Navitas (from Latin): zeal, energy, diligence

Gravitas (from Latin): dignity, seriousness, solemnity

A few weeks ago, we featured some of our research content regarding Monolithic Power Systems (MPWR), startup Navitas Semiconductor (NVTS), and their part in helping develop Nvidia’s (NVDA) high-voltage data center architecture that will begin deployment in 2027. Here’s the video link: Nvidia’s AI Data Center Power Infrastructure — New Growth For MPWR Stock and NVTS Stock

In particular, we’ve been critical of Navitas in the past. Here are the videos on the topic for reference (August 2023 and August 2024, excuse the quality please, we aren’t pro video creators): 2 EV Startup Stocks to Sell (NVTS & INDI), and 2 Big Semiconductor AI Stocks to Buy (MCHP & AMZN)? 3 Small-Cap Chip Stocks to Avoid in 2024

We stated a few weeks ago we were willing to keep an open mind on this hyped-up and retail investor favorite power chip stock – provided Navitas could prove the ability to deliver financial results. Did they deliver? Well… it’s time for some gravitas.

What does Navitas do again?

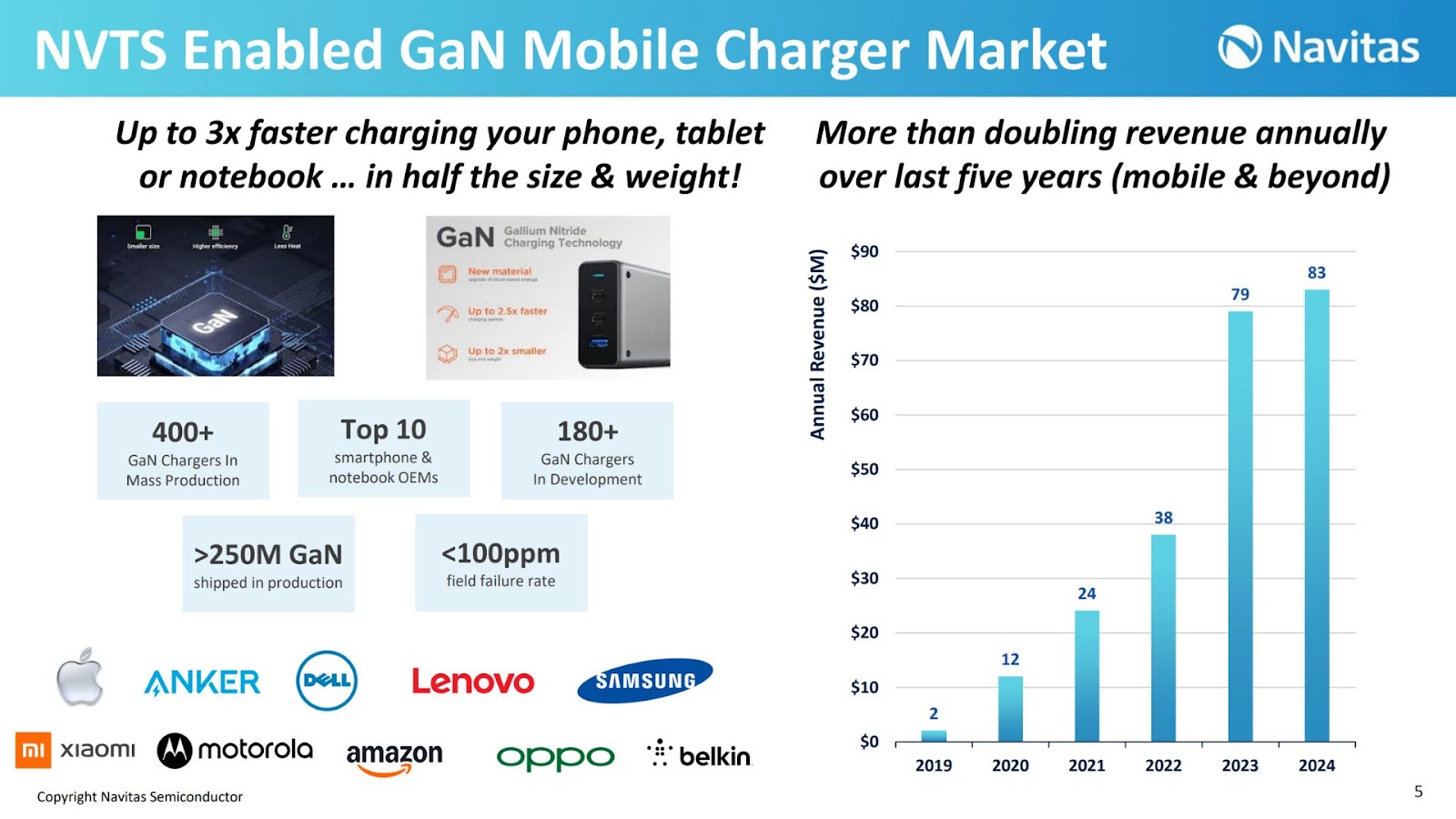

Navitas is a fabless (they develop patents and semiconductor devices, and outsource manufacturing of their designs) designer of power chips. Their targeted end markets skew towards consumer products. Originally, they were sampling power chips for smartphone and laptop chargers, and later they attempted to make some headway in electric vehicle charging.

Additionally, Navitas was name-dropped by Nvidia back in May, which we’ll get to in just a moment.

With a lot of these end markets in recovery mode after a couple year downturn, Navitas should theoretically be poised for a new run of massive growth.

What’s Nvidia got to do with it?

Nvidia data center systems, powering all things “AI” these days, draw a lot of power. As a result, Nvidia is early on in developing new power architecture for data centers (HVDC, or high-voltage data centers). Below is the press release in which Navitas was mentioned alongside some peers and other power infrastructure equipment providers. This was the press release that sent Navitas from left-for-dead startup to latest small-cap stock craze.

And here’s a link to our blog on the topic a few weeks ago: https://chipstockinvestor.com/monolithic-powers-fast-and-steady-growth-in-the-ai-data-center-era/

Navitas in particular is a “pure-play” developer of what’s known as “wide bandgap semiconductors” GaN (gallium nitride) and SiC (silicon carbide). Wide bandgap-based devices can operate at higher voltages than traditional silicon (Si), and hold the promise of greater power efficiency as well. Below is a chart showing some of the applications for wide bandgap devices from Navitas competitor Infineon. https://www.infineon.com/technology/wide-bandgap-semiconductors-sic-gan

Navitas further organized Nvidia’s list of HVDC co-developers and suppliers as follows, with grid and data center infrastructure providers on the left, data center power equipment in the middle, and then “AI chip” companies on the right.

Where does Navitas fit into the equation? Power chips play a critical role in any computing system, managing the “flow” of electricity by converting and splitting the power so that only the right amount reaches the computing system component (like the GPU chip, for example). With power and voltages headed higher in new data centers, there will be a need for new wide bandgap devices to help with the infrastructure build.

The narrative sounds good, but…

As we discussed last month, Nvidia’s HVDC architecture won’t begin initial customer buildouts until 2027. In the meantime, Navitas will need to pay the bills in other ways. Props to them for pointing this out in their August 2025 investor presentation.

Note the expected total addressable market for HVDC power chips will be a mere $164 million in 2027. It only reaches a $1 billion market by 2029. And bear in mind, Navitas may be a wide bandgap designer pure-play, but it’s hardly the only co-developer of power chips for Nvidia. In other words, even if the addressable market size predictions are true, Navitas can only grab a piece of the pie. And that speaks nothing to any potential profit available for Navitas.

So where does that leave Navitas in the meantime? Primarily pulling in revenue from its very small smartphone/laptop charging chips, and a bit from EV charging and solar infrastructure. Over the last few years, Navitas has talked up each of these initiatives as the next big thing. Revenue of $83 million in 2024 misses that “next big thing” mark.

Now management is re-prioritizing once more for Nvidia HVDC, and it’s clear that failed past mass-commercialization initiatives are winding down from customer sampling and testing. Navitas’ quarterly revenue remains in year-over-year decline in Q2 2025, and operating losses continue.

If you want to make great financial visuals like the ones above, check out our blog sponsor Fiscal.ai. Visit our special link to get 15% off any paid plan! Fiscal.ai/csi

For a (mostly) pre-revenue publicly traded startup company like Navitas, we compare their situation to a race against the clock. The time left on the “clock” in this case is cash on the balance sheet. With revenue minimal and losses draining that cash on balance, Navitas will need to bridge the gap between now and 2027. It did so last quarter by issuing and selling more NVTS shares onto the market (dilution of any future profit for existing shareholders).

Nevertheless, the new cash infusion does get Navitas enough liquidity to perhaps last it until 2027 when the HVDC rollout begins. But what then? After all, Navitas continues to expect meager revenue and ongoing losses. Here’s the Q3 2025 guidance:

All of this is to say the hype around Navitas since May 2025 that sent it back to a market approaching $2 billion at times served to help management raise the cash it needed for the next couple of years. None of it has done much to help any hopeful shareholders in the immediate term.

Suffice to say we’ll keep an open mind. But there remains no clear path towards sustainable financial returns that can keep Navitas Semiconductor stock rising higher – at least not anytime soon.

We have more research on this and lots of other topics. Join us over on Semiconductor Insider for the full discussion! chipstockinvestor.com/membership

One Response

Great piece! Thanks for the level-headed clarity.