We left off the first half of this series awaiting earnings from one of the industry’s big names: Analog Devices (ADI).

We now have ADI’s Q1 fiscal 2026 in hand (another weird fiscal year, ADI’s Q1 concludes at the end of January). And indeed, the indication is the U.S. industrial sector (industrial design and a bit of manufacturing too, in ADI’s case) is awakening. https://investor.analog.com/static-files/3ebfdc7f-b046-475c-93a0-f5e8b165293a

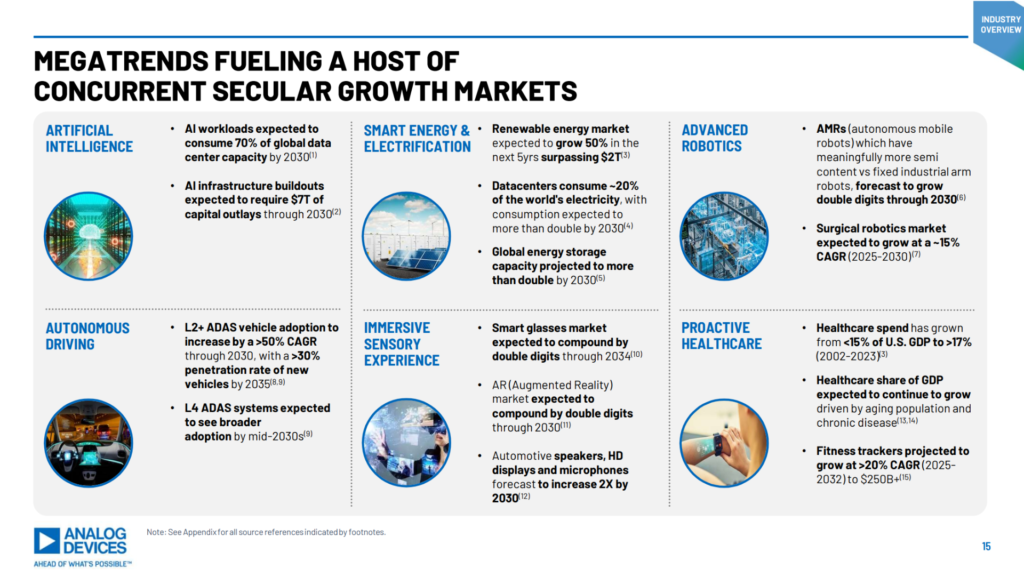

AI isn’t just digital, analog is a big secular growth trend too

For a lot of investors in 2026, artificial intelligence (AI) chips means GPUs and related parts and pieces for data centers — a lot of digital (1s and 0s that make up the foundation of software) semiconductors. But analog chips, the original semiconductor technology that interacts with physical world signals (electrical, light, motion, etc.) and converts those signals into digital ones, are needed too.

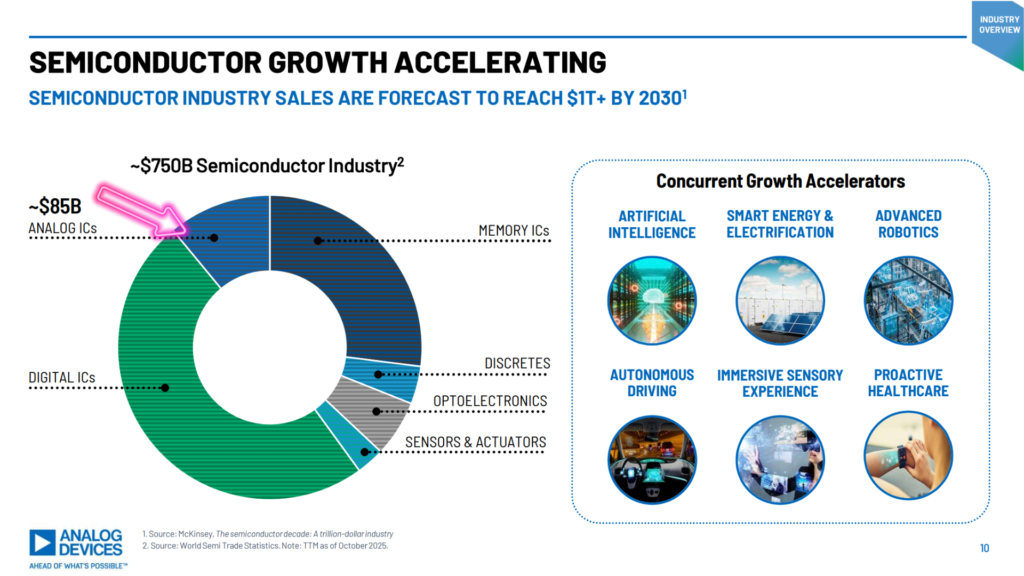

As the company’s name implies, analog chips are ADI’s forte. And while analog is a smaller slice of the overall industry end-market pie (~$85 billion of the ~$750 billion end market sales in 2025), analog integrated circuits (ICs) are growing in demand across ADI’s customer base.

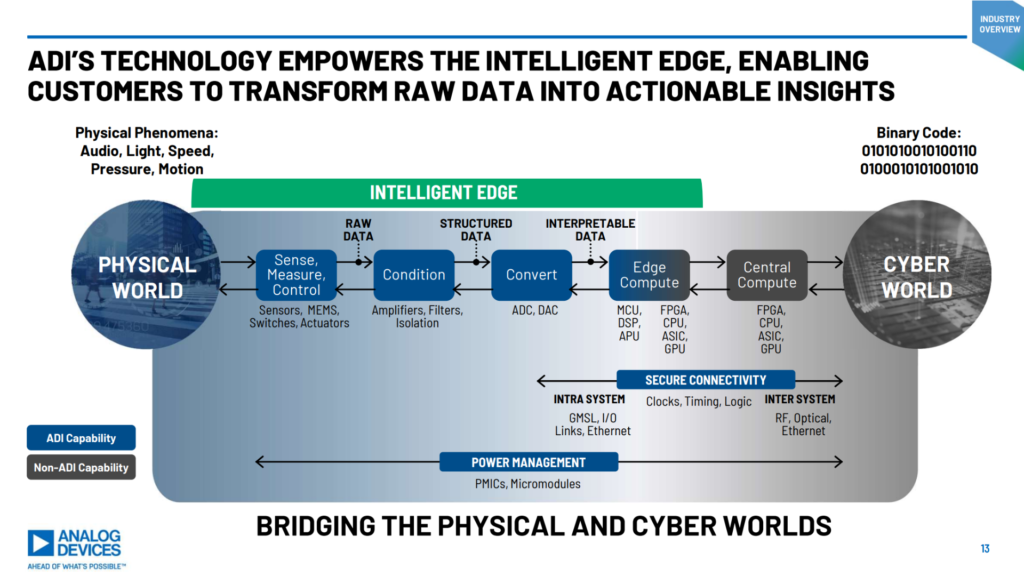

ADI’s IC solutions span sensors to analog-digital and digital-analog signal converters to power management chips.

We will get to ADI’s end market sales by industry in a moment, but the company highlights the secular growth trends it addresses. Within AI specifically, it isn’t just data centers. One of the key purposes of modern data centers is to train algorithms for use in the real world, like auto safety and self-driving systems, manufacturing and healthcare robotics, and other smart devices.

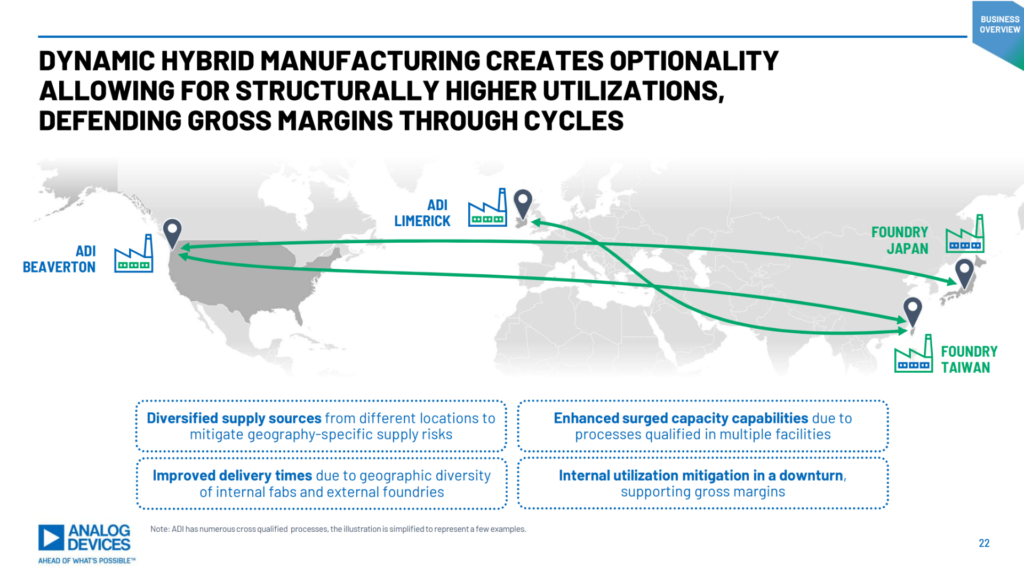

Like other semiconductor businesses that have been around for decades, ADI has been reworking its business structure to address these high-growth secular themes within the economy. Along with that, ADI has also been adjusting its internal manufacturing and adopting a “hybrid” model that also utilizes third-party fabs and chip packaging partners so it can maximize profitability for shareholders.

Analog Device’s business model and financial targets

This “hybrid” business model has become a common theme among the other leading IDMs (companies that both design and manufacture their own semiconductor products) around the world. For ADI, this means reliance on Taiwan Semiconductor Manufacturing for wafers needed in more advanced products, while keeping its own internal fabs focused on the advanced analog stuff.

As part of this reshuffling of the manufacturing model, it sold its small fab in Milpitas, California in 2022 (now owned by Gem Realty Capital and Cannae Partners, the fab has since been leased to quantum computing startup PsiQuantum since 2024); and ADI agreed to sell its chip packaging facility in Malaysia to ASE Technology in late 2025.

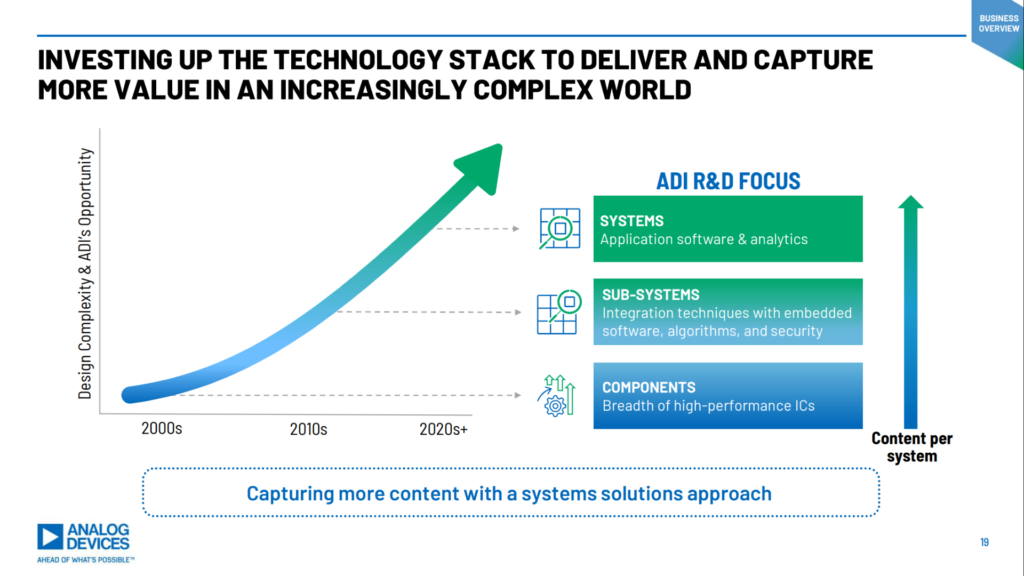

Along with utilizing third-party fabs, ADI has made a push into designing whole systems — chips assembled into a computing system, along with system-level software and even final applications.

The implications of this move into higher-levels of the technology stack are notable for shareholders. Like other (famous) semiconductor businesses that have broken through the commoditization problem of just supplying components, ADI is now taking an active role in designing embedded software and apps, monetized primarily through the sale of hardware to its customers.

As a result, the company has some of the best profit margins in the industry — and not just in product gross margins. Adjusted operating margins are headed well over 40%, with a free cash flow (FCF) profit margin target of 40% by next fiscal year (2027).

Notes on outlook and valuation

Now, none of this means ADI is no longer a cyclical industrialist. On the contrary, all businesses are cyclical. It’s a matter of determining what the cycle is, and how long the present cycle will last. Historically, auto/industrial/power IC sales cycles are short and last a couple years or so.

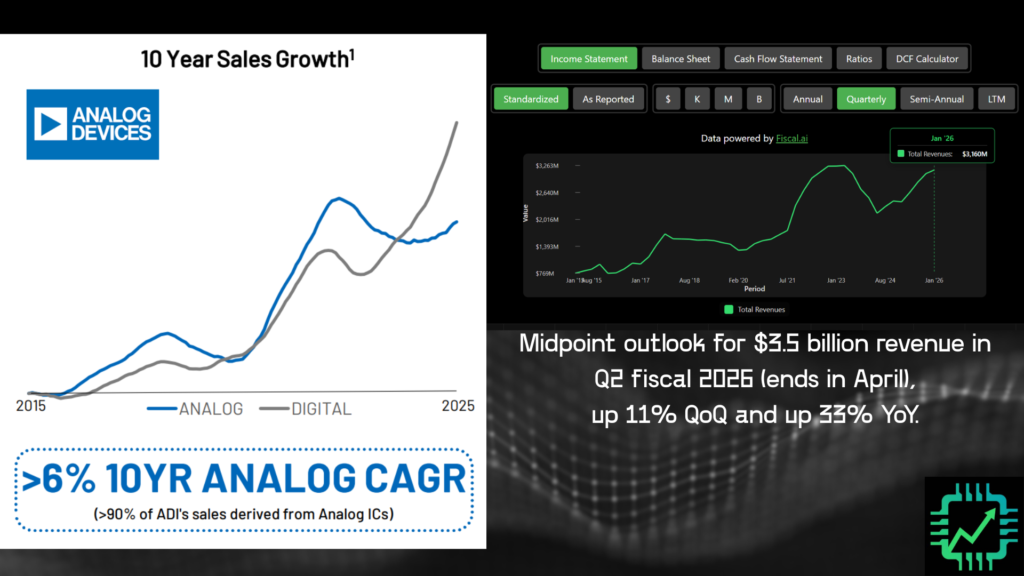

ADI itself provides some help on this front. On the left side of the chart below, ADI has the general sales growth pace of analog vs. digital chips going back over a decade. Pre-pandemic, semiconductor end markets tended to move in lockstep. But especially since the pandemic supply chain disruption, and then the ChatGPT and Nvidia moments of 2022 and 2023 that set off the current data center buildout super-cycle, a “bullwhip effect” has been going on. The analog IC sales cycle has decoupled and been delayed a bit from digital IC sales.

The indication, if the near- to medium-term future mimics the last few years, is that ADI’s revenue rebound back to 2022 all-time-highs (right side of chart above) is going to continue as it “catches up” to the data center buildout cycle (digital chip sales, like GPUs).

As a result, ADI’s Q1 fiscal 2026 revenue increased 30% year-over-year, and the midpoint of fiscal Q2 guidance implies 11% quarter-over-quarter and 33% year-over-year growth — an acceleration from the Q1 result.

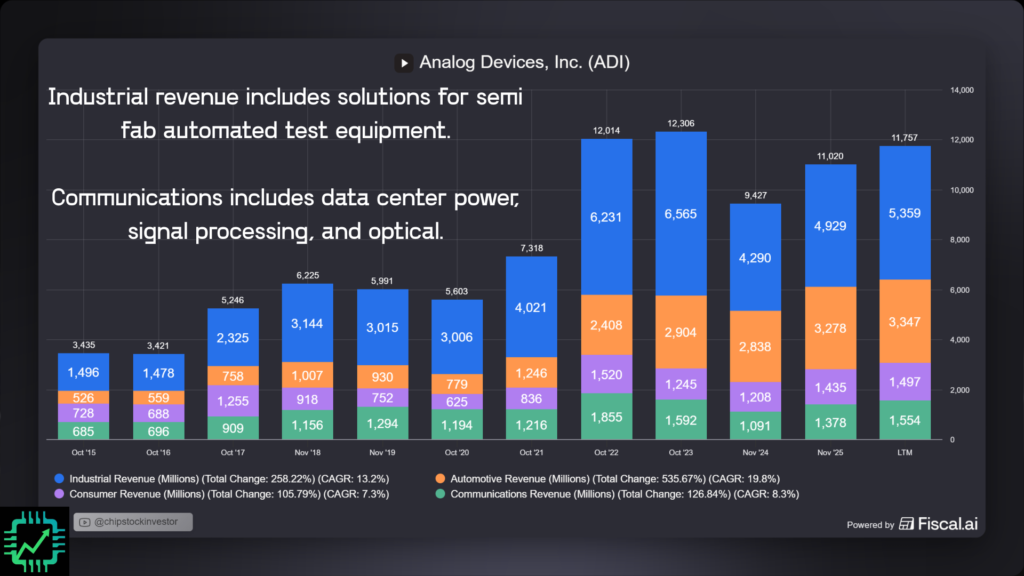

Given the ratcheting-up of revenue to new highs, and ADI management commentary about 2026 being a banner year, you might think all of this growth is all AI data center-related. But… it isn’t. And that too is an interesting implication. “Communications” revenue, which includes data centers but also internet and wireless network customers too, was only 13% of revenue over the last 12-month reported period ending in January 2026.

Need to make financial visuals like the one above for your own research? Fiscal.ai has you covered! Get an additional 15% off any paid plan using our special link: Fiscal.ai/csi/

Yes, data center applications (power control systems, analog-digital and digital-analog data converters, timing, optical networking, etc.) are a high-growth market for ADI right now. But so is Industrial and Automotive, especially high-end edge computing applications — or, as the kids are calling it these days, “physical AI.” That’s a reference to those AI algorithms trained in the data center now being deployed in the real world.

For ADI, physical AI takes many forms. It could be a self-driving car, an e-commerce fulfillment robotic system, a robotic-assisted surgery machine, an automated manufacturing system for an automaker or pharmaceutical company, smart glasses with speech recognition and display built into the lenses, or even a humanoid robot company burning cash to try and create that “killer app” that creates a brand new commercial market. ADI is behind the scenes working on it all.

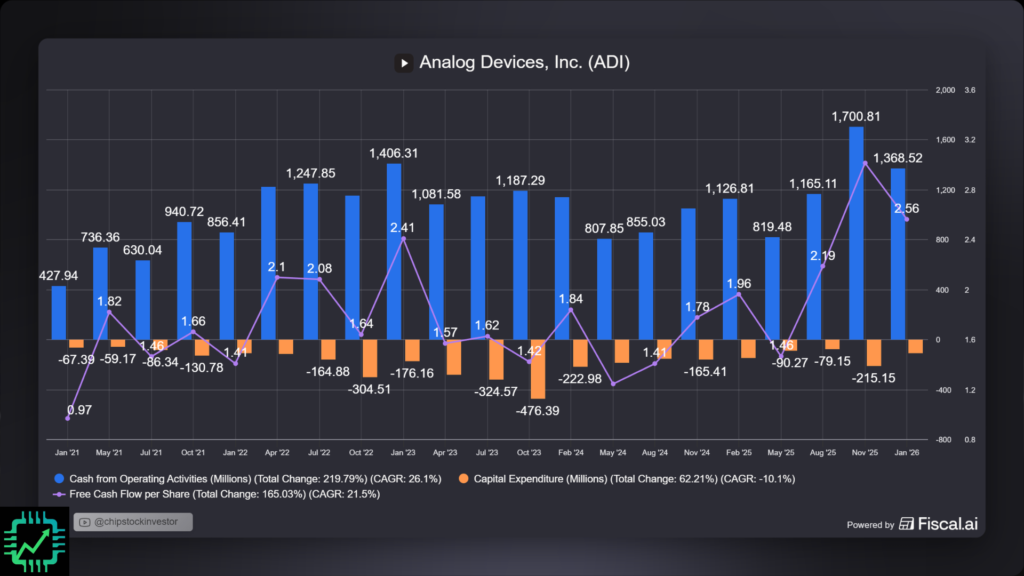

Thanks to ADI re-working its hybrid business model, profitability — especially on an FCF basis — has actually already reached new all-time-highs thanks to increasing profit margins. The margin increase outlook trend is set to continue with the incremental increases in revenue expected through 2026.

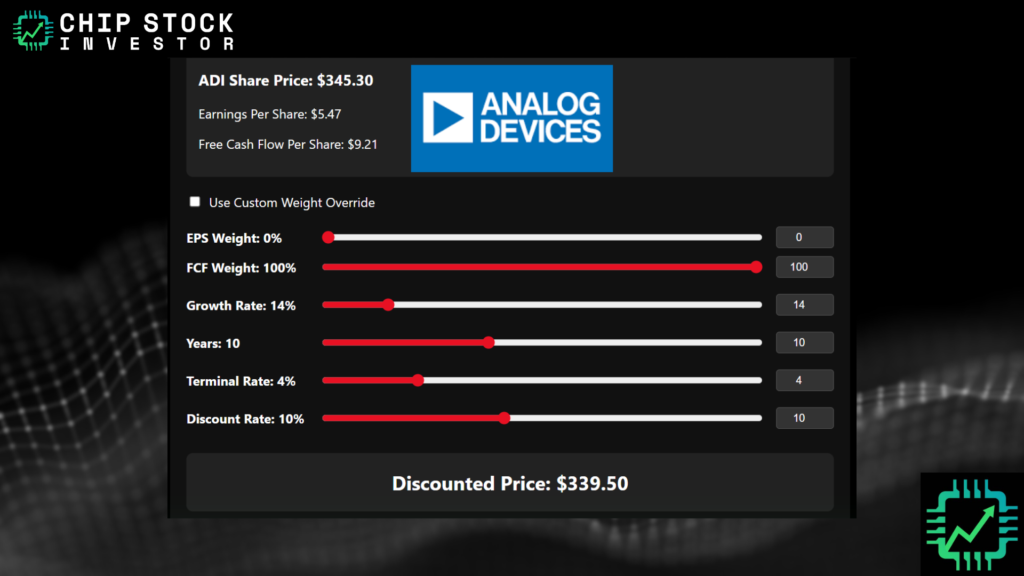

But is there still value in ADI stock? After all, shares have run over 50% higher just since late November alone (after ADI’s fiscal 2025 update and 2026 outlook). It depends on numerous factors, most important being your personal investment needs. But we ran a reverse DCF (discounted cash flow) to try and judge what expectations are now baked into the current valuation.

- Trailing 12-month FCF-per-share of $9.21

- Per-share profit growth of 14% for 10 years

- Terminal growth rate of 4% thereafter

- Discount rate of 10%

- = current stock price ~$340

For a cyclical business, this still might present a reasonable valuation — depending on the length and magnitude of the current growth cycle. As it stands right now, ADI is poised to make a lot of profit in 2026, with momentum perhaps carrying over into 2027. If so, there could be room for shares to run higher.

But that’s the trick with cyclicality. Timing is hard, and the end of a growth cycle can be painful if you’re caught over-allocated in one company or industry group. Nevertheless, as far as we can tell, something big is coming in the short-term. The industrial and manufacturing sectors are heating up, and the analog portion of the semi industry (auto/industrial/power) is in good shape for 2026. We’ll continue monitoring the situation.

Join us over on Semi Insider for the complete conversation, and access to our Research Dashboard and investing tools.