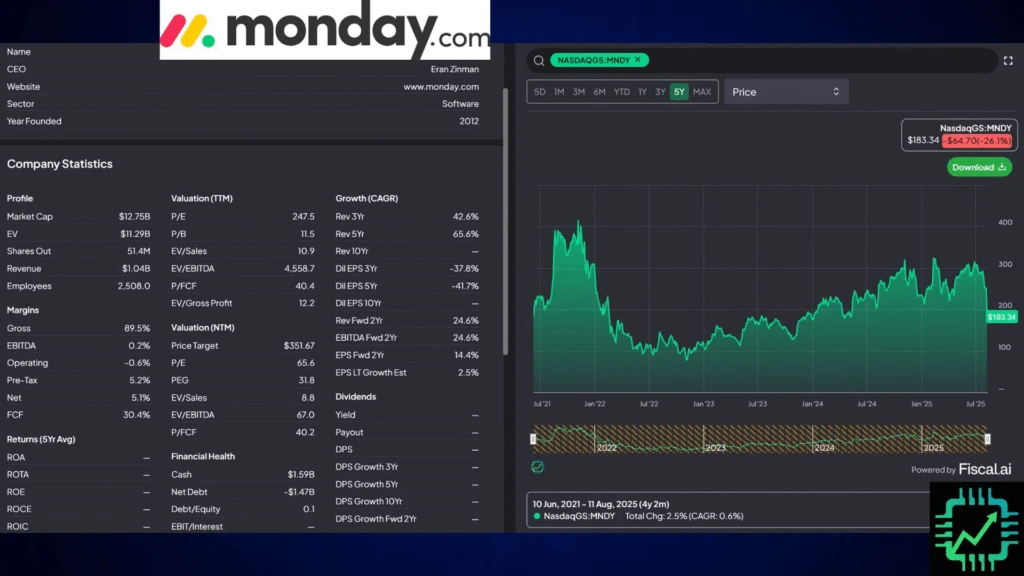

For every victory in Q2 earnings season this year, it seems there’s been a corresponding disaster. Last Monday, the “disaster” was Monday.com (MNDY).

Much has been said of the “AI is going to eat enterprise SaaS” thing. Sort of like how SaaS was eating traditional software last decade (it didn’t, it augmented the traditional software market). We’ve actually already discussed this at length in late 2024 in the light of Salesforce (CRM), what was at the time supposed to be a hot IPO in Klarna (oh yeah, what happened there?), and smaller software companies like UiPath (PATH).We’ll address some of these topics later on in earnings season, because the AI (ahem, really its “accelerated computing” more broadly, thanks to Nvidia) will most certainly impact software.

But for now, what happened to Monday? As usual, let’s zoom out. Since bottoming after the bear market a few years ago, Monday’s stock has actually done quite well, recovering to a much more rational valuation after the 2020-21 SaaS boom and IPO craze.

We’ve owned some shares of MNDY since the depths of said bear market, and long story short, we’re still happy owning it. In an aged work management software industry, Monday.com continues to outperform its peers in profitable growth at scale.

As a point of comparison, competitor Smartsheet was taken over by private equity in January, no doubt to maximize cash flows for its new owners. Atlassian and Asana have had struggles sustaining momentum so far in the bull market since 2023.

Building off its core service, Monday has launched multiple new products. Most notable as of late is its CRM (customer relationship management) tool, which MNDY reported has just reached a $100 million annualized revenue run rate.

Since Nvidia kicked off the AI craze a few years ago, investors have been waiting for that enterprise software AI moment. Only a couple of early winners have emerged, like AppLovin, Palantir, and ServiceNow. Overall, enterprise “AI” progress has been slow-moving.

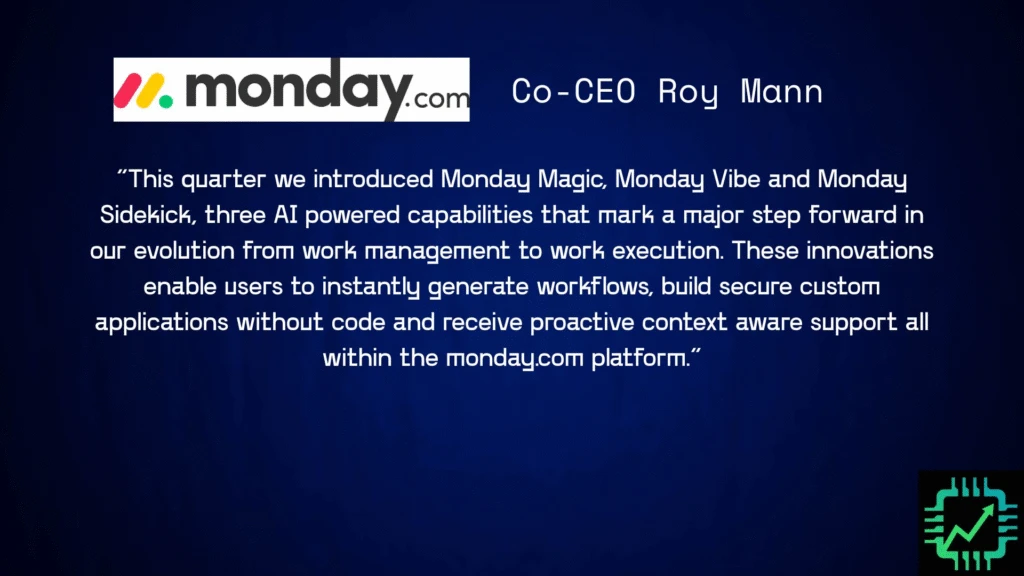

For its part, Monday has launched some AI products within its platform, and management noted this recent quarter that it is expanding in new directions like workflow automation, vibe coding, and service support.

Understanding the SaaS product cycle

As we’ve discussed in some of our live events on Semiconductor Insider, every industry has a “cycle.” For Software-as-a-Service (SaaS), the cycle tends to be product-driven, which means higher Research & Development (R&D) and related employee stock-based compensation (SBC) expenses. It would seem Monday is in the midst of just such a cycle, which makes this a great learning experience.

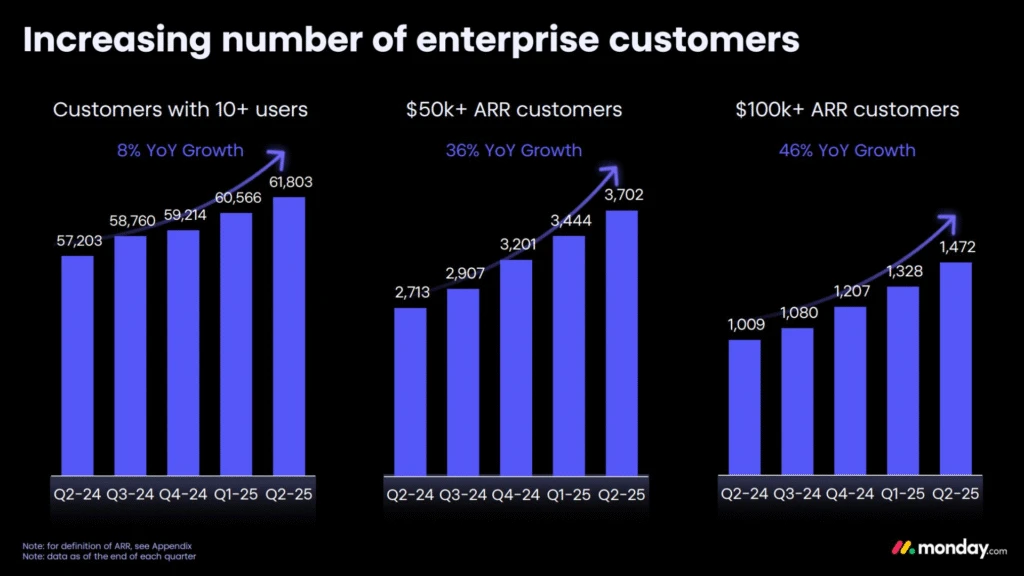

Firstly, some of the older core products geared towards small businesses have begun to slow in momentum. You can see this show up in the “customers with 10+ users” metric, which grew just 8% year-over-year. Monday is moving upmarket to bigger enterprises, which is where the momentum is right now – but this customer base is still relatively small.

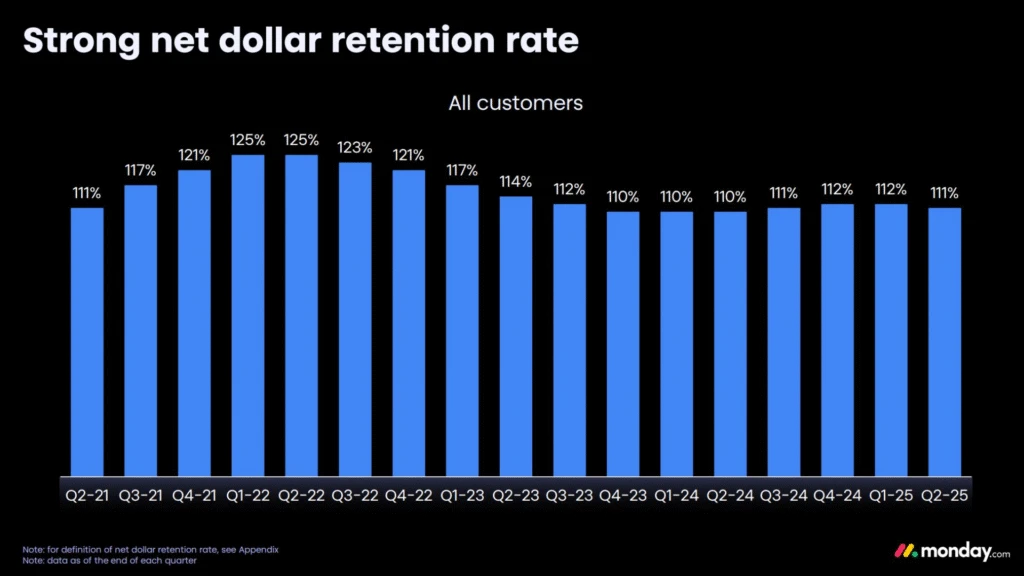

This trend also appears in the total Net Retention Rate (NRR), which was 111%. A rate over 100% is good, as it represents increased spending among existing customers, but this was another sequential slowdown. Again, the sluggish metric is caused by smaller business customer churn rates, offset by the expanding base of large enterprise customers.

Additionally, during the Q&A section of the earnings call, management cited that changes in Google’s search algorithms are affecting traffic to Monday.com, which is a key channel for attracting those smaller customers.

The numbers behind the narrative

Clearly, analysts were a bit worried about the trajectory of the company as it rolls out new products and goes after larger customers. But then again, all of this was already baked into the guidance Monday has been providing all year. Notice the scale-up of profitability as sales have grown, even as R&D expense increased to 20% of revenue in Q2 2025, compared to 16% the year prior. This is the SaaS product cycle at work.

This investment phase includes Monday’s previously stated plan to increase employee headcount by approximately 30% this year. This affected, among other things (aforementioned SBC), free cash flow (FCF) margins, which fell to just a 21% margin in the quarter, down from 39% in Q1. Time to panic, right?

Hardly. The outlook, even three months ago after the 39% FCF margin quarter, was for those margins to moderate throughout the year. And even after Q2 FCF came in “light” due to elevated R&D, MNDY still increased its FCF margin outlook for the full year.

We’ll leave you with one final data point. We calculated the free cash flow-per-share on a trailing-12-month (TTM) basis through Q2, 2025. Even with the higher employee SBC, MNDY is still making good per-share profit progress, up 21% from the same TTM period that ended in Q2 2024.

In our estimation, this is still a young SaaS business. Things get messy, and even small changes in expectation can have a big impact on valuation and stock price. That’s what’s happening right now for Monday.com, especially as it gets aggressive in that new product development cycle. And it’s why we decided to buy a little more and strap in for some turbulence. It’s all par for the course when making small-cap bets.