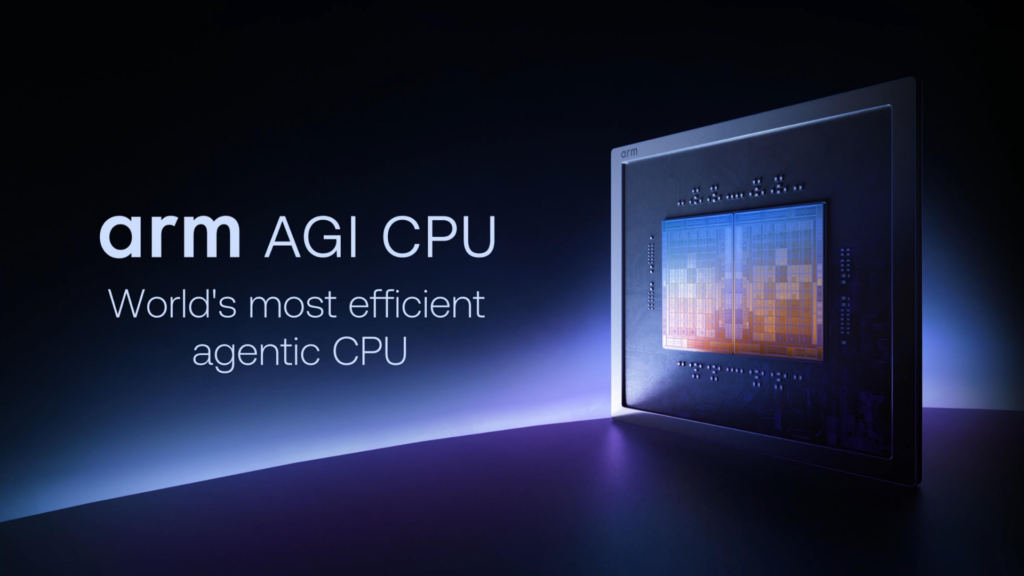

While most investors were (understandably) worried about geopolitics this week, semiconductor IP (intellectual property) licensing and royalties company Arm Holding (ARM) held its “Arm Everywhere” special event to officially announce a new AI chip. And not just any chip. This is Arm’s first in-house designed chip. Rather than selling access to the IP so a customer can do their own design work, the new Arm AGI CPU is ready to go into production, for customers to purchase and install in their data centers.

Arm’s extensive IP portfolio has helped Arm-based chips become one of the most pervasive CPUs in the world (ranking high alongside the mighty x86, aka Intel and AMD CPUs). Arm’s dominance is especially in mobile applications, but it’s been picking up market share in data centers too. So naturally the company’s entrance into the fabless chip design market debuts an AI CPU, with AI inference in mind.

What does this mean for Arm shareholders? We take an early look at Arm’s competitive move in this article. Next week, we’ll do a follow up on the impact for data center CPU market competitors as AI inference takes center stage.

Higher licensing revenue from big semiconductor design customers

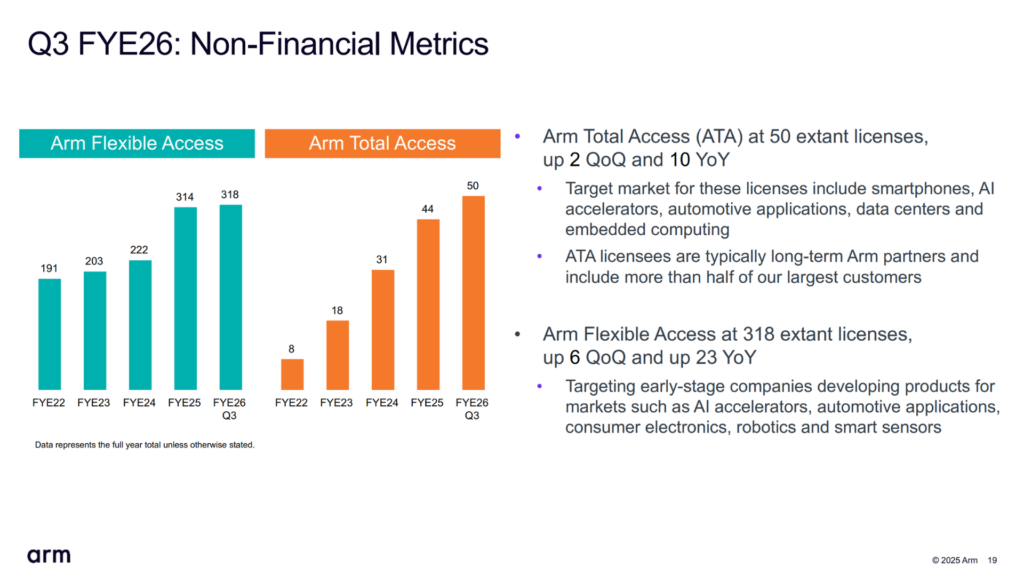

It’s well known that Arm has been ratcheting up its take of IP licensing and royalty from its customers. The company launched “Arm Total Access” (ATA) in 2020, providing its biggest customers (Apple, Nvidia, Amazon, etc.) robust access to its portfolio of IP and support services, and a bigger licensing revenue source for Arm. ATA customer count reached 50 in the latest quarter (Q3 fiscal year 2026), versus 318 customers for the Arm Flexible Access licensing tier that provides more à la carte access to the IP portfolio.

Then a few years ago, Arm also launched Compute Subsystems (CSS). CSS goes further than just providing semiconductor IP blocks for customers to design with. CSS provides full validated and verified production-ready CPU, GPU, and NPU chip foundations for customers to work with — still customizable foundations, but with a lot of the LEGO-like block building already complete. Arm CEO Rene Haas reiterated during his keynote at Arm Everywhere that CSS helps customers speed up time to production by up to 12 months, and sometimes as much as 18 months.

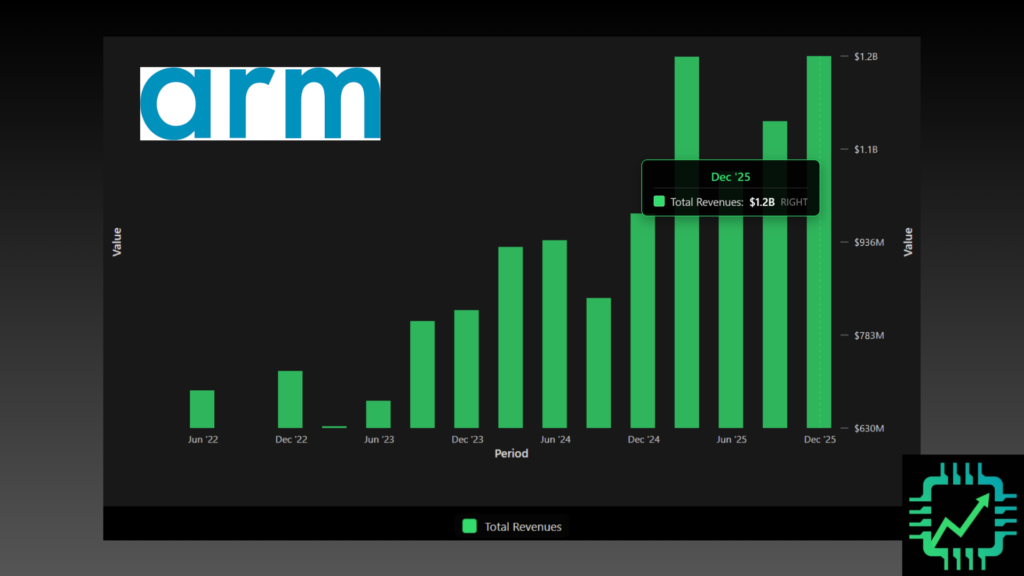

Over the last few years since SoftBank did a partial spin-off of Arm (SoftBank still owns ~87% of Arm equity), higher licensing value and more royalties from these new products has kept the company in respectable growth mode. Q3 fiscal 2026 revenue increased 26% year-over-year to $1.24 billion. Q4 fiscal 2026 (the final quarter for Arm’s fiscal year, which ends every March) revenue guidance was for $1.47 billion, implying 19% year-over-year growth.

We’re building investor tools and analysis for the semiconductor and technology supply chain. Join Semi Insider and get access to charts like above, powered by data from Fiscal.ai! chipstockinvestor.com/pricing/

Why is Arm keen on doing the job of its customers?

After CSS, the natural meandering next-step progression is of course doing all the design work of a fabless chip company, and sending the finished product to the manufacturing floor (Taiwan Semi Manufacturing). Rather than selling the IP and collecting royalty payments, Arm will get to log the entire value of the sale of its new AGI CPU as its own revenue, in true fabless chip designer fashion.

But why turn into a fabless design company? Isn’t this going to turn Arm into a competitor of the companies it supplies IP to? Yes, to an extent it could. But things are more nuanced.

With AI hardware design work getting more complicated and expensive, and many of the top semi companies and data center operators are working on full-system design these days, why not offload some individual chip development work to a trusted and capable supplier like Arm? The company is already hiring lots of engineers to compose IP blocks and CSS, and collecting higher licensing and chip royalties, so said customers very well may apply pressure back on Arm and simply say, “Your IP is good, so design the whole chip yourself, and we’ll buy some of them too.”

Indeed, Haas said in his keynote presentation that partners have asked for an Arm in-house-designed CPU. Meta and OpenAI are two of those customers that have been working closely on the AGI CPU’s development (there were executive guest appearances from both companies at the Arm Everywhere keynote).

CPU demand is going up as data centers pivot to AI inference

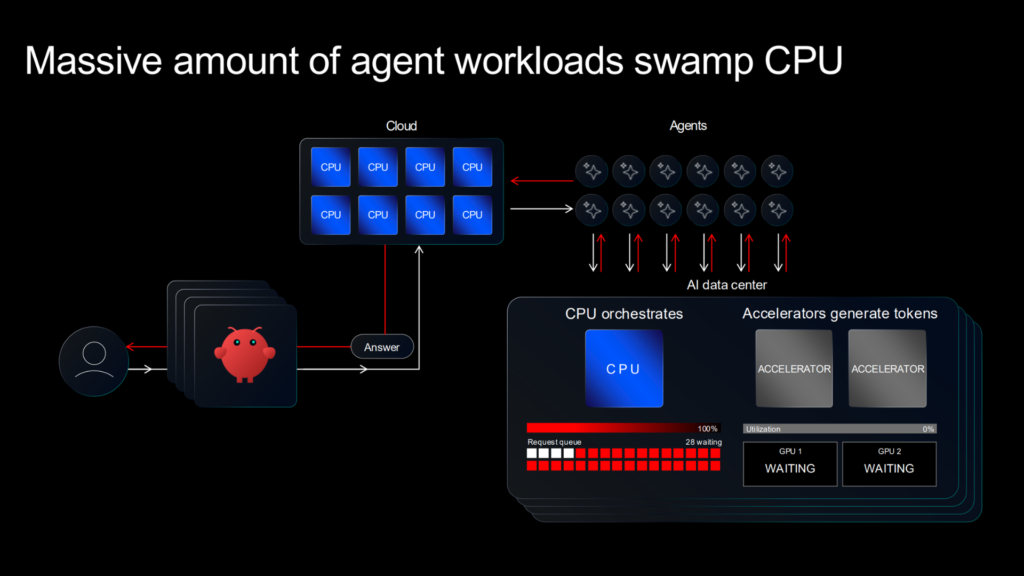

Besides meeting customer demand, Arm also discussed at length how the CPU is still very much a relevant part of an accelerated computing data center system (Nvidia has known that all along as well, and announced another CPU and CPU system at GTC earlier in March, more on that next week).

Haas likened CPUs as the orchestrators of AI and accelerated computing workloads, like tractors moving dirt around a job site.

Orchestrating AI inference, AI agent-powered software in particular, is asking too much of the legacy cloud computing server CPU. In other words, these CPUs are a “bottleneck,” contributing to idle GPUs as they wait for instructions to generate tokens. (See also our last write-up on Nvidia’s Groq LPX.)

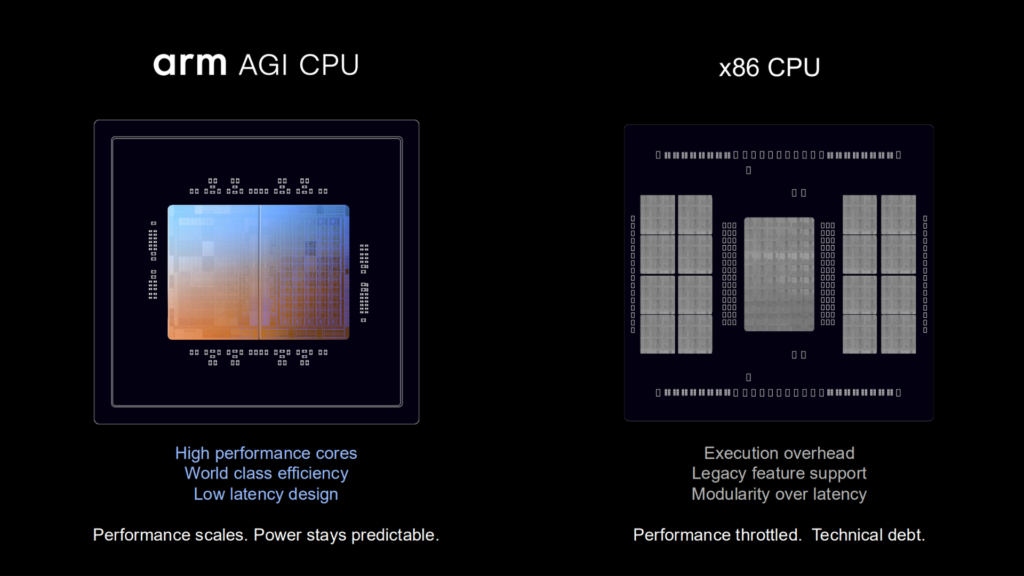

Haas and company spent ample time showing off performance comparisons to x86 (Intel and AMD, no independent or specific benchmarking available yet) favoring Arm AGI by a wide margin. Per usual, decades of x86 technical debt is blamed for a lot of the poorer performance. As AI inference workloads ramp up, new hardware and system architectures are needed compared to what worked during the early years of the cloud.

And like other chip designers, Arm is touting the custom composable architecture for the AGI CPU used in server racks. When used versus x86 CPUs, AGI claims 2x performance and ongoing energy cost savings. Ultimately, though, the AGI CPU will be offered as a part-and-piece as big data center customers engineer their next-gen systems, versus Arm designing and selling a full system rack.

Put another way, more CPU choice is great for data center system and operator customers, regardless of how true the performance advantages of AGI prove to be.

But will this new chip be a game changer for Arm? It could, eventually. At the very least, it’s a new sales outlet that could keep the company’s revenue growth at or above 20% during this bull market.

However, we’ve steered clear of ARM stock since its re-IPO a few years ago, and we’re still not ready to buy. Thanks in part to SoftBank owning most of the equity, resulting small float, and high institutional investment in Arm because of the company’s size, the valuation remains extraordinarily high in our view. Enterprise value (EV) to sales is at a whopping 32x as of this writing, and even one-year-forward expected price-to-earnings and price-to-free cash flow is at 67x and 80x, respectively.

That said, Arm’s move to become a fabless chip designer could have a meaningful impact on the data center market, especially in the CPU space, over the next five years. We will delve into this further next week.

Join Semi Insider for the full rundown on this discussion! chipstockinvestor.com

2 Responses

deep analysis