Before the recent Wall Street Journal article used the dreaded “b-word” (bankruptcy) in connection with silicon carbide (SiC) pure-play manufacturer Wolfspeed (WOLF), our Semi Insiders were given a write-up on the situation. In fact, we’ve been calling out issues at Wolfspeed for nearly two years now. In August 2024, though, serious warning signs began to flash. We made a video, “3 Small-Cap Chip Stocks to Avoid In 2024,” that didn’t sit well with some investors: 3 Small-Cap Chip Stocks to Avoid in 2024

Fast forward to today, and Wolfspeed’s new management team has indicated it could indeed be headed to bankruptcy court. What went wrong? And what was the process that led us to the call we made? What follows are the research notes – the story Wolfspeed’s balance sheet was telling – we provided to Semi Insiders last October as a follow-up to the original video we had posted in August. Here’s the video based on those October 2024 research notes: Chip Stock Disaster? Why Investors Need to Be Cautious With This Semiconductor Manufacturer (WOLF)

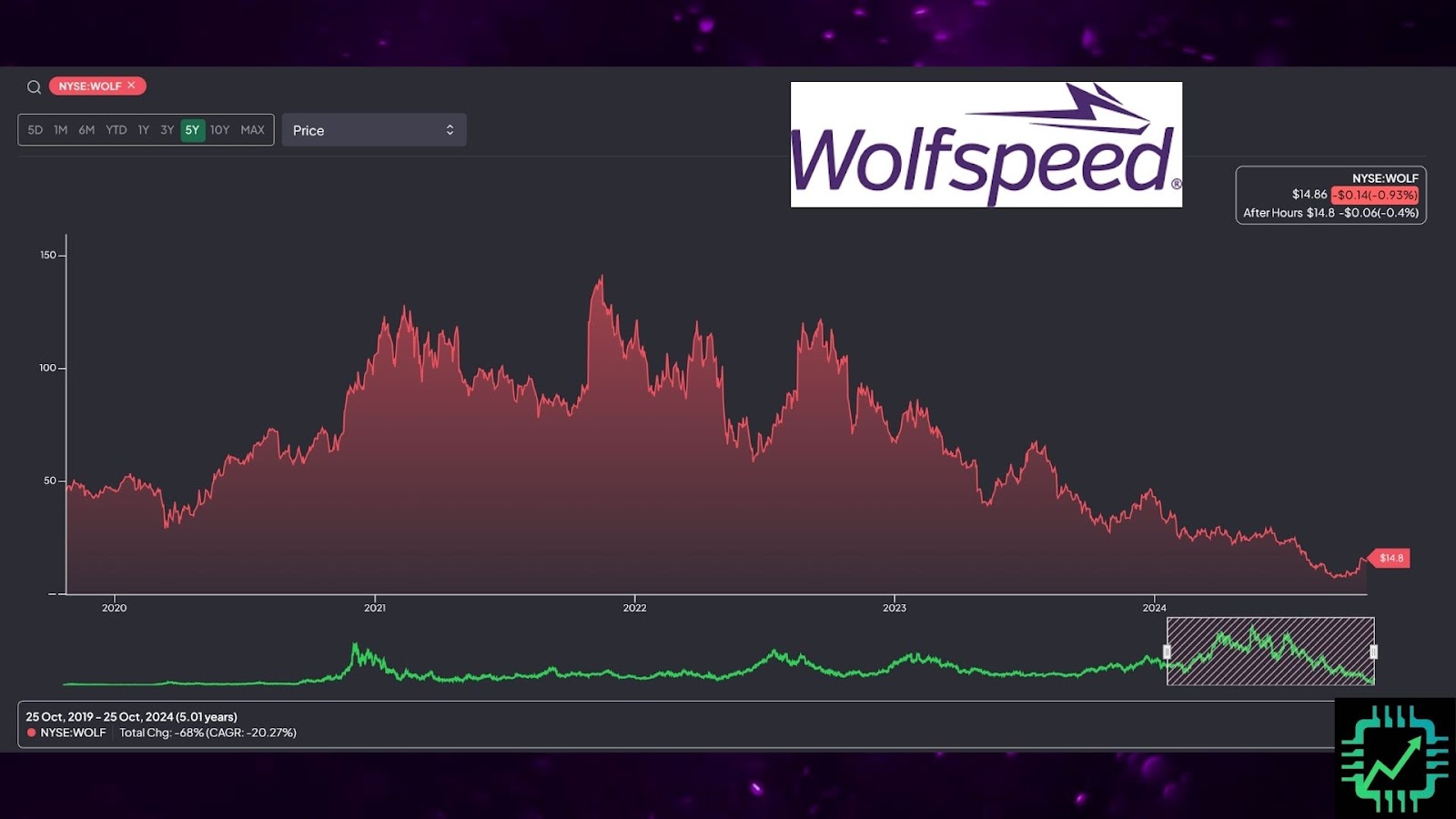

WOLF stock rallied in October 2024, are better times ahead?

We are fine with the fact that Wolfspeed has rebounded from the levels in late August when our last video/research notes were published, and even more so from the depressed stock price levels in September. But this is in no way an indication all is well.

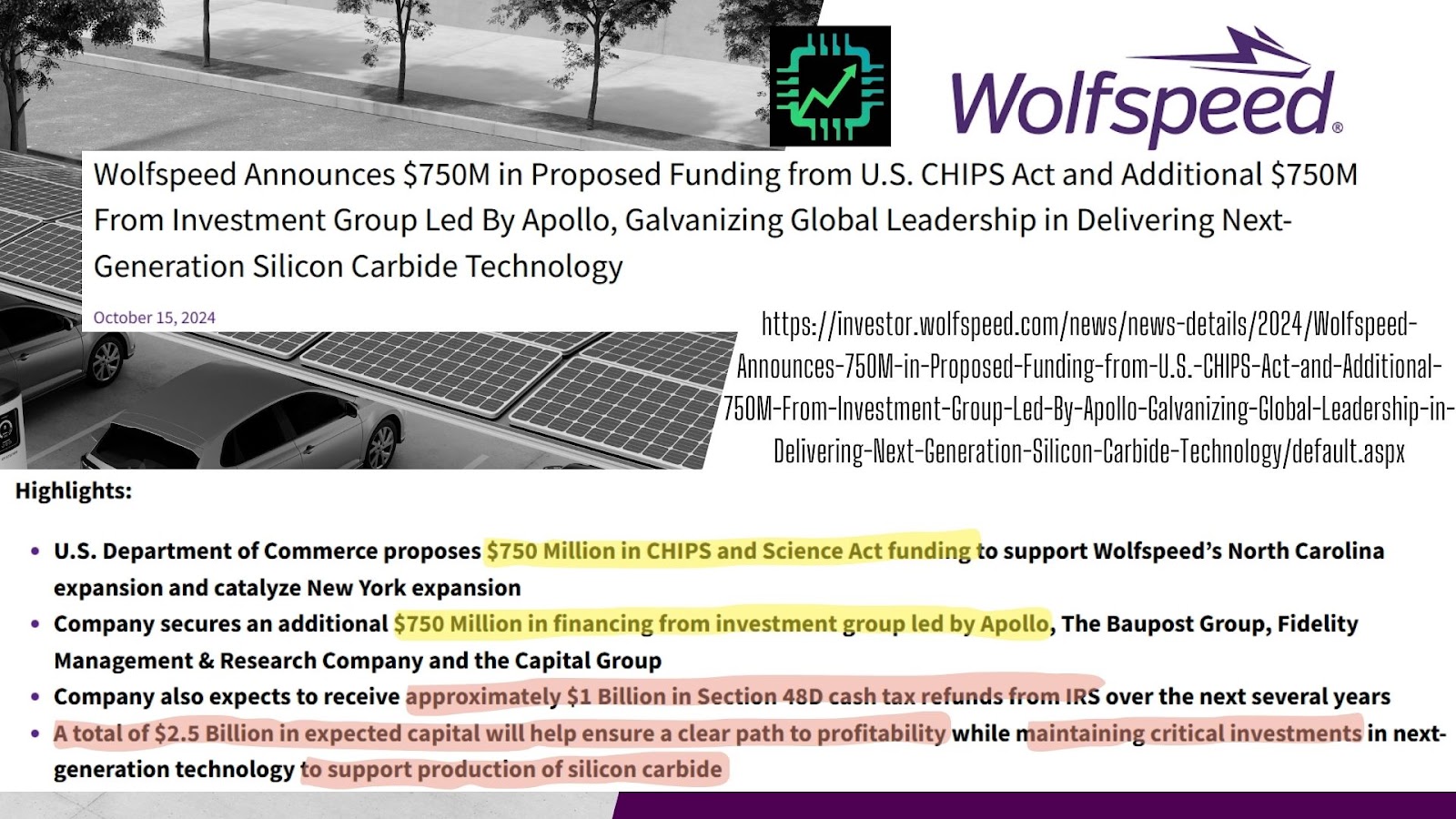

What happened to cause this recent rally? An uptick in auto and EV sales? Automaker interest in transitioning to more EV models? The Fed interest rate cut? No. U.S. CHIPS Act funding, as well as a new round of financing led by global asset manager Apollo Global (APO), is the reason for the breath of fresh air. Between the CHIPS Act award, new debt, and tax credits, Wolfspeed will get a cool $2.5 billion to complete its U.S.-based silicon carbide (SiC) fabs.

The CHIPS Act funding was awarded under the legislation’s “Rule 48D” for advanced semiconductor manufacturing. Among A LOT of other things, some startups have been inquiring as to whether space-based chip manufacturing is covered by Rule 48D. We’ll let you peruse the lengthy document yourself (plug it into an AI assistant for help, if you’d like) to find some juicy tidbits in the CHIPS Act.

Anyways, about the Wolfspeed funding needs

$750 million in direct funding from the CHIPS Act plus tax credits sounds like a great way to bolster a business. And indeed it is. But remember, Wolfspeed’s problem is it was very ambitious with its plans to build several brand new SiC chip fabs in the U.S. and Germany. These awards aren’t simply bolstering a business. Wolfspeed really needs the cash just to complete the projects it’s started!

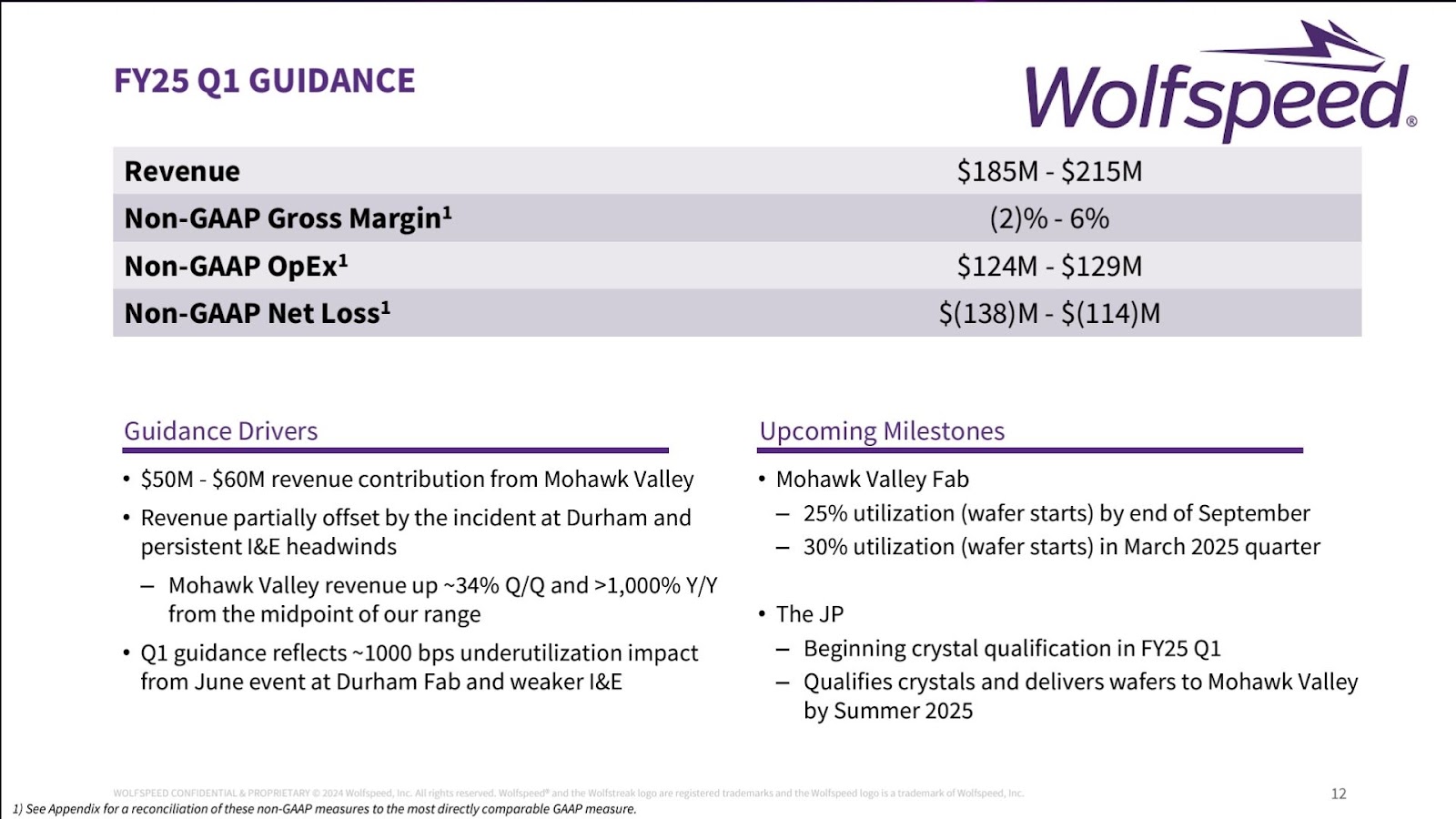

Case in point, look at the guidance for the Q1 fiscal 2025 quarter (which will be reported on November 6). Because much of Wolfspeed’s new facilities are still sitting idle (fab utilization guidance implies 25% to 30% of total fab capacity by summer 2025), Wolfspeed won’t just be operating at a loss. Its gross margin on products sold is expected to be an extremely meager mid-single-digit %. Yikes!

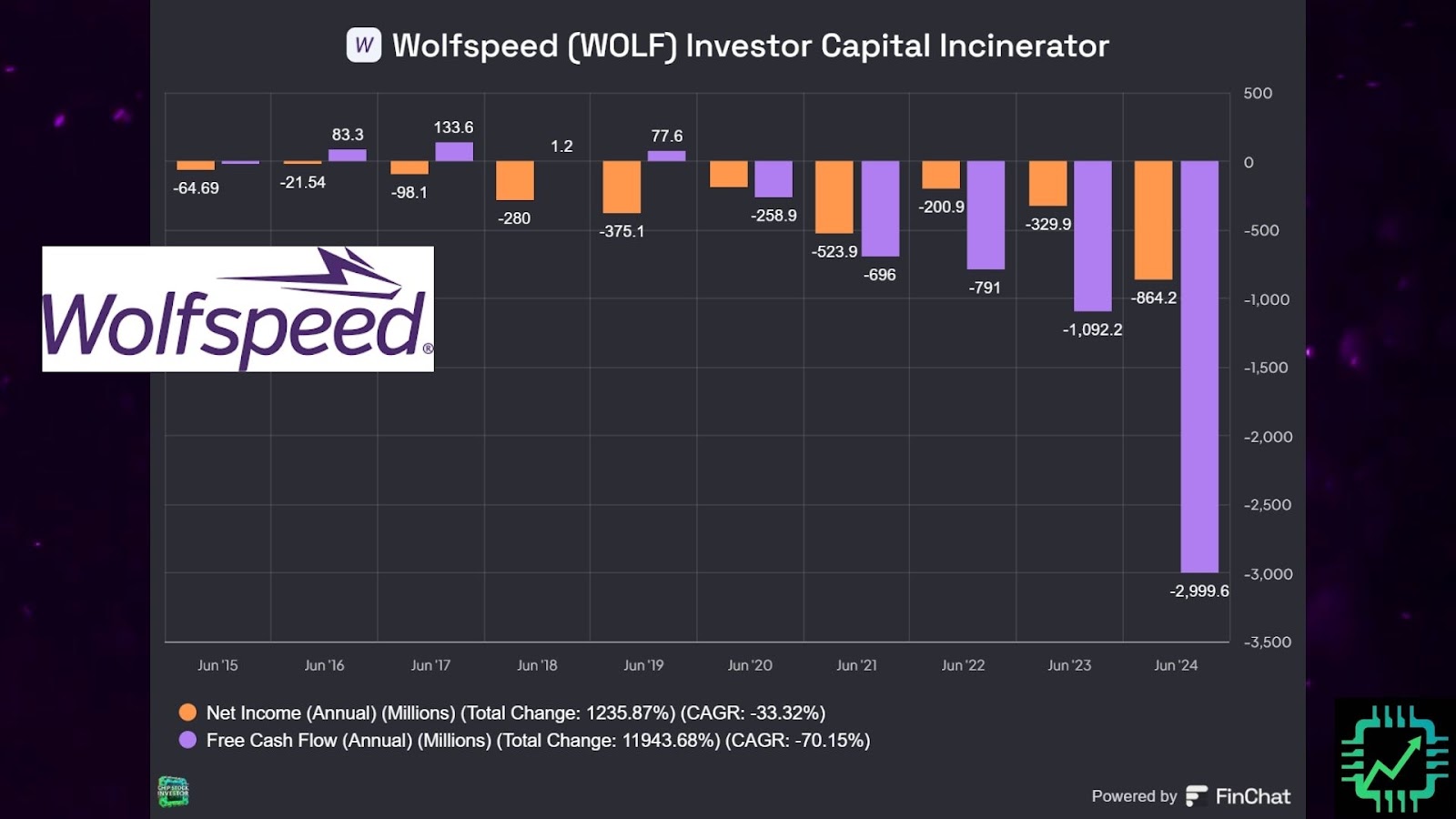

Debt is a patch-it fix until SiC revenue grows

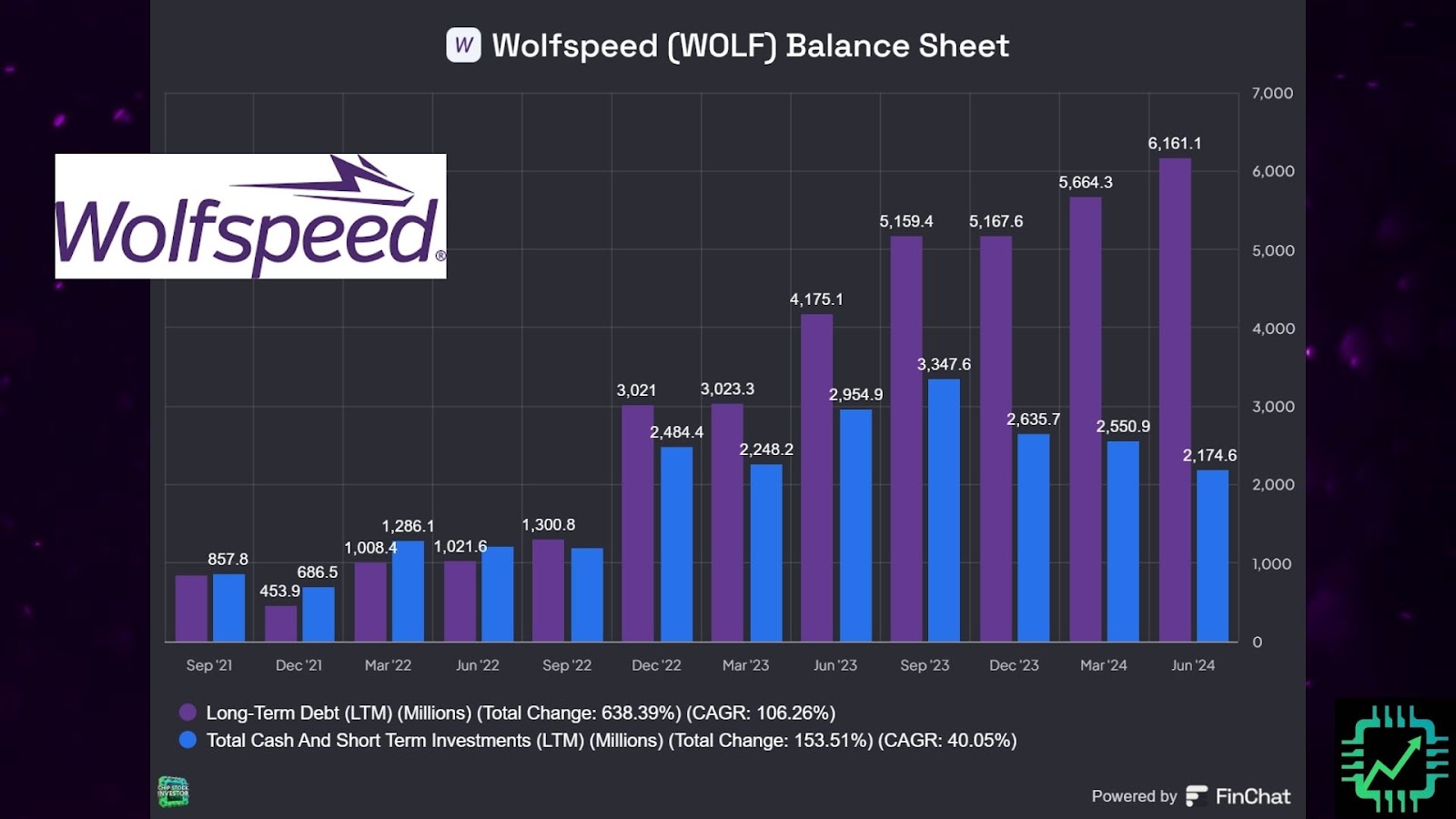

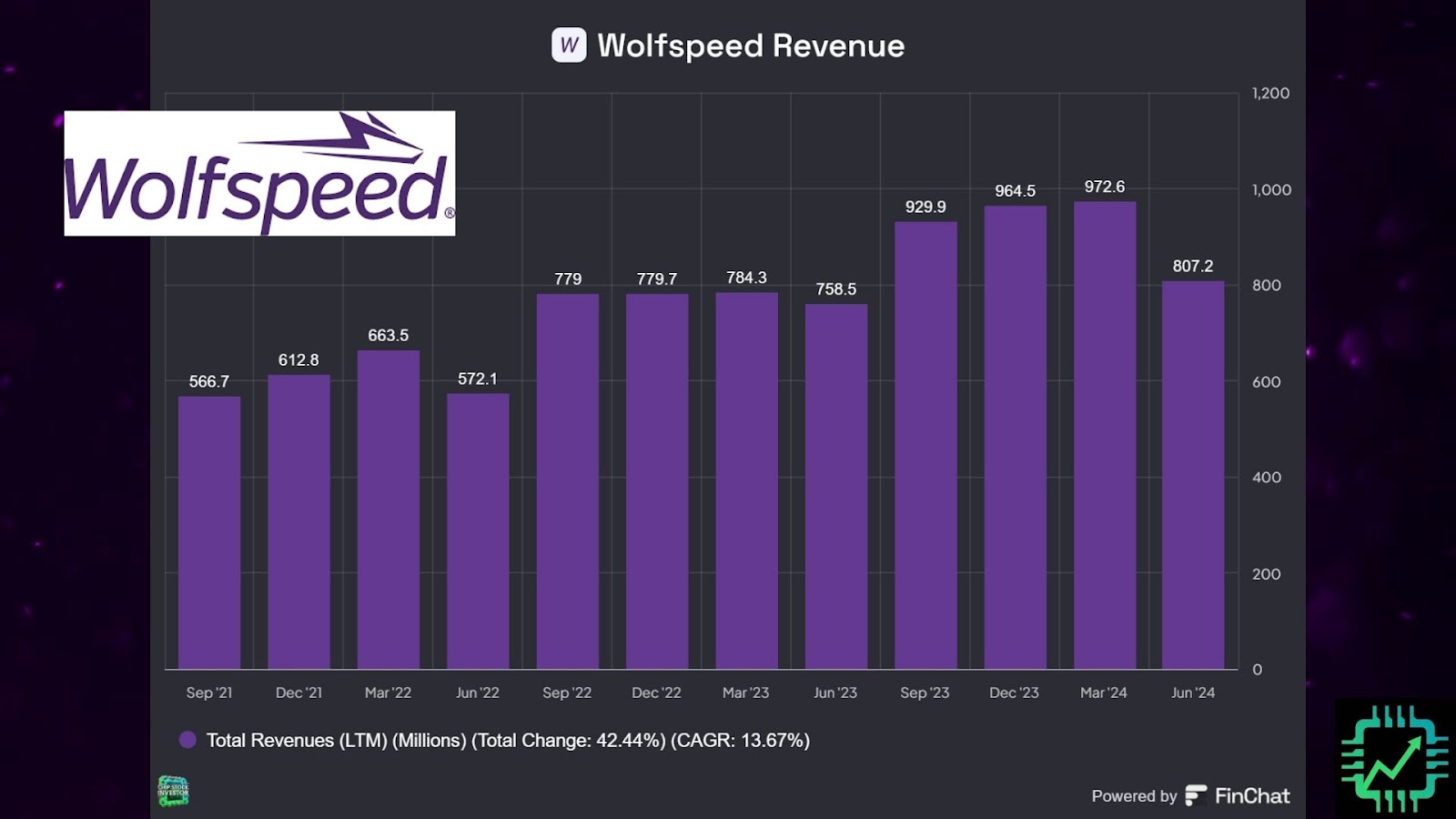

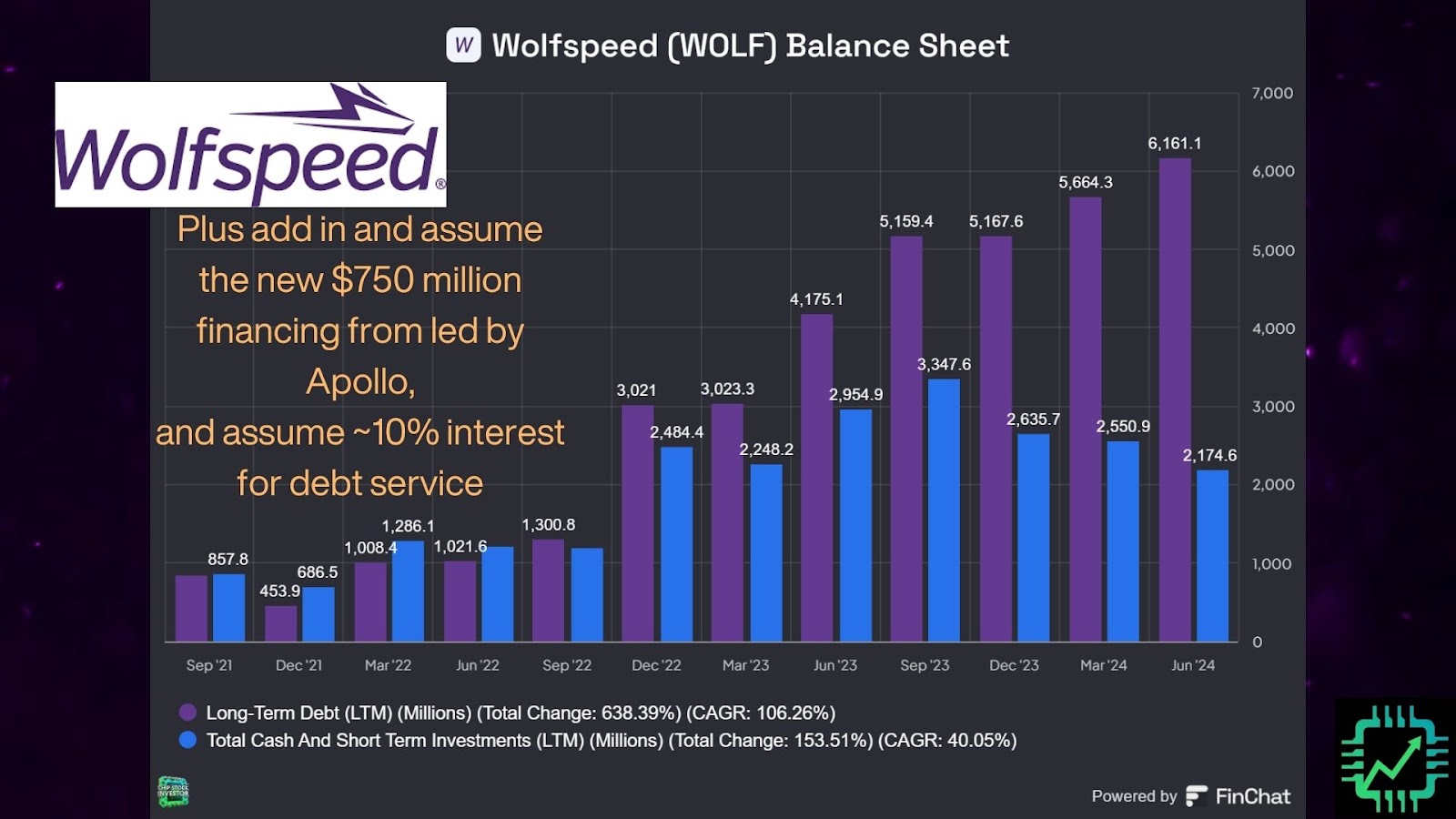

Really, this situation is just a continuation from the situation that has been in place the last couple of years. Since the auto and EV chip shortage turned into excess supply last year, Wolfspeed’s revenue has declined (hurting profitability), and ratcheting up the need to fund its fab expansion with debt. The balance sheet is now a mess.

Do note, total debt will be increasing even more because of the just-announced new $750 million debt funding round led by Apollo, shown in the slide earlier.

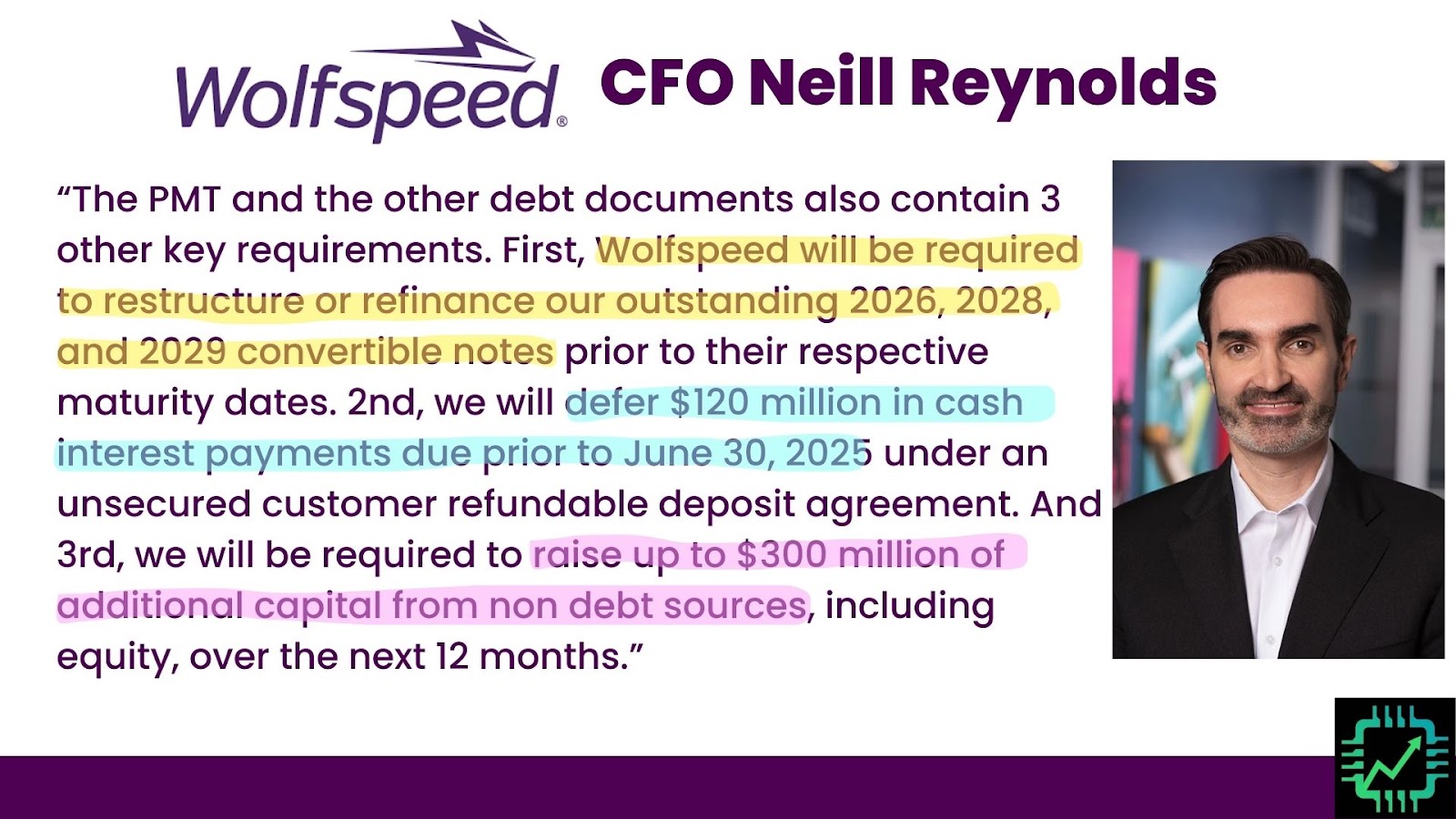

Now, the good news is Wolfspeed’s $2.5 billion in total capital from the CHIPS Act and the Apollo investor consortium does get Wolfspeed what it needs to finish U.S. expansion. And once these facilities are complete, they’ll support roughly $3 billion in total revenue (not a guarantee of $3 billion in revenue, but the U.S. fabs can support up to about $3 billion-worth of SiC product). That’s more than triple the amount of revenue Wolfspeed has been reporting. Company CFO Neill Reynolds explained on a recent call regarding the CHIPS Act and Apollo investment:

So what’s the problem? First, CHIPS Act money isn’t “free money.” There are strings attached, including the need to refinance part of the existing debt on the balance sheet. And of course, Apollo and its fellow investors want something in return for their cash. Reynolds explained in three parts:

What the Wolfspeed funding means for investors

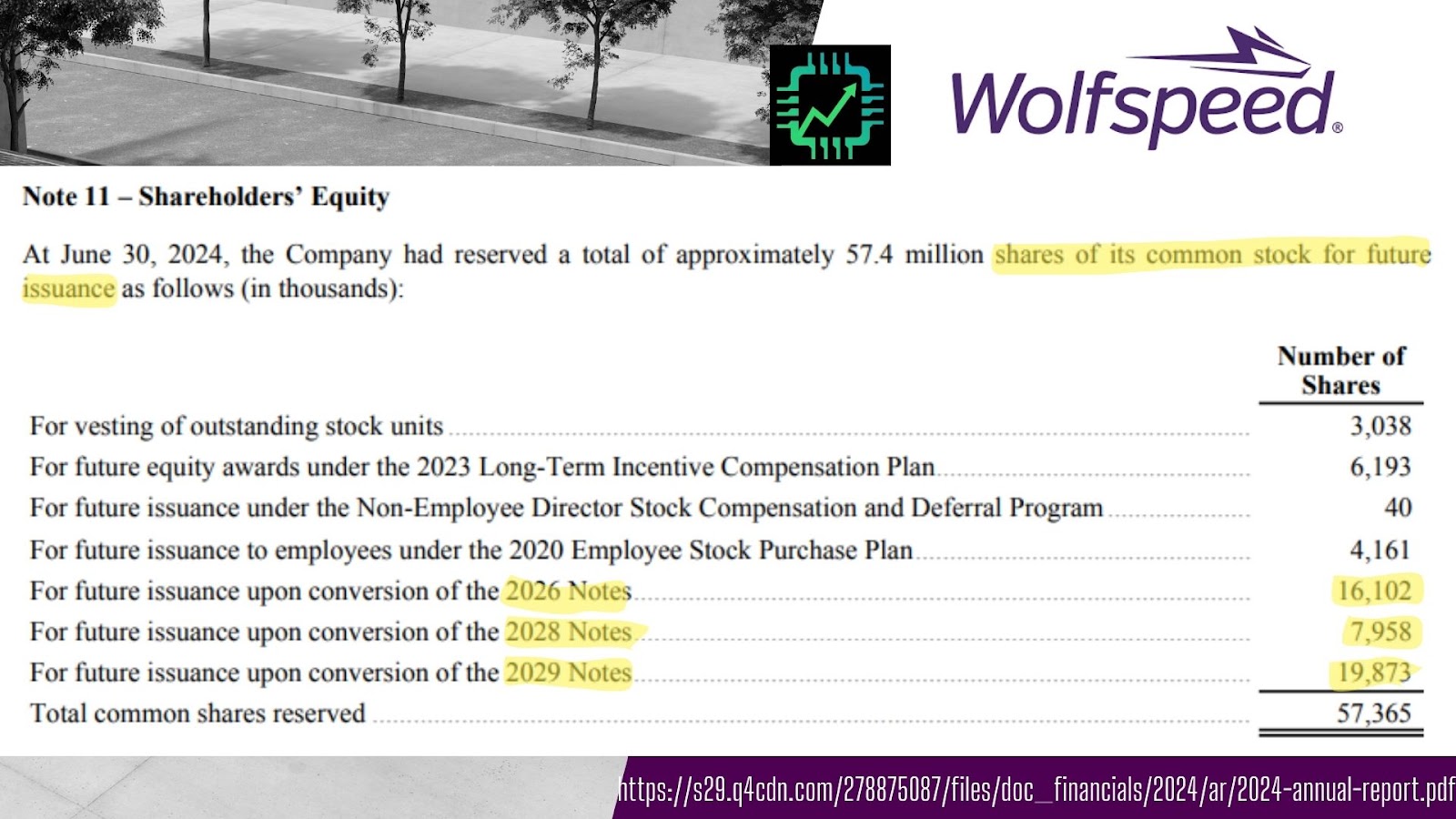

Let’s break down the above quote. Let’s start with point one, highlighted in yellow. About half of the company’s existing debt on balance (just over $3 billion) is debt that converts to WOLF stock in 2026, 2028, and 2029. That future dilutive event for shareholders (via issuance of new stock) is going away as that debt will be restructured, likely into new higher-interest-bearing debt.

However, the dilutive event isn’t going away entirely. As outlined in point three (the highlight in pink), Wolfspeed is being required to raise cash by issuing $300 million-worth of new stock within fiscal 2025 (which ends summer 2025).

And then point two (highlighted in blue), some other debt carrying ~$120 million in interest payments will also be restructured into new debt too.

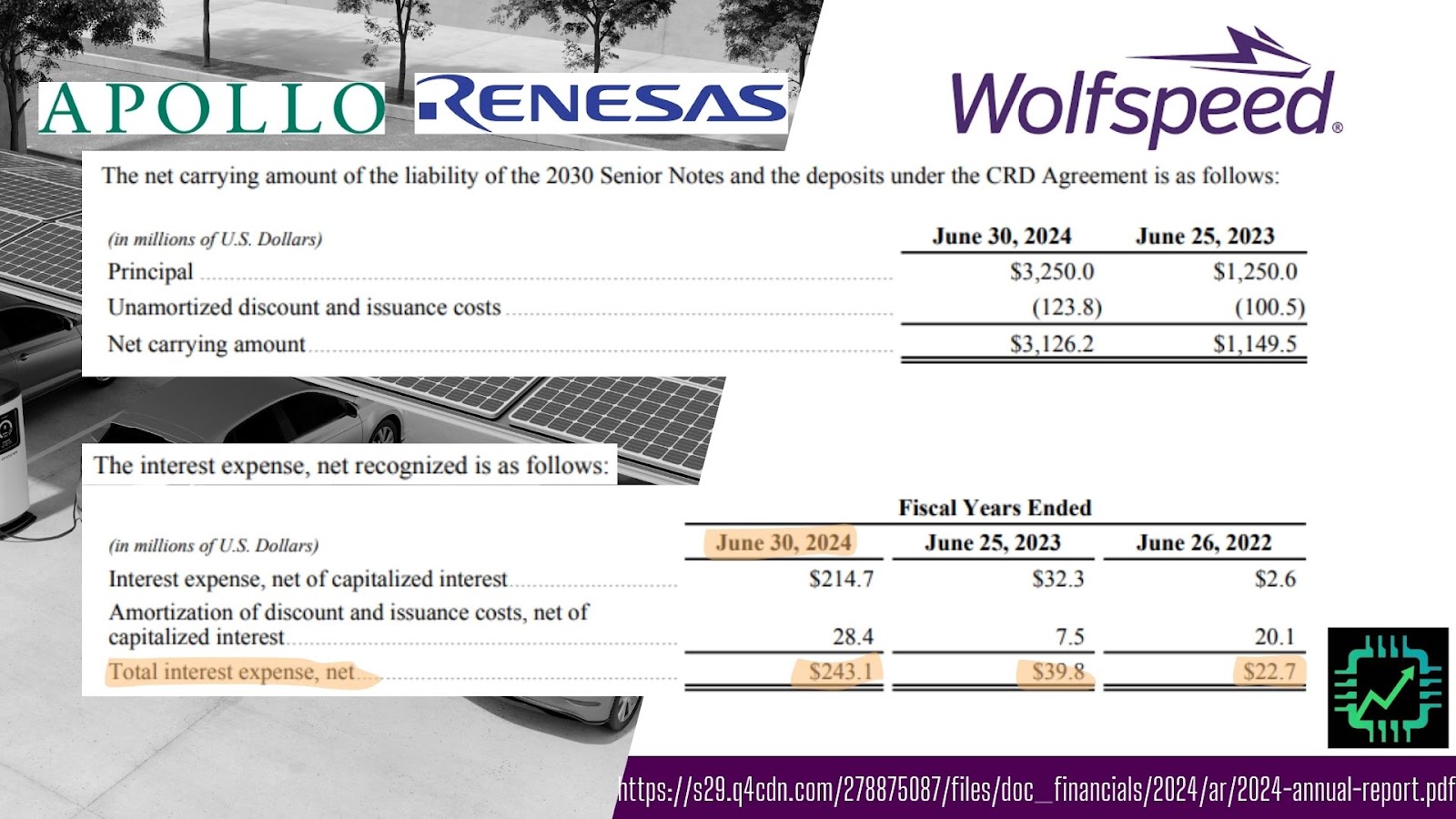

Now there’s the other half of the Wolfspeed’s existing debt on balance (also ~$3 billion), which is also owned by Apollo (announced in June 2023) and an advance deposit that carried an interest rate from Japan’s Renesas for future SiC wafer supply from Wolfspeed (announced July 2023). https://www.wolfspeed.com/company/news-events/news/wolfspeed-announces-1-25-billion-funded-secured-notes-led-by-apollo-credit-funds/ https://www.renesas.com/en/about/newsroom/renesas-and-wolfspeed-sign-10-year-silicon-carbide-wafer-supply-agreement

Notice the large increase in interest payments Wolfspeed had to make in the last year related to these two debt holders.

This, paired with the new debt funding from Apollo, seems to imply Wolfspeed’s interest payments are headed towards $300 million or more starting in fiscal 2025. This will be yet another drag on profitability for shareholders of WOLF stock, as the company is incinerating cash as it tries to complete its U.S. fabs and fill them with customer orders.

Chip Stock Investor is staying away from the WOLF of chip stocks

One final note on the balance sheet, which we’ll get an update on in early November: Much of Wolfspeed’s debt is going to carry an interest rate of 10% or higher. With new debt likely to be added, this is going to be a heavy burden for the SiC manufacturer to bear. Congrats, Apollo, you won this one. Owners of the stock took it on the chin.

There’s no foreseeable end to this situation, and in fact, Wolfspeed has yet to really address the promised SiC fab in Germany, which will also need funding. There are potentially year’s-worth of losses still in the forecast. And even should Wolfspeed eventually max out its U.S. fabs with $3 billion-worth of revenue, and manage a 20% operating margin ($600 million of operating profit), potentially half or more of that profit will be sent to investors like Apollo.

Suffice to say this makes Wolfspeed stock a no-go for us as long-term investors. If you’re looking for a swing trade or something similar, maybe your analysis is different. But for anyone looking for a long bet on SiC chips for autos, EVs, and other energy efficiency secular growth trends, it’s hard to imagine how Wolfspeed could adequately take care of its ordinary shareholders (owners of WOLF stock) for the next five years or so. Perhaps that will change, though. We’ll see.