This post is taken from our show notes. A full list of these are available to our Semiconductor Insider membership via our Ko-Fi shop. Enjoy!

Nvidia‘s (NASDAQ:NVDA) accelerated computing data center boom has created a stir. More electricity is needed to operate these supercomputers, and new ways of cooling the chips and hardware down too. Nvidia has name dropped one partner company in particular: Vertiv Holdings (NYSE:VRT). Let’s take this power delivery and cooling equipment company through the Chip Stock Investor framework.

Vertiv (at the time, called Emerson Network Power) was a spin-off from Emerson Electric (NYSE:EMR) in 2016. It was separated from Emerson and sold to private equity.

Later, in 2020, the name was changed to Vertiv and the company was taken public via SPAC (special purpose acquisition company, remember those?). In 2022, activist investor Starboard Value took a stake in Vertiv and “encouraged” management to boost profit margins. (https://www.cnbc.com/2022/10/29/activist-starboard-takes-a-stake-in-vertiv-and-an-opportunity-to-boost-margins-is-in-sight.html )

Some recent AI data center history

One reason investors are suddenly hot on Vertiv stock? It recently entered the Nvidia (NASDAQ:NVDA) Partner Network, announced in tandem with GTC 2024 in March. It was also announced Vertiv would use and integrate with Omniverse, Nvidia’s “digital twin” supercomputing simulation ecosystem, which can be used to design data centers. https://www.vertiv.com/en-emea/about/news-and-insights/news-releases/vertiv-joins-the-nvidia-partner-network/ https://blogs.nvidia.com/blog/omniverse-next-gen-data-center/

Clearly there’s a lot of potential for companies to piggyback off of Nvidia’s big win from pioneering accelerated computing. There are big engineering challenges to solve in power delivery and cooling.

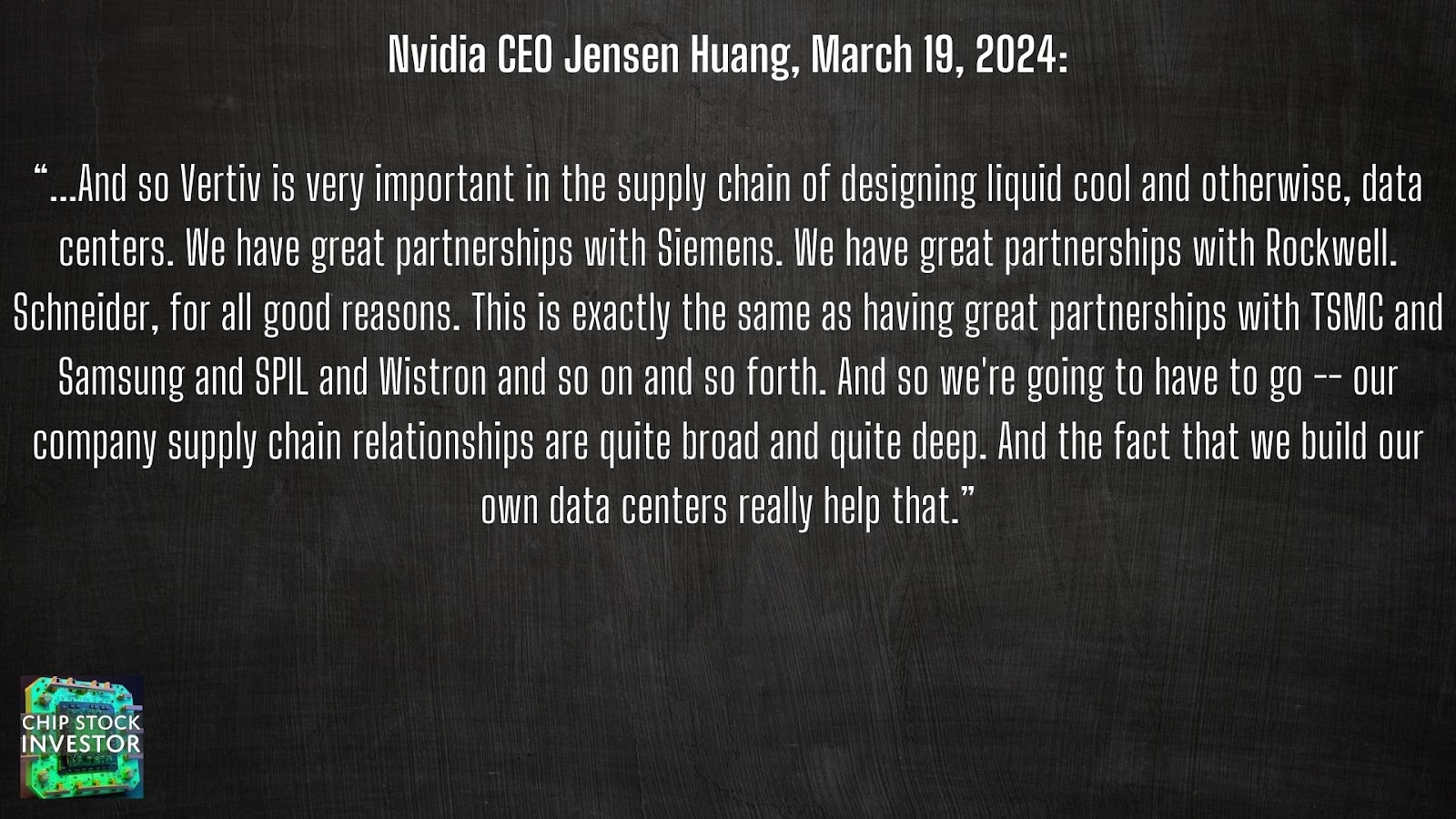

CEO Jensen Huang, addressing a question from analyst Matthew Ramsay from TD Cowen, following the GTC keynote in March 2024. Ramsay:

“…My team has been spending a good bit of time on power. I’m trying to decide if I should spend more time there or less. Some of the systems you introduced yesterday are up to 100 kilowatts or more. I know that scale of computing couldn’t be done without the integration that you guys are doing, but also we’re getting questions on power generation at the macro level, power delivery to the cabinet at that density. I just would love to hear your thoughts about how your company is working with the industry to power these systems.

Huang:

“…Power delivery, 100 kilowatts, as you know, for computers is a lot, but 100 kilowatts is a commodity. You guys know that, right? The world needs a lot more than 120 kilowatts. And so the absolute amount of power is not an issue. The delivery of the power is not an issue. And the physics of delivering the power is not an issue, and cooling 120 kilowatts is not an issue. We can all agree on that, okay? And so none of this is a physics problem. None of this requires invention. All of it requires supply chain planning. Makes sense? So that’s the way — and how big of a deal is supply chain planning? A lot. I mean we take it very seriously. And so we think about supply chain planning all the time. And you’ve got to go — the reason why we have great partnerships with — if you — I think if you look at Vertiv, I think the front page is a paper that we wrote together. So Vertiv, NVIDIA engineers working on cooling systems, okay?

And so Vertiv is very important in the supply chain of designing liquid cool and otherwise, data centers. We have great partnerships with Siemens. We have great partnerships with Rockwell. Schneider, for all good reasons. This is exactly the same as having great partnerships with TSMC and Samsung and SPIL and Wistron and so on and so forth. And so we’re going to have to go — our company supply chain relationships are quite broad and quite deep. And the fact that we build our own data centers really help that.”

Vertiv is thus tightly intertwined with Nvidia’s fate, which certainly isn’t a bad place to be. And this is a strong business model. Vertiv is an engineering business as much as it is an equipment manufacturer. This isn’t a simple assembler of parts, like what Super Micro Computer (NASDAQ:SMCI) does for the assembly of data center servers (computing units installed on racks, see pictures below).

So what does Vertiv do exactly?

From Vertiv’s 10-K (https://d18rn0p25nwr6d.cloudfront.net/CIK-0001674101/3b5064e9-e29d-4824-a962-b9a9ff66e5e1.pdf see “Business” section):

“Vertiv is a global leader in the design, manufacturing and servicing of critical digital infrastructure for data centers, communication networks, and commercial and industrial environments…

…Our portfolio of hardware, software, analytics and services aim to enable our customers’ vital applications to run continuously, perform optimally and scale with business needs.”

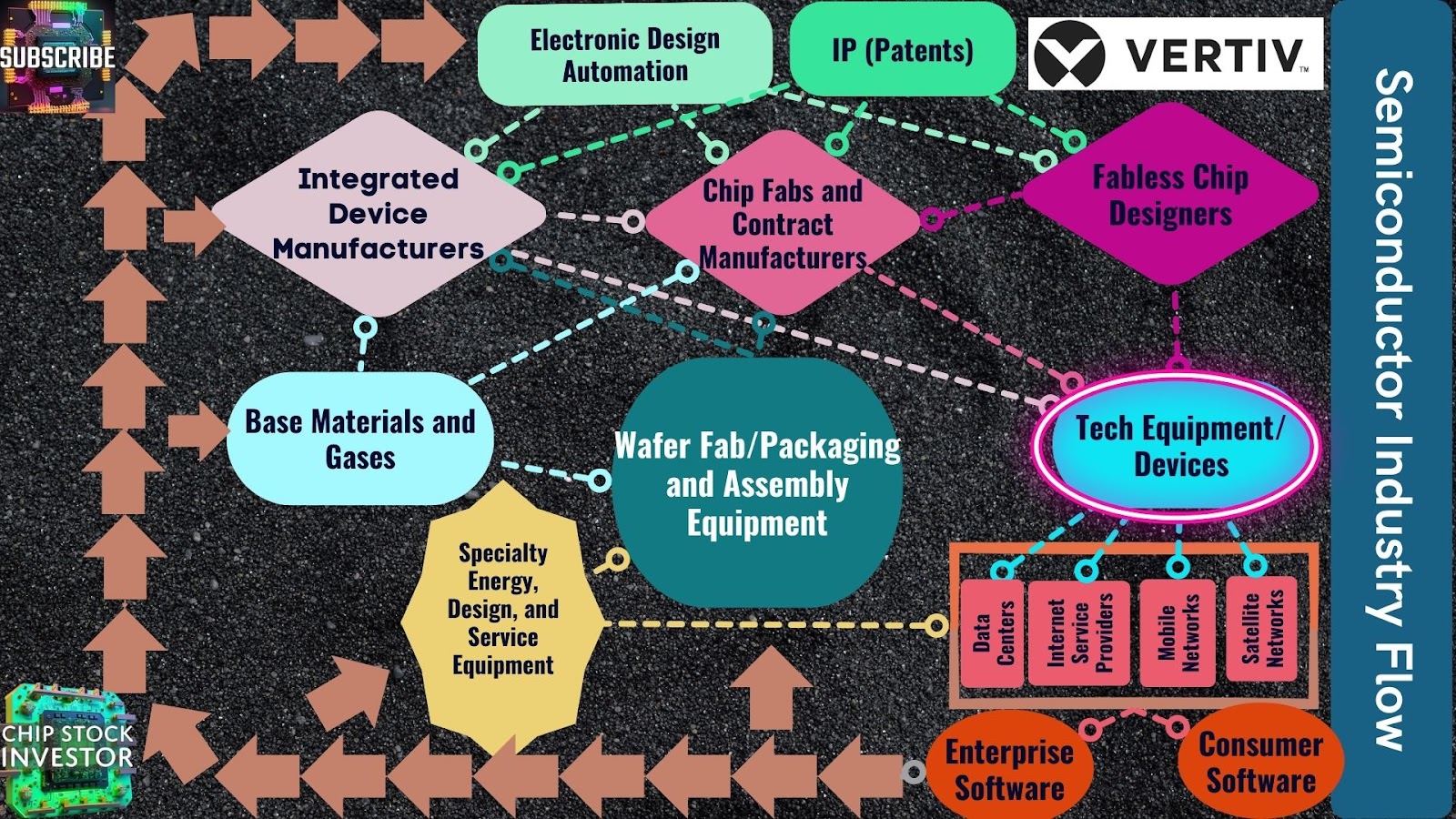

When placing it in the Semi Industry Flow, Vertiv falls into the tech equipment and hardware section. It provides critical power delivery and cooling infrastructure used in data centers, communications networks, manufacturing facilities, and the like.

A couple months ago after Nvidia GTC in March, we talked about how Nvidia is pulling off this massive acceleration in computing power by, in part, designing bigger chips. But bigger chips (and more of them) creates other issues. It means more power needs to be delivered to the data center and servers inside of them, and new cooling systems to keep everything operating optimally, and to prevent heat expansion (which can break the millions of tiny components inside of an AI server). More on that from our Nvidia/Cerebrus video here: Bigger Chips = Better AI? Nvidia’s Blackwell vs. Cerebras Wafer Scale Engine

Speaking of power delivery and cooling, we’ll be discussing that in our next video/write-up regarding quantum computing. Notice a theme? Higher computer power = more energy use = new engineering challenges regarding power delivery and cooling.

Vertiv’s two-part solution

Higher power use always creates heat problems. This is inherent with electronics design. Electrons jumping from one atom to the next (the “flow” of electricity) and higher voltage (the high 120 kilowatts of power in the Jensen quote earlier) creates heat as the electrons move through various components, and run into resistance from others.

First, Vertiv engineers and assembles power chips and other components into power delivery systems, those cabinets you see in videos of data centers with pull-out racks of servers (computing units).

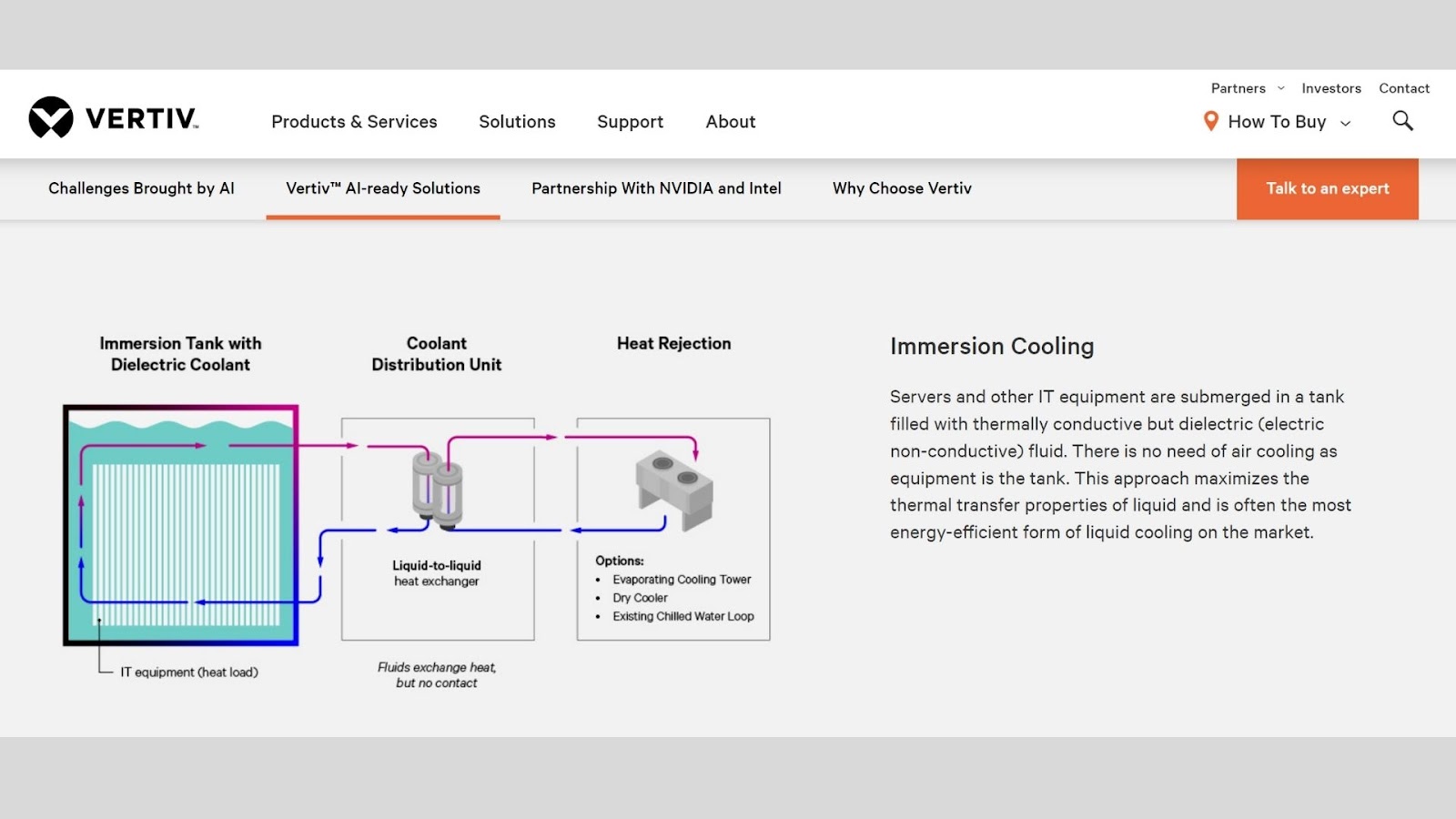

And second, as these giant rows of cabinets draw more power, Vertiv designs the systems to help keep them cool. Think of these cooling systems — and especially the liquid cooling systems (versus air cool, like the fan in your PC or laptop) — like a radiator for the engine of a car. Piping of cool liquid flows to the chip, absorbs heat, and is then carried away and dissipated.

This transition from air cooling to liquid cooling in data centers is having a sizable positive impact on performance, according to Nvidia. This explains why Vertiv made the acquisition of liquid cooling startup CoolTera in December 2023 (which is why there’s been a dip in Vertiv’s profitability, more on that later).

Vertiv’s profit margin, valuation, and potential risks with competitors

First, let’s address who your fellow shareholders would be, should you (or if you) buy Vertiv stock. Vertiv is primarily owned by institutions. There’s not much insider or C-suite ownership. That’s not much of a surprise, given this was an old business that used to be part of Emerson Electric.

Also, there’s only one share class (Class A shares). We’ll address what “warrants” are momentarily.

There are others besides Vertiv…

Ok, so the shareholder makeup checks out, but what about competition? As Jensen alluded to in the quote at the outset, Vertiv is but one Nvidia engineering partner for power and cooling. Vertiv itself acknowledges it competes against smaller businesses offering individual solutions, as well as big industrial and tech companies offering a full suite of solutions just like they do.

Given this situation, gross margins have been in a roughly mid-30% range, and operating margin at about a high-single-digit % range. Not great. No wonder Starboard Value wanted to shake things up. Vertiv has work to do to improve its profit profile (mid-teens % operating margin is really where this should be). Note, the recent dip in margins has to do with that CoolTera acquisition, which is still a startup and won’t begin meaningfully contributing until later years.

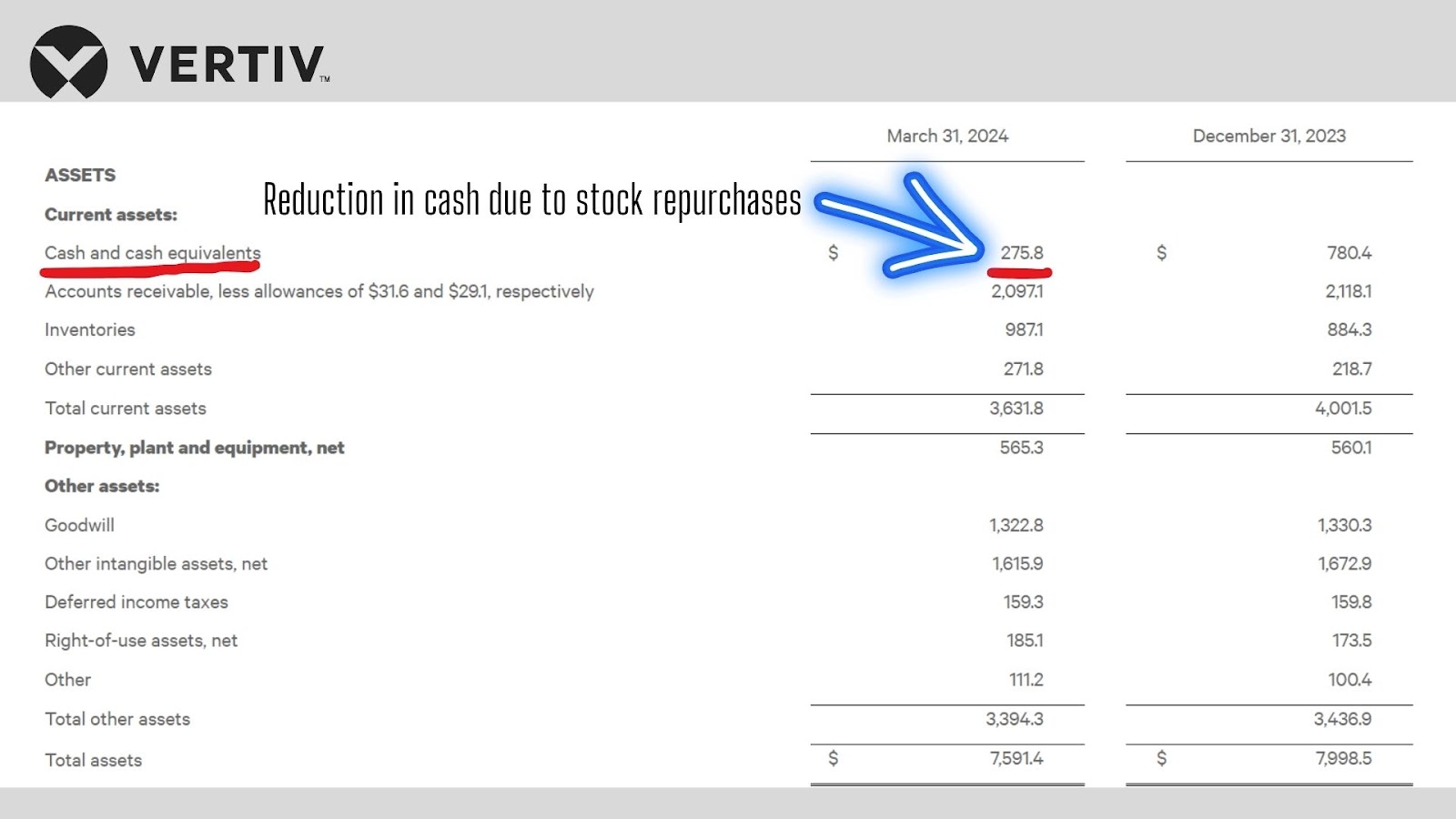

There are also balance sheet concerns. Vertiv is slim on cash and long on debt (the debt being a holdover “gift” from Emerson Electric and old private equity owners years ago).

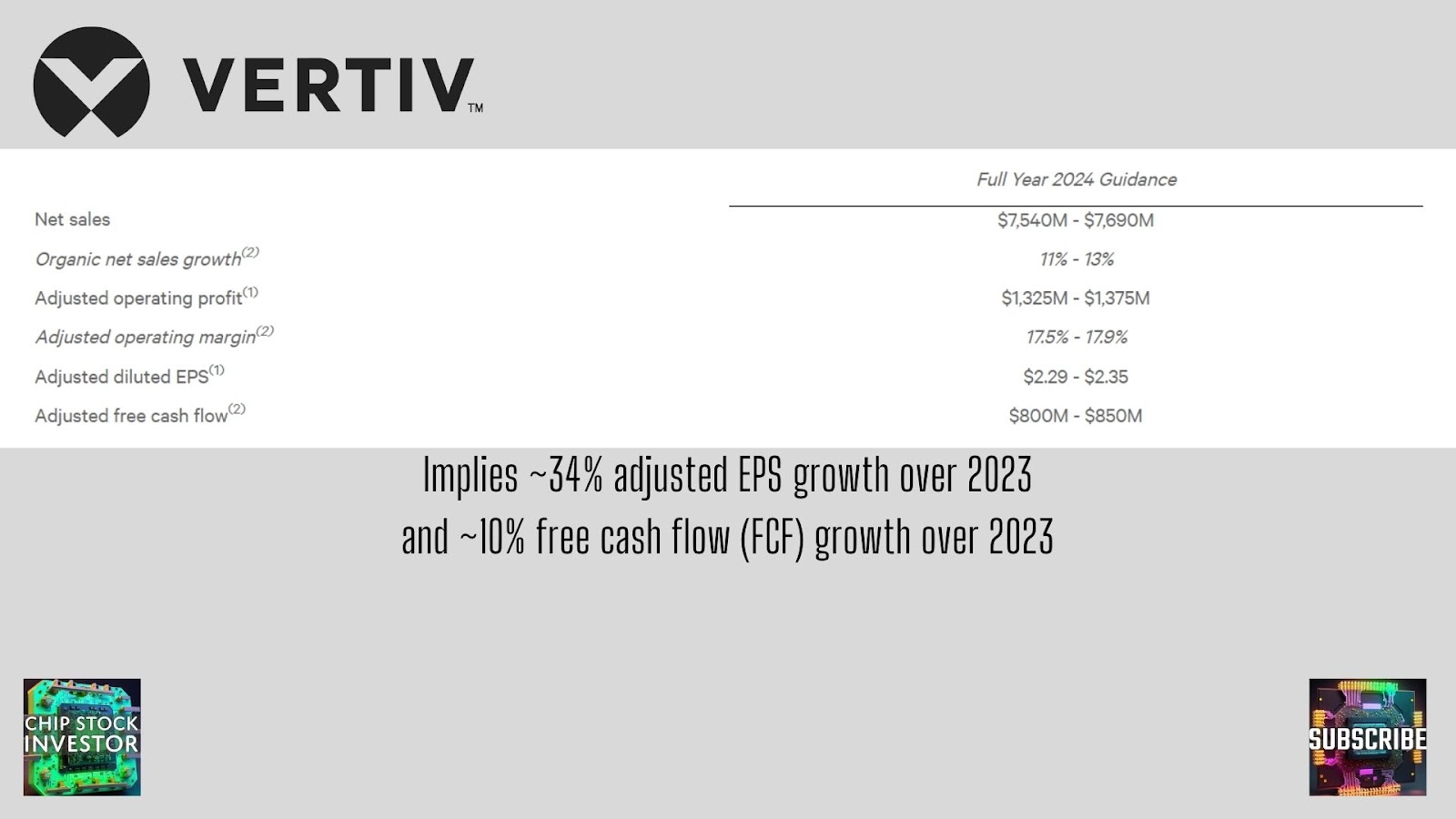

Rising revenue, rising margins… is it good enough?

The good news is Vertiv management is forecasting solid revenue growth (12% organic, excluding acquisition effects) for 2024. Earnings per share (EPS) are also on the rise, though free cash flow (FCF) looks a bit more lackluster for now. Perhaps that will pick up in subsequent years when new liquid cooling system designs start getting sold to Nvidia’s data center and AI customers.

Ok, about that Vertiv valuation

However, after more than doubling in price so far in 2024 alone, Vertiv stock trades for a hefty premium – even after factoring for a solid 2024 outlook.

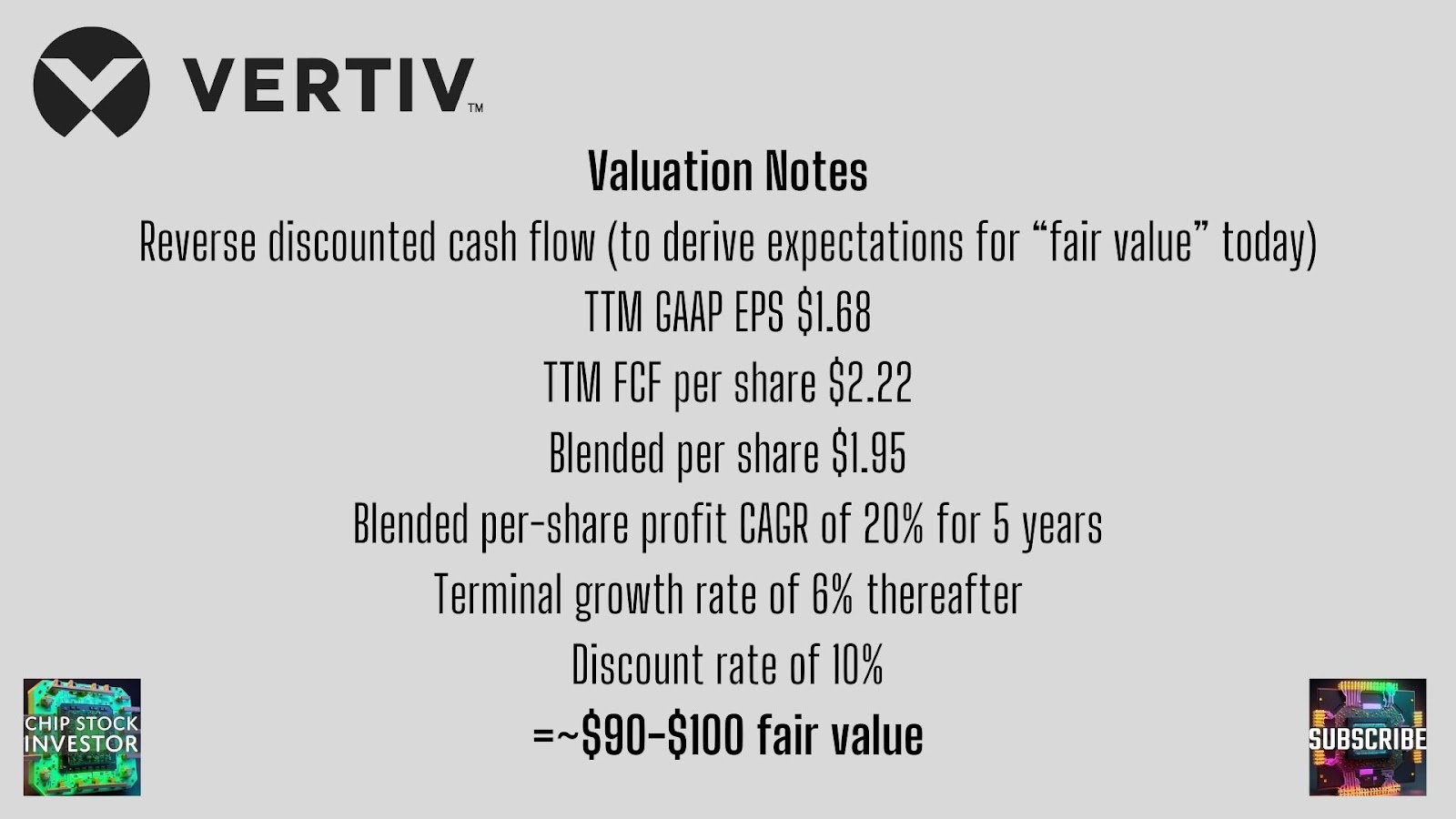

The growth and margin expansion story looks totally factored in, as far as we can tell. Using a simple reverse discounted cash flow (DCF) model to try and figure what Wall Street is expecting from Vertiv given the current valuation, we’d say a pretty high bar has been set.

In other words, when blending GAAP EPS and FCF, the market seems to be implying an average 20% per-share profit growth rate can be sustained for the next five years. For a big industrial engineering outfit like Vertiv, it doesn’t scream “great value” to us right now – even with power delivery and cooling expected to be a high-growth segment of the industry.

Chip Stock Investor’s final take on Vertiv

Much like Super Micro Computer, we took an early look at Vertiv stock and passed on making a buy. Such is life in 2024 with the AI supercycle. We’ve been “punished” for owning the stock up over 80% year-to-date (Nvidia), instead of its smaller ecosystem partners riding Nvidia’s coattails (Super Micro is up 170%+ so far in 2024, Vertiv up over 100%, as of mid-May).

That said, Vertiv doesn’t seem to provide a simple commoditized engineering service. It does have competitors, but it appears to be a focused bet on power delivery and cooling infrastructure. There’s enough to like with this one that we’ll continue to keep tabs on Vertiv Holdings. If the price (and growth outlook) ever align for us, perhaps we’d make a buy.

One Response

Thank you for the brake down of the company.