Led by Nvidia’s (NVDA) accelerated computing platform, we believe data center infrastructure is on pace to become the largest end market for semiconductor sales in 2025. This will make chip sales to data centers larger than the mighty smartphone and mobile end market – the key pillar of the bull market of the 2010s.

Colloquially referred to as the cloud (in simple terms, computing power available for rent), the companies setting the pace for this data center boom are often referred to as “the greatest businesses to have ever existed.” Last week’s blog addressed whether these businesses are a bubble in the stock market. https://chipstockinvestor.com/a-magnificent-7-bubble-and-sp-500-concentration-risk-is-it-real-if-so-how-do-investors-cope/

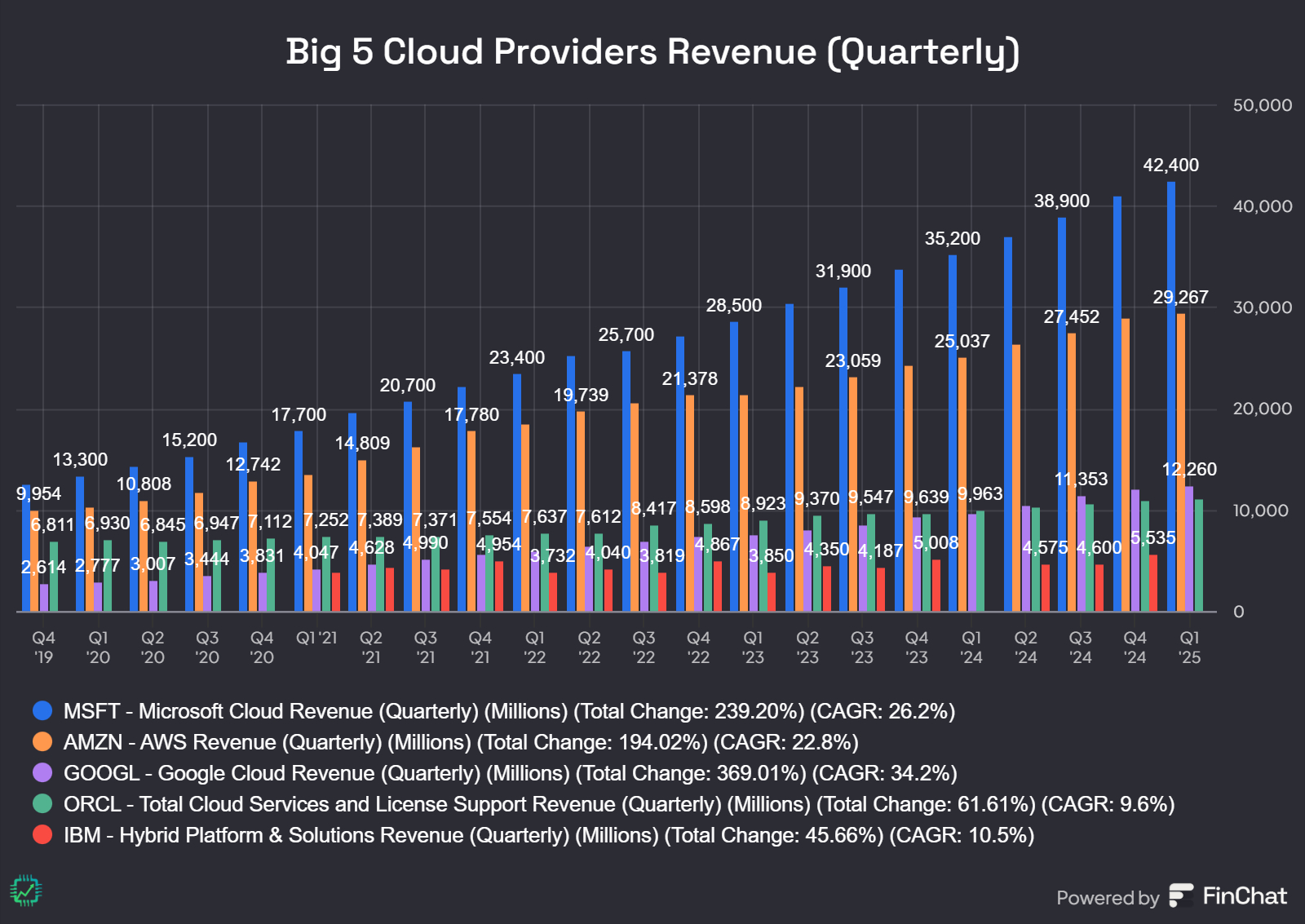

What is the current makeup of the cloud businesses providing data center infrastructure for rent? Below are the five big cloud providers’ revenue (excluding Meta, which operates its data centers primarily for its apps Facebook, Instagram, and WhatsApp) on a quarterly basis from the last five years.

To make your own financial visuals like the one above, check out Finchat.io! Use our link, Finchat.io/csi, for 15% off any paid plan.

But within these “Big 5” modern 21st century infrastructure and utility companies, there are caveats and key differences. For example, Microsoft, Oracle, and IBM in particular are legacy software businesses, so their platforms differ materially from those of Amazon and Google. So let’s break them down one by one to get a sense of where the biggest semiconductor sales outlet is headed.

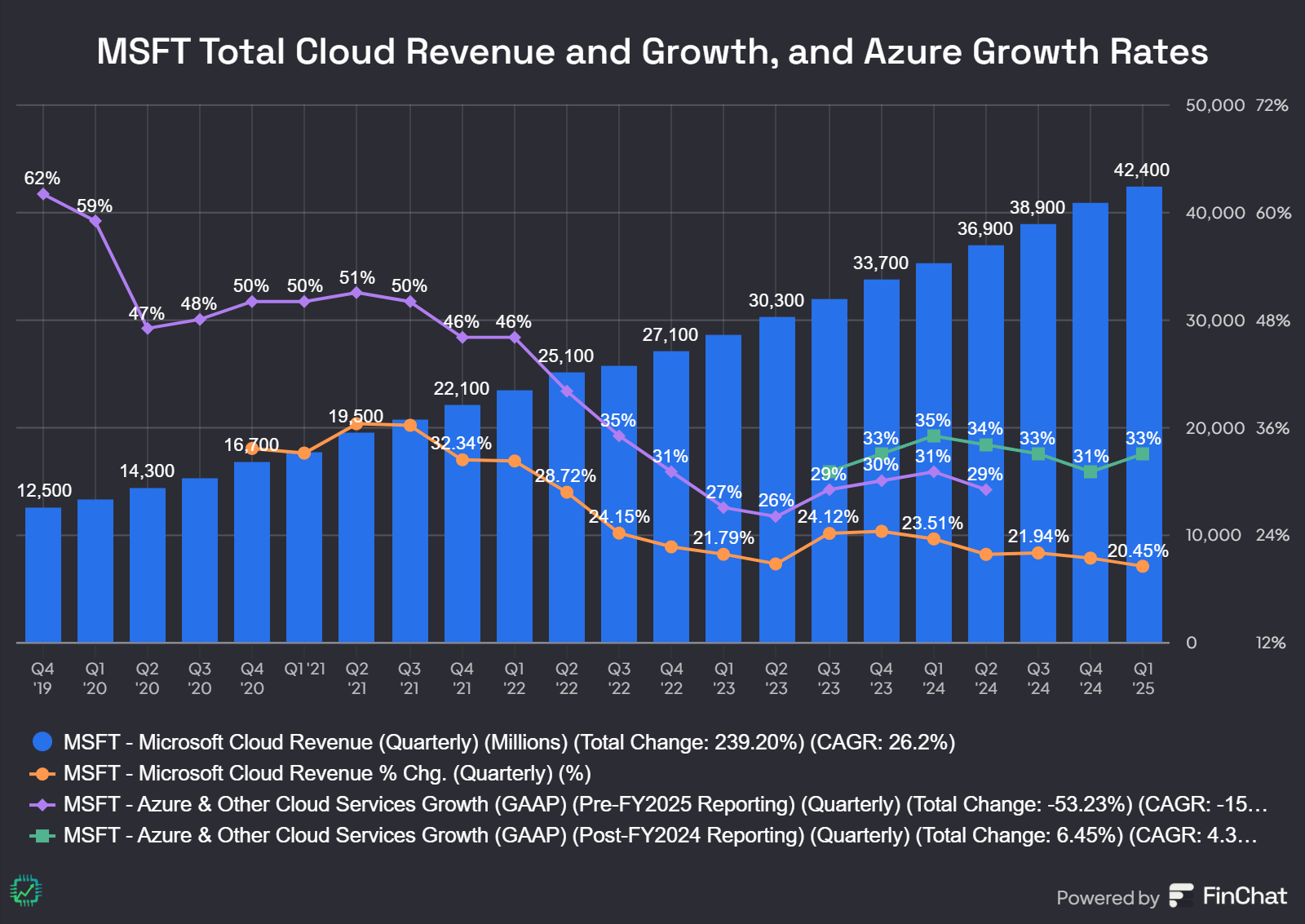

1. Microsoft (NASDAQ:MSFT)

As stated above, Microsoft is an old software company that pre-dates the cloud. Its total cloud revenue metric includes both infrastructure services (Azure) as well as older cloud-hosted software products, server products, and support.

Microsoft doesn’t give specific revenue numbers for each, but does give Azure’s growth rate (a clearer picture of its infrastructure services growth metric minus software products). Also, starting with fiscal 2025 (began July 2024), Microsoft internally shuffled the Azure segment and recast the growth rate, making for the higher reading for fiscal 2024 and 2025 in the chart below.

It would be nice to know exactly how large the Azure infrastructure business is for the sake of comps, but such is life. We’ll take what we can get. Note: the below chart plots Microsoft Cloud and Azure quarterly figures on a calendar year basis, not on Microsoft’s fiscal year basis (each MSFT fiscal year ends in June).

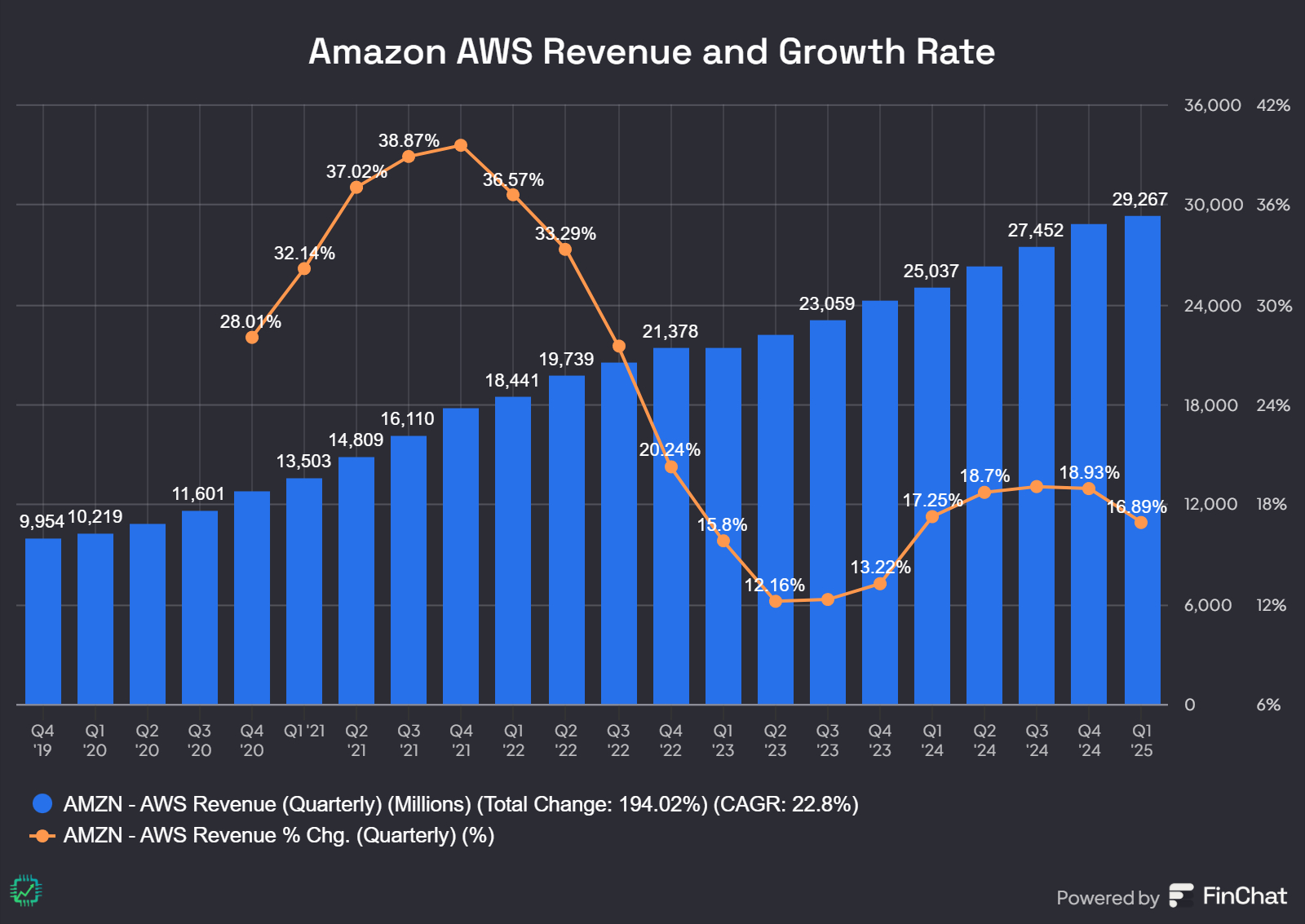

2. Amazon (NASDAQ:AMZN)

Amazon’s AWS is of course the big disruptor, the company that pioneered the “cloud” back in the late 2000s and especially 2010s by renting out its excess data center computing power.

As such, Amazon AWS is primarily a cloud infrastructure business, with some services and third-party software resales mixed in (as is the case for most infrastructure businesses, including Google Cloud). Amazon’s software business is housed in the e-commerce side, especially the Amazon advertising segment.

In other words, Amazon AWS often gets credited as being the largest cloud provider, given that it’s a pure-play reported segment, versus Microsoft’s more messy mix of cloud software product + Azure revenue report. Also, to this day, AWS still makes up the bulk of Amazon’s operating income (61.5% in Q1 2025), despite AWS only accounting for 17% of total Amazon revenue.

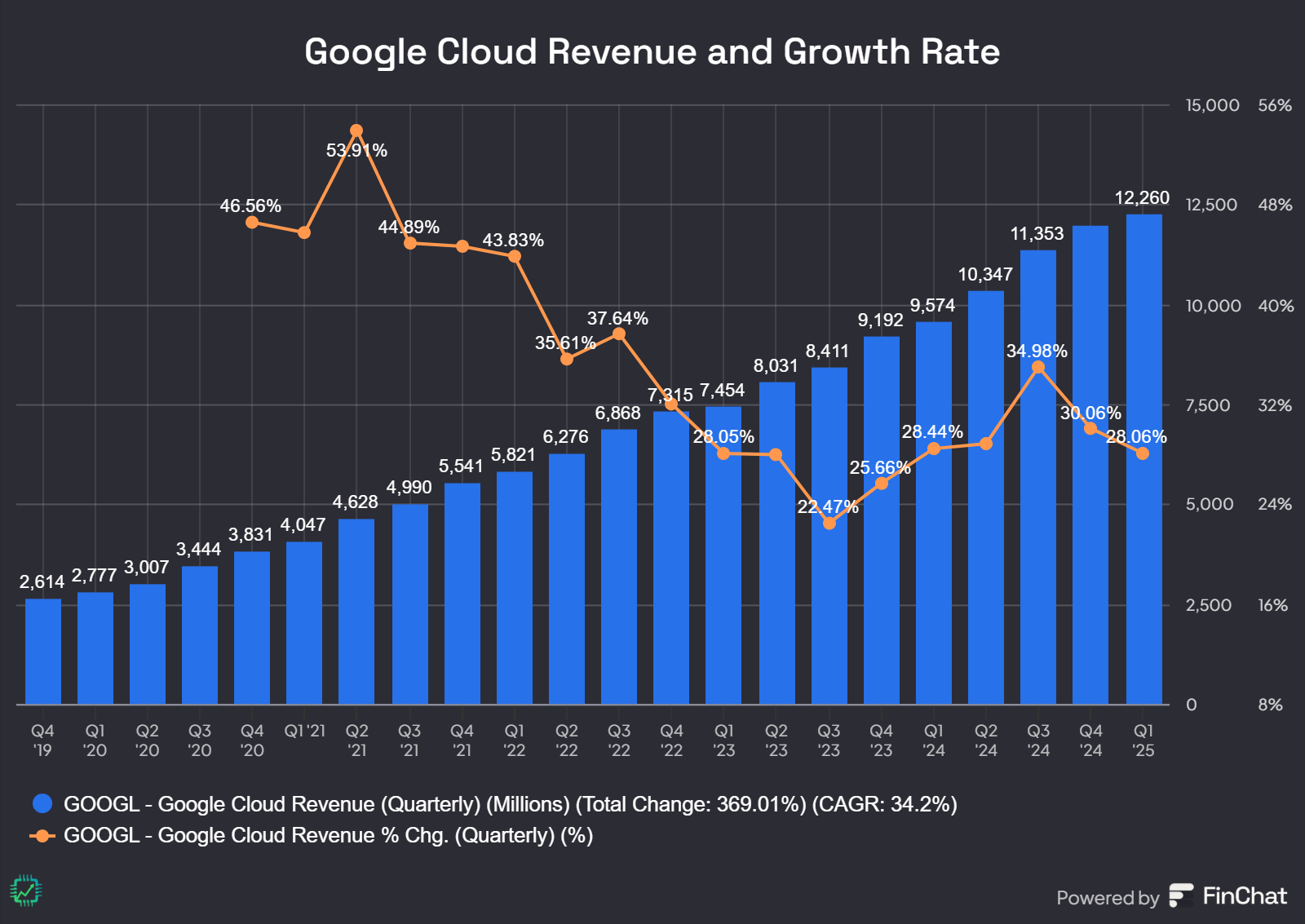

3. Google Cloud (NASDAQ:GOOGL/GOOG)

Alphabet’s Google Cloud is also a computing infrastructure “pure play,” without all the messiness of a legacy software products provider mixed in. Thus, similar in structure to Amazon AWS above. Google Cloud picked up on the “rent your spare data center compute to customers” trend later on, likely because its data centers were built for Google Search and didn’t have the big “spare compute” problem Amazon did back in the 2000s.

Google Cloud flipped to an operating profit the last few years, so it’s currently the most important profit growth lever for Alphabet right now. It’s also clear Google wants to bolster its position as a go-to place to build AI and AI apps with its focus on in-house cybersecurity (acquired Mandiant a couple years ago, in process of acquiring Wiz). See our blog on this topic (https://chipstockinvestor.com/what-is-cnapp-besides-google-who-else-is-investing-in-the-next-big-thing-in-cybersecurity/), and there’s even more detail over on Semi Insider.

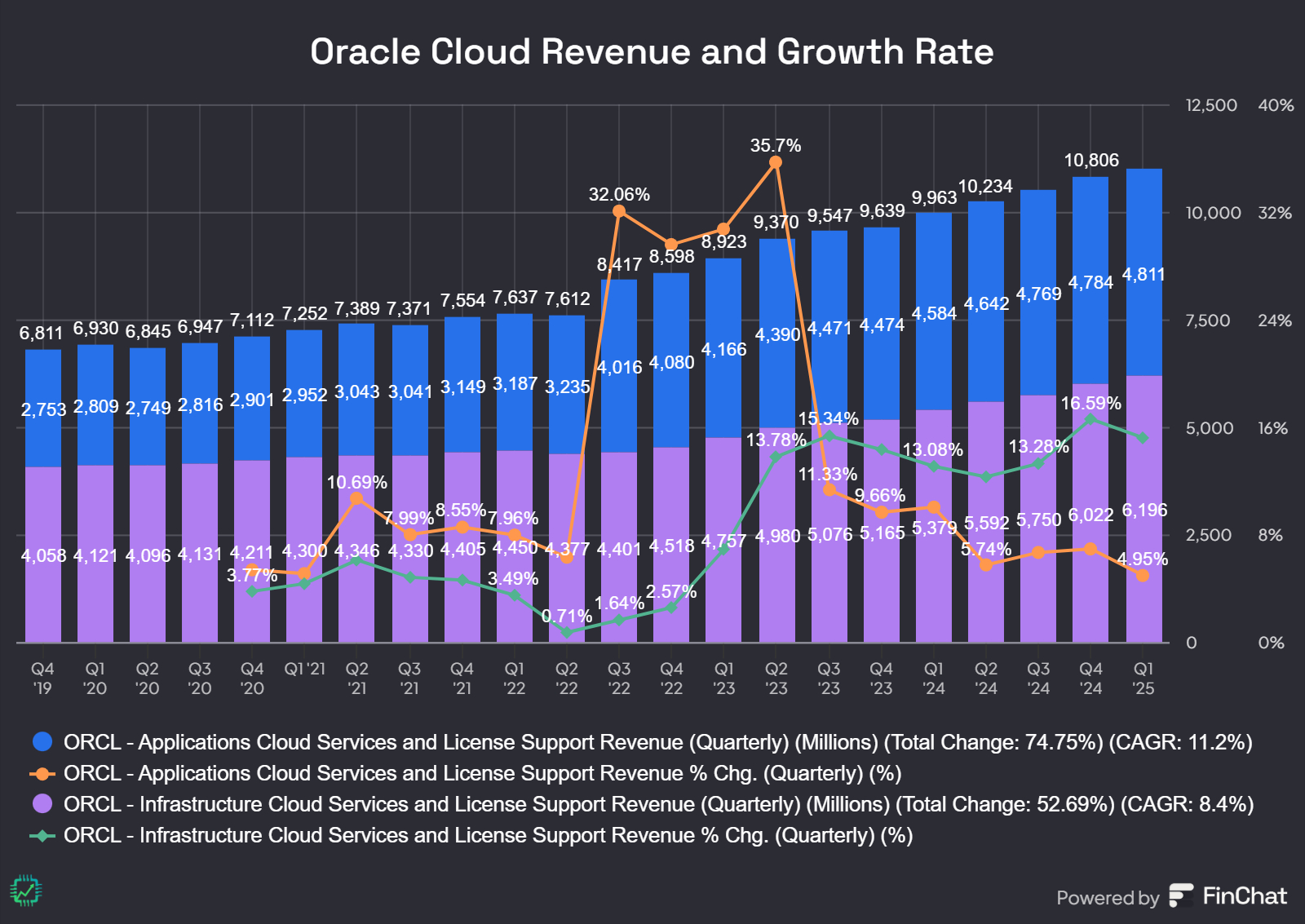

4. Oracle Cloud (NYSE:ORCL)

We’re back to legacy software provider-turned-cloud infrastructure business. Oracle Cloud has reignited the old and dusty Oracle machine. But much like Microsoft, its “cloud” segment includes both software products and infrastructure.

But, unlike Microsoft, Oracle gives us the luxury of knowing the breakdown between what part of its cloud revenue is software (apps) and which is infrastructure. Oracle Cloud Infrastructure (or OCI, an IaaS or infrastructure as a service solution), is the high-growth segment, thanks in no small part to OCI’s first-mover advantage on Nvidia H100s back in 2022 when most investors were freaking out about the bear market.

For reference, Oracle completed the big acquisition of healthcare software company Cerner the summer of 2022, which is what accounts for the “Apps” growth rate heat-up at that time. Also, Oracle has another goofy fiscal year that ends every May, thus the weird looking quarters in the chart below vs. what you’ll find when you open up the company’s press releases.

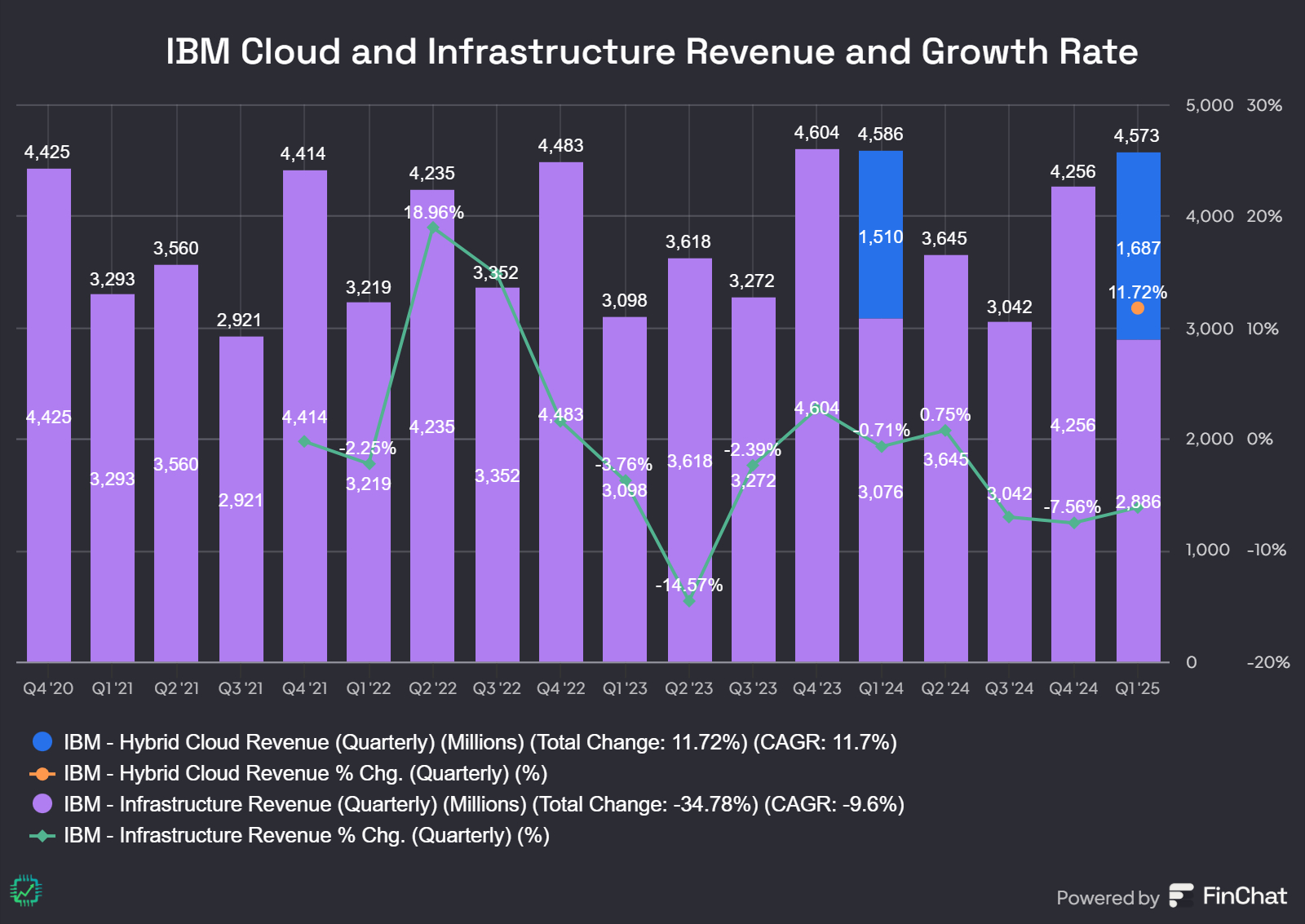

5. IBM (NYSE:IBM)

Yes, IBM, International Business Machines. A dinosaur of tech, parts of which have been resurrected in recent years after spinning off its old Kyndryl (KD) segment a couple years ago.

Actually, Kyndryl has been alright on its own. More proof corporate break-ups are the way to extend the lifespan of assets and maximize shareholder value. Creative destruction is totally a thing, and we shall make it known…

Anyways, IBM has begun, as of 2025, breaking out its “Hybrid Cloud” revenue so shareholders can get a clearer picture of what’s driving returns. Previously, Hybrid Cloud was mixed in with all sorts of other software and services at IBM (see the first chart showing IBM’s old comp to the other Big 5). Here we’ve presented you with the new “Hybrid Cloud” alongside the older “Infrastructure Revenue and Support” that’s still reported as a separate line item, the old on-premises business including mainframes. On a standalone basis, Hybrid Cloud grew nearly 12% YoY in Q1 2025.

Besides the above Big 5, there are also the neoclouds, which we feel are a totally different discussion. We have a small position in small biz cloud DigitalOcean (DOCN), considered CoreWeave (CRWV) during IPO but ultimately passed during the downturn (https://youtu.be/OcFsXMKzHBY), and have a tiny “experimental” position in Nebius (NBIS).