This is a follow-up to some of our recent write-ups about the struggles for the old industry biz model, the IDMs (integrated device manufacturers). Monolithic Power Systems (MPWR) continues to win lots of new business at their expense in the AI data center era, diversifying across a multitude of third-party foundries and outsourced assembly and test companies (OSATs) to nimbly supply its end market customers where and when they need.

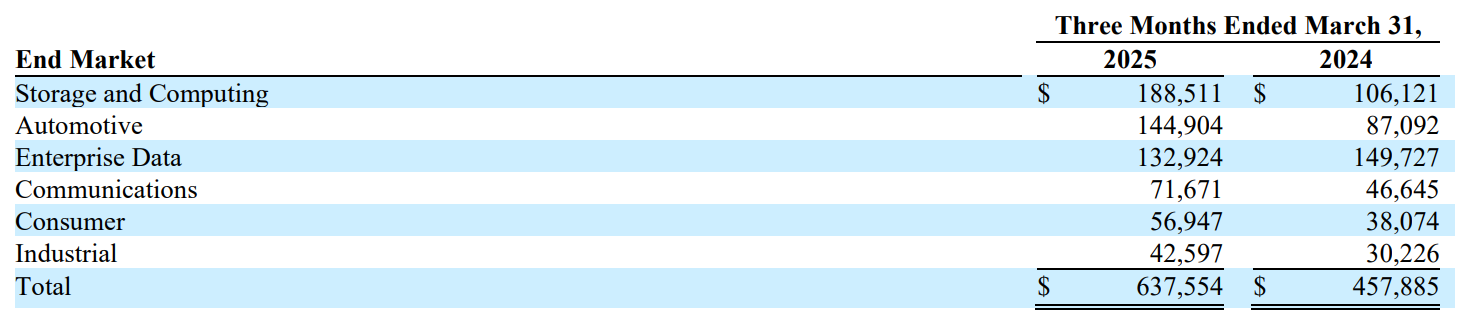

Below are Monolithic’s sales by end market as of Q1 2025. Total sales increased 39% year-over-year, far outpacing its IDM peers:

These segments can be a bit confusing, though, especially “Storage and Computing” and “Enterprise Data.” What’s the difference?

Monolithic Power’s investor day update for the dawn of AI data centers

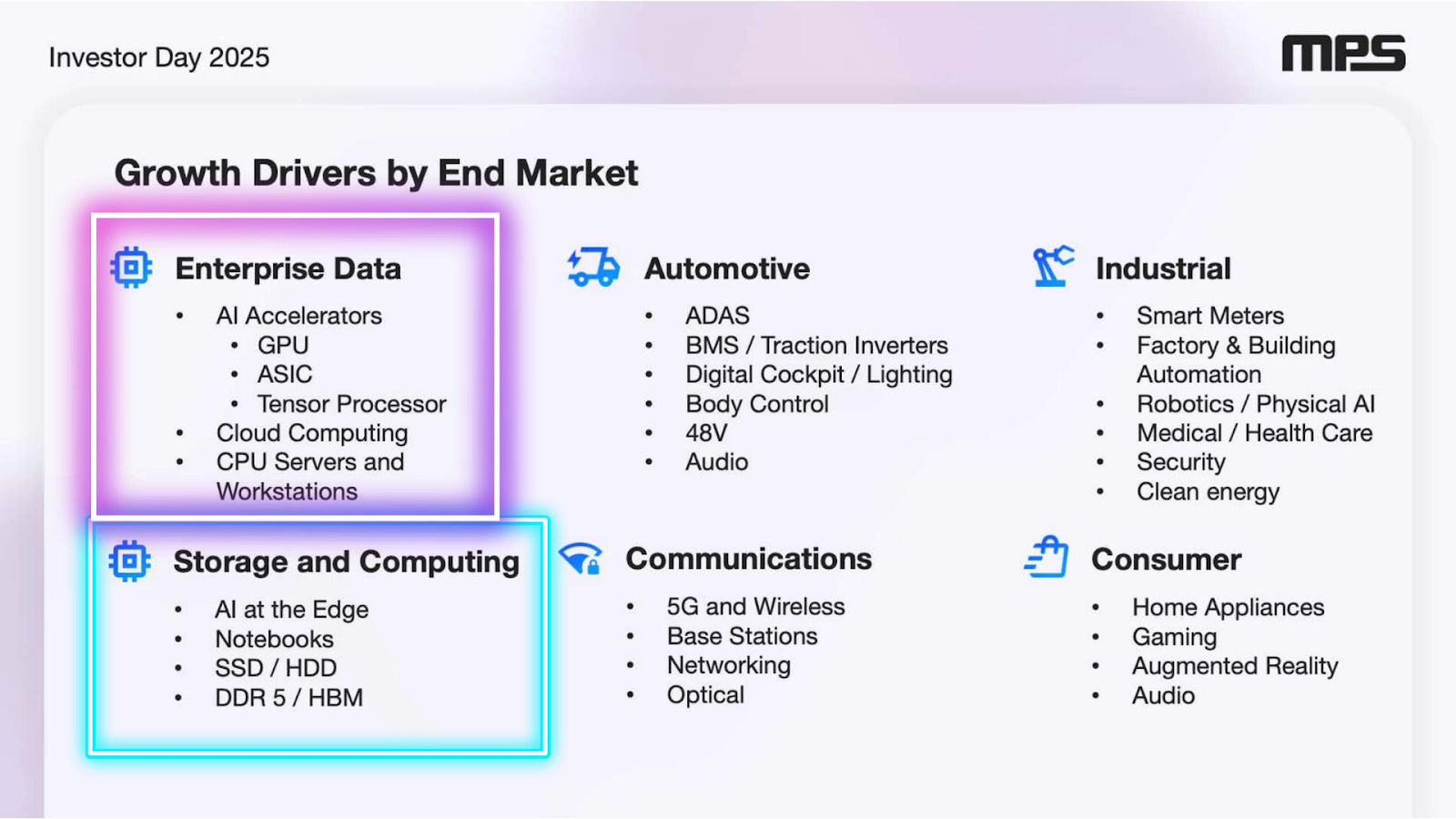

First, what is “Storage and Computing,” the first line above? And how does that compare to “Enterprise Data” on the third line? Here’s the slide from the Monolithic’s Analyst Day presentation in March 2025.

Storage and Computing, the largest revenue segment (see next slide below), is in growth mode – mostly from the ramp-up of HBM (high-bandwidth memory) for data centers. It’s also getting a bit of lift from improving consumer electronic inventories after there was a bit of excess global supply in Q1 2025.

Enterprise Data, on the other hand, was down slightly year-over-year. That’s the segment for AI accelerators and data center servers (GPUs). Why in the world would that segment be in year-over-year decline? The short answer: Monolithic is ramping up production during the second half of 2025 for new systems, including Nvidia (NVDA) Blackwell GB300s, Alphabet’s (GOOGL, GOOG) Google TPUs using Broadcom IP, AMD Instinct accelerator systems, and others.

Monolithic CEO Michael Hsing was cautiously optimistic this Enterprise Data segment would have a big 2H 2025 during the last earnings call.

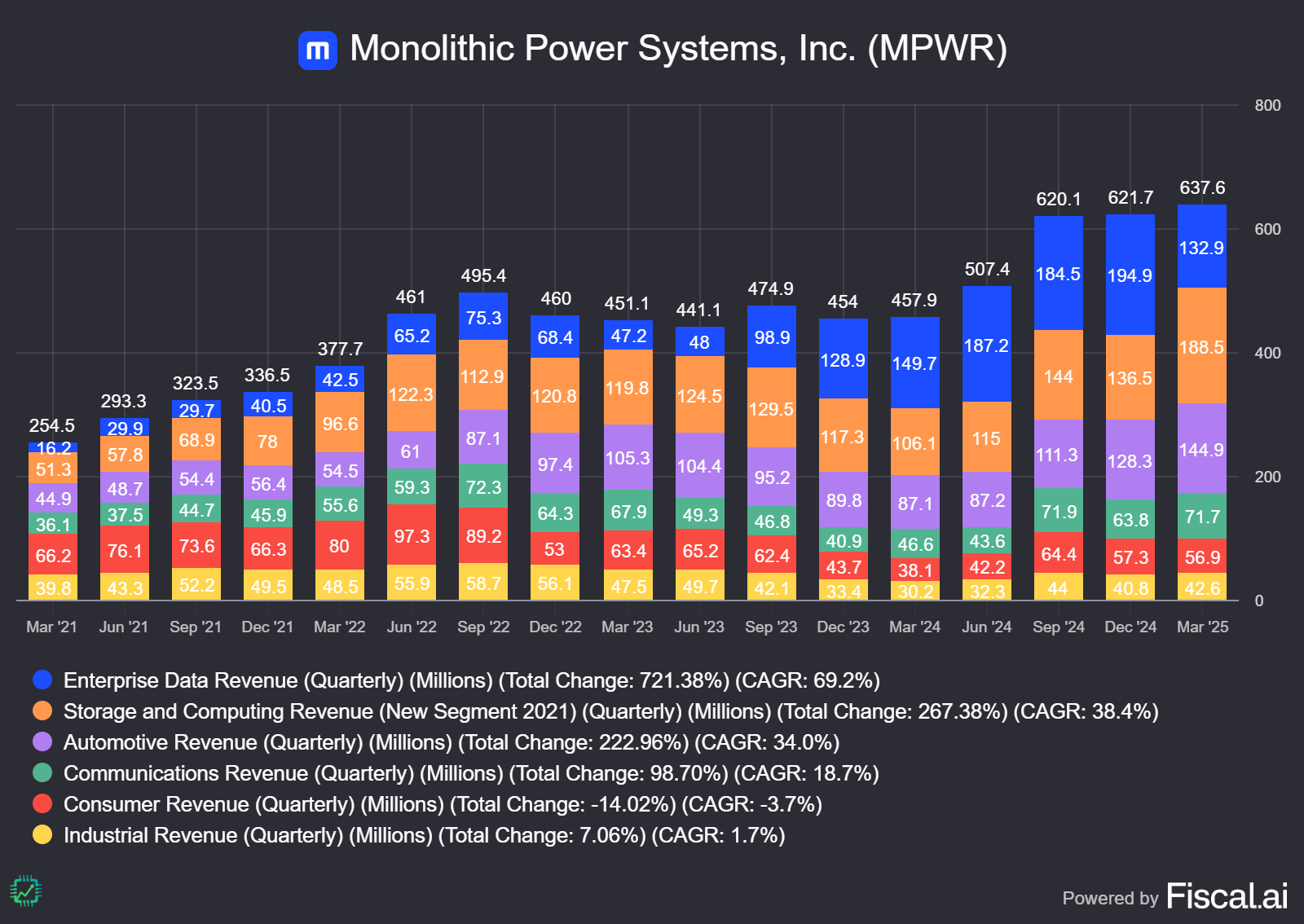

Here’s a visual of the revenue segment trends over time. Note the especially large ramp-up of both Storage and Computing and Enterprise Data since 2021 – not long before Nvidia’s Hopper data center architecture took flight.

If you want to make great financial visuals like the ones above, check out our blog sponsor Fiscal.ai. Visit our special link to get 15% off any paid plan! Fiscal.ai/csi

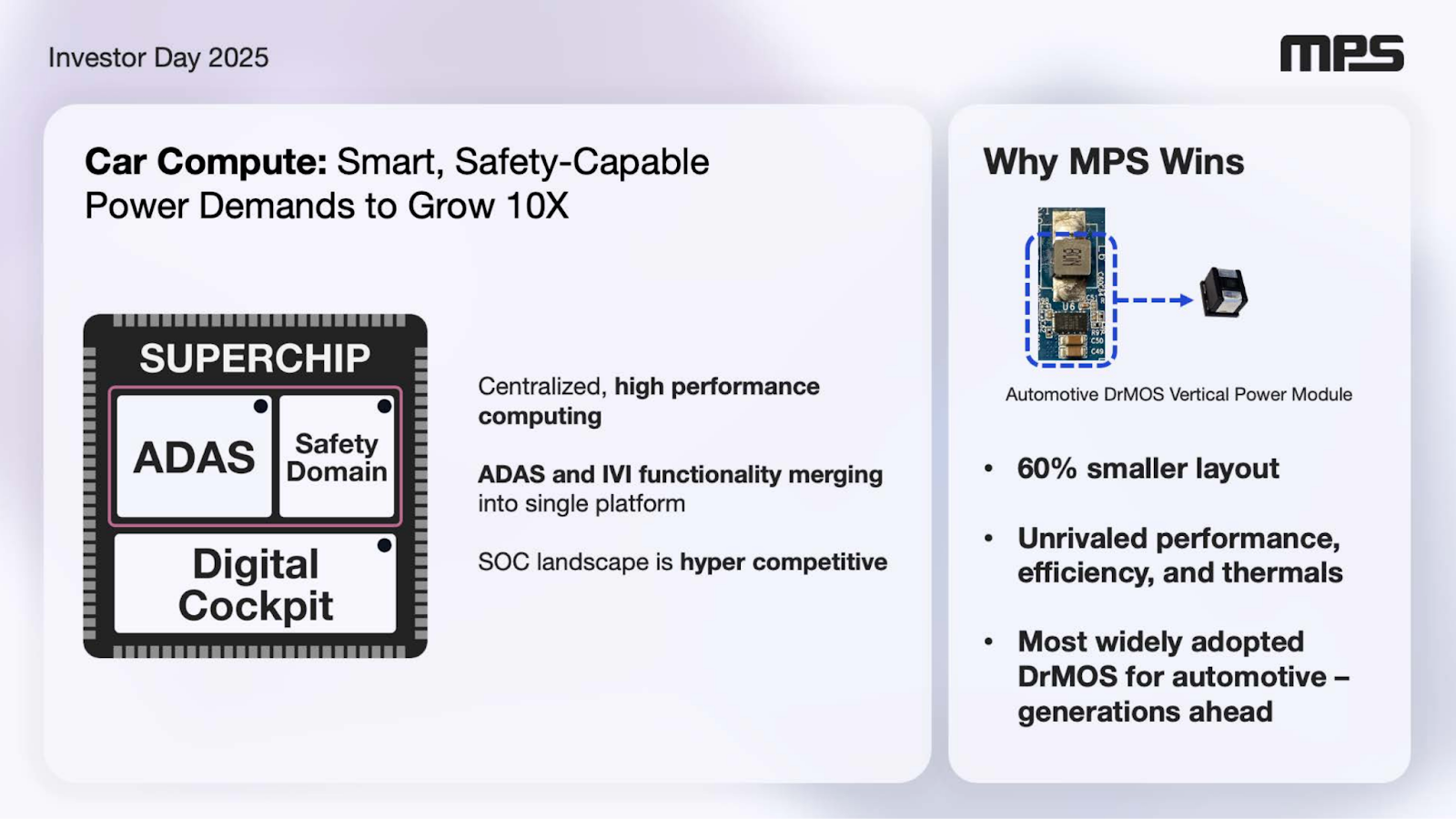

What about automotive and industrial – including robotics?

Monolithic fits into our auto/industrial/power basket of chip stocks, and for good reason. The modern car is using up a ton of power to enable all of the tech consumers want. And for all things power management, Monolithic excels.

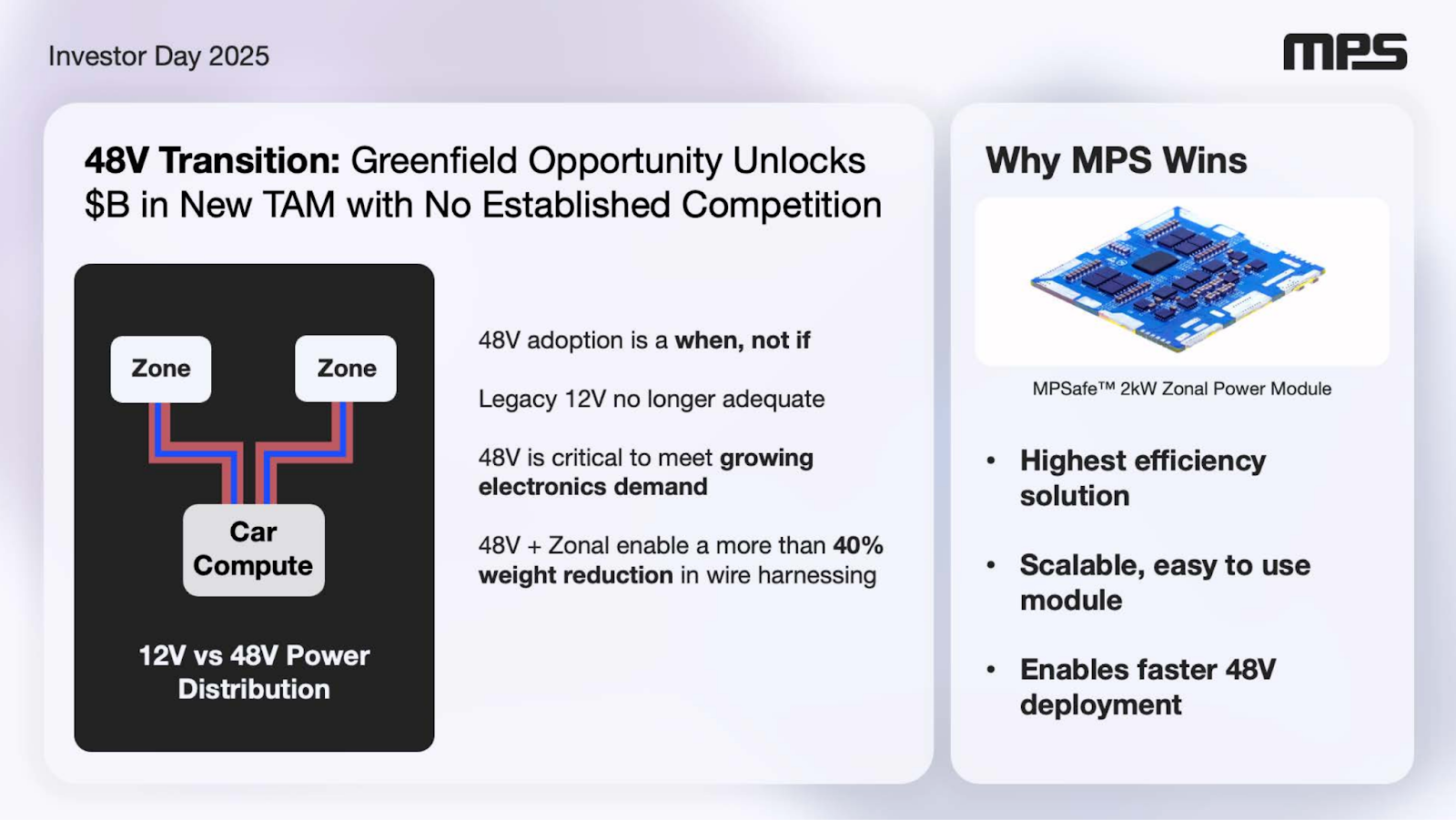

Note in the last visual, the “Automotive” revenue segment has continued to buck the industry downturn. That’s because Monolithic is landing a lot of new design wins in the auto industry, across all three continents where auto manufacturing is a key industry. This includes the battery transition (some high-end models, not industry wide) from 12V to 48V.

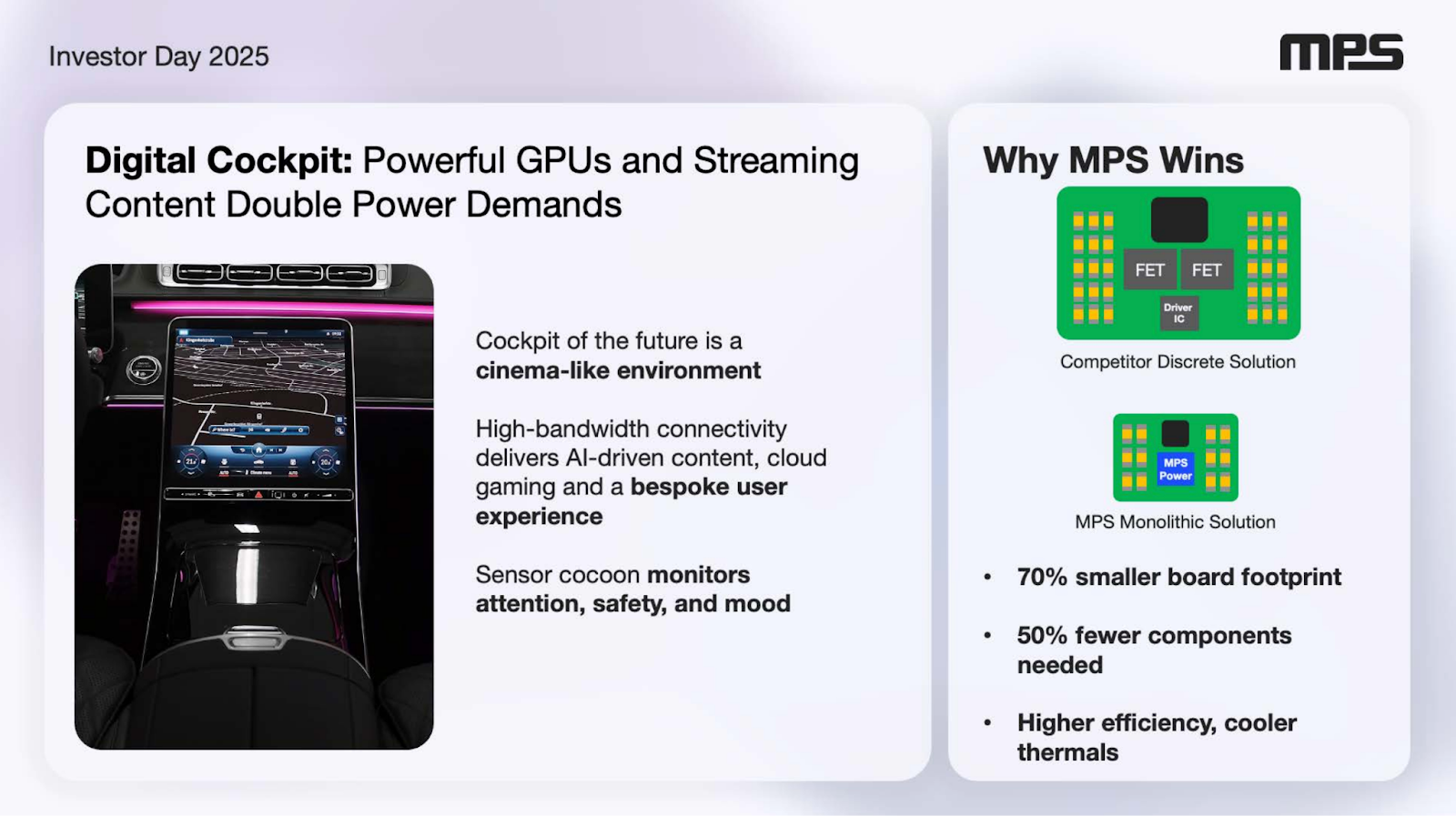

And as we’ve been discussing as of late in our videos, some of this work in Automotive (currently one of the biggest “robotics” markets) is spilling over into the nascent “humanoid robot” industry (if we can even call it an industry at this point).

Monolithic provides integrated motor control and power solutions in tiny packages. Working on hand dexterity is particularly tricky. See all the components needed in the first slide below? And the small Monolithic power module in the second slide?

If investing in humanoid robots excites you, seriously, chip designers are where it’s at right now. And Monolithic Power Systems could be an under-the-radar beneficiary.

Are AI data centers fueling profitability?

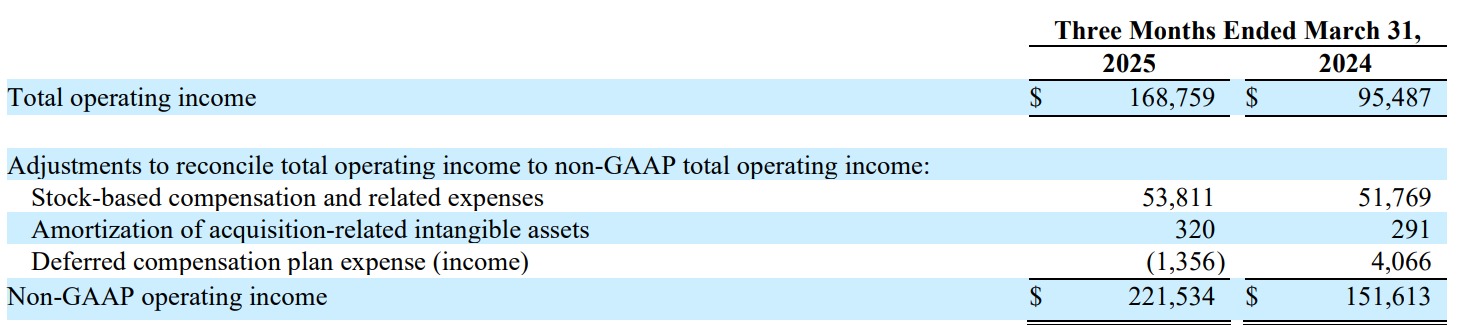

We’re in the early-to-middle of a new growth cycle for Monolithic, so the valuation is wonky. Below is the operating income and adjusted operating income reconciliation for Monolithic from Q1 2025. The company is enjoying great operating leverage during its data center- and automotive-fueled expansion

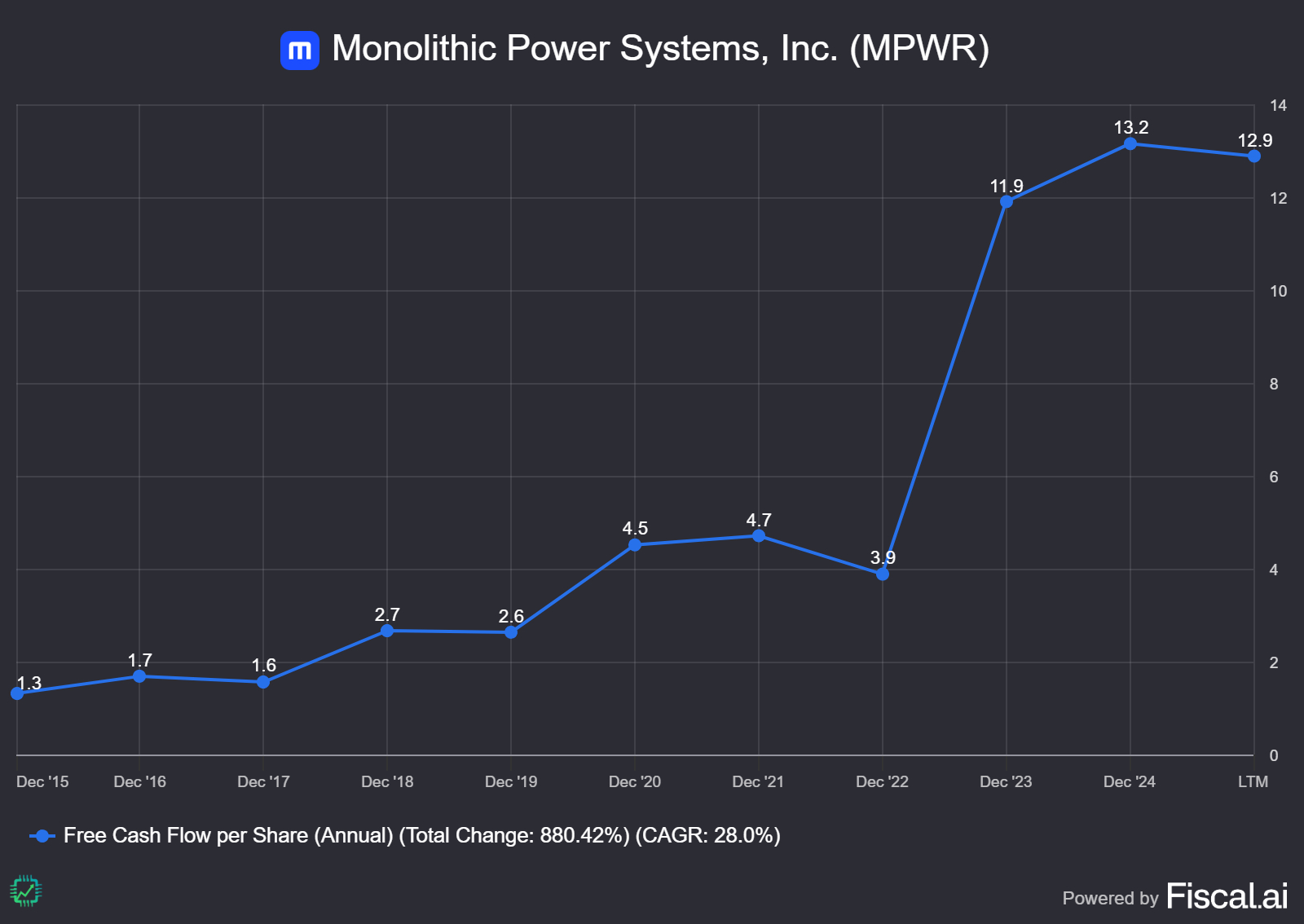

Also of note on the above, Monolithic actually shrunk its share count both quarter-over-quarter and year-over-year with its share buyback program in Q1 2025. This share buyback program should help with the free cash flow (FCF)-per-share growth story as well. Here’s the trend over the last decade:

Monolithic Power Systems has been a massive market and industry outperformer in its two-decade existence as a public company. And with a new growth cycle underway, perhaps powered by Nvidia’s AI data center Blackwell systems starting later this year, the stage is set for the company’s positive story to continue. We’ll have more updates on the company soon, and join us over on Semiconductor Insider for the full discussion! chipstockinvestor.com/membership

3 Responses

Great piece! One of my fav holdings. I’m a very happy business owner.

Thank you Nicholas

I love how this is an under-the-radar robotics play. You make me want to buy more.