It’s 2026, and investing in AI is not so simple anymore. Gone are the days when just buying Nvidia (NVDA) and forgetting about it was good enough.

In fact, investors are now grappling with what seems to be a paradox: AI data center and cloud operator (hyperscaler) stocks, and enterprise software company stocks (the ones feared to be disrupted by AI), are all getting punished.

It seems the only safe place to make money so far in 2026 are the memory and optical networking chipmakers! What is going on?

The AI stock paradox explained

Given the potential of AI, it would stand to reason that someone‘s stock should be winning right now — if not the hyperscalers, then their software customers building new AI products. Or if neither, why not the biggest chip suppliers like Nvidia? It’s a paradoxical situation… at least on the surface.

The hyperscalers and their massive data center assets are in prime condition to win in the AI era, but the data center infrastructure is getting incredibly expensive to build.

Software’s total addressable market is getting much bigger thanks to AI, but a new research & development cycle has expenses rising.

As for the AI chip suppliers, an end to the hyperscaler data center growth cycle always needs to be factored in (data center spend is directly correlated to semiconductor company revenue growth, or lack thereof, right now).

All stocks are valued based on future cash flows (profit). With this new fledgling AI industry in all-out construction mode right now, cash flows for a lot of companies are down, or at least viability of future cash flows are being called into question. And that future outlook on cash flows must be discounted. The “AI stock selloff” paradox (lower business valuations), in all reality, isn’t a paradox at all. It’s a sign of market still operating with a healthy dose of skepticism.

It’s a nerve-racking time to be invested, but such is always life for an investor.

Turning to the 2026 AI infrastructure build outlook

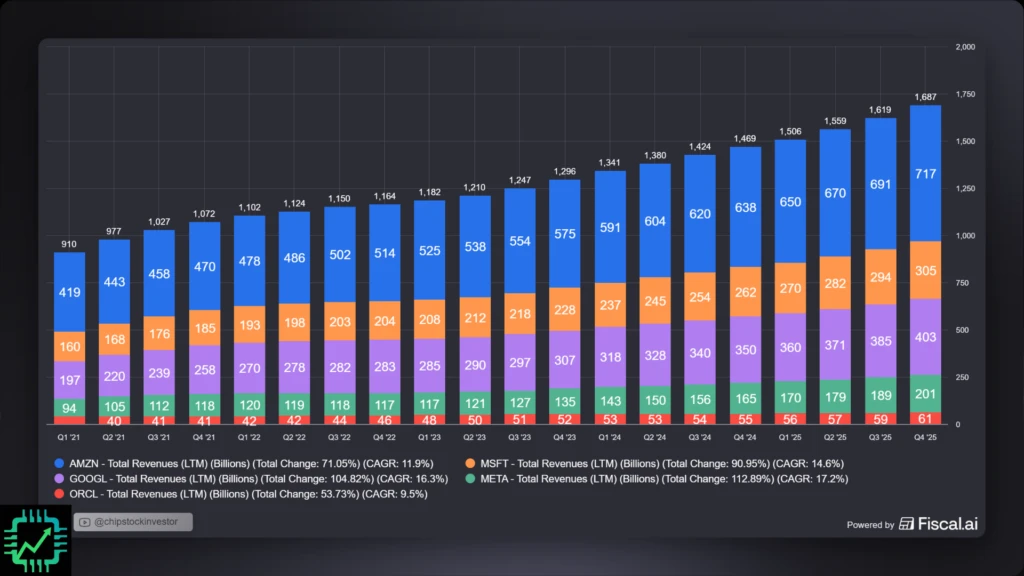

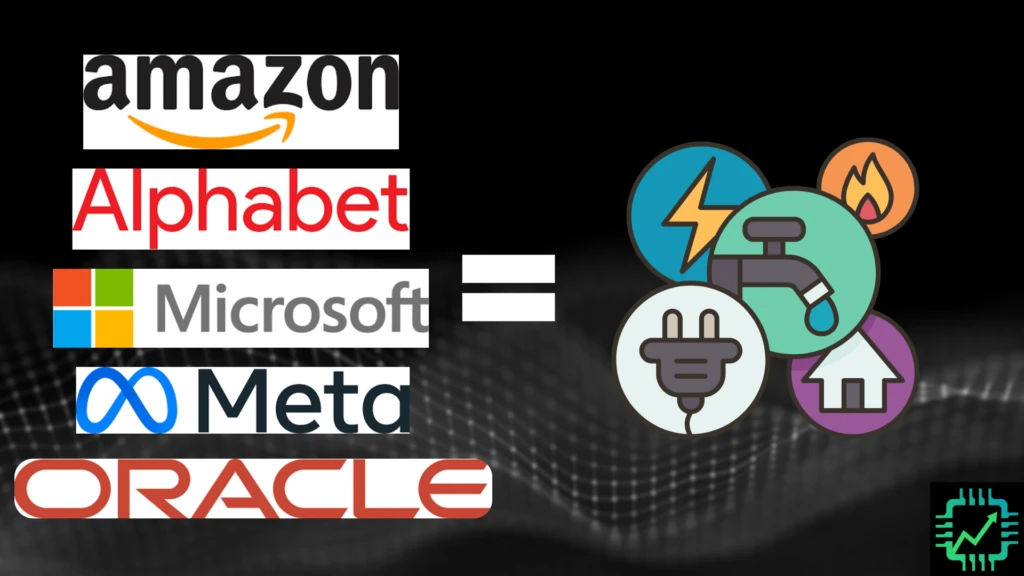

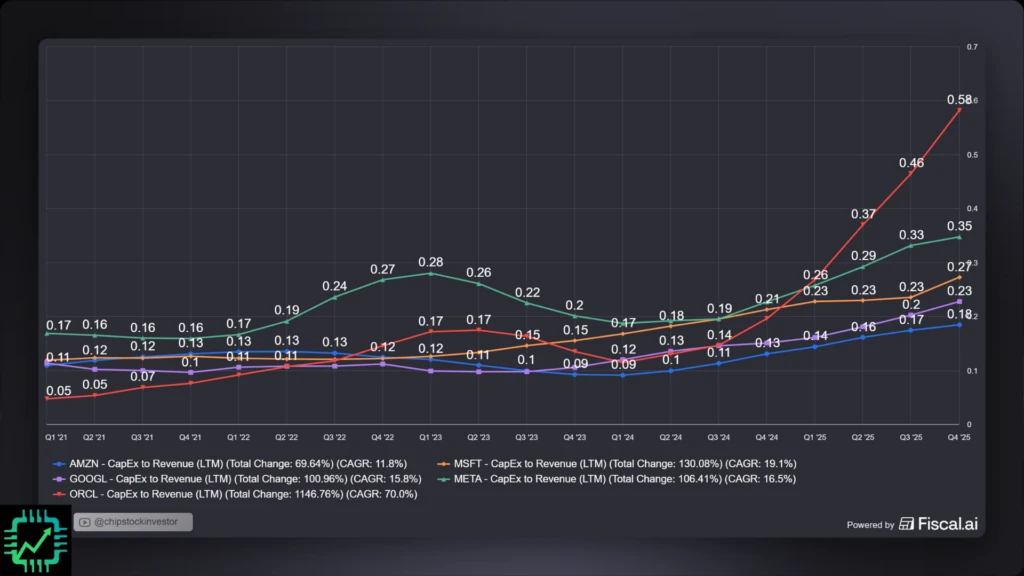

To help explain the ripple effects AI is having on the global economy, let’s focus on the hyperscalers — Amazon, Microsoft, Alphabet (Google), Meta, and the relatively small newcomer Oracle. The financial markets are getting jittery as these companies are each spending tens of billions of dollars every quarter on capital expenditures (CapEx, spending on property and equipment, in this case data centers and servers).

But the upshot? These tech giants are reporting mind-boggling revenues, and the growth rate has been overall accelerating. Total revenue has gone from ~$900 billion in annualized sales five years ago, to nearly $1.7 trillion in calendar year 2025. The hyperscalers have picked up an extra $200 billion in sales in the last year alone.

Thanks to our friends over at Fiscal.ai for these visuals. Get 15% off your own paid plan using our special link, plus new reduced pricing on Fiscal’s financial research terminal! Fiscal.ai/csi/

Data center compute is essentially a modern utility business model. Can’t afford to build your own AI and high-performance computing infrastructure? Yeah, most can’t. That’s ok, a hyperscaler can rent out to you only what you need!

The bad news? Demand for this data center computing infrastructure-for-rent is skyrocketing, and the hyperscalers are in build mode (the reason for the stock volatility above). In fact, expectations for 2026 CapEx keep getting raised. It’s a race to capture future customer demand.

As a reminder, and in simplest form, free cash flow (FCF) profitability = Cash from operating activities – CapEx

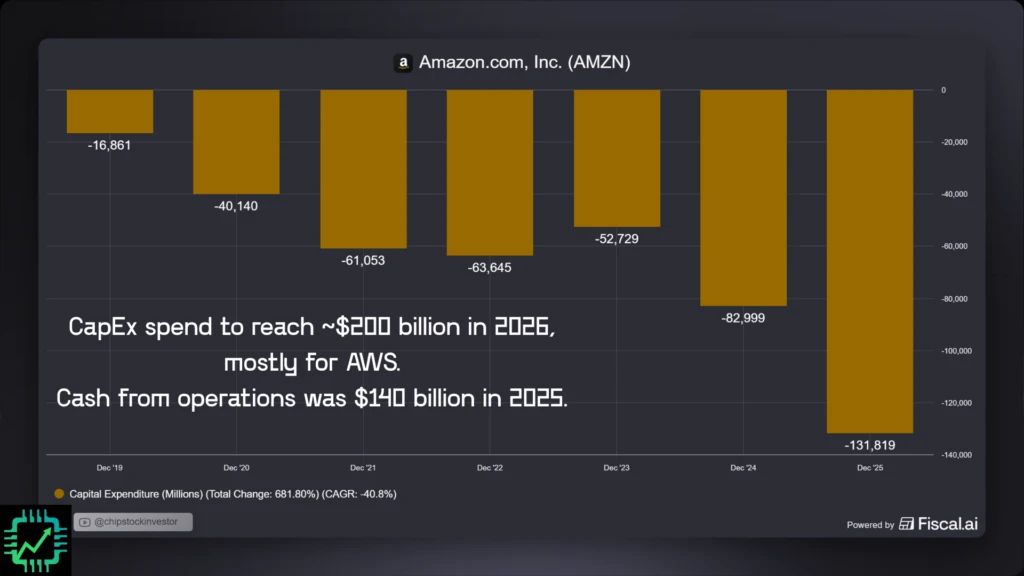

- Amazon’s 2026 CapEx guide is $200 billion, implying a 52% year-over-year increase

- 2025 cash from operations was $140 billion

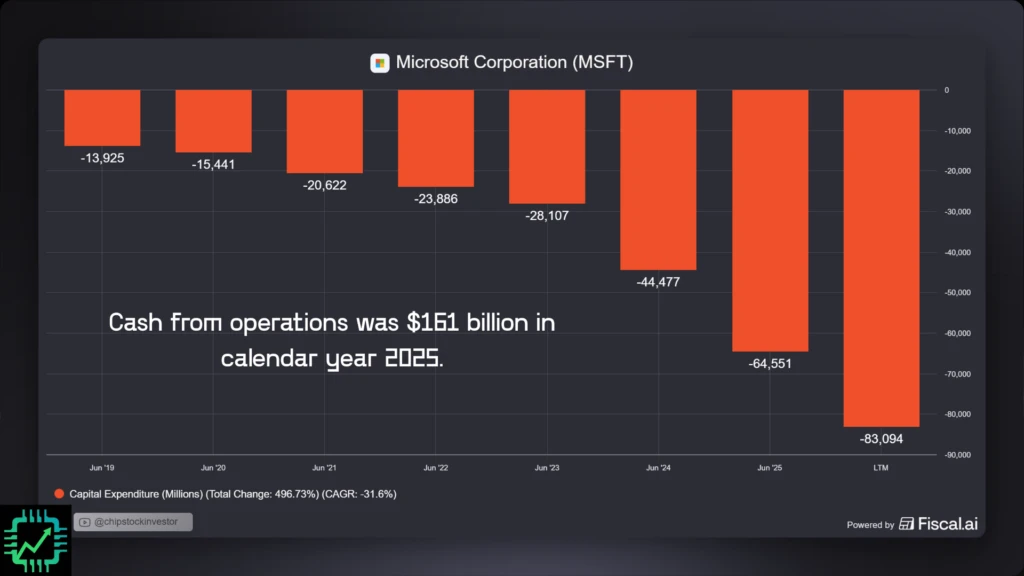

- Microsoft’s 2026 CapEx guide hasn’t been provided (the company’s fiscal year ends in June 2026), but CapEx in calendar year 2025 was $83 billion, rising 28% over the trailing-12-month period that ended just six months prior (fiscal 2025 ended last June)

- Calendar year 2025 cash from operations was $161 billion

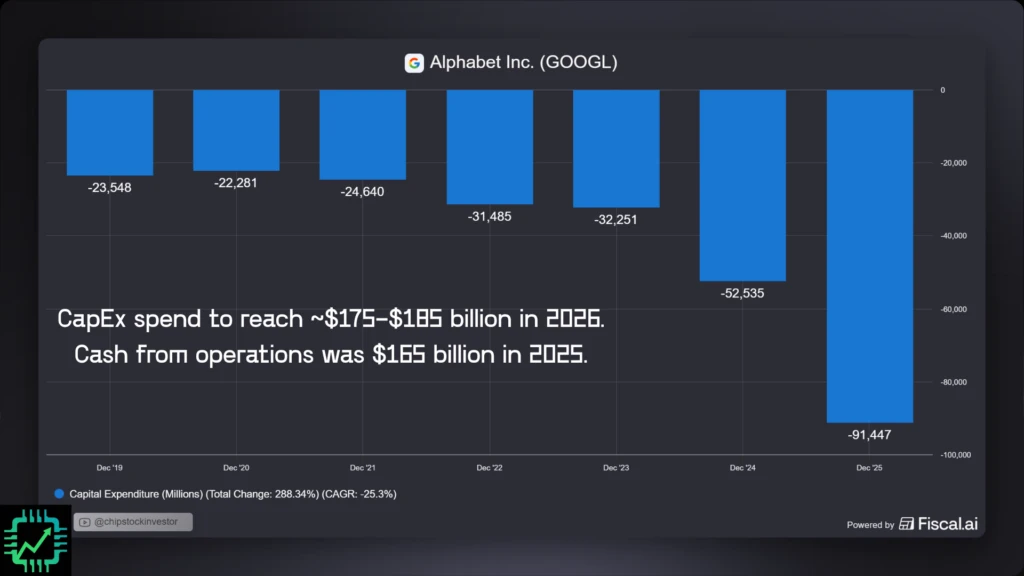

- Alphabet’s 2026 CapEx guide is $175 to $185 billion, implying a 98% year-over-year increase at the midpoint

- 2025 cash from operations was $165 billion

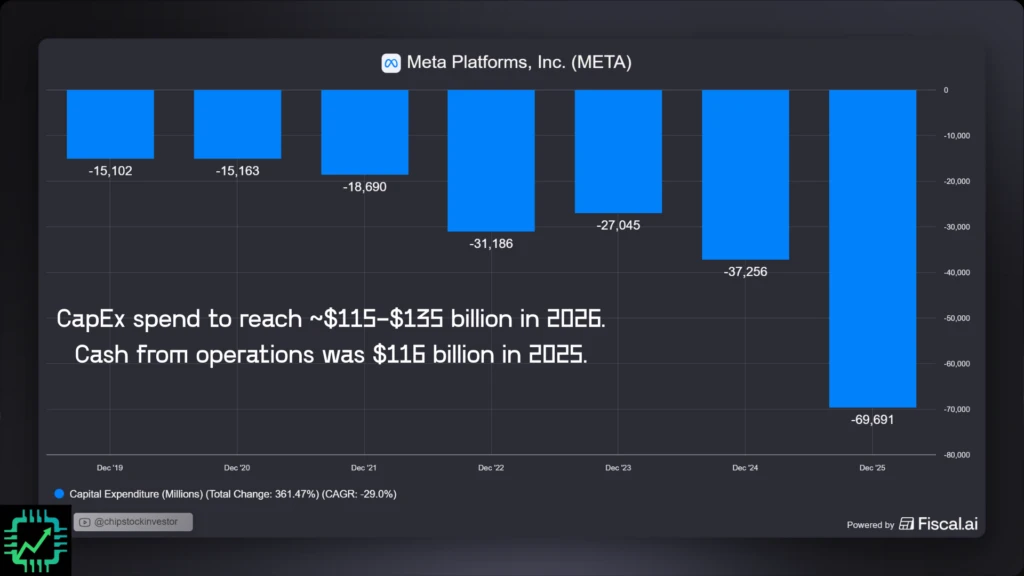

- Meta’s 2026 CapEx guide is $115 to $135 billion, implying a 79% year-over-year increase at the midpoint

- 2025 cash from operations was $116 billion

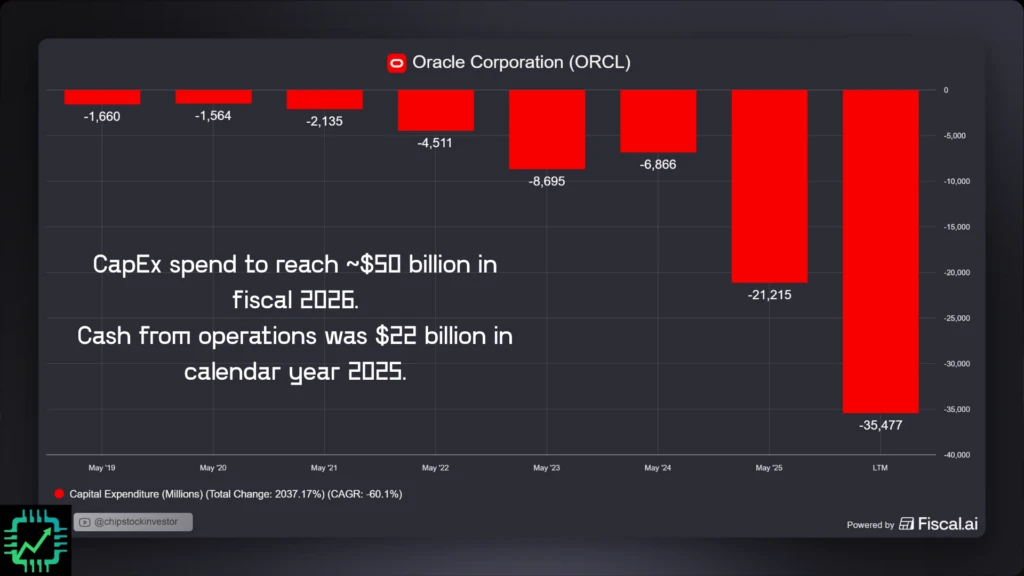

- Oracle’s fiscal 2026 (year ended in May 2026) is for $50 billion, implying a 138% year-over-year increase from fiscal 2025

- Calendar year 2025 cash from operations was $22 billion

It’s not hard to see the hyperscalers are racing to get data center infrastructure built, and are willing to spend nearly all of their operating profit to do so — if not a bit more, dipping into their deep pockets (cash on balance) to keep up. We’ll continue to use CapEx-to-revenue ratios to monitor this epic buildout. At some point, the hyperscalers will need to settle into a more steady rate of CapEx spend. But there’s no telling just yet where that natural ratio will settle once the industry matures.

In the meantime, the trade-off to the chart above is tens-of-billions-of-dollars of incremental revenue every quarter. Only you can decide if the current CapEx cycle is worth that for your portfolio.

As a result, it’s going to be a banner year for semiconductor suppliers, and data center server designers and builders. The bumper year won’t last forever, though. We continue to view the hyperscalers and their massive CapEx cycle as a natural “soft hedge” when paired with top semiconductor stocks.

However, caution is warranted. The “bullwhip effect,” made famous during pandemic-era global supply chain disruptions, is showing signs of making a comeback. AI data center demand, especially for sold out memory products, is having an effect on other areas. Chief among them being consumer electronics. Qualcomm just reported disruption to its smartphone chipset sales for this year due to customers managing supply from memory unavailability.

As we’ve discussed over the last month-and-a-half, current momentum is favoring the optical networking and memory chipmakers. Value can still currently be found in the auto/industrial/power chip companies. And of course, though shares have sold off once more, the lion’s share of profit in semiconductor land will be made by leaders like Nvidia and Broadcom (AVGO) in 2026.

And beyond semi suppliers and the hyperscaler utilities, software is down in the dumps. It’s a painful trade to make right now. But if you believe select software companies will benefit from AI over the next five years and beyond, value is certainly there at the moment. Meltdowns like we’ve seen so far in 2026 always yield opportunity for investors. This time will be no different, if you’re willing to look beyond the media-fueled narratives.

Have you tried Semi Insider yet? Join for more on the above conversation! We also have a very simple easy-to-use DCF (discounted cash flow) calculator built in now, so you can gauge what is currently factored into a stock price by the market. Try it now! chipstockinvestor.com/membership/

One Response

Unbelievable amount of cash out, totally 600 bln for 2026. And where is this cash going, with other words, for which companies this is cash in? I guess a huge part is continuously spend on data centers. That means suppliers of CPU’s, memory, connections, cooling eq., etc.

Down the supply chain it will go; Fabs, semi equipment, packaging, testing, materials…