With Q1 fiscal 2025 earnings in hand (for the three months ended in August 2024), investors are feeling a bit more optimistic about Aehr Test Systems (AEHR) stock once again. We won’t spend a lot of time on that today. The market is particularly fickle on this one, likely reflecting the high amount of trader (less long-term investor) interest in this semiconductor manufacturing equipment provider.

And even among long-term investors, there is some growing impatience with Aehr’s seeming lack of progress since the stock peaked in summer 2023. Remember, Aehr is a very small company (market cap of ~$400 million, enterprise value of ~$360 million), and it’s in the midst of a cyclical downturn due to the brakes getting slammed on the EV market, especially in North America. A potential Aehr rebound was always going to take time.

We get it, watching a stagnant stock price on a company you had high hopes for can be like watching paint dry. So… don’t sit around waiting for paint to dry. Let’s quickly run through the expectations Aehr has in place through May 2025 (when the current fiscal year ends), and then move on for now.

Remind me what does Aehr does again?

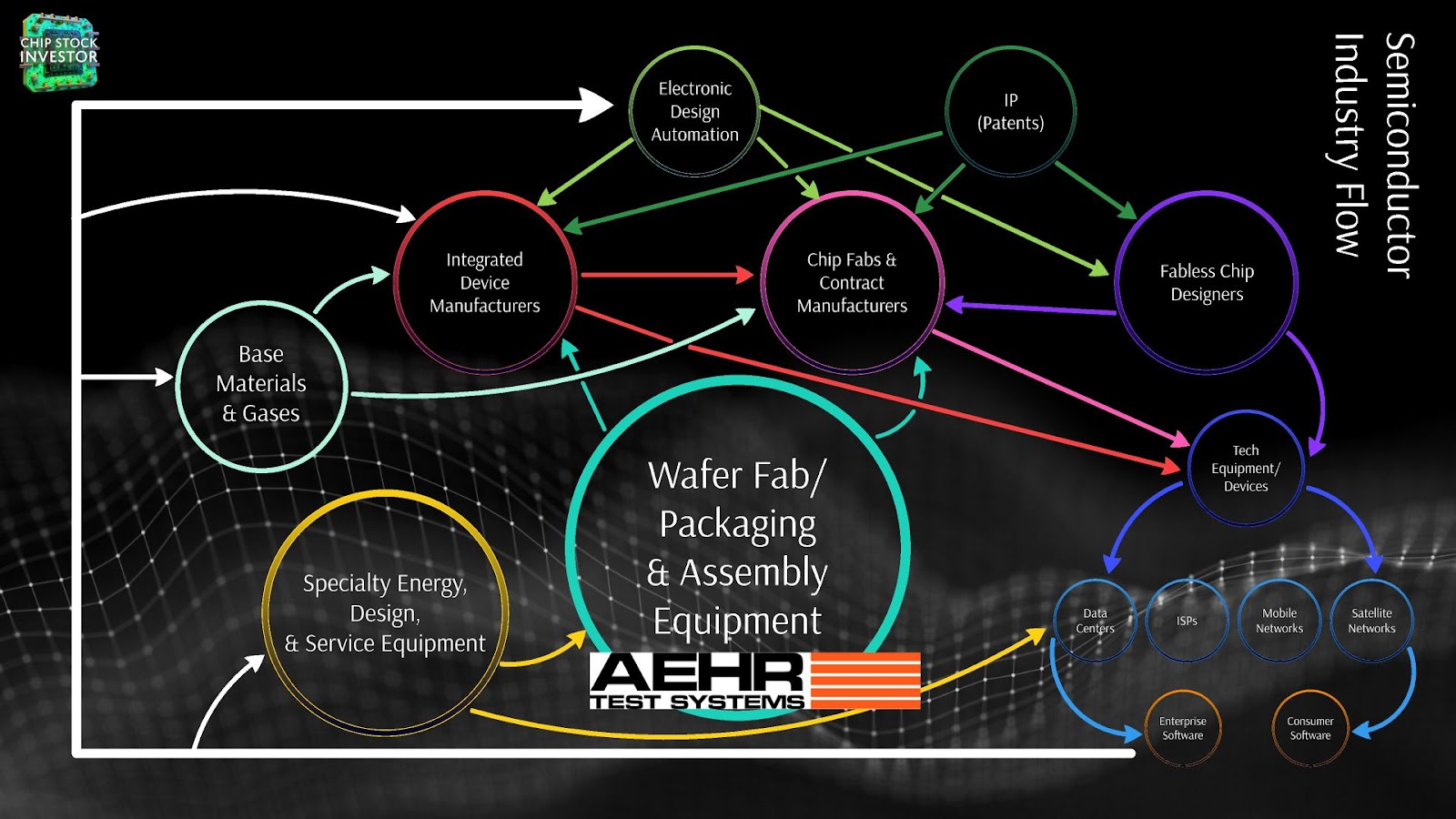

Aehr provides semiconductor manufacturing equipment, that critical “choke point” in the electronics supply chain. These are powerful businesses. If you want to manufacture semiconductors, it’s these toolmakers – many of which own a lot of the process technology for making chips – that you have to go through to build and manage a fab.

Aehr is a tiny participant in this sub-industry, though. The “Fab 5”, ASML, Applied Materials, Lam Research, Tokyo Electron, and KLA Corp, in that order, control roughly 70% of the over $100 billion-a-year spent on wafer fab and chip packaging equipment. Aehr’s niche has big potential, a fact you probably already know if you’ve somehow found your way to this post. Silicon carbide (SiC) devices are a key ingredient in the traction inverters, charging hardware, and such in EVs. There’s lots of upside from other markets too, from solar power infrastructure to industrial equipment.

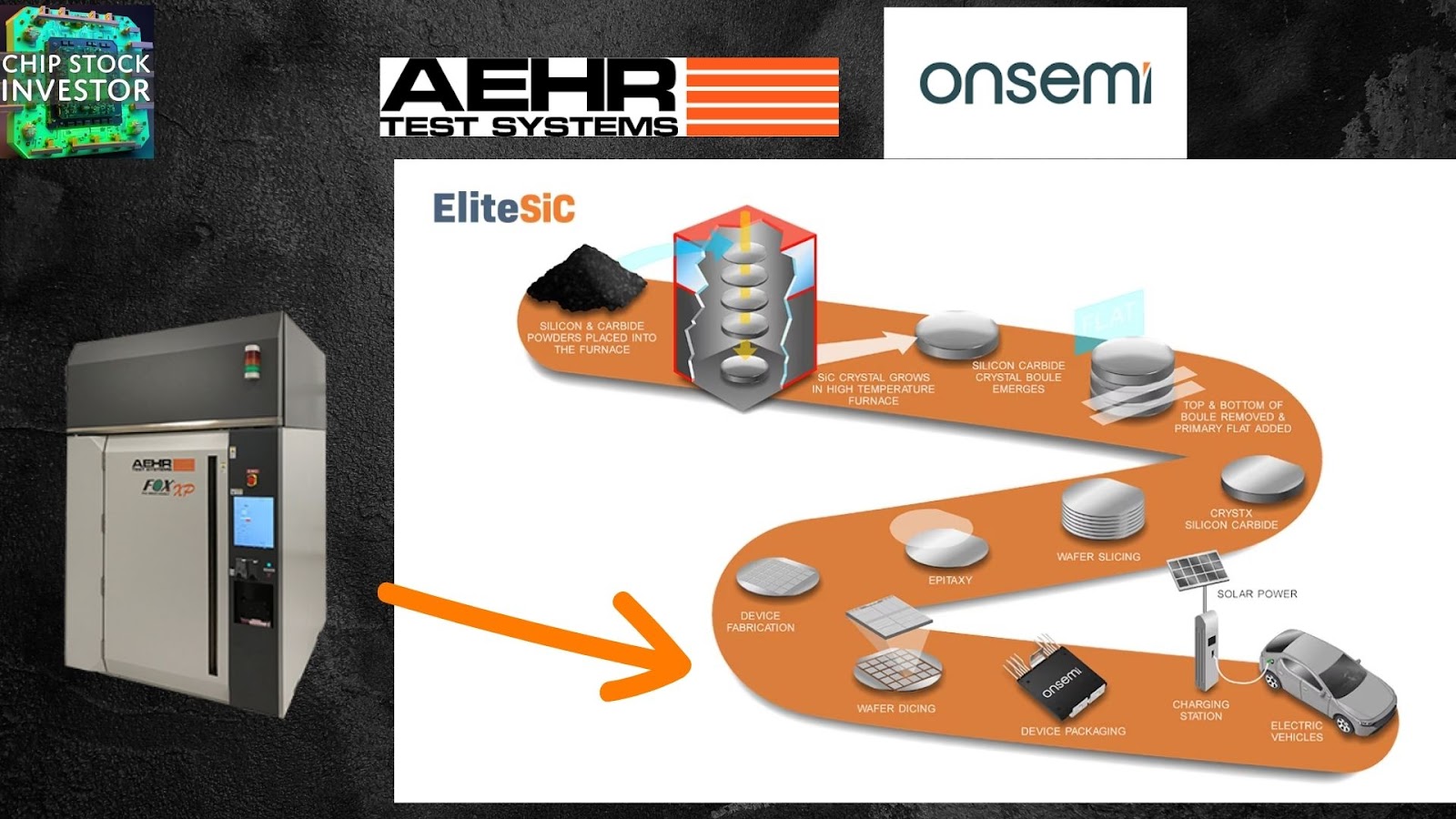

But SiC devices in particular benefit greatly from what’s called “burn-in.” Aehr’s equipment, the FOX family of systems, applies a high voltage to an entire SiC wafer (which later gets diced and packaged into devices). This not only weeds out early failure rates of SiC chips on that wafer, but burn-in also “ages” the substrate, stabilizing it for the high-voltage applications SiC is used in. Think of it like aging fine wine, or a fruit cake, if such things required the flow of electronics to be enjoyed.

To date, one SiC manufacturing leader – Onsemi (ON), also one of our portfolio stocks – makes up the majority of Aehr’s sales. In fiscal 2024 (ended this past May), Onsemi accounted for just over 67% of full-year revenue. https://www.sec.gov/ix?doc=/Archives/edgar/data/1040470/000165495424009642/aehr_10k.htm pg 54

These tests and burn-in of SiC wafers tend to occur either with the raw SiC wafer, or after the wafer has been developed but before it is diced into chips.

Let’s be realistic with fiscal ‘25 expectations

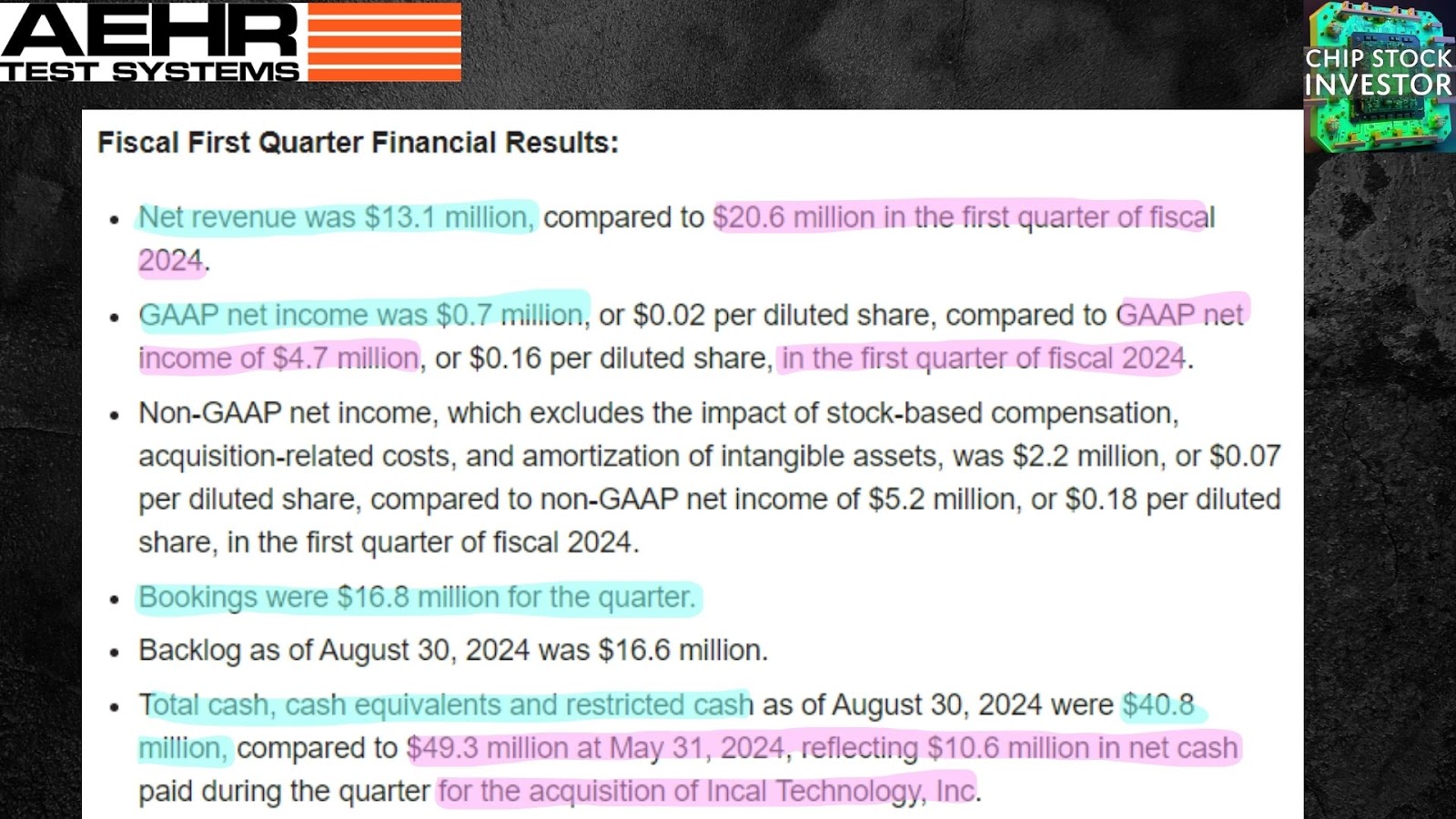

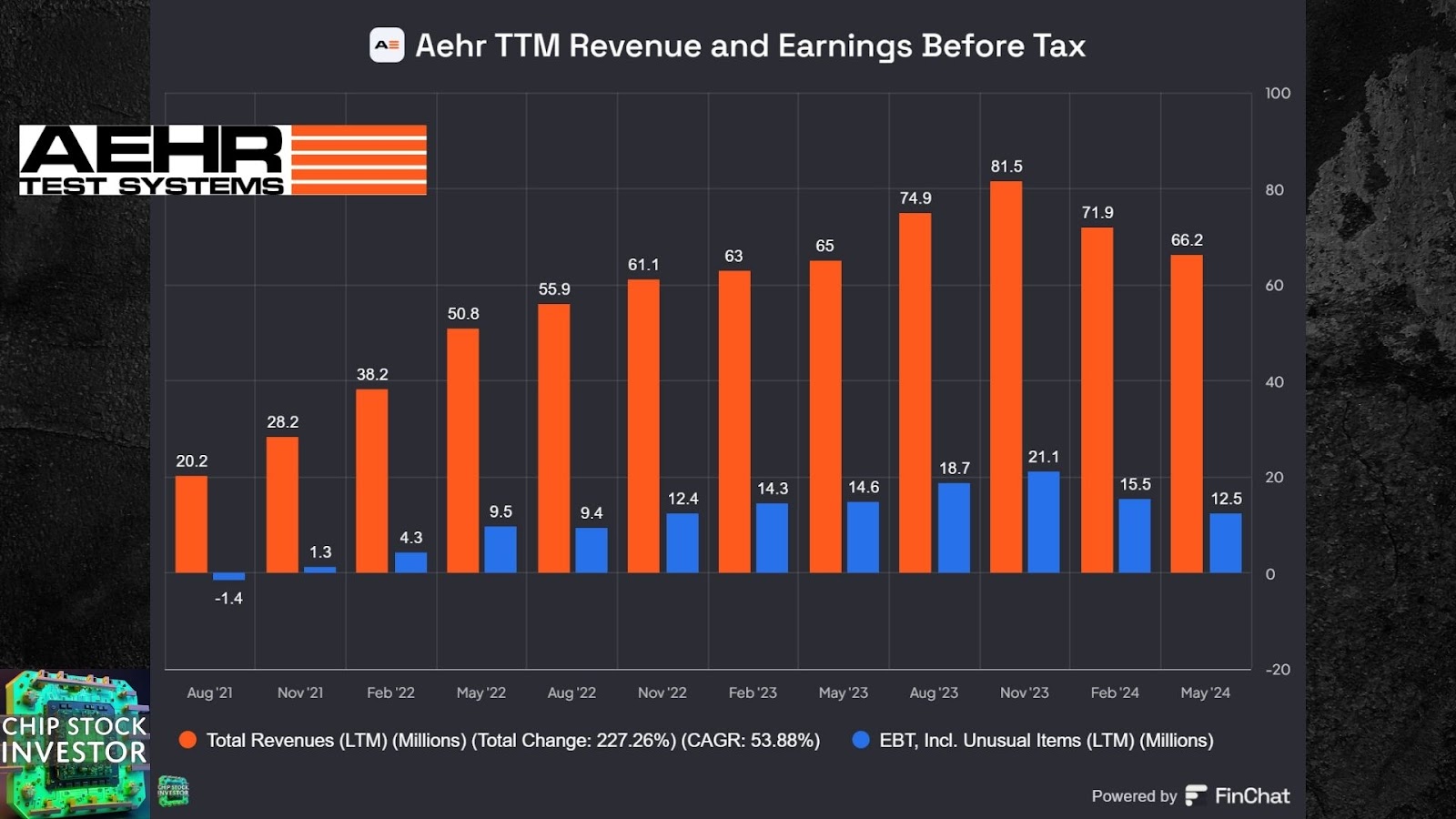

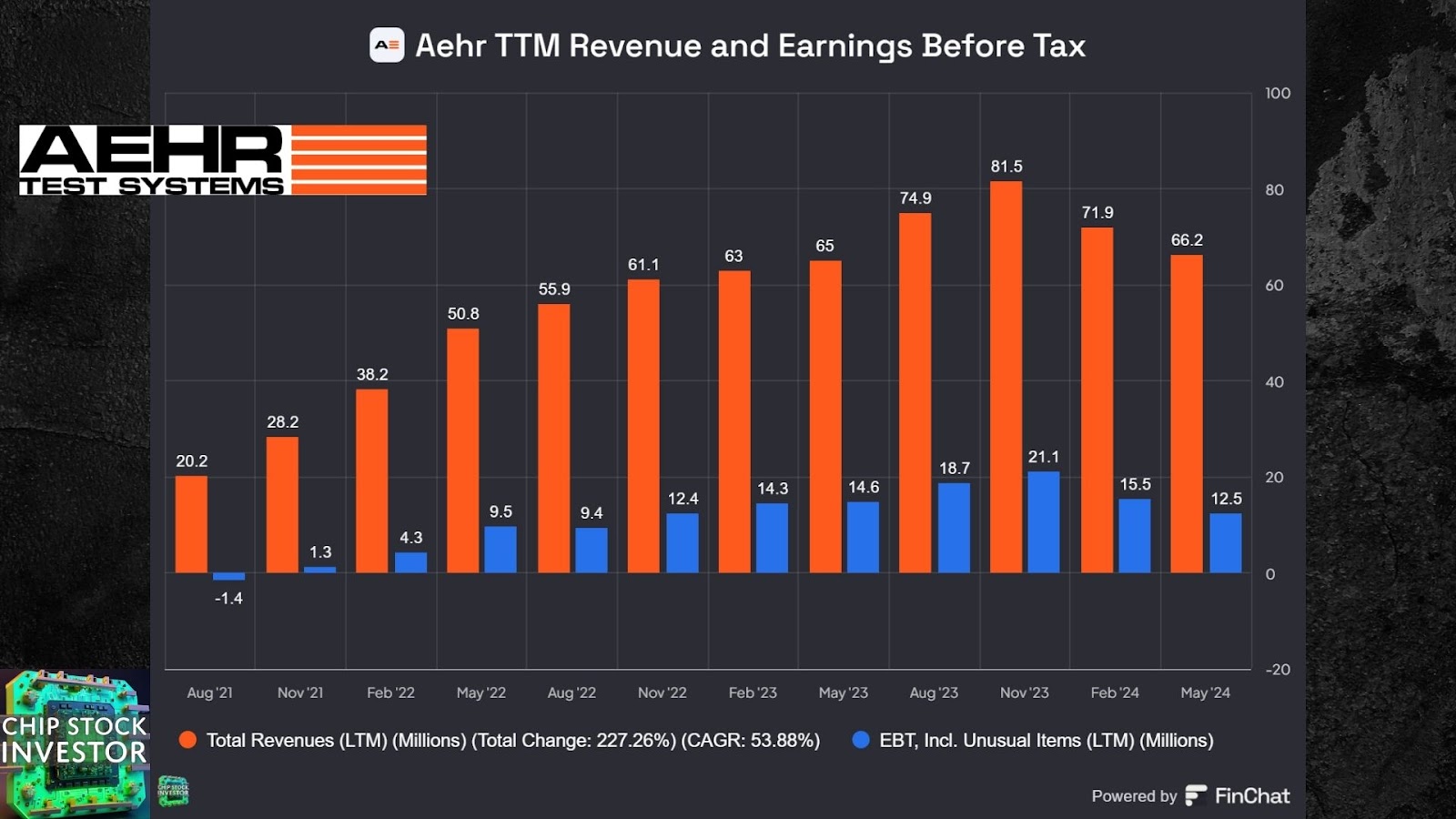

Aehr’s Q1 revenue and net income was down significantly year-over-year to $13.1 million, and down from the previous quarter as well, but this was not wholly unexpected. The company also managed a small GAAP net profit.

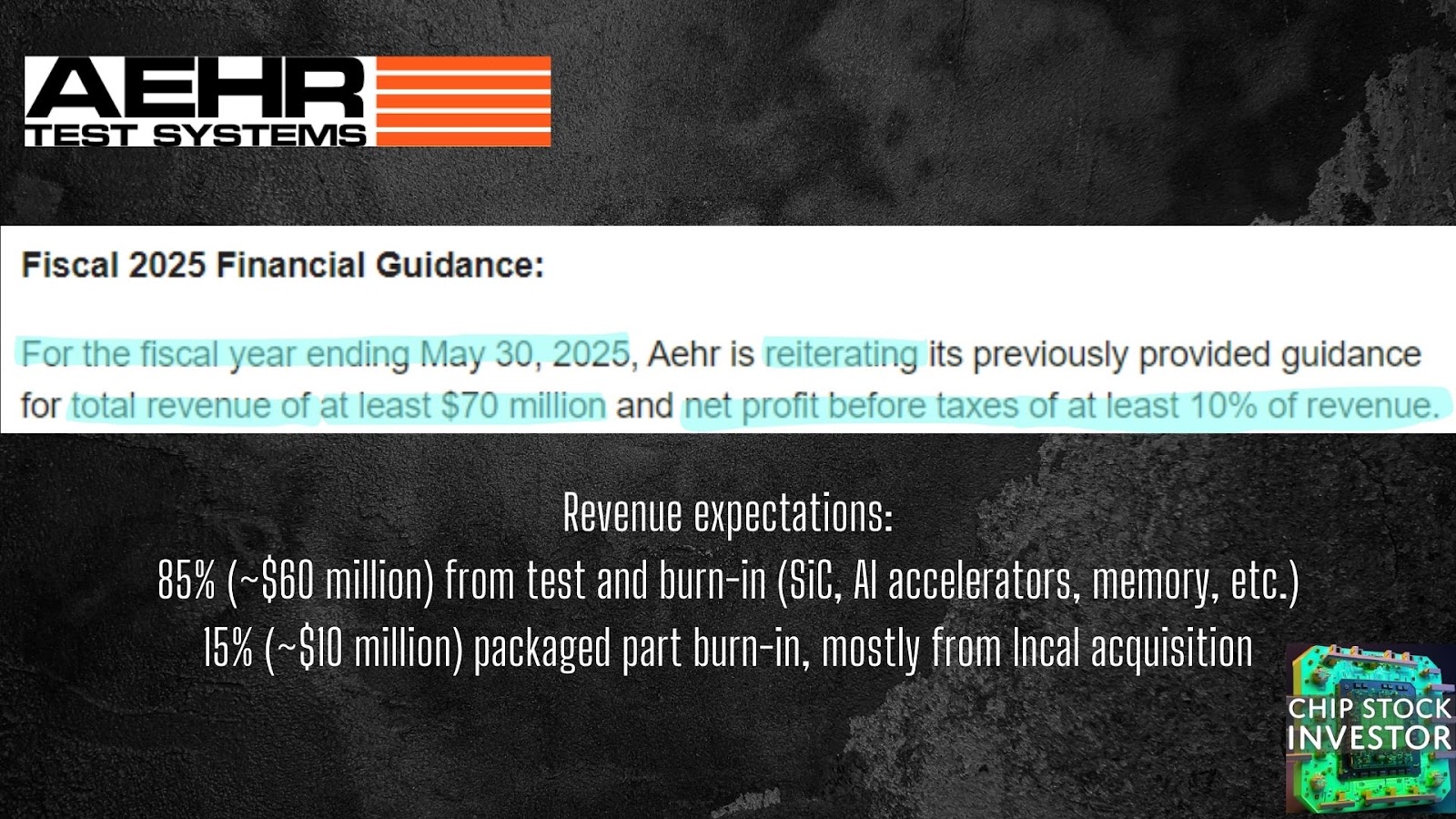

More importantly, however, and the likely reason for the stock’s rally after the report, was management reiterated the full-fiscal year guidance it issued three months ago.

Notably, some investors have soured on this outlook because Aehr just acquired a small peer called Incal. Incal provides test equipment for packaged electronics. As we break down above, excluding Incal’s expected contribution, Aehr’s expected revenue this year represents a sizable decrease from fiscal 2024’s peak sales.

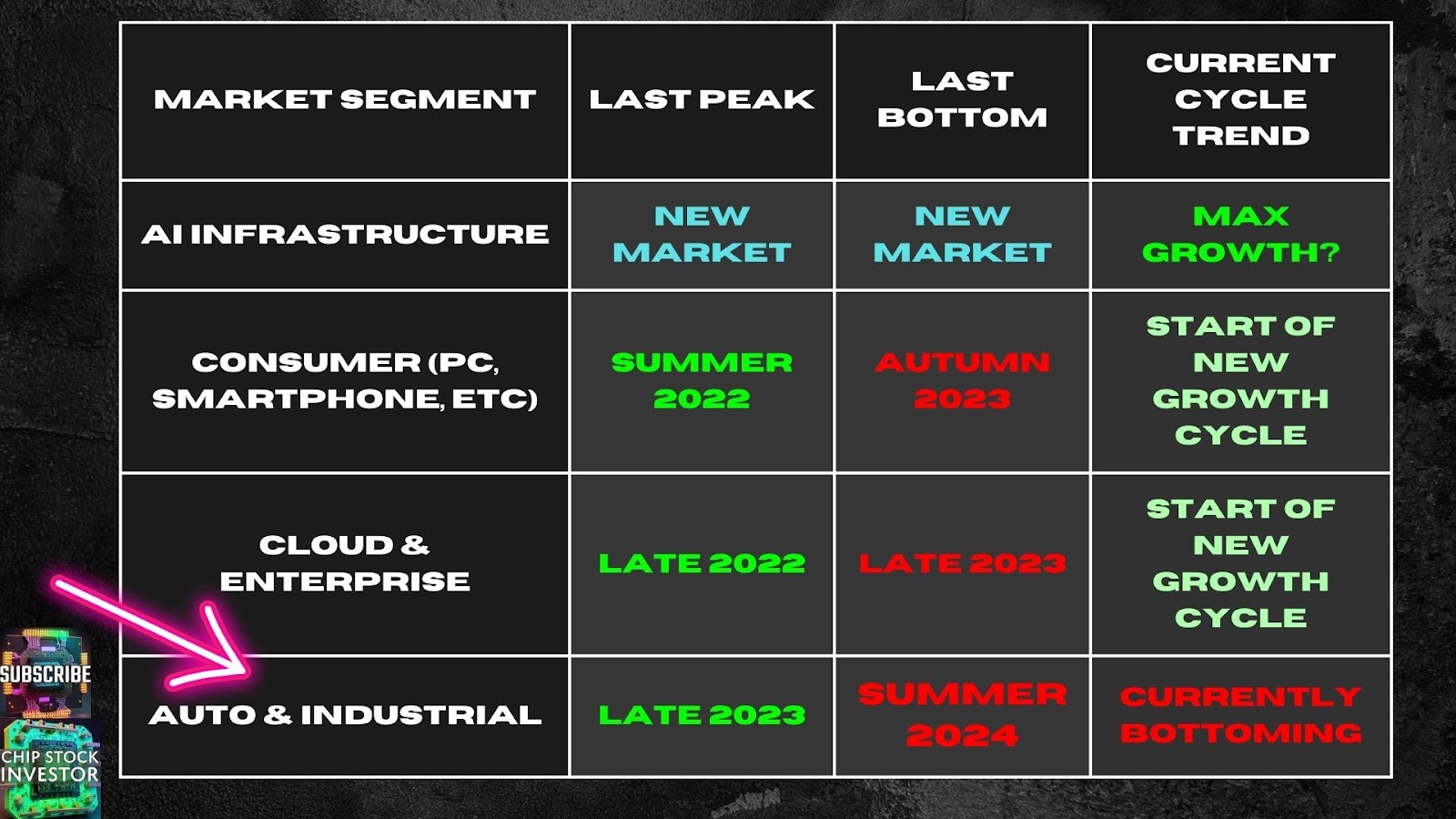

This shouldn’t really come as a surprise. The whole auto/industrial/power chip industry is in a downturn, driven largely by EV growth in North America and Europe stalling out this year and last. Reports from power chip manufacturers (like Onsemi) suggest demand is bottoming out and in the very early stages of a recovery. But for an upstream equipment provider like Aehr, the rebound will come later. Its customers won’t order more equipment until they’ve seen sufficient demand to warrant expanding their manufacturing capacity.

Thus, more patience will be required for those still holding out hope for a big Aehr stock recovery.

When will Aehr return to growth?

The good news is Aehr could be headed for sequential growth sooner than later. Why? Quarterly revenue was just $13 million in Q1 (or just $52 million on an annualized basis), but Aehr reiterated full-year guidance for $70 million or more. This implies sales are headed higher in the next few quarters, if management’s estimate is correct.

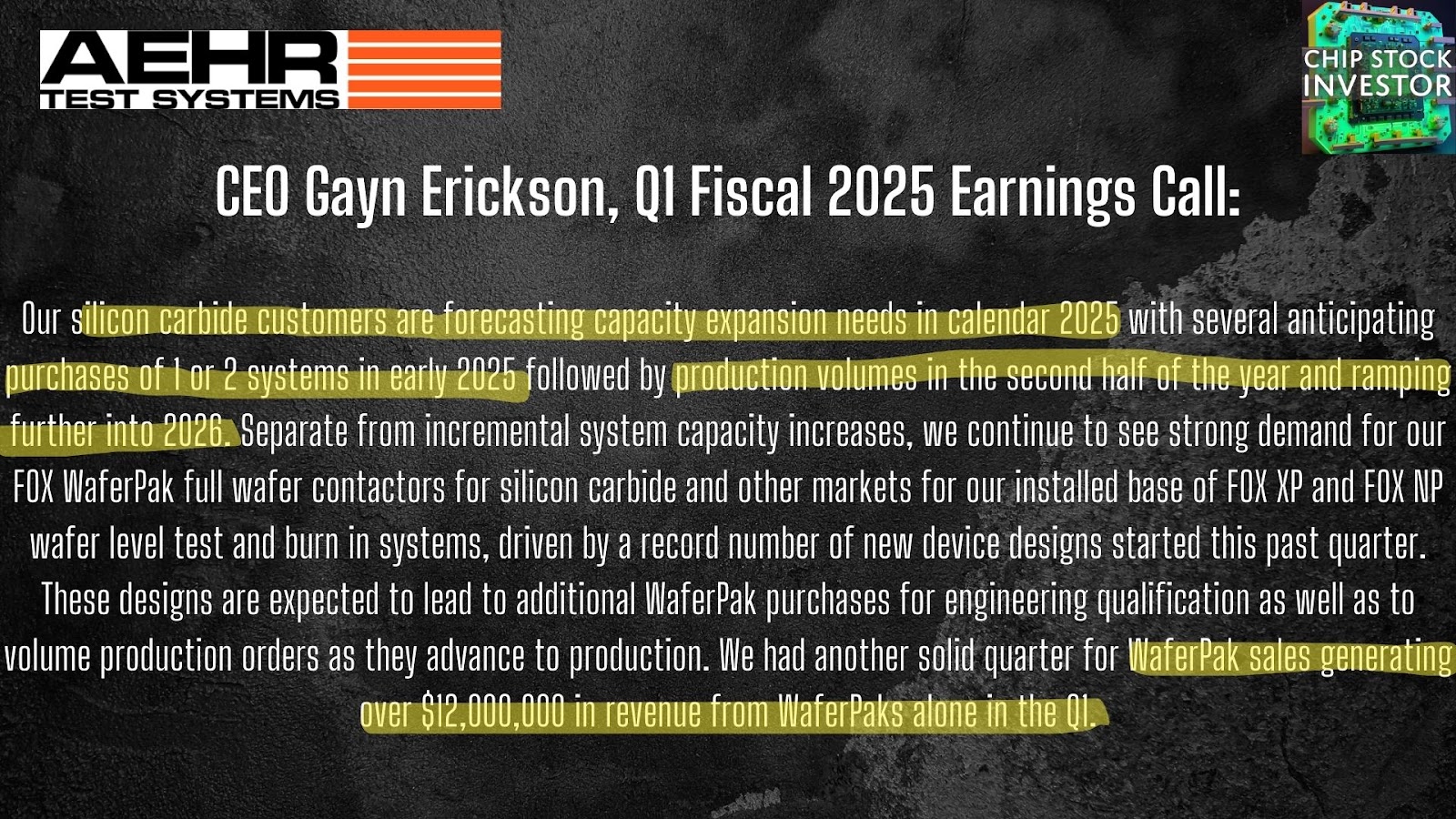

Better still, the next wave of SiC production expansion could continue into 2026. Aehr CEO Gayn Erickson said this on the earnings call:

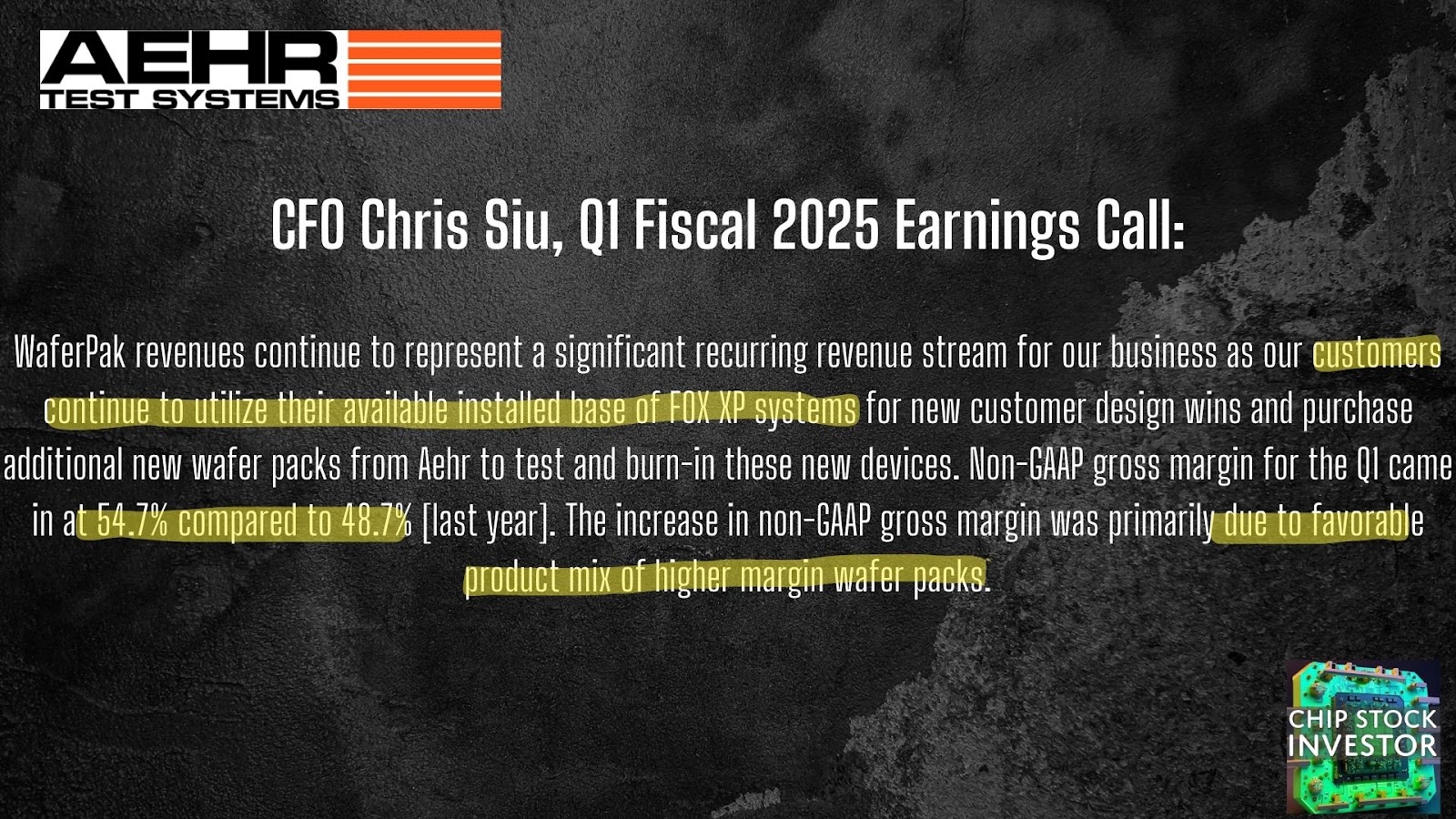

This is a positive comment regarding the sale of more test and burn-in equipment. However, for the time being, the WaferPaks (basically, a probe card used by the FOX test machines, that makes contact with and applies the electrical current to the wafer) are generating most of the revenue. Not bad, as these WaferPak sales carry a higher profit margin, but WaferPak sales aren’t going to grow Aehr’s business. More FOX system sales are needed to do that.

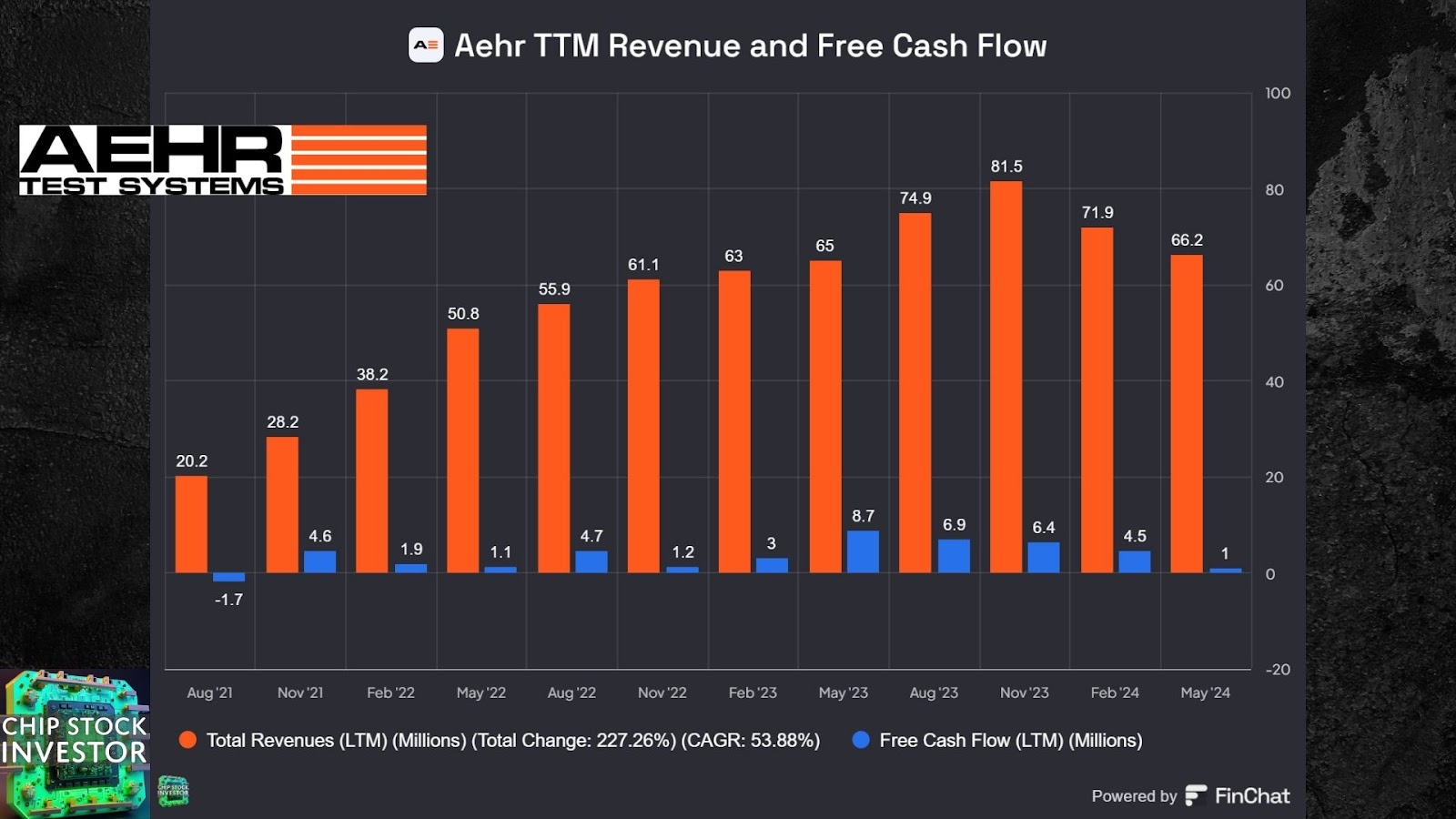

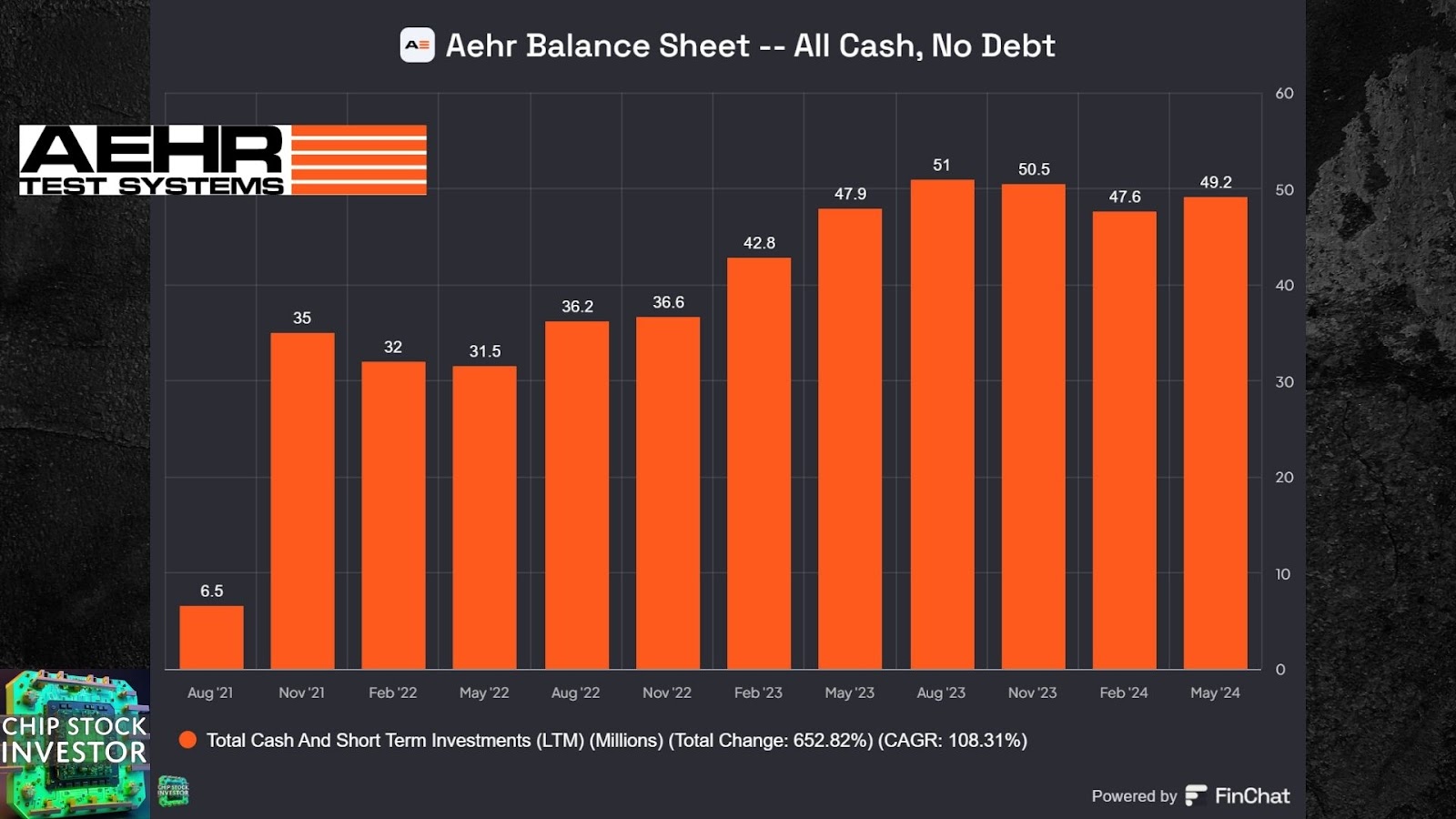

For those hungry (wine or fruitcake, anyone?) for some good news, though, this early indication points towards a structural rebuilding back towards Aehr’s peak revenue achieved in 2023. Perhaps by next summer of 2025, Aehr will be back. And in the meantime, the business remains profitable – both on a GAAP and free cash flow basis. Aehr also has adequate cash on hand even after acquiring Incal, so it’s in good shape as it waits for the next growth cycle to get underway next year (calendar 2025).

Aehr also has other irons in the fire, like the sale of test equipment to an “AI accelerator company,” as well as (finally, hopefully!) getting some traction in the memory chip market as well. Silicon photonics testing is still a possibility, but that will be a longer-term development. For now, the return of EV sales is the driving force behind Aehr’s ultimate performance – both as a business, and a stock.

We will likely get some more insight into the EV and broader power chip market when Onsemi reports on October 28.

For now, we are content holding our small position in Aehr as part of our “small bets with potentially big upside” basket of our portfolio. We aren’t sweating the wild swings in stock price, and feel no urge to try and babysit this one. Aehr will simply take more time to rebuild, if that’s the final outcome. If you’re a buyer at all, remember to keep the position very small. No need to potentially blow up your portfolio in the hopes Aehr is some sort of “next big thing.”

See you all again next week for our quarterly updates on TSMC and ASML, and if you’re only here for AEHR coverage, we’ll see you in 2025!