Over on Semi Insider, we’ve been discussing where value can be found as 2026 gets rolling. The digital payments industry, and finance sector at large (a top consumer of all things IT), is one such area. Below is an excerpt from the article series on how blockchain technology has matured, and is now actually producing revenue-generating businesses.

As you may have heard, the Trump administration announced an executive order to impose an interest rate cap of 10% on credit card debt, effective January 20, 2026. https://x.com/WhiteHouse/status/2009799629442035968

While it’s unlikely to hold up as-is (the industry itself has stated the economics don’t work, not to mention the legal battle that will ensue), it does illustrate the ongoing pressure to reduce friction in the U.S. credit and digital payments market. The U.S. DOJ is still working on its Visa (V) debit card antitrust case; and Visa and Mastercard (MA) also published their final proposed settlement for interchange fee litigation.

The concern among banks and lenders with the interest rate cap is it could reduce availability of consumer credit, which in turn could hurt usage of digital payments networks.

Not to mention there’s the whole blockchain and crypto industry gunning for a slice of this pie too. Let’s talk about that a little bit. But first, we need to answer the question: How does a “legacy” digital transaction work?

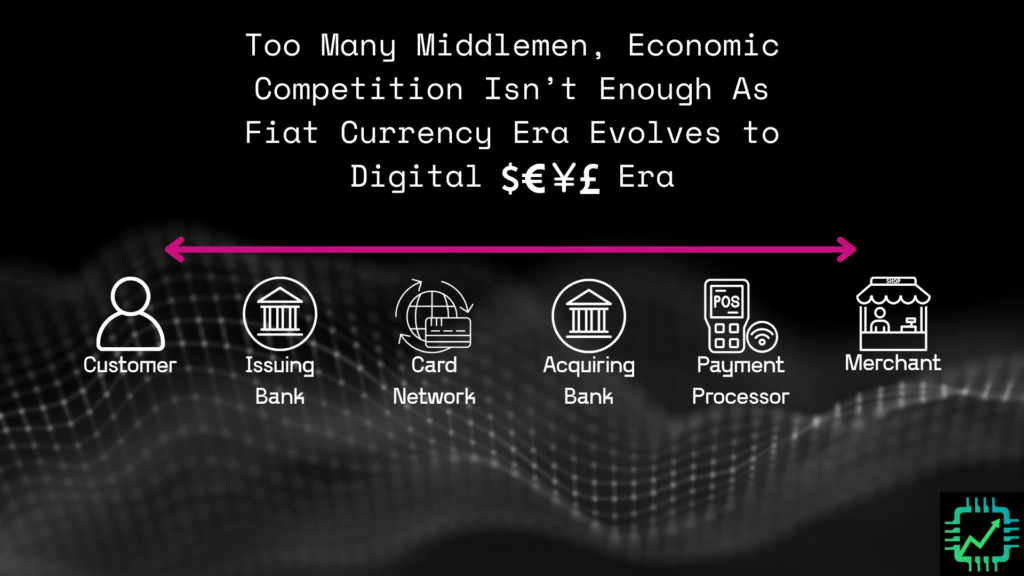

How do traditional digital payments work?

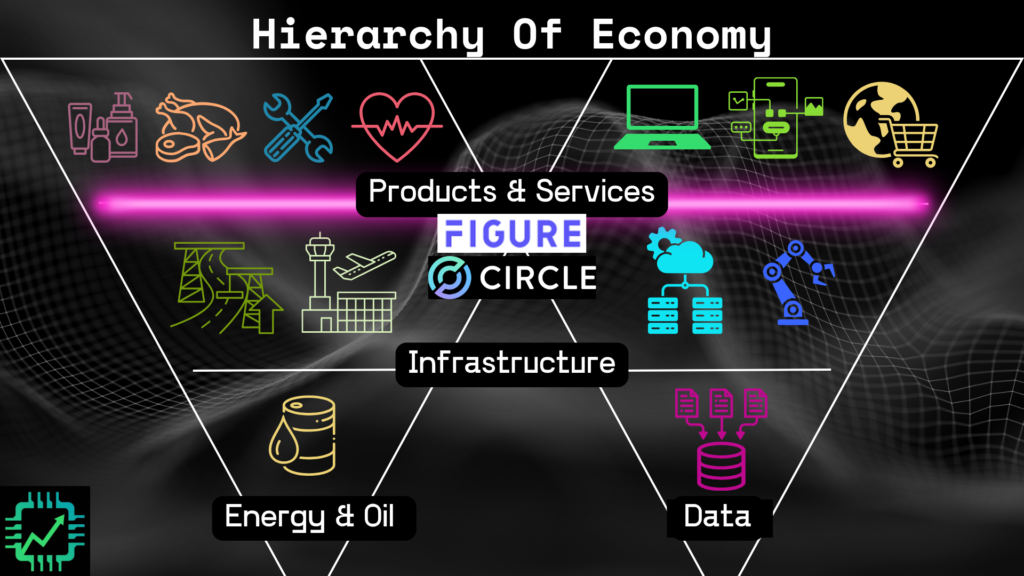

Two IPOs in 2025 illustrate this next push into the massive market that is digitizing money and money flows: Circle Internet Group (CRCL) and Figure Technology Solutions (FIGR).

In this article, we’ll address Circle and how it makes money off of stablecoins (which in turn could help reduce digital payments friction from expenses). To understand this, we need an understanding of how a traditional digital payments transaction works.

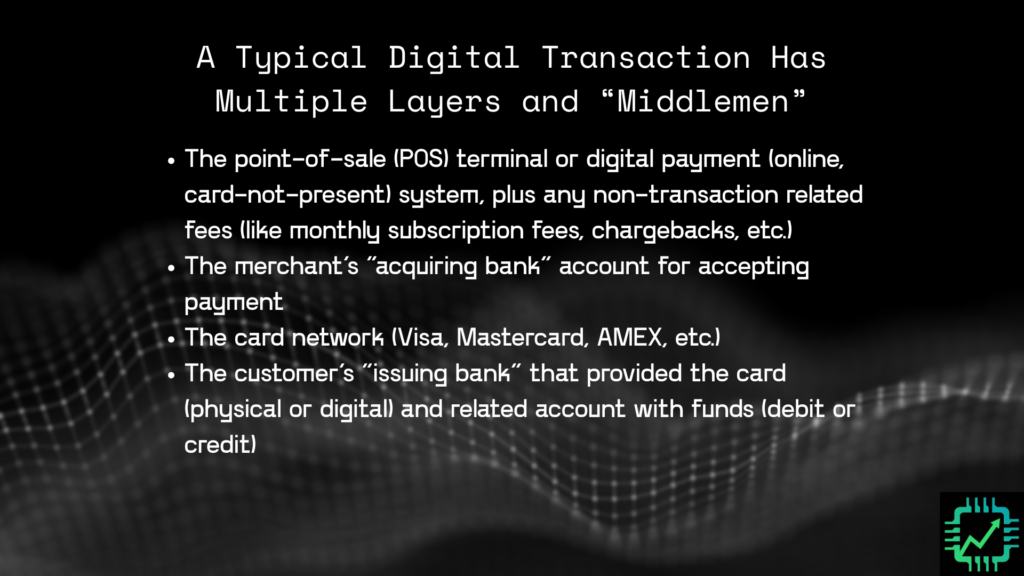

First, let’s define all the players that get a cut of a digital transaction. Each of these players gets a cut when a card is swiped (in-person transaction) or when a virtual card (online transaction) is made, plus separate assessment fees card networks charge banks for transaction processing and network usage. The ultimate interchange fee (usually paid by the merchant to the bank) is variable, depending on if the card is credit or debit, the card network (Visa, Mastercard, American Express, etc.), if the customer’s card has a rewards program, the type of merchant itself (certain merchants deemed to be higher risk pay a higher interchange fee), and so on.

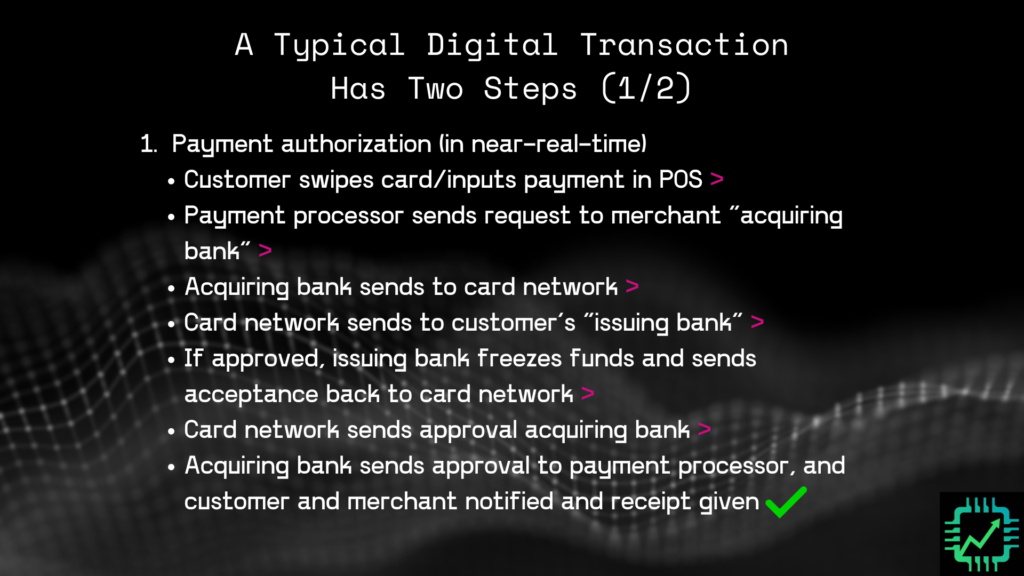

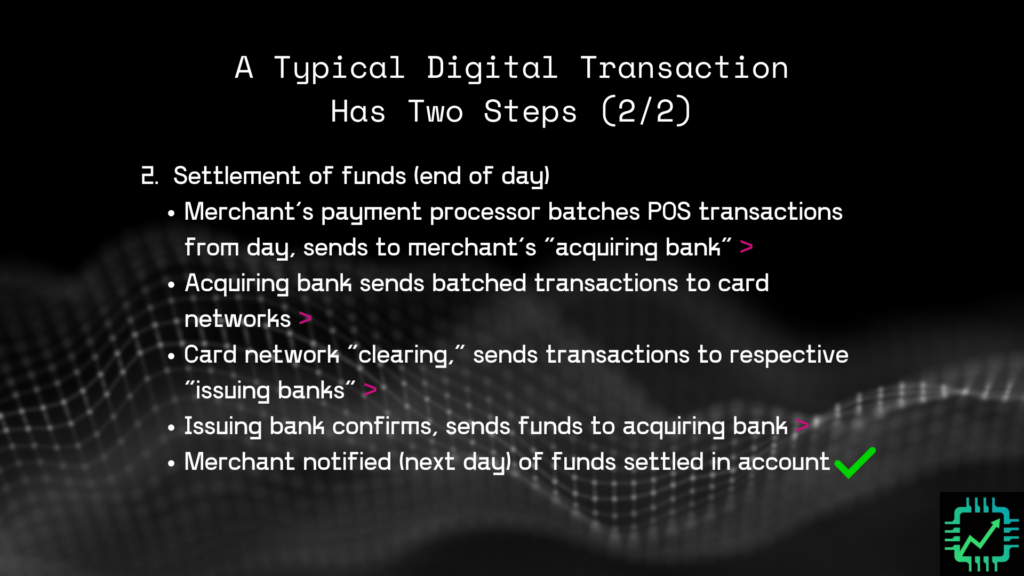

The transaction itself gets processed in two steps: 1. Payment authorization, and 2. Settlement of funds.

As you may have noted, card networks never actually touch or handle any funds and transfers, let alone earn any money from credit card interest charged by the bank. So absent any destruction of consumer usage of digital payments, a cap on credit card interest rates wouldn’t affect companies like Visa and Mastercard, and their respective global data center-based tollbooth business.

But what about a stablecoin company like Circle? It too isn’t earning any revenue from interest on consumer credit. As the technological disruptor of (some of) the status quo in digital payments middlemen, it might actually benefit from downward pressure on traditional banking and consumer credit markets (banks looking for alternative ways to grow their balance sheet assets).

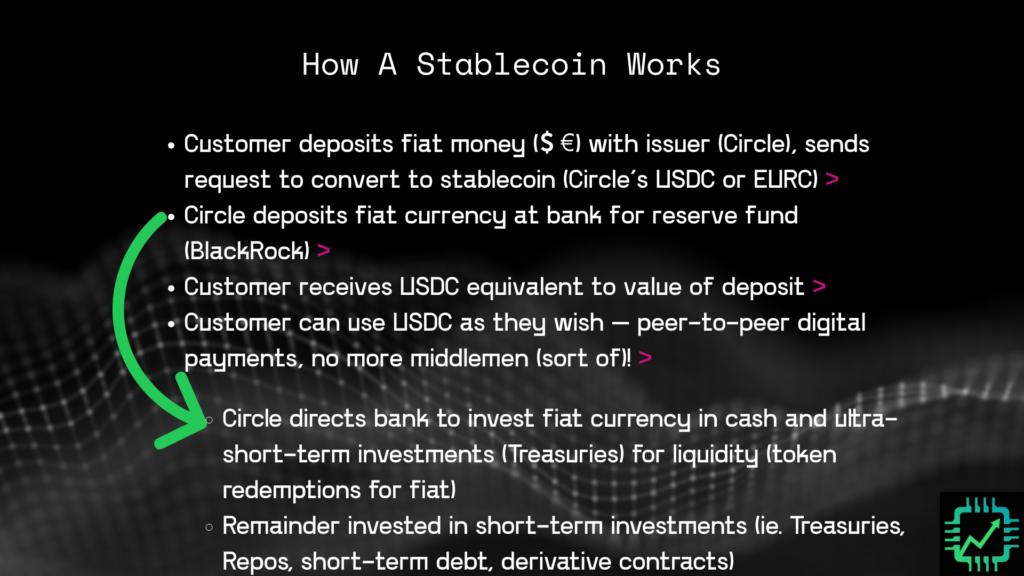

How a stablecoin works as a digital payments facilitator

In contrast, here’s how a stablecoin works. Hint: It winds up making a stablecoin issuer like Circle operate more like a traditional bank, less a card network operator like Visa.

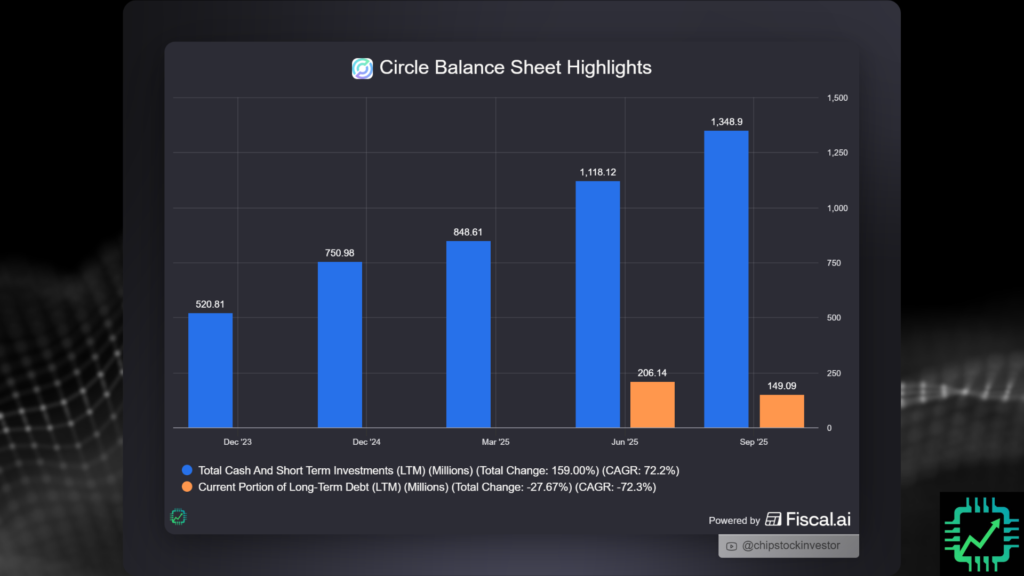

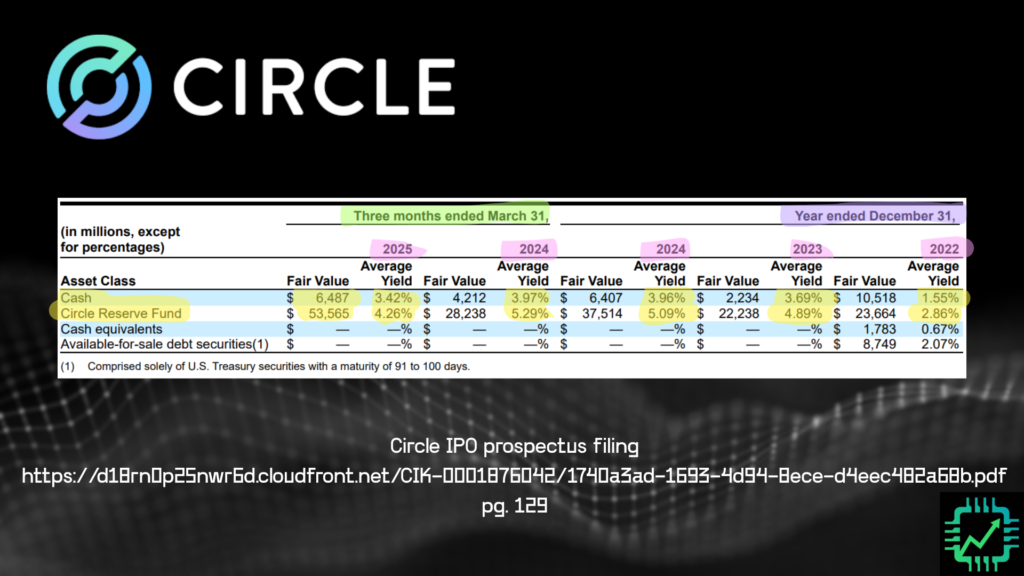

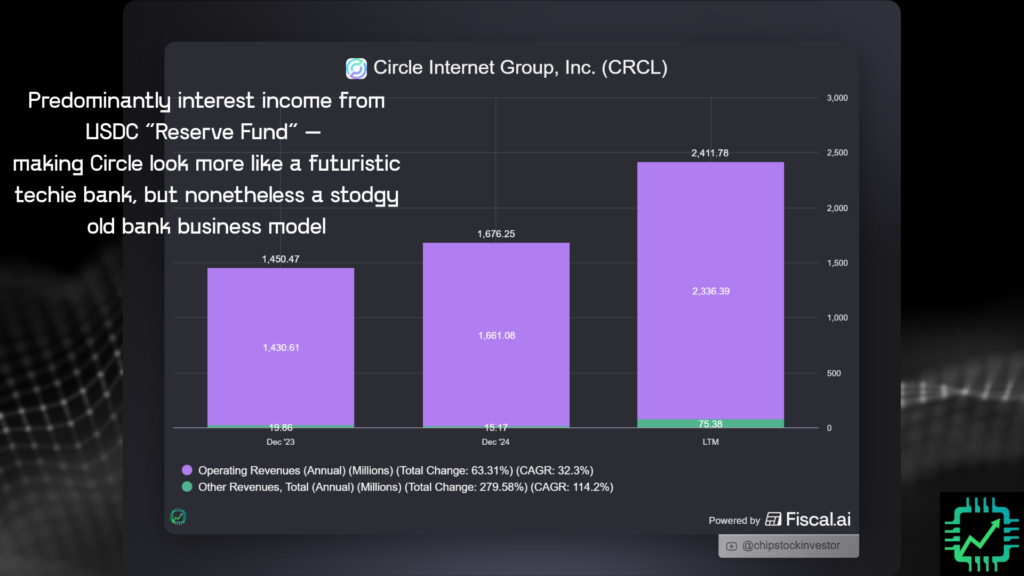

For the most part, after Circle accepts the fiat currency and provides an equivalent amount of stablecoin (USDC in this case) for customers to use, it’s the fiat currency deposit (cash and short-term investment equivalents on the balance sheet) that gets invested and interest income earned off of it (managed by Blackrock) that earns Circle revenue.

Want to make finance visuals like the one above? Fiscal.ai just reduced its pricing on subscriptions! Plus get an additional 15% off using our partner link: Fiscal.ai/csi/

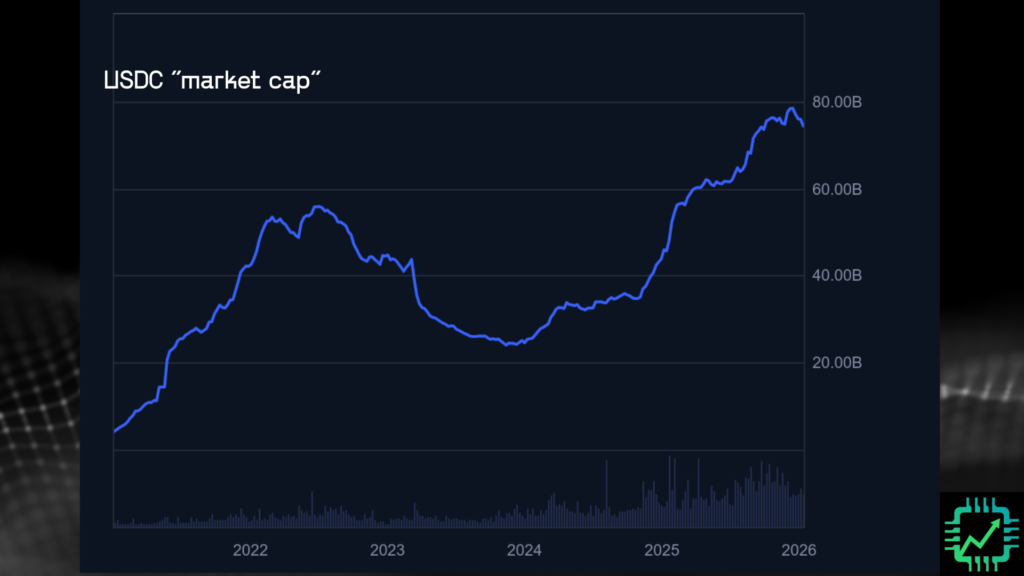

Thus, similar to a bank, growing customer deposits (balance sheet assets) and increasing the value of total USDC in circulation (USDC “market cap”) is ultimately what will help Circle’s business grow. Rather than being susceptible to credit card interest rate risk, Circle is affected by short-term interest rates (like those set by the U.S. Federal Reserve) that affects cash and short-term equivalent yields.

Fun fact: Card networks like Visa can also perform settlement services for stablecoins too. So blockchain technology like this isn’t a total disruptor of traditional digital payments networks. The bigger risk from the rise of stablecoins, as well as pressure on consumer credit interest rates, is to the banks.

With time and increased adoption, stablecoin networks like Circle will also be able to increase their technology offerings to partners — like security, data, and related software. This has been a great value-add for shareholders of Visa and Mastercard over the years. But at this early stage, Circle operates in similar fashion to a non-credit lending bank.

There are ample risks to this model as Circle expands its reach and usage. But we like it as part of our small bets basket of stocks and potential disruptor of digital payments. Next up on our fintech software journey, we’ll discuss Figure and its consumer credit business utilizing blockchain technology.

See you over on Semi Insider for more of the discussion!