What’s happening with memory right now is like Nvidia 2022–2023 all over again. Nuts. We’ve been invested in memory during this craze and are keenly interested in where we are in this AI data center expansion cycle. So let’s get more granular.

The revenue picture

The most recent quarter came in at over $41 billion in revenue with operating profit over $33 billion. Guidance for Micron’s Q4 fiscal 2026 (corresponding mostly to Q3 calendar 2026) is $50 billion in revenue and an implied operating income over $41 billion, at the midpoint of the outlook. The 10-year average revenue growth rate, even when you include the last decade-plus of boom-bust cycles, is starting to look pretty good once you factor in recent quarters and upcoming guidance.

Something real has seemingly changed, and it’s called the Strategic Customer Agreement, or SCAs, that Micron is structuring with its customers as a take-or-pay agreement. What is that? And why does it matter?

What’s a take-or-pay agreement?

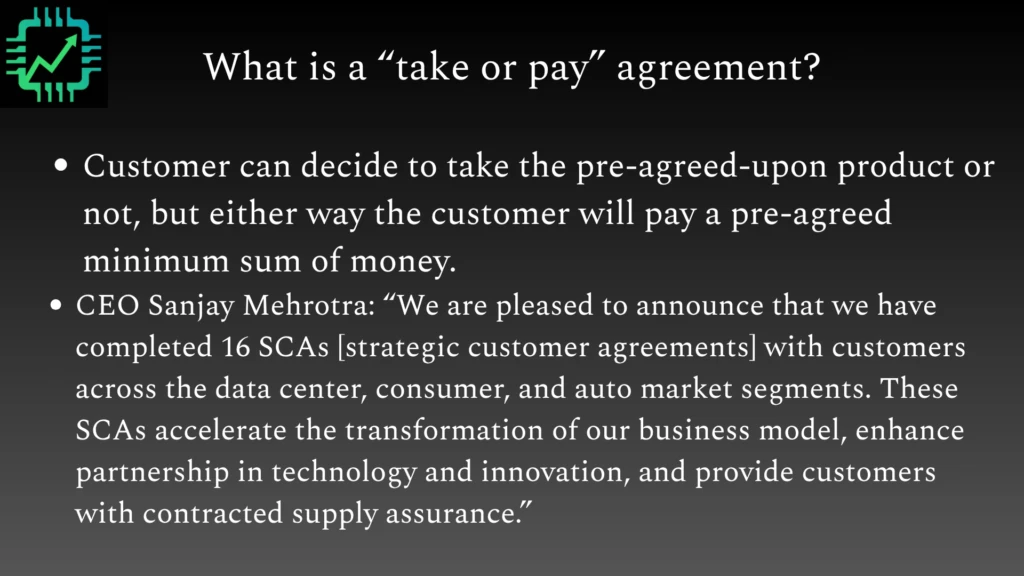

It’s actually just what it sounds like. The customer either takes the agreed-upon product, or if they decide to cancel the order, they still have to pay a pre-agreed minimum sum of money. Basically think of it like an order cancellation charge.

Micron has now signed 16 SCAs with varying terms depending on the customer and industry. It seems the bigger SCAs, likely with the hyperscalers and/or Nvidia, have the take-or-pay clause. Why does this matter?

Because this is exactly how the semiconductor industry got hosed in 2022. Customers double- and triple-booked orders during the chip shortage trying to get supply allocated to them, then canceled many of those orders when the market flipped to oversupply starting in late 2022 and 2023. Micron is making sure that doesn’t happen again, and it isn’t left holding the bill for a bunch of fab expansions because of fickle customer activity.

SCA details

Here’s what management disclosed:

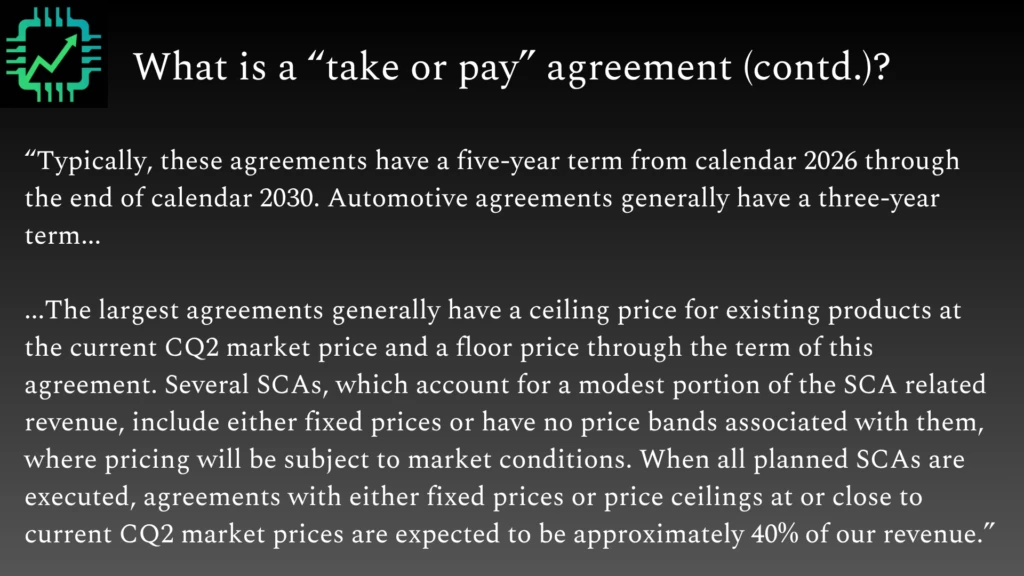

Terms: Hyperscalers and Nvidia get five-year supply agreements running from calendar 2026 through the end of 2030. Automotive and other industrial supply agreements (smaller SCA deals) are generally three-year terms.

Pricing structure: Some SCAs have fixed prices. Others have a price ceiling and floor (price bands) for existing products dictating what a customer will pay. A ceiling price applies to current products, which seems to imply these deals are not structured to address newer upcoming memory such as future generations of HBM (high-bandwidth memory).

Coverage: When all SCAs are executed, this is expected to represent roughly 40% of Micron’s revenue.

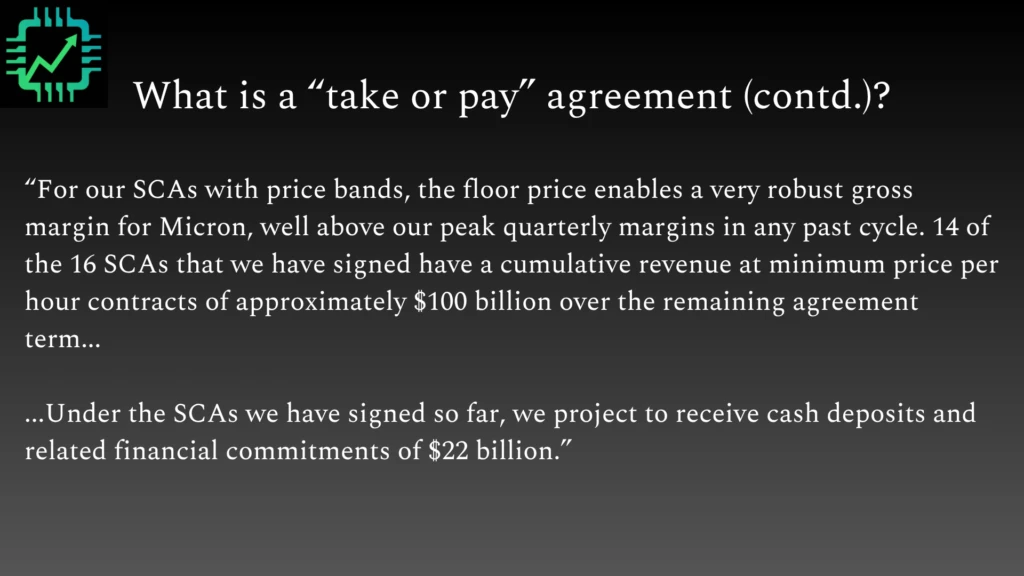

The backlog: These agreements are cumulatively worth $100 billion in revenue over the next three to five years.

Cash deposits: A number of the larger SCAs include an upfront cash deposit. Expect to see roughly $22 billion in deposits show up on the balance sheet in the next couple of quarters. These deposits will be listed as a liability – it’s cash for work not yet finished – but it’s also a payment sitting on the liabilities section of the balance sheet that Micron can realize as revenue, as terms of the agreement are fulfilled.

The reason Micron can structure agreements this way? Samsung and SK Hynix are also sold out of capacity. A customer who cancels can’t simply walk down the street and get supply allocated elsewhere. Micron is using this industry dynamic to its benefit.

Is “this time different” for cyclical memory?

Yes and no. Many investors would like to frame this as a total restructuring of memory that eliminates cyclicality. We believe these SCAs are an indication that this period of growth has been extended, and the magnitude of the growth is amplified. But that does not absolve the memory sub-industry from cycles, even within the next five years, especially margin cyclicality.

Additionally, a lesson from economics also helps frame what is really happening. How do you ensure more supply and more favorable pricing in the future? Pay the high prices now. It’s a counter-intuitive principle in economics.

The hyperscalers signing these SCAs today are helping guarantee more supply will come online through 2030 – and with it, eventually, some memory pricing relief. Maybe not this year. Maybe not even next year. But by 2028–2029? Memory pricing might begin to moderate, and memory chipmakers’ margins could moderate along with it.

All of this is good for Micron. Good for the other memory makers. And over the longer-term, SCAs may reframe memory from a boom-bust industry to a more gentle and much more manageable business than in the past. However, bear in mind those SCAs will need to be renegotiated from 2029 and 2030 onwards. For now, the story favors the memory cartel.

Semi Insiders received an expanded post & video early on this topic. Get your subscription here.