While there are several notable differences between the present bull market and the dot-com boom of the 1990s, there is one key commonality: The Earth-based infrastructure boom (AI data centers now, internet infrastructure then) has a corresponding expansion of the space economy (next-gen communications and space data center experiments now, early SatComm networks then).

Starting this time a year ago, we took a look at one of the investor darlings, Rocket Lab (RKLB). Rocket Lab (RKLB) Stock — Buy the Dip Before Liftoff?

Yes, we missed buying RKLB. We cited a certain valuation as being an attractive range for us, which RKLB nearly reached for a single day on April 4, 2025. Hopefully the research itself was helpful to those of you that did buy. The caveat: We made a lot of other speculative bets during the selloff, though, including on April 4.

This go around, we’ll look at another emerging favorite in the space economy, and a different kind of space economy “lab,” Planet Labs (PL).

Planet Labs lift-off — why now?

RKLB buyers benefited greatly from a selloff this time in 2025 due to the tariff tantrum, and worry over U.S. government spending cuts hitting RKLB contracts. There’s been no such worry for space stocks in 2026.

Not only did the U.S. government not cut space spending, in many ways it has increased greatly. Recent conflict, including the war in Iran, has no doubt played a part in helping new space company revenue re-accelerate. Bookmark that thought for a moment, we’ll come back to it in a moment.

Additionally, Planet Labs has benefited from a name drop by Nvidia (NVDA) at GTC, and Alphabet (GOOGL) with Project Labs involvement in Google’s Project Suncatcher moonshot. Not exactly the same uplifting story as Project Hail Mary, but nonetheless notable. Google owns nearly 10% of Planet Labs. Both initiatives from Nvidia and Google are eyeing space, and solar power, as a solution for future data center compute.

It’s like the Cold War all over again, commercial company edition! These are bets by two mega-companies looking at sustaining growth far into the future, and using investor excitement to help drum up support for the R&D.

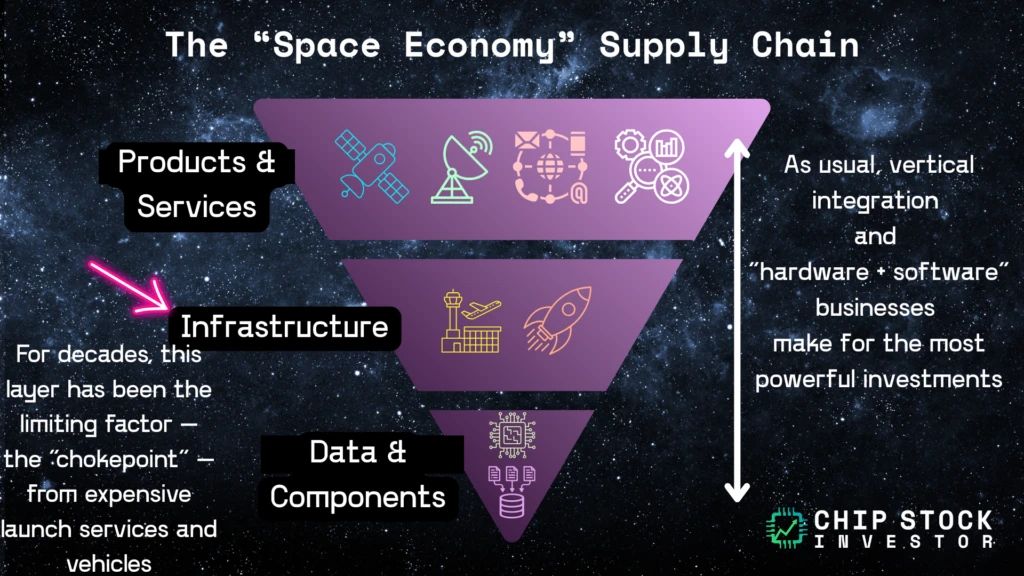

But what about Planet Labs? What’s the company up to, and what competitive advantages does it have? Let’s start with a reminder on the “bottleneck” to reaching space, and Planet Labs’ way of addressing it.

Space orbit has two primary barriers to monetization

For a company trying to tap into the revenue opportunities that space offers, there are two primary chokepoints: 1. Launch services, and 2. Space vehicles.

Chip Stock Investor is building new tools for investors that follow a process, with financial data powered by Fiscal.ai. Sign up today, join the conversation with a community of like-minded investors, and start building your intelligent portfolio. chipstockinvestor.com/pricing/

Planet Labs is a vertically-integrated space company, addressing the “vehicles” part of the equation with in-house designed and manufactured satellites. Primary assembly of its Owl, Pelican, and Dove satellites takes place in San Francisco. A second production facility in Berlin was announced late in 2025, specifically for NATO and European government agency customers.

Planet Labs’ launch services are typically handled by SpaceX.

How does Planet Labs make money?

So vehicle manufacturing is handled in-house, and to an extent, vehicle build is monetized (like via Google’s Project Suncatcher, or other customized solutions). But how does Planet Labs primarily make money (the vertical integration with services built atop a satellite constellation)?

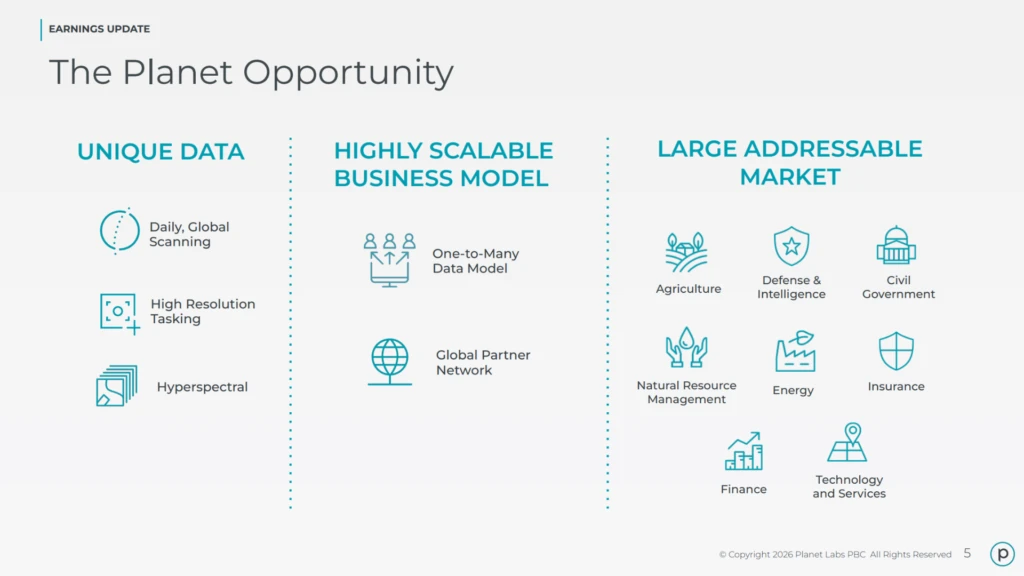

Think of Planet Labs as a type of data services and data analytics software company. It continuously images the entirety of the earth’s surface every day. This data is searchable via cloud services, enabling various analytics and data science use cases for government agency, aerospace & defense, and commercial customers.

Source: Planet Labs.

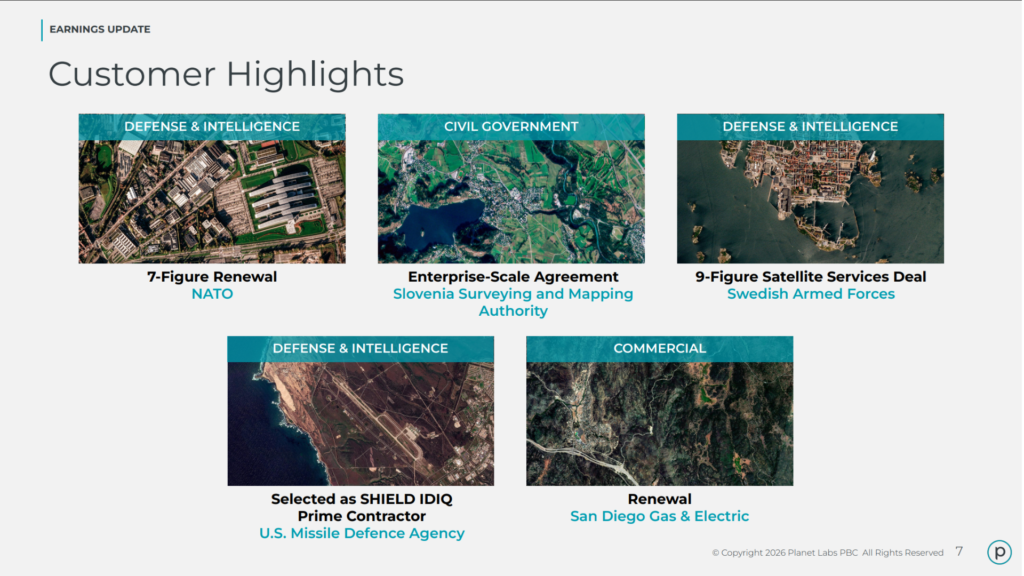

Given recent events and ramp up of defense spending in the U.S. and Europe, Planet Labs has been highlighting a lot of new defense customer contract wins. Other government contracts include surveying and mapping with Slovenia, and monitoring services for San Diego Gas & Electric.

Source: Planet Labs.

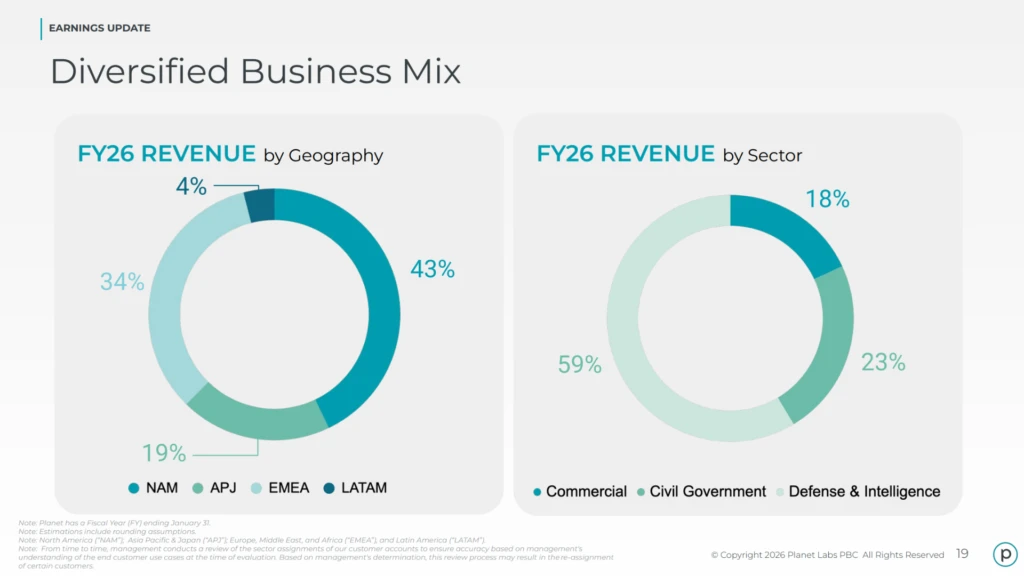

For at least some investors, the skew towards defense spending (59% of revenue in the last fiscal year) may not jive — especially given Planet Labs is a PBC (public benefit corporation). Of course, defense is a public benefit. But given defense spending is opaque by design, there will no doubt be questions and critique from some investors on what exactly Planet Labs’ data is being used for. File that away as a risk.

Source: Planet Labs.

A closer look at recent financials

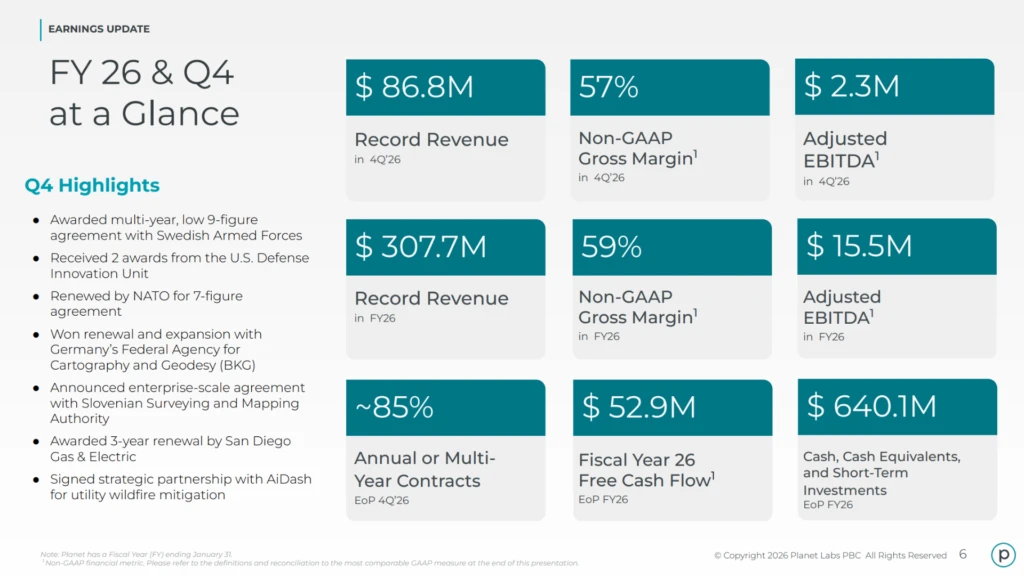

Planet Labs revenue re-acceleration was on display in Q4 of fiscal 2026 (the three months ended in January 2026). Revenue was $86.8 million, up 41% year-over-year, helping full-fiscal-year revenue increase by 26%. Adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) was slightly positive at $2.3 million in Q4 and $15.5 million for the full year. More on profitability in a moment.

Source: Planet Labs.

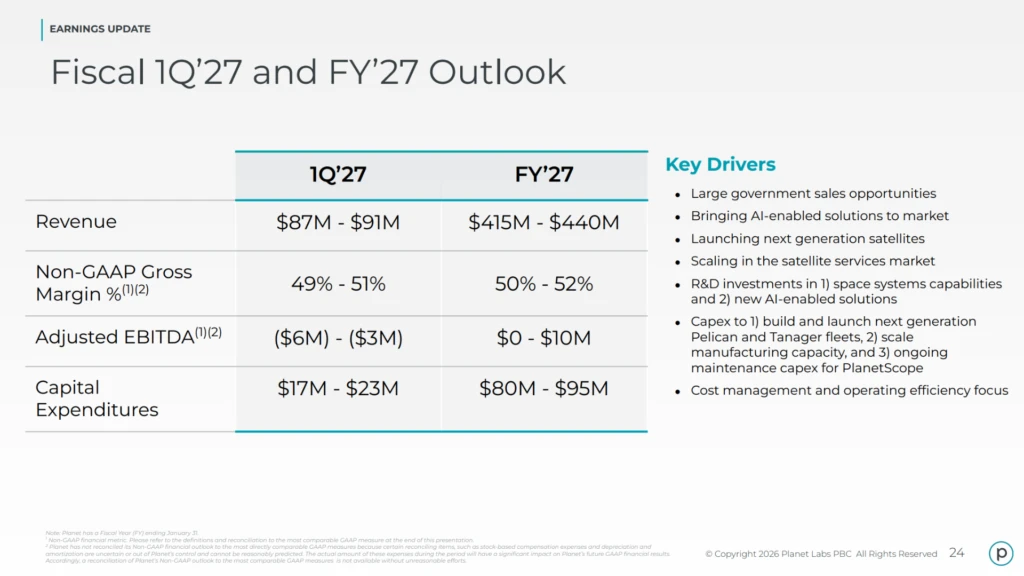

As a proof point, management said revenue should be in a range of $415 million to $440 million this next year (ended January 2027). That implies a 39% increase in revenue this year at the midpoint of the outlook. However, adjusted EBITDA was forecasted to remain close to 0. Capital expenditures are set to rise to $80 million to $95 million, compared to $77 million last year, so the lack of adjusted EBITDA growth implies other expenses will also be going up (sales and marketing, R&D, etc.).

Source: Planet Labs.

Balance sheet and profitability

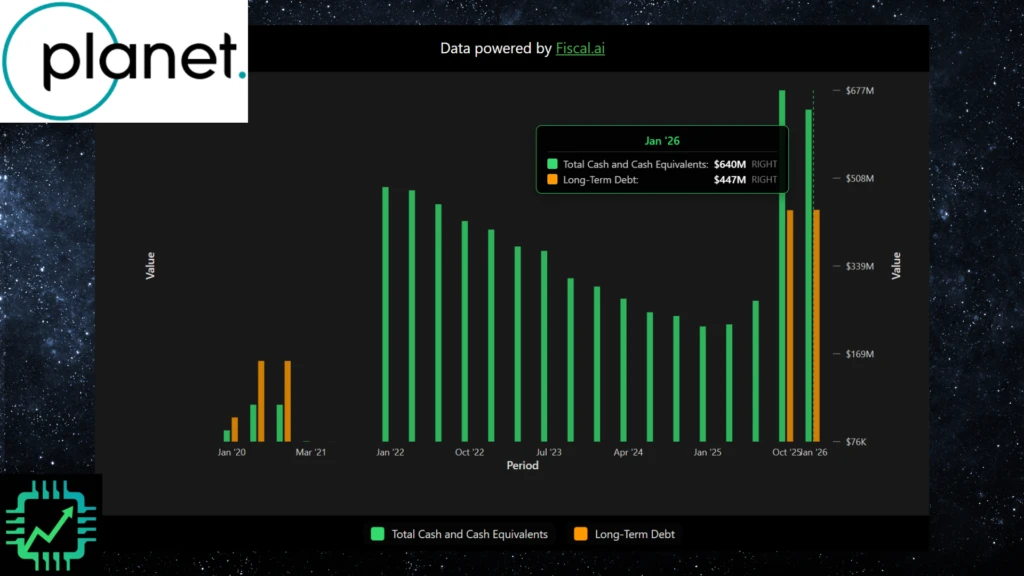

Back to profitability. The growth story is certainly there, but the adjusted EBITDA metric expected to go flat in fiscal 2027 indicates there could be some growing pains. Last year, Planet Labs raised some cash via a debt offering to help with scale-up ($447 million in debt on balance). The cash balance was $640 million at the end of the last quarter, but was back to shrinking again. We’d expect this to be the case given the higher expense outlook.

Source: chipstockinvestor.com

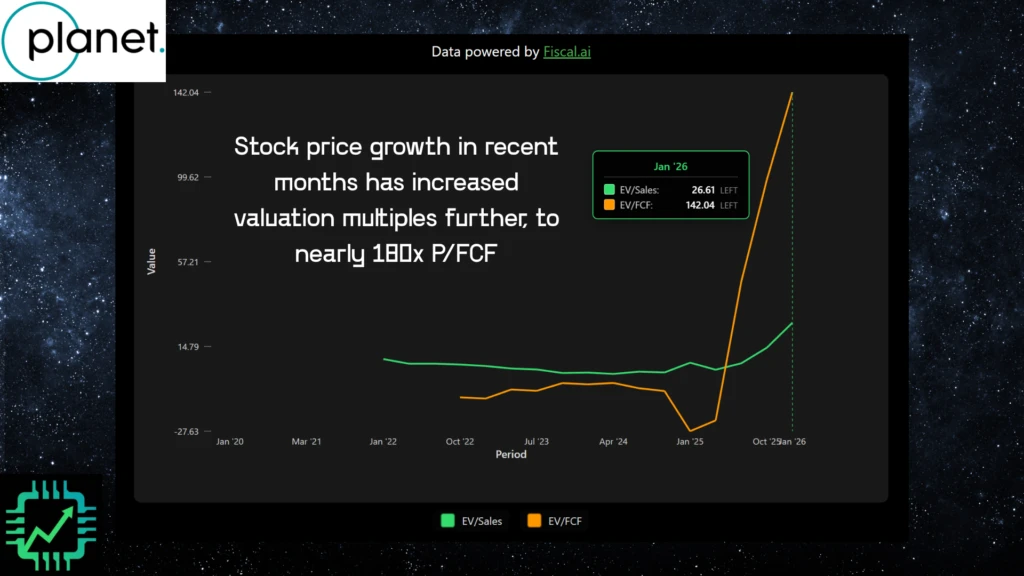

Nevertheless, investors are focused on the accelerated pace of revenue, expected to be near-40% this next year. As a result, trailing-12-month price-to-free cash flow has risen to near 180x (nearly 38x enterprise value to sales) as the stock price has continued running higher this year.

Source: chipstockinvestor.com

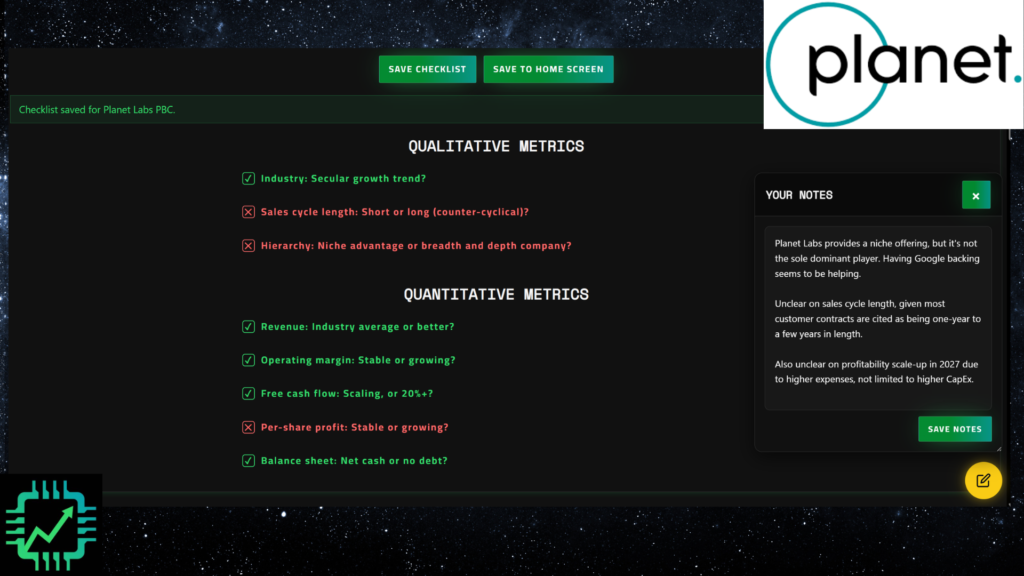

To us, this certainly appears to be geopolitical conflict and war in Iran-driven price action. Planet Labs checks off a number of boxes for us (see our checklist below, although profitability scaling has been called into question), but the valuation doesn’t look attractive. We’re not ones to chase momentum if it’s driven by a temporary event (at least, we’re really hoping the Iran conflict is temporary).

Source: chipstockinvestor.com

As with Rocket Lab and other space stocks like Planet Labs, the best time to buy was last March and April. For now, we’re going to continue watching the lift-off… from the ground — the exception being our ownership of PL via owning Alphabet stock.

Read next: Arm Announces A New AI Chip – Why We’re Watching the Stock From the Sidelines