Over on Semi Insider this week, we’ve been discussing diversification and patience during earnings season. For investors with an overall buy-and-hold strategy, it might be tempting to sell when a stock price underperforms for many months, even years. It’s easy to let the emotion of seeing a depressed stock price find its way into a “my thesis is broken” analysis.

Some companies, especially those with a proven track record, need to be given time to let their strategy play out. Noisy earnings season and big stock price moves to the downside and upside can distract from that need to be patient.

Fortinet surprises to the upside — why it wasn’t really a surprise

Speaking of giving companies several years to work through pivots in their business model, let’s talk about Fortinet’s (FTNT) big “surprise” Q1 2026 earnings.

As we’ve discussed over the years, including a few months ago during the cybersecurity industry refresh, Fortinet is highly differentiated from its peers. And co-founder and CEO Ken Xie is fine with keeping his team’s head down and ignoring the Monday-morning-quarterback banter about whether the differentiated strategy will work or not.

While most of its large cybersecurity platform peers/competitors have gone the pure-software route (with reliance, to varying degrees, on cloud infrastructure and distribution), Fortinet still has a large presence in selling its own hardware (firewalls). In fact, it keeps winning market share in this area.

Yes, Fortinet also relies on cloud infrastructure too, most notably Alphabet Google Cloud. But Fortinet has been spending money to install its own converged networking-security, network traffic, and data storage servers within this global cloud footprint to improve its customer performance and meet their unique needs.

Image and data source: Chip Stock Investor.

A few years ago during the pandemic and post-pandemic software boom, Fortinet got dinged at times for not moving faster in software services. Then it got a hardware boom benefit. Then it got dinged again during the bear market of 2022-23, and dinged again in 2025 for not selling enough hardware during a customer refresh cycle.

And now, low and behold, investors are very pleased again with re-acceleration in hardware as customers are investing in Fortinet’s capabilities to secure their new AI workloads — even as the software service segment lags (reminder: there’s usually a year or two delay between initial product sale and then recurring service kicking in higher gear).

Image and data source: Chip Stock Investor.

It’s almost as if investors collectively don’t understand how Fortinet operates. Perhaps this is partially true. But this is more likely a case of the stock getting discounted when Xie and team announce a new round of business investment, and the the stock rewarding shareholders when it becomes clear the round of elevated investment is paying off.

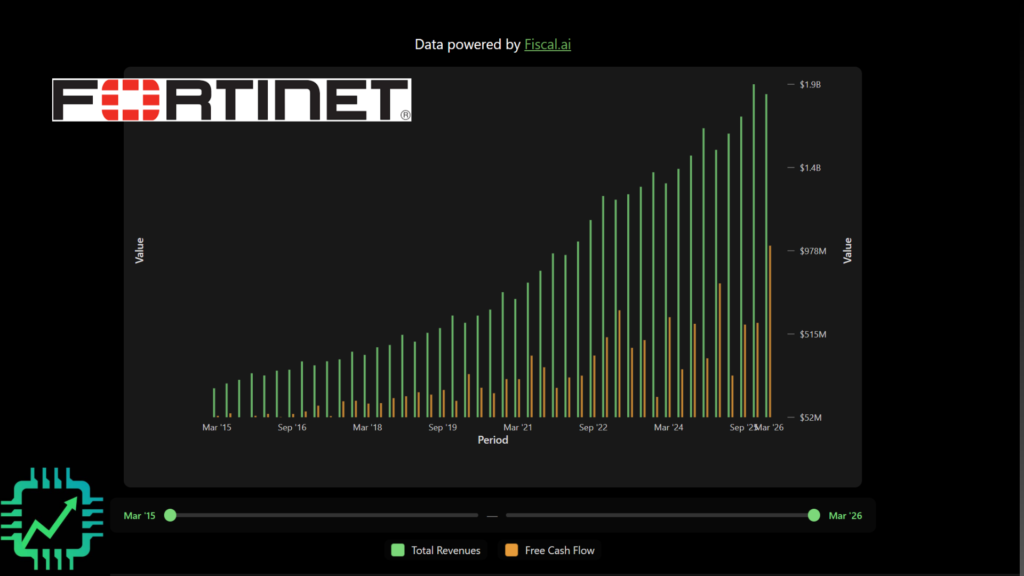

Though service revenue has become the larger chunk of revenue at about two-thirds of the total, Fortinet is very much a hardware-driven business. Which means there’s seasonality, cyclicality, and uncertain timing of cash flows. But as you can see below, the free cash flow surged in grand fashion in Q1 2026 to a nearly 55% margin.

Xie and team continue to execute, and offer investors a differentiated opportunity (truer diversification) from the other cybersecurity companies.

Image source: Chip Stock Investor. Data powered by Fiscal.ai.

The guidance was the key

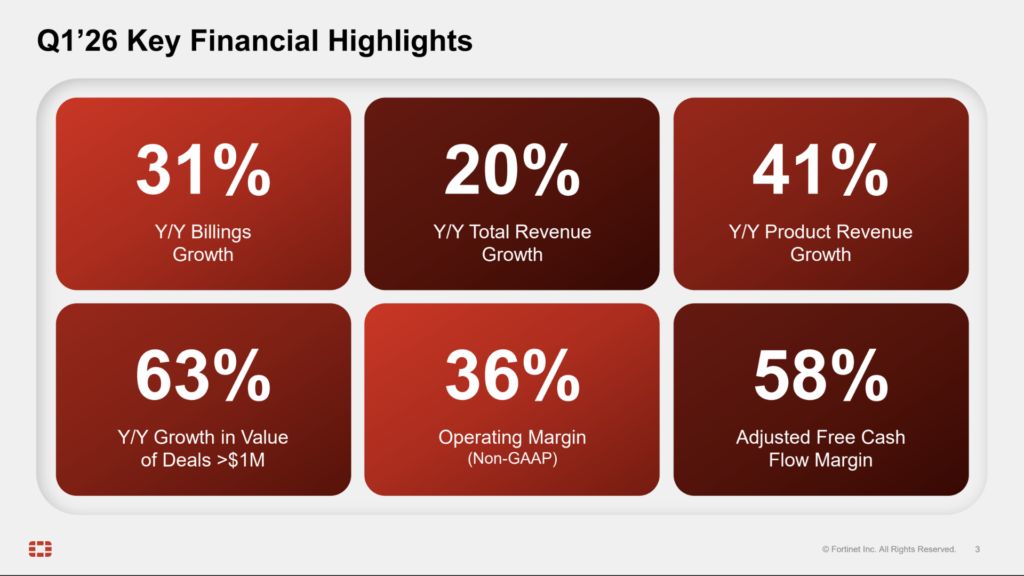

Product revenue (hardware and hardware-based sales) increased a whopping 41% year-over-year in Q1 2026 to $645 million. Revenue in total grew 20% to $1.85 billion. But note the customer billings increase of 31%. Customers are ramping up spend with Fortinet again, and new AI workload activity has been the key.

Image source: Fortinet.

Among other things, management cited its investment into its own cloud infrastructure as a standout. Certain customers with elevated risk controls (like “sovereign cloud”) are attracted to Fortinet’s ability to provide them a dedicated network to increase security posture.

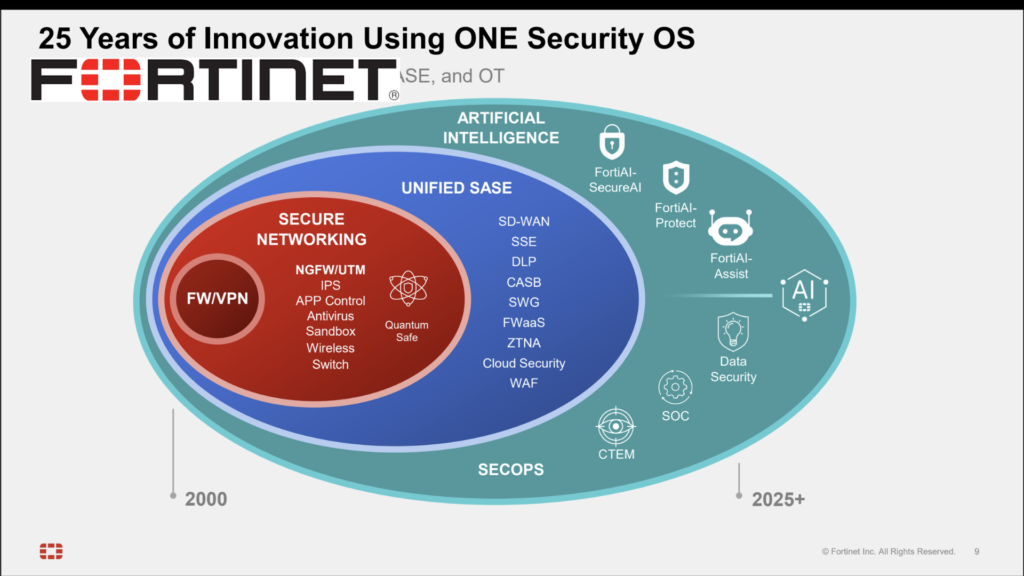

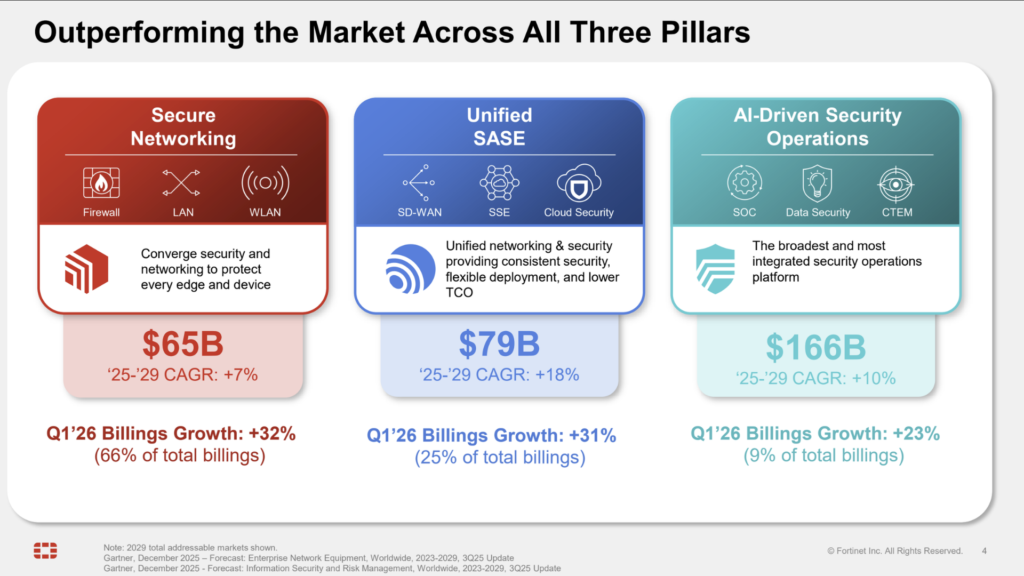

This should translate to higher recurring services, which remain stated as “accelerating by end of 2026.” But it all starts with the purchase and install of the new hardware (the red “kernels” in the slide below), and then expanding from there into Fortinet’s software services (blue outer kernels; SASE = secure access service edge).

Image source: Fortinet.

All of these addressable markets (colored kernels) are expanding. But note the customer billings are increasing fastest in the first red kernel. Investors are suddenly optimistic that the trickle-down into higher service growth is coming, starting in earnest late this year and into 2027.

Image source: Fortinet.

As a result, Fortinet raised its full-year 2026 guidance across all metrics. Billings should be in a range of $8.8 billion to $9.1 billion, implying midpoint growth of 18%. Total revenue is now in a range of $7.71 billion and $7.87 billion, implying midpoint growth of 15%. The lagging service revenue guidance range is from $5.09 billion to $5.15 billion, implying midpoint growth of 12%.

With hardware punching above its weight, there’s upside for that service segment revenue especially in 2027, to accelerate to a high-teens % or maybe even higher.

And yes, those profit margins. Here at CSI, we expect free cash flow profit to average out a bit from the seasonally elevated Q1, but still dial in at a best-in-class mid-30% range in 2026.

There’s a well documented reason why Fortinet stock was depressed last year and through Q1 this year. And well documented reason things are looking back up for the company. Differentiated businesses yield a differentiated return. And we’re quite happy with the outcome.

Chip Stock Investor is building a new Research Dashboard. Read all of our research articles, create your own research project, and get weekly live Q&A sessions with the CSI team. Join Semi Insider here!