The following is taken from a Semi Insider on July 5, 2025. And yes, we understand Entegris (ENTG) stock is up ~10% since then. But we still find the research valid. The market is running hot, so we’re looking for businesses that still need to prove their financials are solid before taking flight.

In the grand scheme of things, though, ENTG stock has been beaten up quite a bit over the last five years. But this is actually a great long-term growth compounder. We’ll discuss everything that has happened, and why the seemingly high valuations in the slide below might now be as “premium” as they appear (remember, a lot of cyclical companies always appear “expensive”).

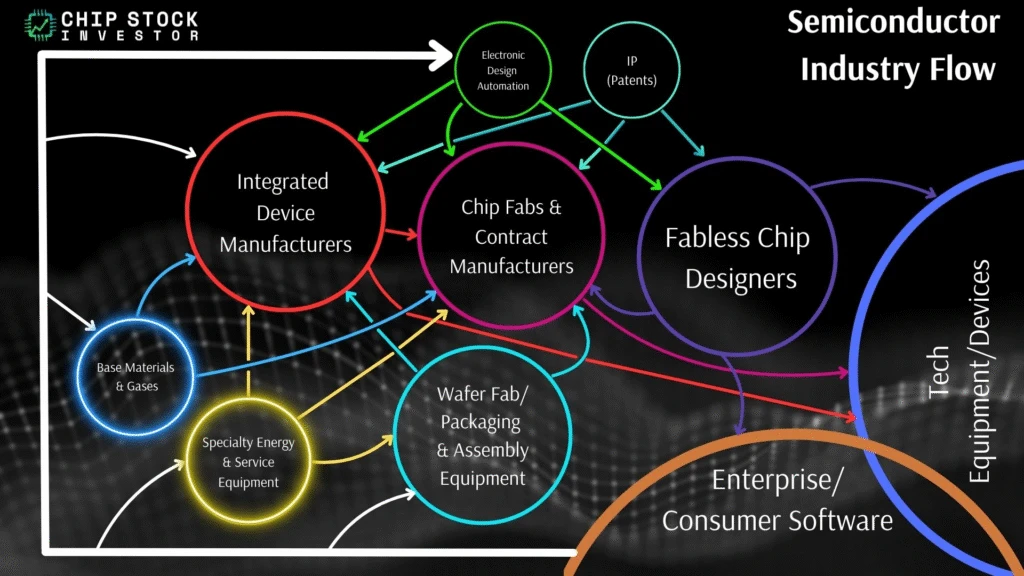

Where Entegris fits in the semi supply chain

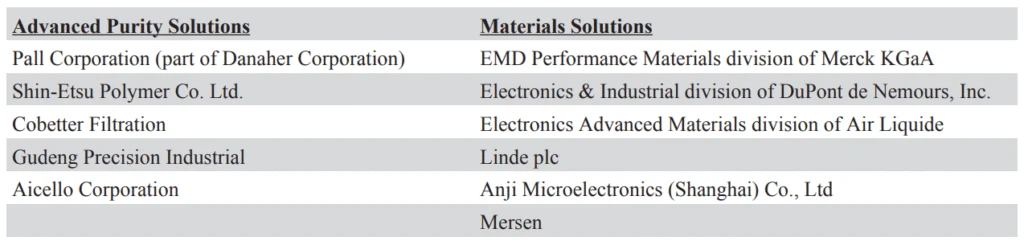

We’ll be visiting a spot on the semiconductor supply chain we haven’t discussed in quite some time: “Base materials and gases” as well as “specialty equipment and fab services.” Entegris does a bit of both. Besides Linde (LIN), Air Products and Chemicals (APD), and Air Liquide (PA:AI), we’ve also taken a snapshot of who Entegris says its top competitors are. We’ll come back to what these specific business segments are momentarily.

In short, Entegris provides “consumable” chemicals and related services and equipment needed in a semiconductor manufacturing facility (a chip fab). Given they provide ongoing consumable materials, the Entegris sales cycle is very fast and very sensitive to semiconductor end-market demand.

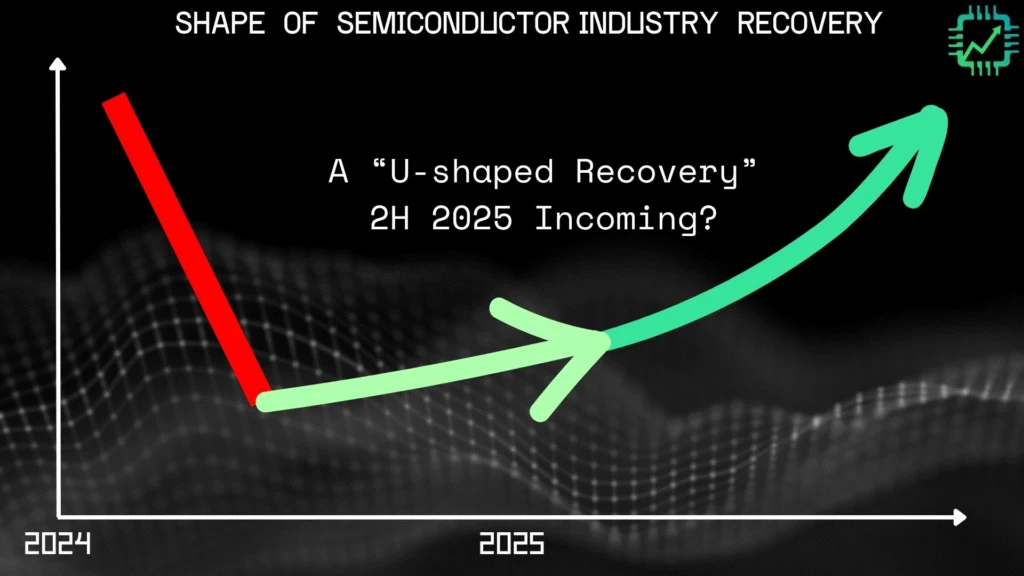

If a fab slows production, Entegris investors would be one of the first to feel it. And likewise, if the manufacturing cycle is about to heat up the second half of 2025, Entegris sales could also return to robust growth as fab chemical and consumable product inventories quickly get reduced. See our other recent updates (really, all of the industry updates for much of this year) for more info on why the manufacturing market is headed for better times the back half of 2025 and into 2026.

What does Entegris actually do?

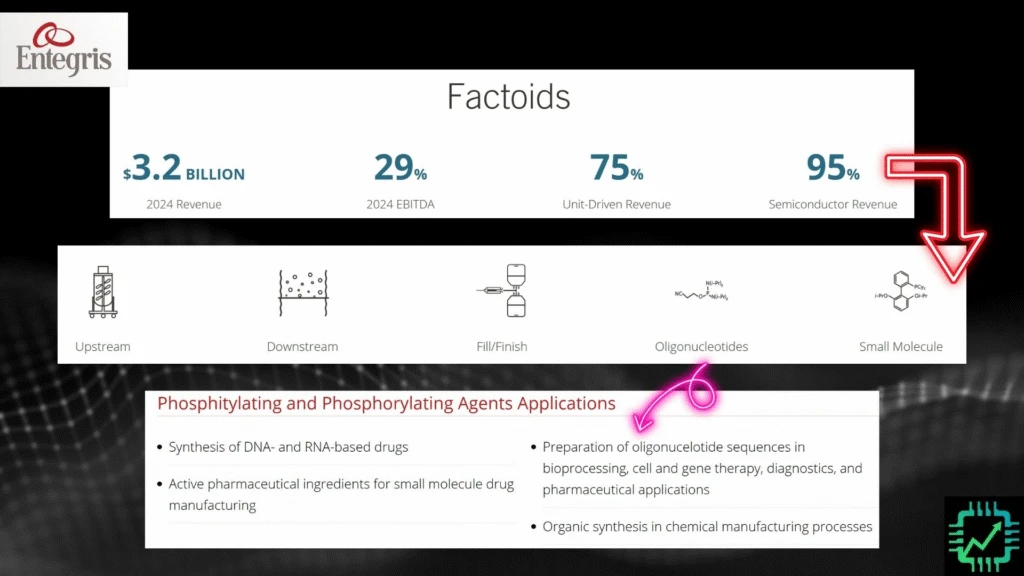

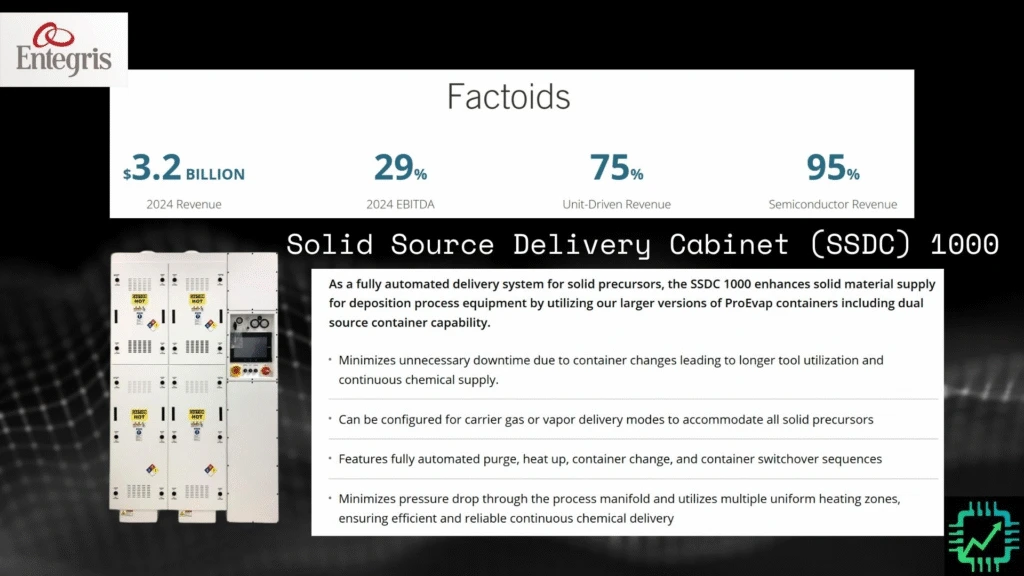

In the slide below are a few high-level factoids about the company. Besides being a mostly semiconductor chemicals and fab product pure-play, there is the 5% of the 2024 company sales to life science labs engaged in R&D (arrows pointing to the “other 5%” journey). We decided not to go too far down the rabbit hole. Just know that you get a small little biotech chemicals bonus with Entegris. Here’s the starter link if falling into that rabbit hole interests you — including one to what “oligonucleotides” are. https://lifesciences.entegris.com/ https://lifesciences.entegris.com/en/home/our-science/by-industry/bioprocessing/oligonucleotides.html

Alrighty then, what about the 95% of 2024 sales? Much of it are advanced materials, chemicals, chemical and gas purification and delivery systems, and wafer and chip shipping containers and products, specific to the semiconductor industry. Entegris provides an expanded list of all their products and services on page 7 of the annual report pdf here (pg. 2 of Part 1, “Business”). https://s205.q4cdn.com/144974603/files/doc_financials/2024/ar/088c4ed0-285c-4f60-9a57-3ebf7e1eee60.pdf

Here are a few examples: The SSDC 1000, a chemical delivery system that manages the output of gases from specialty gas tanks, used in various steps of developing a silicon wafer.

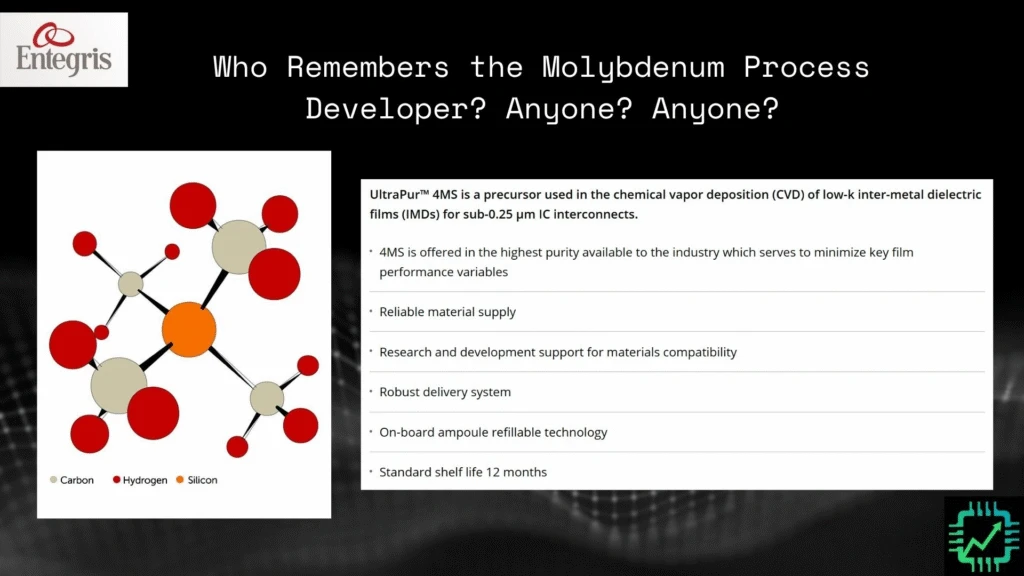

Here’s another one: A special precursor chemical called UltraPur 4MS used in molybdenum CVD thin films. Anyone recall that fun little video from last year? Anyone?

Lam Research‘s (LRCX) molybdenum, or “moly,” manufacturing process. Here’s the video link from the relevant update in Q4 2024, for those of you that like chemistry. https://youtu.be/ddUDQxynR_Q

And Lam Research’s video on how new flash memory chips are made, where this new moly process is used: https://www.youtube.com/watch?v=hglK1cf3meM

Long story short, Entegris plays an important role in making this molybdenum process work, among a lot of others in the fab.

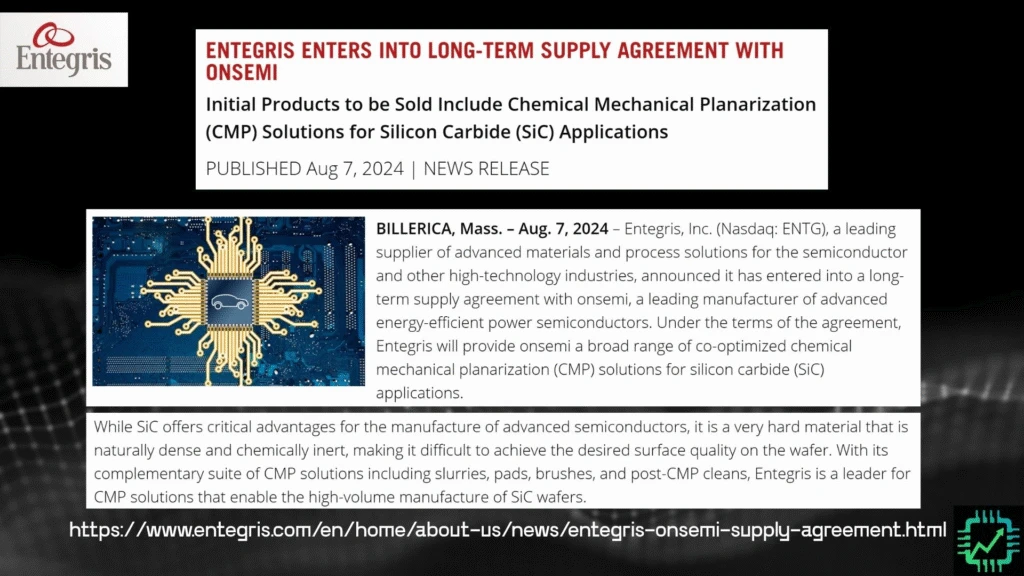

Here’s one more. Entegris also supplies slurries and other chemicals needed to “grow” silicon carbide (SiC) semiconductors. It signed a long-term supply agreement with who all you already know to be the emergent leader in SiC production, Onsemi (ON).

What else is cooking in the Entegris chemistry lab?

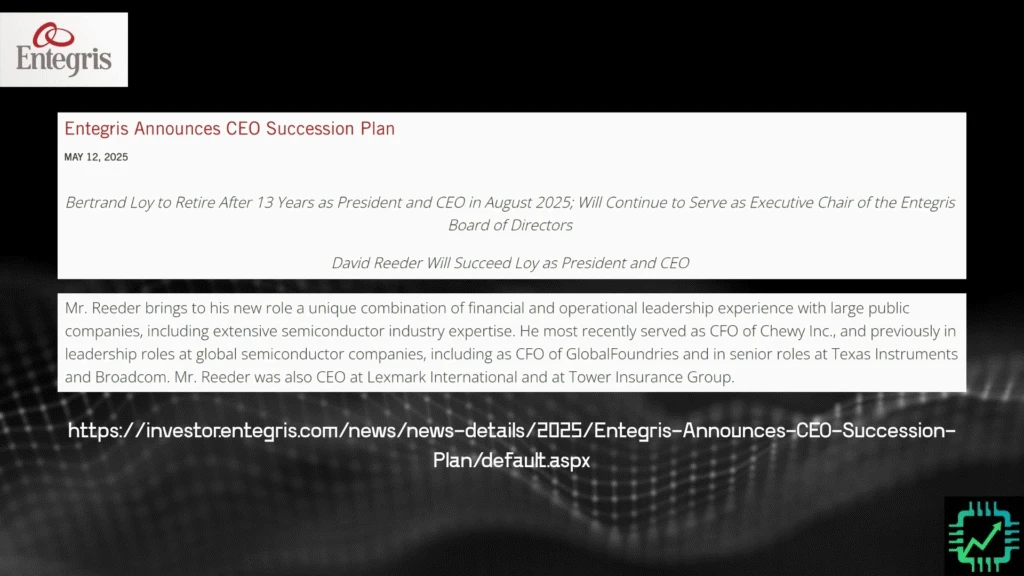

You should also know that Entegris’ CEO Bertrand Loy is retiring. It was an epic 13-year run. He will remain on the board of directors.

The new CEO, David Reeder, has a financial background. Most recently, he was the CFO of Chewy, as well as having held other roles at semiconductor companies like GlobalFoundries (GFS).

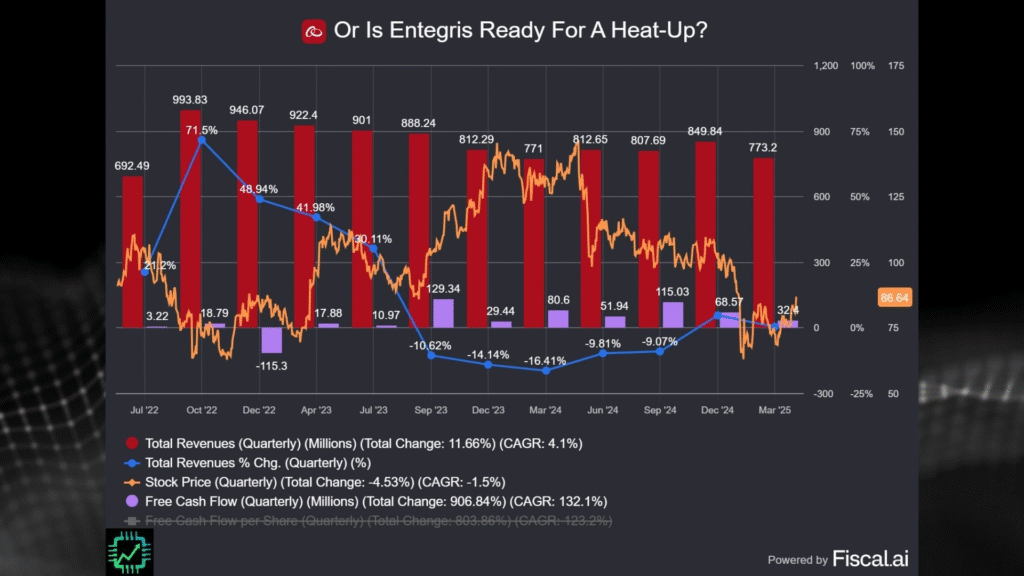

Amidst this CEO transition, it would appear Entegris’ business cycle — driven by the 2+ year downturn and sluggish recovery in most semiconductor end markets (excluding accelerated computing, see opening slides in this article) — is bottoming out. Revenue is now roughly flat with where it was a year ago. There was the seasonal decline from Q4 2024 to Q1 2025, but otherwise signs are pointing towards a resumption of growth.

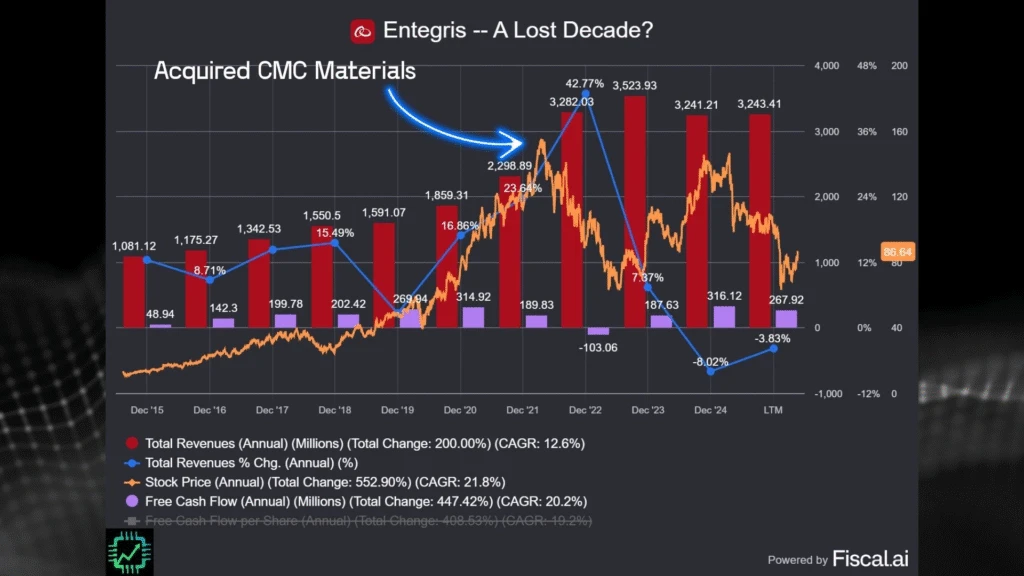

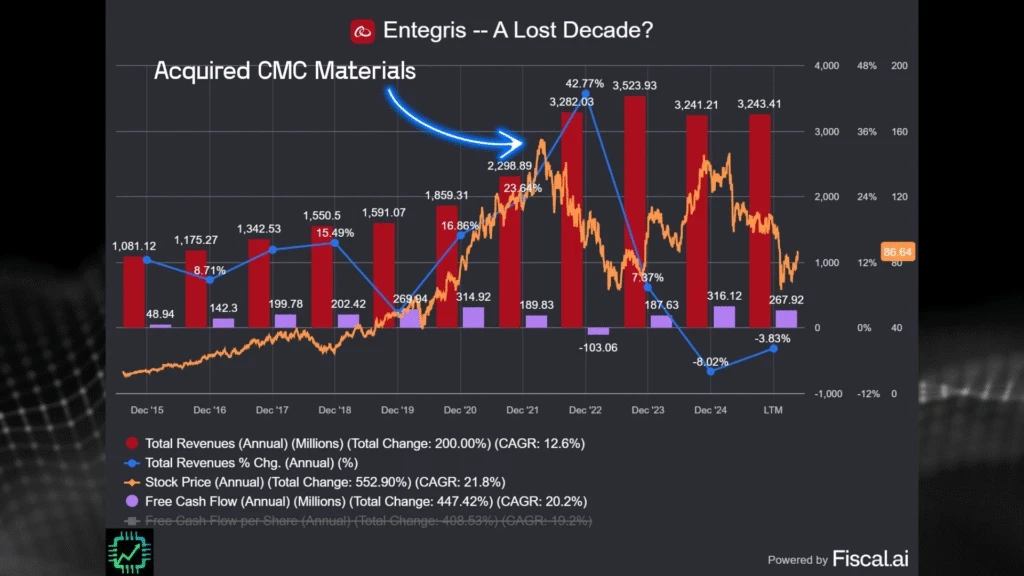

But what happened over the last 5-year stretch, anyways? It was ugly…

We do need to acknowledge the last 5 years were pretty rough. There was the pandemic, the ensuing chip shortage, and then the massive chip oversupply problem that started the second half of 2023 (oversupply started earlier for consumer electronics).

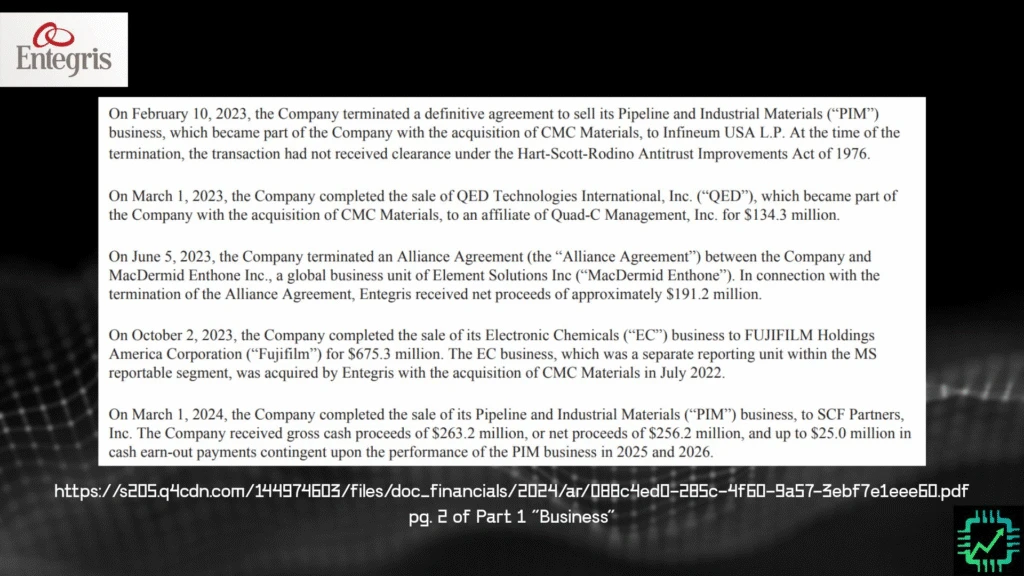

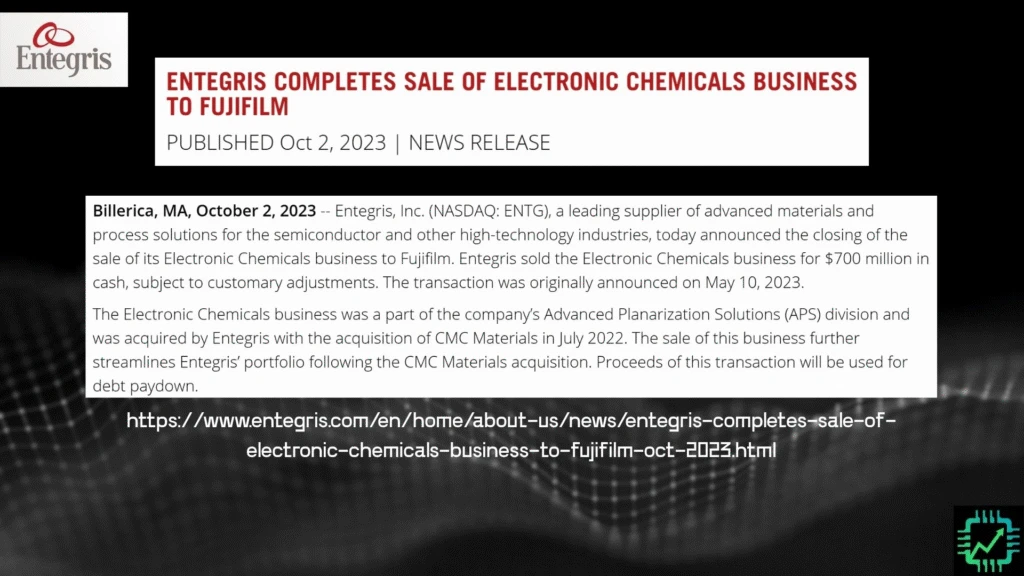

And during this period, Entegris made a sizable acquisition of a peer called CMC Materials. Bolt-on acquisitions have been a frequent feature of Entegris’ business under CEO Loy, but this one was a big deal given all the asset divestitures that ensued since July 2022 as Entegris repositioned as a specialist of advanced semi materials and chemicals. (See also https://s205.q4cdn.com/144974603/files/doc_financials/2024/ar/088c4ed0-285c-4f60-9a57-3ebf7e1eee60.pdf pg. 2 of Part 1 “Business”)

One of the final steps in the acquisition and subsequent asset re-shuffle was the sale of the electronics supply chain chemicals unit to Fujifilm (Entegris whittled down its segments to a more focused play on semiconductors, versus more generalized electronics manufacturing, see our update a couple weeks ago on OEM, ODM, and EMS companies: https://youtu.be/-Tgx2ghde48).

Ok, so the last 5 years were rough-and-tumble, but look at this slide again. Even including the 2020s, Entegris has a 10-year free cash flow (FCF) CAGR (compound annual growth rate) of 20%. 20%! As a retail investor, you should pray to the market gods you can own a blended portfolio of companies with such an average. It will beat the market handily.

To make financial visuals and conduct in-depth company research, check out our Fiscal.ai. Use our link to get 15% off a paid plan! Fiscal.ai/csi

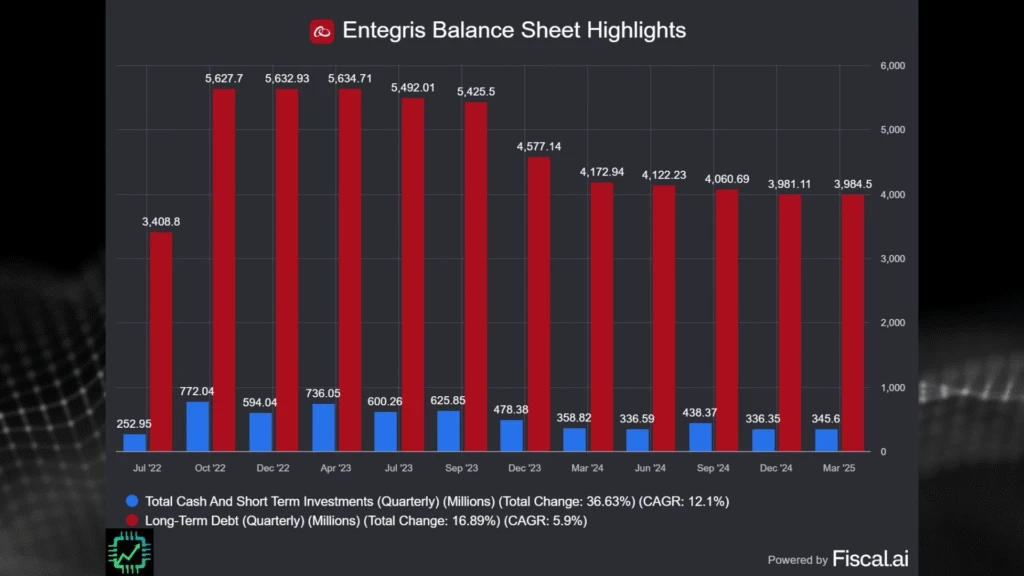

So can Entegris return to that market-beating form? Again, it would appear the down cycle has bottomed. Here are the same financials as above, but on a quarterly basis.

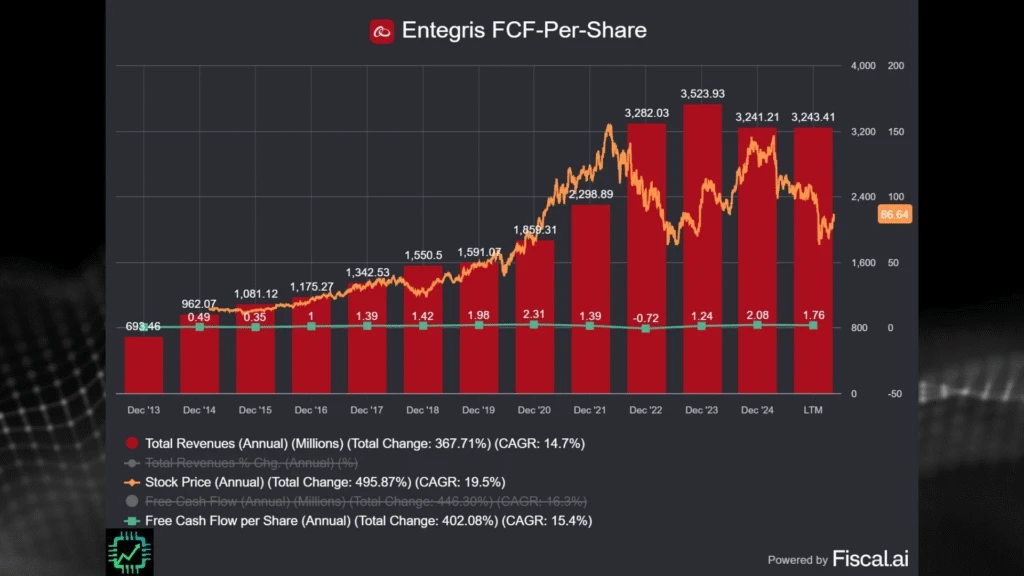

And here’s going back just a bit further to capture the entirety of Loy’s tenure as CEO. FCF-per-share (green line) has been quite good, excluding the last few years.

Besides a need for sales and profit to ratchet back up again, Entegris will also need to de-lever its balance sheet — especially after taking out a sizable chunk of debt to acquire CMC in 2022. Cash on balance is running a bit thin for our personal taste, even for an industrial chemicals business.

Nevertheless, with profitability depressed and Entegris possibly close to a cycle bottom, the trailing valuation metrics cited at the beginning of this update could be misleading. If revenue ratchets up, expect margins to expand at an even faster pace (remember, for some cyclical businesses, a very high double-digit % or even 100%+ profit growth rate is possible in the first year of a new growth cycle).

That said, we ran a simple reverse DCF (discounted cash flow) to see what kind of assumptions Wall Street (not Chip Stock Investor’s estimate) has for Entegris baked into the current valuation. We came up with the following (you can adjust the two-year growth rate up or down, and adjust your terminal rate accordingly the opposite direction if you believe the market is factoring for a lower value).

- $1.76 TTM free cash flow-per-share

- 25% free cash flow-per-share growth rate for two years

- 7% terminal growth rate thereafter (ballpark semiconductor industry long-term expected average)

- Discount rate of 10%

- = fair value of $85, about where the stock was trading on July 3, 2025

In summary, Entegris could be a pretty good buy right now, assuming it is on the cusp of returning to growth and the CMC acquisition made three years ago begins to yield profitable results. If you do decide to buy, mind the fast cycles inherent in Entegris’ sales to fab customers. Purchases of a company like this ought to be timed around these cycles, and patience exercised in between.

And if you pass, that’s ok too. Small-ish industrial chemical businesses aren’t for everyone. Alternatives to Entegris might include the very large and diversified Linde, among others (we exited Air Products due to the activist investor drama, board shake-up, CEO exit, etc.). We’re waiting for earnings season to make our own personal decision on ENTG stock.

One Response

Superb write-up on Entegris. This company seems so sexy to me. I’m taking a nibble here to add some diversification to my portfolio and to keep an eye on the semiconductor market. I’m calling this a watch tower stock. I went too far into the rabbit hole, and there’s no coming out of it. Moly for life!