Workflow management and automation is a segment of the software and enterprise SaaS industry we’ve invested in for years. But an existential threat has emerged in artificial intelligence (AI), and has sent top stocks in this category tumbling. Is AI really disrupting these businesses, or is there a standout in workflow automation that will benefit from AI? And what changes need to take place for AI to help SaaS companies, rather than hurt them?

ServiceNow and the current state of workflow management software

Excluding big tech names that have some of their own in-house offerings, workflow management software leaders include ServiceNow (NOW), Atlassian (TEAM, discussed during our “browser wars” update last year), Monday.com (MNDY), Asana (ASAN, not one we cover here at CSI), and Smartsheet which was acquired and taken private in January 2025.

The CSI portfolio owns Monday.com and ServiceNow. But the latter, ServiceNow, the leader among workflow automation offerings, has provided some proof that AI might be a benefit to its platform. Let’s focus on some recent developments and data points.

AI the disruptor, or valuable add-on?

Workflow management software — used by organizations to orchestrate employee tasks, keep them productive, and automate redundant tasks — was built using the subscription (SaaS) model. Compute-hungry AI, on the other hand, is following a very different business model: Usage-based (consumption) pricing, basically billed based on how much the customer is using the AI product.

In ServiceNow’s case, AI products revolve around its AI Control Tower (centralized management and visibility for an organization’s AI software) and AI Agents (build and connect AI to data to automate tasks). A lot of new capabilities around these two AI product categories have been announced in the last year at ServiceNow — the result of ongoing development, as well as a long-running partnership with Nvidia (NVDA) to continuously improve on workflow automation. https://www.servicenow.com/platform/infrastructure/nvidia.html

As one of the current arguments go against the traditional SaaS model, new AI automation tools are handling more tasks and freeing up employee time. This could reduce the number of employees that need access to the software (the number of “seats” a software company charges its customers for), thus reducing SaaS company revenue.

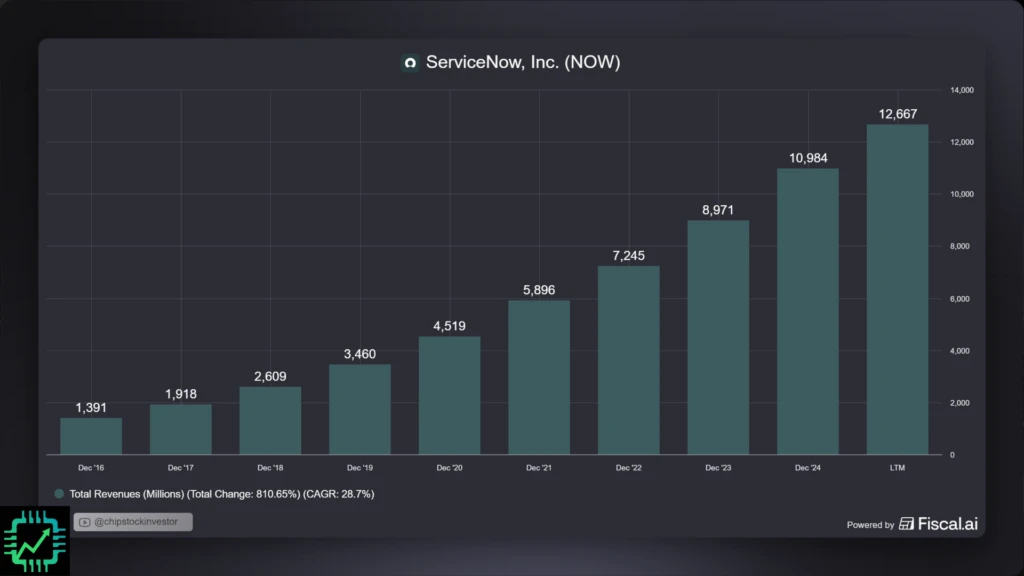

However, as of yet, AI has done little to slow ServiceNow down. Revenue growth rate has cooled to the 20% to low-20% range, but that’s a natural progression given the company’s size, pushing $13 billion in annual sales and targeting $15 billion in 2026.

Want to analyze businesses make financial visuals like the one above? Use our link to get 15% any paid plan to your one-stop shop for analyzing businesses of all kinds. Fiscal.ai/csi/

In fact, on December 10, 2025 at the Barclay’s Global Technology Conference, ServiceNow CFO Gina Mastantuono said that, rather than being a disruptor, AI has helped the business lay the foundation for more growth.

Like most other enterprise SaaS companies, ServiceNow has adopted a hybrid pricing model for AI: Part traditional subscription, part AI usage pricing. As part of its early hybrid, ServiceNow has begun to price AI consumption into subscription plans and renewals. Mastantuono said these plans are getting as much as a “30% pricing uplift” due to adding AI use into the subscriptions.

By the back half of 2026/early 2027, the new subscriptions with AI plus additional AI volume revenue will begin to have an impact on total revenue, as visualized above. AI products are on track for ~$1 billion on the ServiceNow platform in calendar 2026, up from ~$500 million in 2025, according to Mastantuono.

New AI development risks still need to be discounted

If AI isn’t a threat, then why is ServiceNow stock on the decline along with many other SaaS stocks?

Developing new software tools costs money. Bolt-on acquisitions that ServiceNow has been making also come at a price. And given that AI and AI agents work when given access to sensitive customer data, developing these new products also bears ongoing risk that ServiceNow will need to manage in the coming years. This ongoing risk is one reason the company has been betting on cybersecurity as of late. Let’s come back to that in a moment.

Since stocks are valued based on future expected cash flows, the prospect of higher spending — even if temporarily — needs to be accounted for in valuation.

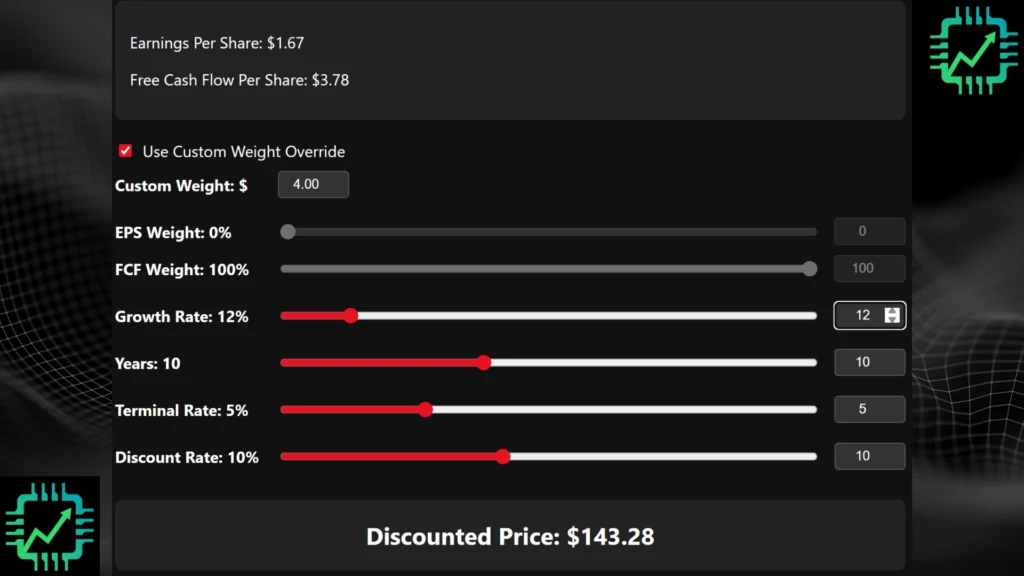

Investors have done just that, eliminating a lot of the premium NOW stock used to fetch over the course of the last decade. Shares currently trade for just under 30x one-year-forward expected free cash flow (FCF). But what does that actually imply? We ran one reverse DCF scenario to arrive at the current stock price (~$135 as of this writing).

Assumptions:

- $4.00 FCF-per-share (~full-year 2025 estimate, Q4 earnings are on January 28th)

- 12% FCF-per-share growth rate for 10 years

- Terminal growth rate of 5% thereafter

- Discount rate of 10%

This is but one possible scenario, but for us, it represents a decent estimate of what Wall St. is currently pricing in for ServiceNow in the AI era. And for us here at CSI, this leaves enough room for upside should ServiceNow beat these expectations over the next 5 to 10 years.

Join us on Semi Insider for more of the conversation on ServiceNow, its recent cybersecurity moves (the CSI cybersecurity industry refresh is coming soon), a growing set of tools to analyze the semiconductor supply chain, and a community of long-term investors!