquisition hunt to get itself ready for AI agents and launch into new enterprise SaaS product categories (like CRM, the domain of Salesforce). Its latest move? Small privately owned identity security startup Veza.

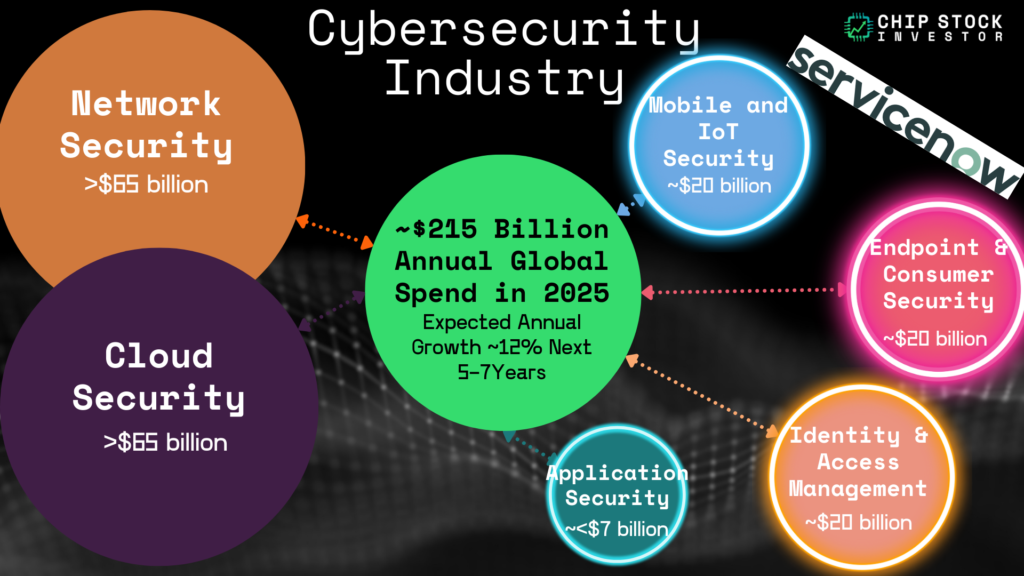

It may come as a surprise to some that, amongst other things, ServiceNow is also a cybersecurity company. Its focus up to this point has been in various support services for IT teams. But adding in identity access management for AI agents (controlling the who, or more specifically what, gets access to an organizations data) puts it more squarely in the cybersecurity software product arena. Veza competitors would include Okta (OKTA), SailPont (SAIL) — and to a certain extent, also CyberArk (CYBR), which is soon to be part of big cyber platform Palo Alto Networks (PANW).

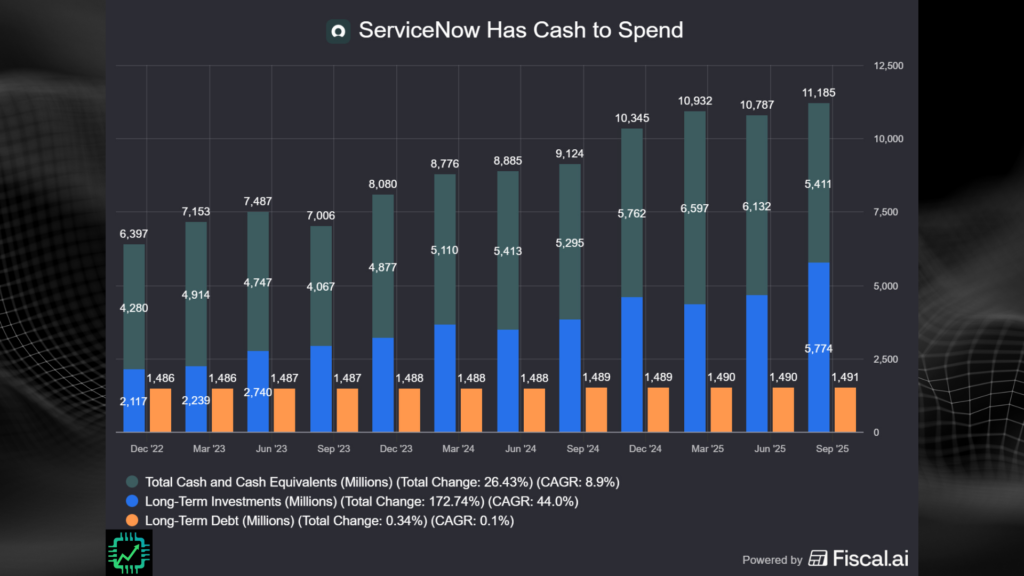

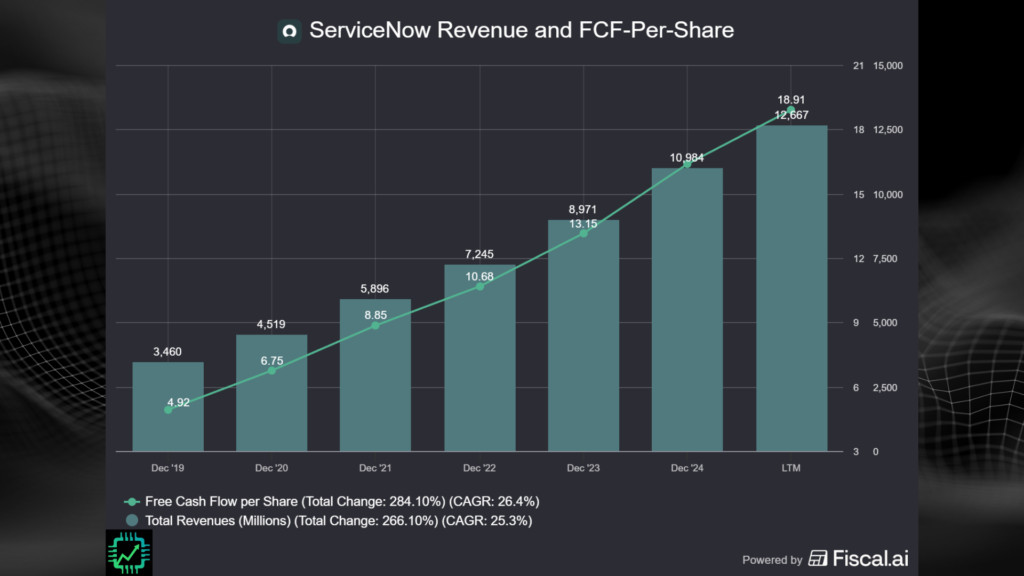

ServiceNow certainly has the cash to deploy on these small bolt-on purchases, nearing $10 billion in net cash and investments over and above a small amount of debt. And ServiceNow’s free cash flow-per-share growth has continued at a healthy pace even this year as development on new AI products has ramped up. What’s the market’s problem headed into the new year?

Indeed it would seem, at least to us, it’s really as simple as valuation. With uncertain future payoff for all this AI activity and startup AI product acquisition, the market took a healthy look at ServiceNow’s valuation late in 2024 and is moderating it. Even after another correction, shares trade for ~45x trailing-12-month free cash flow, and around 35x expected next-12-month free cash flow. So… still a bit of a premium price.

When we finally started buying ServiceNow stock over the last two years, it was a view to holding for many years in the future during this pivot to AI automation. We’ve seen no reason to lose patience.

Join us over on Semi Insider for more write-ups and live events regarding enterprise SaaS investments for 2026, including our “benchmarking” of this portion of our portfolio to indices like the Vanguard IT Index Fund (VGT) and the software-focused iShares Expanded Tech-Software Sector ETF (IGV). And remember to watch that latest Salesforce update, in which we discuss some of our other recent software SaaS stock purchases.