Earlier in 2025, we allocated new money to a basket of “small bet potential big winner” stocks, which we discussed over on Semi Insider. One of those companies was Credo Technology Group (CRDO), which has since become a fairly well known emerging growth business — famous for its purple cables used in AI data center interconnects. What’s the big deal?

Hint: It has to do with helping customers reduce future power consumption, and break networking and memory “bottlenecks.”

What does Credo do?

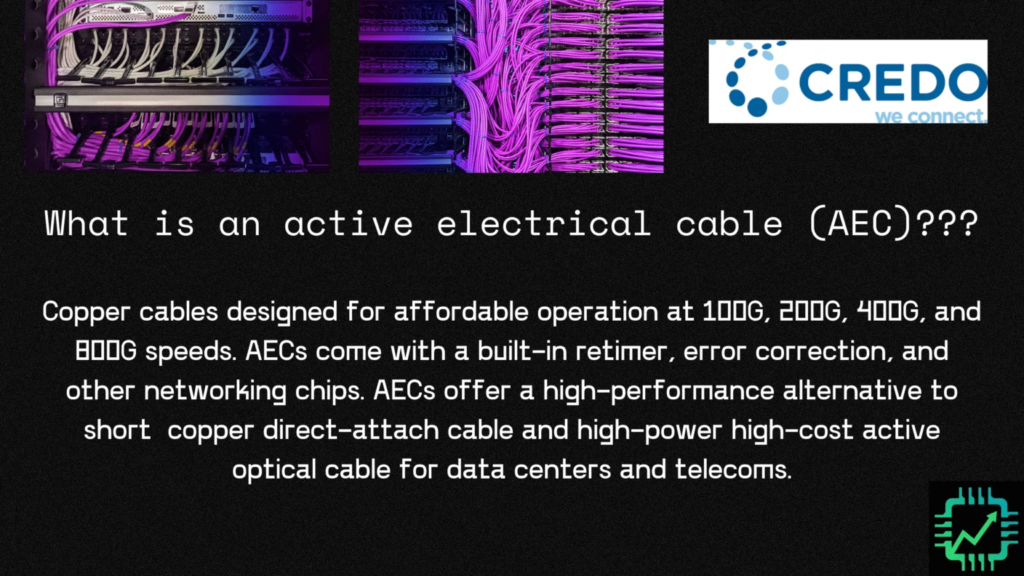

Credo, and Astera Labs (ALAB) too, are small fast-growing fabless chip designers competing in the data center networking and chip-to-chip interconnect market. It designs and sells the semiconductors that control active electrical cables (AECs), licenses IP to cable manufacturers, and has a few other products in development we will discuss shortly. With AI data center construction ongoing at a fast pace, Credo has gone from totally under-the-radar to “famous purple cable” status.

Let’s start with the biggest and most important product, the AEC, copper cables with high-performance networking chips (like a retimer) built into the plugs that can be a cost-effective replacement for more expensive optical cables.

1. Credo AECs still in hypergrowth

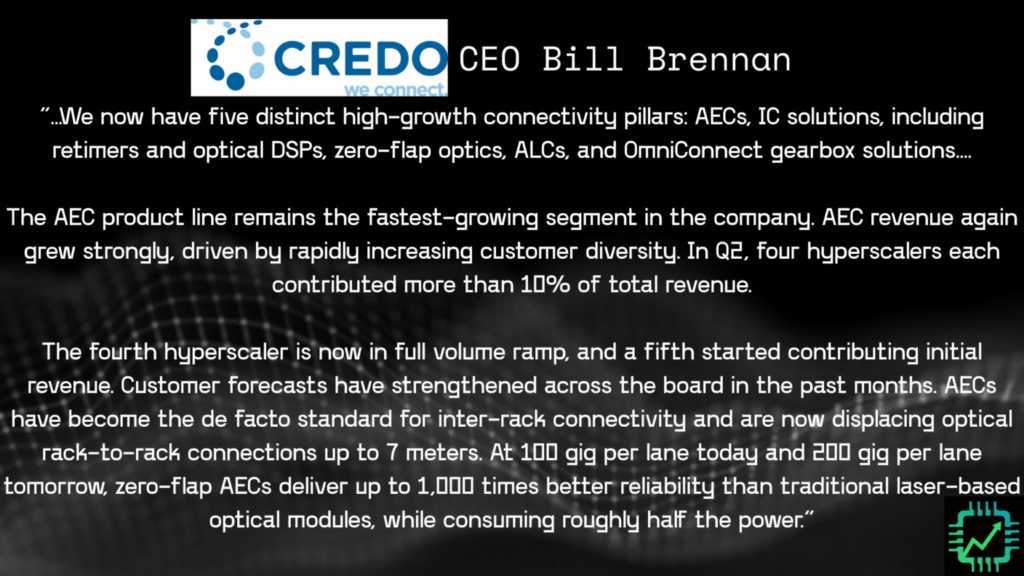

Let’s start with this quote from Credo CEO Bill Brennan on the last earnings call:

“…We now have five distinct high-growth connectivity pillars: AECs, IC solutions, including retimers and optical DSPs, zero-flap optics, ALCs, and OmniConnect gearbox solutions….

The AEC product line remains the fastest-growing segment in the company. AEC revenue again grew strongly, driven by rapidly increasing customer diversity. In Q2, four hyperscalers each contributed more than 10% of total revenue.

The fourth hyperscaler is now in full volume ramp, and a fifth started contributing initial revenue. Customer forecasts have strengthened across the board in the past months. AECs have become the de facto standard for inter-rack connectivity and are now displacing optical rack-to-rack connections up to 7 meters. At 100 gig per lane today and 200 gig per lane tomorrow, zero-flap AECs deliver up to 1,000 times better reliability than traditional laser-based optical modules, while consuming roughly half the power.”

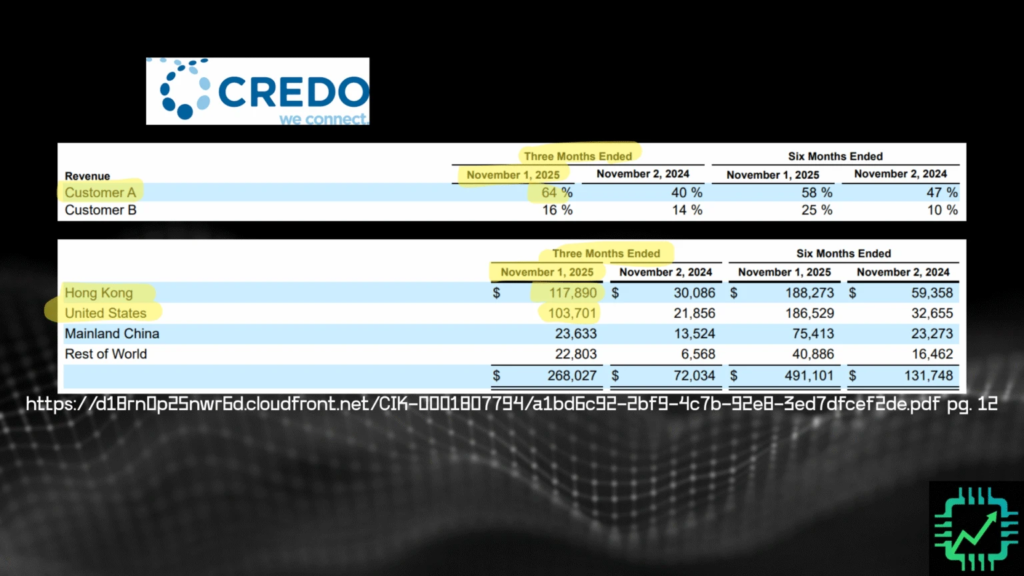

Revenue concentration among the hyperscalers can fluctuate from one quarter to the next, but it seems that the lead customer — believed to be Amazon AWS — is still the largest by far at 64% this last quarter. But good news, a fifth hyperscaler is now ramping up purchases too.

AEC purchases are still ramping up quickly. Note the revenue recognition broken up mostly between Hong Kong and the U.S., which is not indicative of the final location of install of the AEC or product, but rather the billing address for the customer, IP licensor, subcontracted cable assembler, etc. https://d18rn0p25nwr6d.cloudfront.net/CIK-0001807794/a1bd6c92-2bf9-4c7b-92e8-3ed7dfcef2de.pdf pg. 12

Nevertheless, revenue concentration and reliance on big tech is going to be the biggest risk for Credo long-term, in our estimation. See our write-up on how this played out last decade for mobile connectivity suppliers: Skyworks and Qorvo Merging, Supplier Customer Concentration Risks, and Investing Lessons

2. Development of active LED cables (ALCs)

Oh boy, more tech hardware acronyms.

Let’s talk about the ALC, which got some attention on the earnings call this quarter following the announced purchase of an engineering team calling itself Hyperlume back in September. Per CEO Brennan:

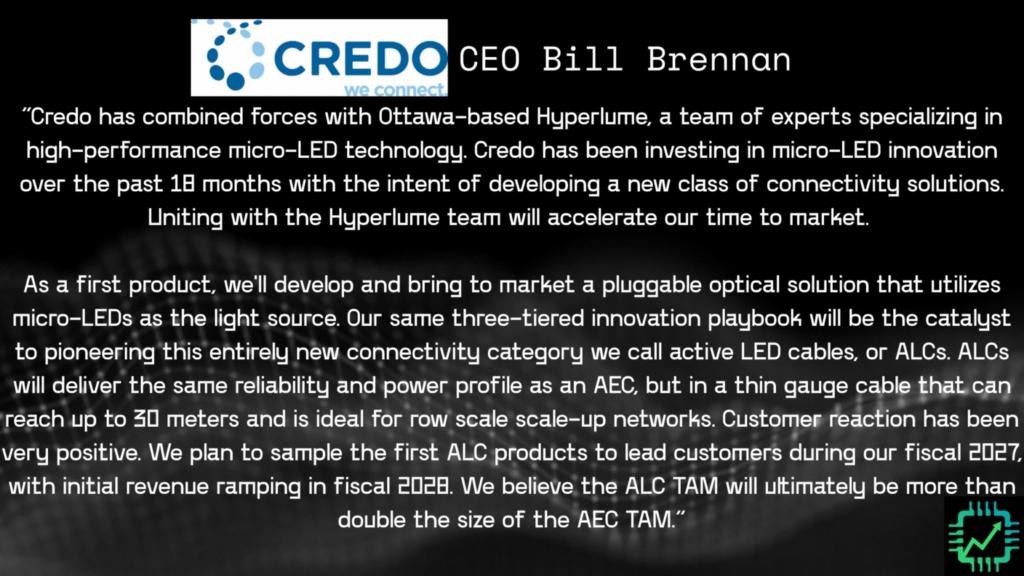

“Credo has combined forces with Ottawa-based Hyperlume, a team of experts specializing in high-performance micro-LED technology. Credo has been investing in micro-LED innovation over the past 18 months with the intent of developing a new class of connectivity solutions. Uniting with the Hyperlume team will accelerate our time to market.

As a first product, we’ll develop and bring to market a pluggable optical solution that utilizes micro-LEDs as the light source. Our same three-tiered innovation playbook will be the catalyst to pioneering this entirely new connectivity category we call active LED cables, or ALCs. ALCs will deliver the same reliability and power profile as an AEC, but in a thin gauge cable that can reach up to 30 meters and is ideal for row scale scale-up networks. Customer reaction has been very positive. We plan to sample the first ALC products to lead customers during our fiscal 2027, with initial revenue ramping in fiscal 2028. We believe the ALC TAM will ultimately be more than double the size of the AEC TAM.”

We’ve talked extensively about our belief that the AI data center “power bottleneck” is already being solved right now. Engineers are working on lower-power hardware that will help hyperscaler customers reduce ongoing utility operating expense, with power and performance savings equating to higher sales for the winning chip designer.

An LED (light-emitting diode, a semiconductor that emits light when powered on, as in the same underlying tech behind an LED light bulb) based optical cable, rather than using a power-hungry laser-based light source, could significantly reduce AI data center electricity needs.

The ALC could cannibalize Credo’s AEC product, as hinted at in the quote above. But given the longer range of an ALC (up to 30 meters), the addressable market of an ALC could go beyond just shorter range copper and potentially eat into optical market share too. Thus, Brennan’s mention that ALC TAM could ultimately be double the size of that of AECs.

Don’t expect any revenue from this product until fiscal 2028 (corresponding with second half calendar 2027 through first half calendar 2028). Until then, AECs and related chips like retimers will be Credo’s focus.

3. Breaking the AI data center memory bottleneck

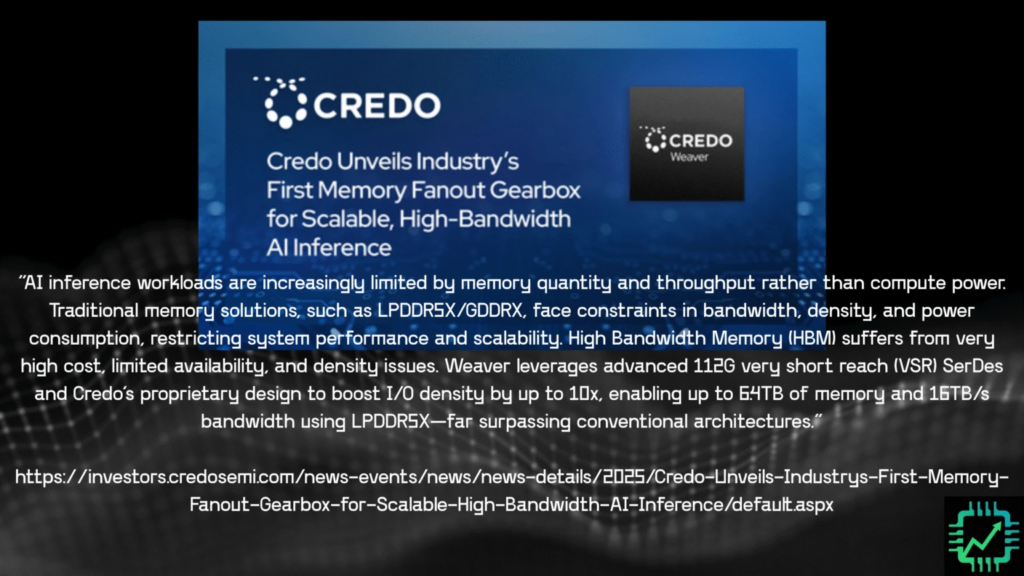

We’ve also discussed how the world’s engineers are also attacking the so-called AI data center “memory bottleneck.” Credo is on the hunt for a solution too. And it thinks it has one: the memory fanout gearbox, dubbed “OmniConnect” with the first product named Weaver.

CEO Brennan said Weaver was developed in tandem with its “lead customer,” and like ALCs, should start contributing revenue sometime in fiscal 2028. So, there’s going to be a lag for investors for this memory bottleneck breakthrough.

However, development is notable, given this addresses the high costs involved with HBM (high-bandwidth memory) in increasingly large scale-up and scale-out of custom accelerators (XPUs) among the hyperscalers. Brennan explained on the earnings call:

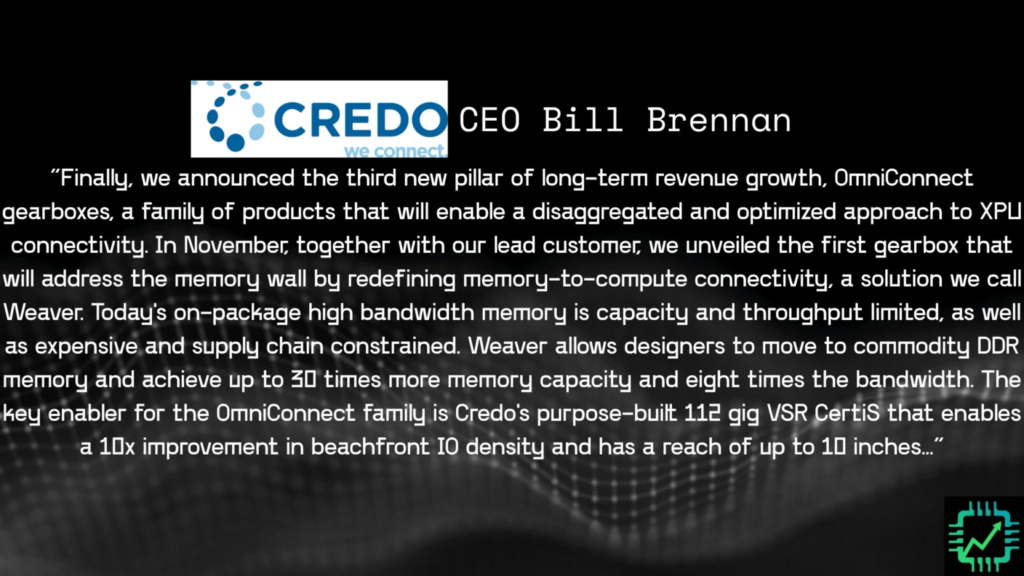

“Finally, we announced the third new pillar of long-term revenue growth, OmniConnect gearboxes, a family of products that will enable a disaggregated and optimized approach to XPU connectivity. In November, together with our lead customer, we unveiled the first gearbox that will address the memory wall by redefining memory-to-compute connectivity, a solution we call Weaver. Today’s on-package high bandwidth memory is capacity and throughput limited, as well as expensive and supply chain constrained. Weaver allows designers to move to commodity DDR memory and achieve up to 30 times more memory capacity and eight times the bandwidth. The key enabler for the OmniConnect family is Credo’s purpose-built 112 gig VSR CertiS that enables a 10x improvement in beachfront IO density and has a reach of up to 10 inches.

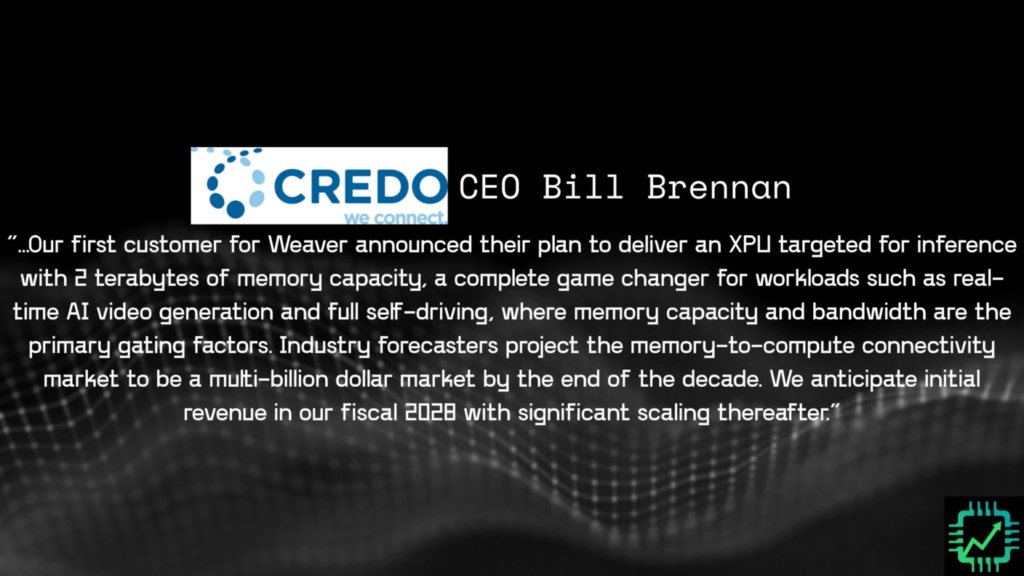

Our first customer for Weaver announced their plan to deliver an XPU targeted for inference with 2 terabytes of memory capacity, a complete game changer for workloads such as real-time AI video generation and full self-driving, where memory capacity and bandwidth are the primary gating factors. Industry forecasters project the memory-to-compute connectivity market to be a multi-billion dollar market by the end of the decade. We anticipate initial revenue in our fiscal 2028 with significant scaling thereafter.”

Remember when we said memory chips, even if they’re super cutting-edge to design and manufacture, are still ultimately a commodity product? Case in point above. All hardware parts and pieces are ultimately a commodity product, a simple input to building a final product. This is the source of most long-term pricing and margin pressure on semiconductor companies as they improve product performance and gain broader adoption, helping offset lower pricing on those products with the passage of time.

Enough of the tech, how about the earnings numbers?

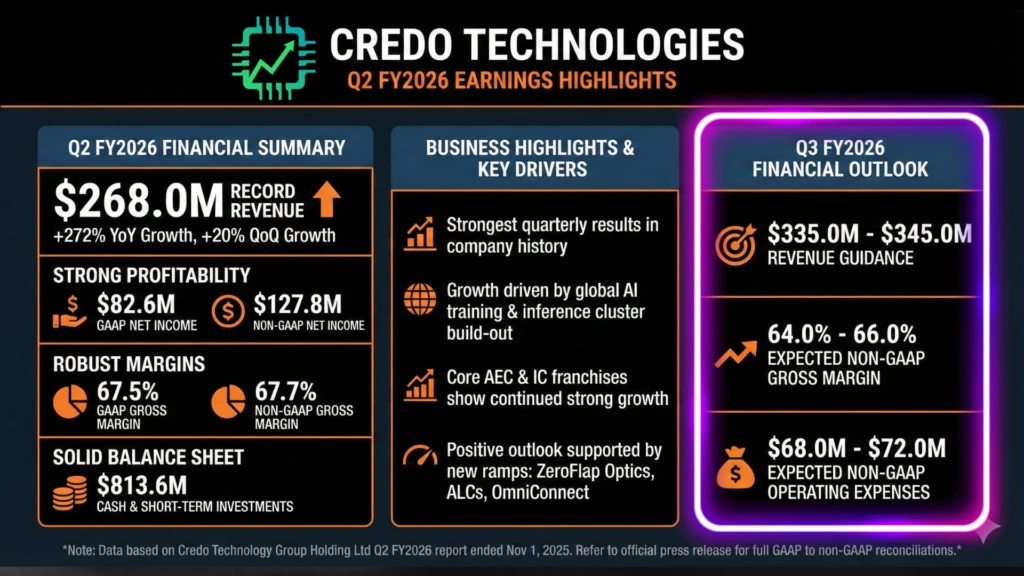

Hey, Nano Banana was behaving, so we got a Credo Q2 fiscal 2026 earnings slide out of it!

Revenue was up 272% year-over-year (YoY) to $268 million, and margins remained remarkably high as demand continues to be very strong for those famous purple AECs. Credo also finished the quarter with nearly $814 million in cash and equivalents, and no debt. Quite the war chest it can use to maximize its growth and reach against bigger diversified peers like Broadcom and Marvell.

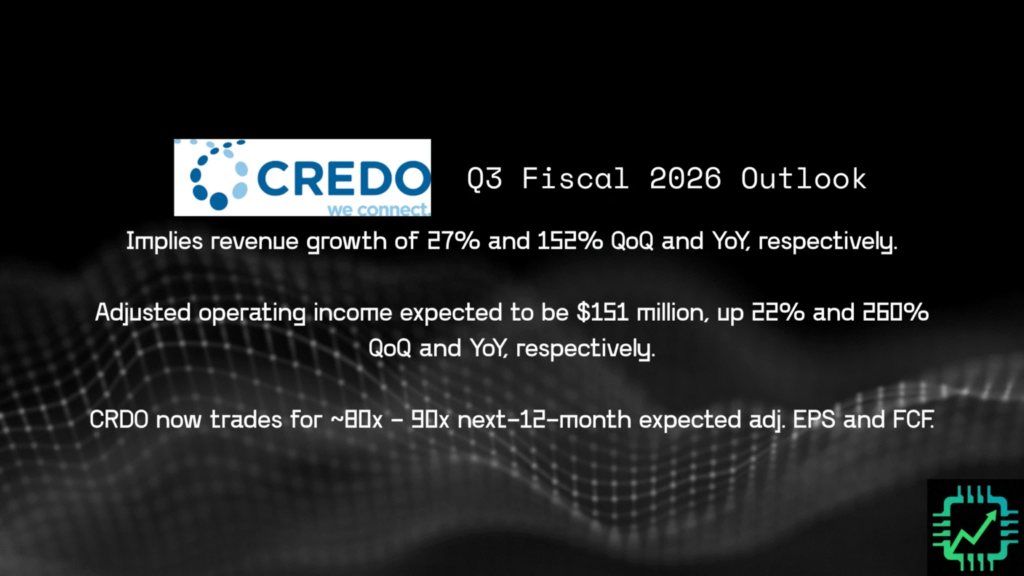

More importantly, though, was the guidance for Q3 (which will end in January 2026) sales of $340 million at the midpoint, with similarly high adjusted profit margins. And based on analyst estimates, Credo stock is now trading for about 80x to 90x both expected adjusted EPS and free cash flow. Whatever the estimate, though, it implies a belief Credo will continue growing its profitability at a triple-digit % in the next 12 months, with the high earnings multiple justified only if that high rate of growth continues for a few more years (like through fiscal 2028, when new products start ramping up).

Is that a good deal? Well it certainly isn’t a value. Credo is a momentum business, and the stock price will only keep rising from here if that momentum continues. But just for fun, we plugged in a reverse DCF scenario to see what kind of momentum we’re talking about through 2030.

- TTM FCF-per-share of $0.79

- Per-share profit growth of 60% for 5 years

- Terminal growth rate of 6%

- Discount rate of 10%

- = share price of ~$150

Given how quickly Credo is growing right now (free cash flow was nil last year), the above scenario implies triple-digit (perhaps 200% or more) FCF-per-share growth through next year, tapering off to about 30% or lower in 2030. And mind you, Credo already has a market cap of nearly $30 billion today. The company is going to need to expand significantly, and into more networking products and adjacent areas of the semiconductor market, to pull off this type of growth story.

Classic momentum stock. We have concerns about how well Credo can do long term. Which is why it’s still in our “prove it” basket of smaller bet portfolio positions. And we also treat it as part of a diversified portfolio allocation to networking and AI data center infrastructure, which of course includes our lead peer position in Broadcom (AVGO).

Interesting developments are being made, though, and Credo keeps delivering on its lofty outlook. We’re happy to stick with them and see how all this AI data center craziness pans out.

By the way, we’ve also completed our sub-industry deep dive and index on copper, optical, and related network chips in the fast-growing data center market. It’s available now on Semi Insider. See you there!