Over the weekend, Micron Technology (MU) announced it’s buying a new fab from one of Taiwan’s smaller semiconductor foundries, Powerchip Semiconductor Manufacturing (or just PSMC, TWSE:6770).

On the surface, Micron’s move is simple: Spend $1.8 billion, get a bunch of new DRAM manufacturing capacity ready for the second half of 2027 — DRAM being the memory chip type needed to make high-bandwidth memory (HBM) co-packaged close to AI data center GPUs.

The simple announcement could send ripples throughout the electronics manufacturing supply chain in the coming years. Here’s why.

The portion of the supply chain we’re discussing today

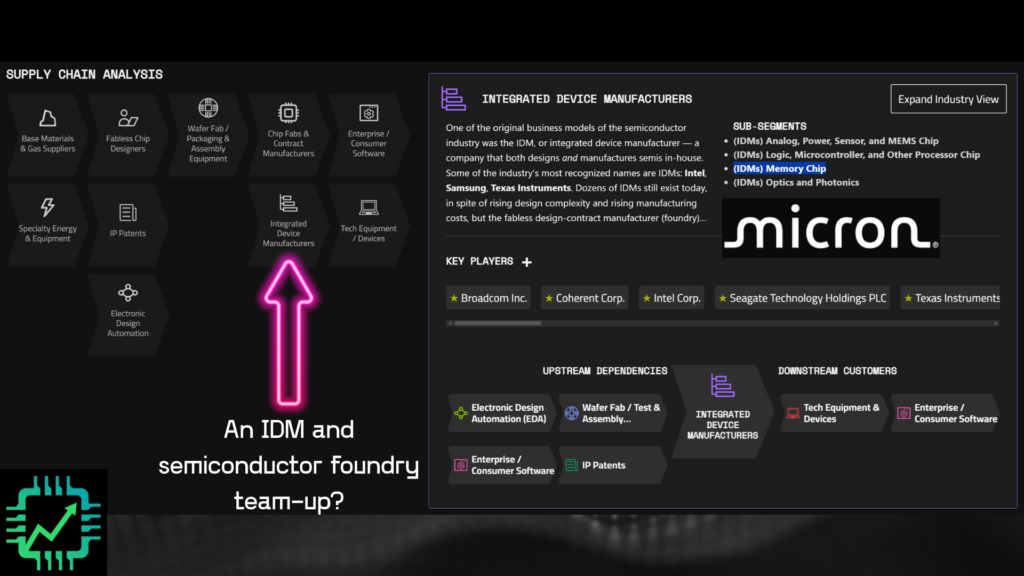

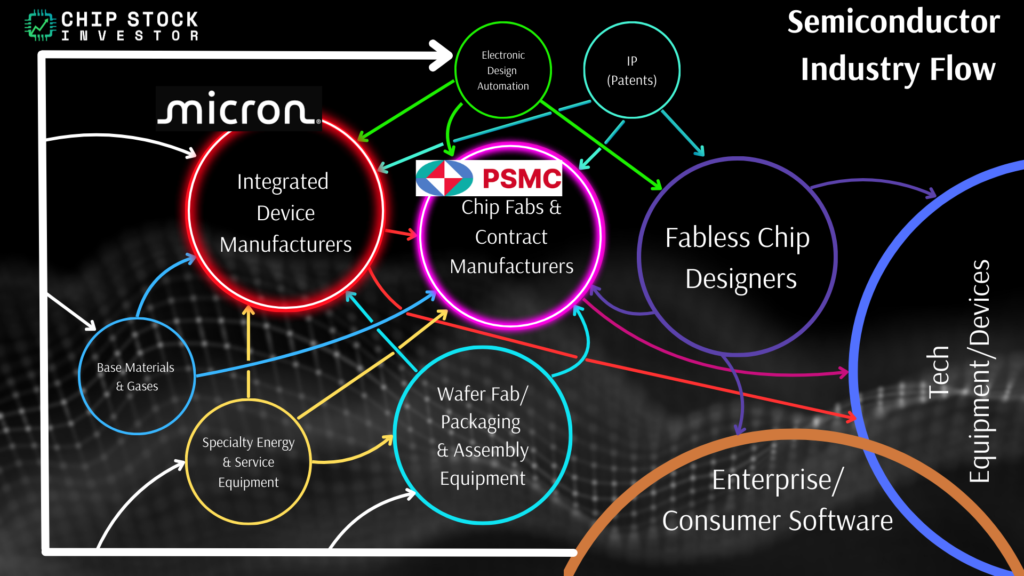

Here’s the visual from the Supply Chain Analysis section of the research dashboard (join us over on Semi Insider for more details). IDMs (like Micron) do most of their own product design and manufacturing in-house. PSMC, by contrast, is a foundry. Most of its customers are fabless designers, that rely on a company like PSMC for semiconductor wafer development and testing.

Or if you prefer our old-school supply chain chart. Some IDMs have begun to outsource some manufacturing to foundries, but Micron’s deal with PSMC is going to take out some foundry capacity in a semiconductor industry end market that has been down in the dumps the last couple of years.

First an intro to PSMC

Actually, we’ve already met PSMC here at CSI in mid-2025. Taiwan Semiconductor Manufacturing (TSM) said it would be phasing out its high-voltage gallium nitride (GaN) processes by 2027, and as a result, GaN design startup Navitas Semiconductor (NVTS) said it would be transitioning to PSMC and its specialty GaN manufacturing foundry as a result. Public blog article here: Enough Navitas, Time For Some Gravitas – Why Investors Need to Cool It With NVTS Stock

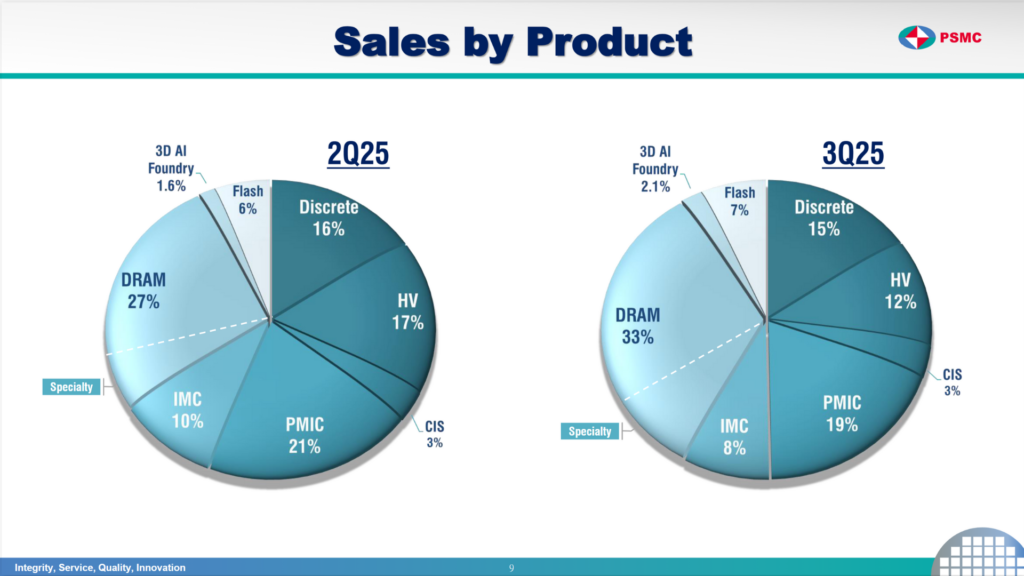

The name “Powerchip” might sound misleading, though. Power management applications are but one of many applications the foundry provides. In fact, power applications are a small part of PSMC’s total business. Below are PSMC’s revenue segments as of Q3 2025. PMIC (power management integrated circuit) and HV (high-voltage) were 19% and 12%, respectively, of sales.

But notice a big chunk of PSMC’s manufacturing process revenue is from memory? The company reported 33% of sales for DRAM and 7% for NAND flash in Q3 2025. We’ve often talked about how the memory IDM market has consolidated down to just a handful of players, but that doesn’t mean there aren’t a few small suppliers outside of the IDM model (the IDMs tend to keep most of their capacity for their own in-house designed products). PSMC would be one of these small memory suppliers.

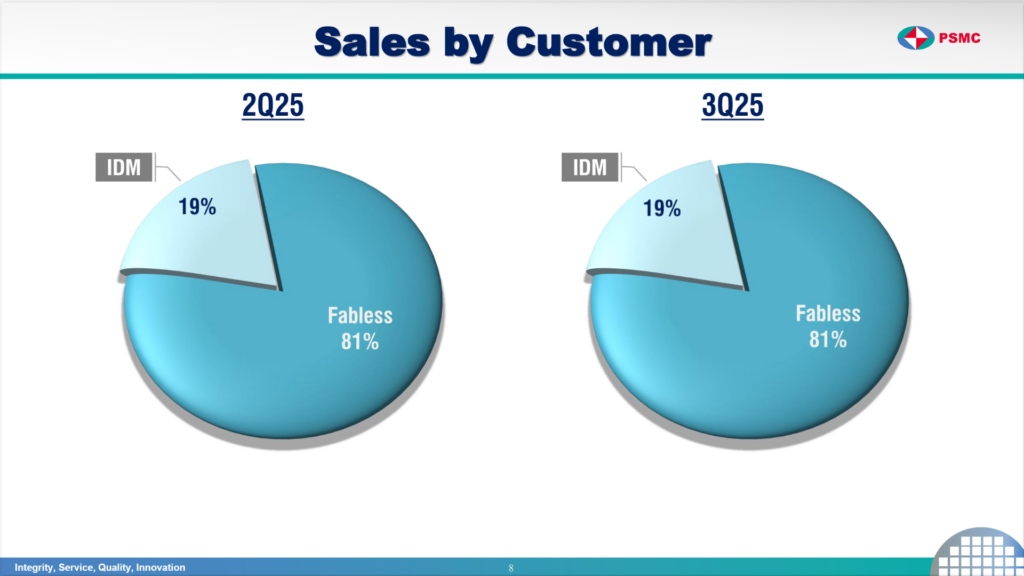

And note that only 19% of PSMC’s total revenue went to the IDM market (for the occasional IDM outsourced parts and pieces they don’t need to bother with in-house). 81% of PSMC’s output goes to the fabless market, with automotive and industrial applications being a top end market. A lot of fabless companies will source small mature memory product from a company like PSMC for their own products. Bear this in mind as we walk through Micron’s deal with PSMC.

What exactly is Micron buying?

Micron’s $1.8 billion deal is for PSMC’s P5 fab. P5 began construction in 2021, in the midst of the global automotive/industrial/power chip shortage in the aftermath of the pandemic. P5’s grand opening was in 2024 — when the chip shortage had flipped, and the auto/industrial/power end market was in severe over-supply. https://www.powerchip.com/en-global/insights/press-releases/content/20240502

Let that sink in for a moment. Micron is scooping up a fab that is less than two years old for a mere $1.8 billion. Is this a steal-of-a-good-deal for Micron?

Powerchip’s capital pain is Micron’s gain?

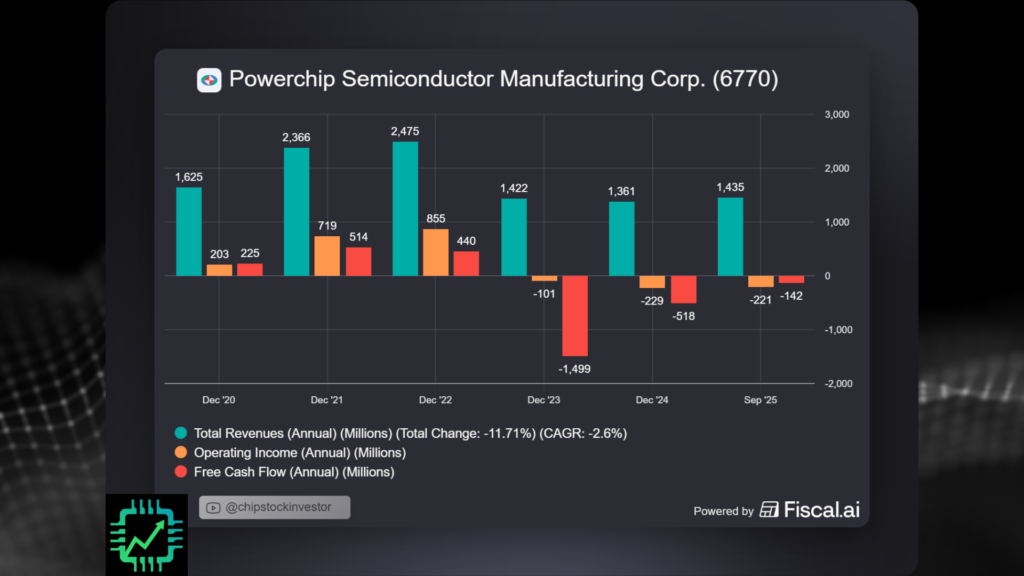

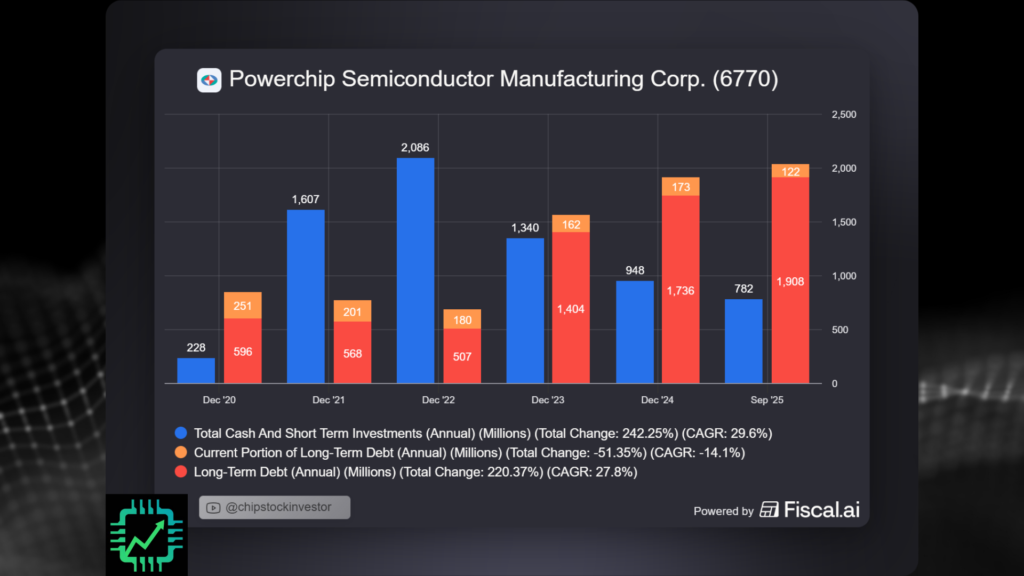

Unfortunately for PSMC, it wasn’t the only company ramping up production for its customers during the last chip shortage from 2021 to 2023. A lot of capacity came online at the peak, customer inventories shot higher as initial customer demand in the wake of the pandemic wound down, and now PSMC is left with fab capacity operating at sub-par profitability. PSMC needs to offload that capacity to clean up its operational efficiency, and it needs a fresh sum of cash after running at a loss for an extended period.

Want to make financial visuals like the ones above? Use our special link to get 15% off any paid plan: Fiscal.ai/csi/

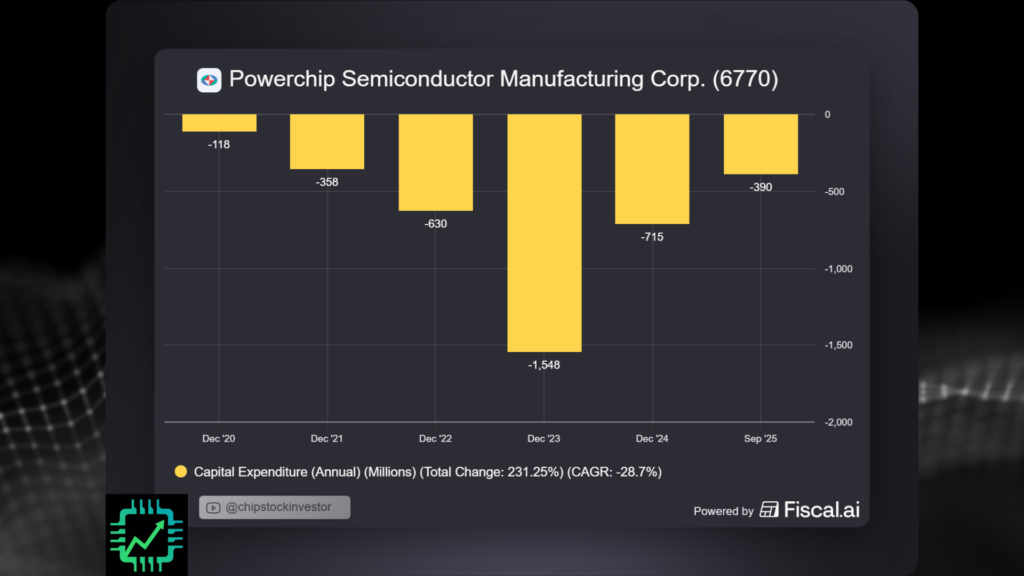

Besides getting some more DRAM wafer capacity for its AI data center needs, Micron will become a DRAM foundry service for PSMC when it takes over P5 later this year. Thus the cheap-looking price tag Micron is paying for the P5 facility that took several years and several billion dollars to build (see PSMC CapEx below, but you’ll get a clearer picture when the company reports gain/loss on sale later in 2026). PSMC offloads a money-losing operation for Micron to manage, gets affordable DRAM capacity from Micron for its own customers, and will gradually phase out all non-AI semiconductor processes.

In addition, PSMC will work on developing its remaining fabs to qualify as a wafer-level packaging facility Micron needs for its advanced products (for 3D DRAM and HBM, including wafer bonding interposers). Micron needs more advanced packaging capacity for its own memory product supply chain, and will work with PSMC to get that planned packaging capacity up and running.

The claim: Memory is no longer cyclical

You probably heard similar arguments during the auto/industrial/power chip shortage that began in 2021. And indeed, the growth cycle at that time was unprecedented… and contagious. We too thought that, at the very least, the cycles would become less severe.

In part, this ended up being correct — but the cycle got extended by the accelerated computing and AI data center party that Nvidia started. Auto/industrial/power end markets have languished in an extended down cycle.

Is the same mistake being made by memory chip investor bulls? With the complexity involved in designing advanced memory products, and a severe unprecedented shortage (DRAM, NAND, HDDs), surely memory IDMs won’t face a cyclical downturn anytime soon.

Make no mistake, though, two key facts remain relevant:

- Memory is merely one ingredient in a final computing product

- Memory is a manufacturing-intensive endeavor

Both items dispel the notion that memory is no longer a cyclical commodity product. Yes it’s a complex commodity part, and a complex manufacturing process and supply chain. But that does not mean a down cycle won’t come… eventually.

Micron as one of the leading AI memory momentum trades of 2026 is still on the table with this deal for PSMC’s P5 fab. But caution is warranted, as investors pile in and increasingly ignore rising valuation without ever factoring for more measured growth, let alone a cycle slowdown, at some point in the future. Call made in June 2025: https://youtu.be/6kxno1b-oAo

Join us on Semi Insider for more of the discussion, and for access to our new Research Platform we are building to help understand the global electronics manufacturing supply chain!

One Response

Good thoughts. It is possible that MU earns as much as $50 per share in fiscal 2027 IF DRAM prices continue to escalate.

But, caution is advisable….I agree with you. bill brown