We’re continuing to parse through the extensive information from Nvidia‘s (NVDA) annual GTC event this week. On Tuesday, we wrote about how the acqui-hire of Groq in December could propel the company to a cumulative $1 trillion in revenue from 2025 to 2027.

In a follow-up Q&A, CEO Jensen Huang dropped another figure making its rounds in financial headlines: A target of 50% of free cash flow returned to shareholders

What does that actually mean for Nvidia shareholders? Let’s break down a few key pillars of the architect of AI’s shareholder return structure (dividends and stock repurchases).

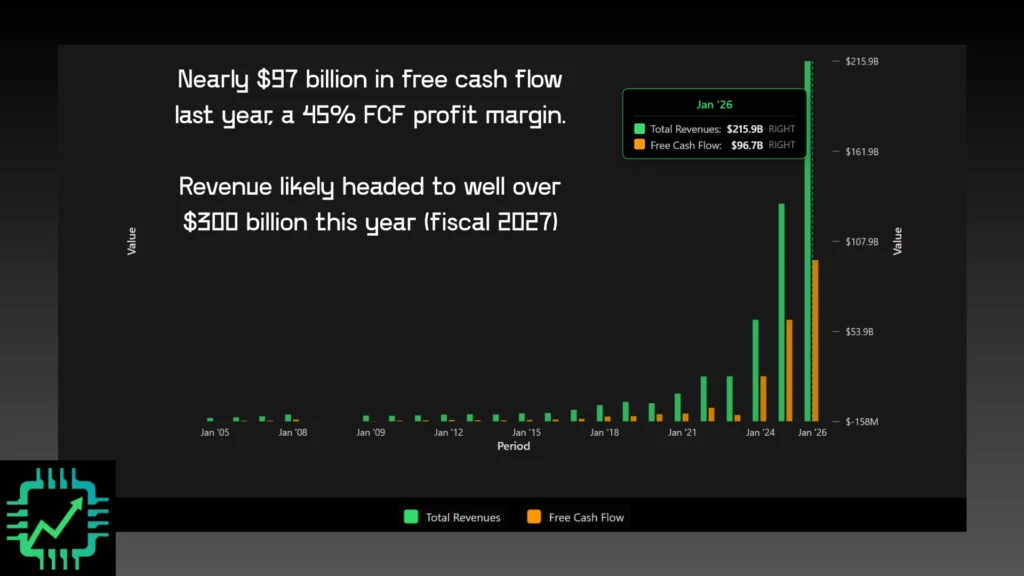

Nvidia’s free cash flow last year

In the last couple of articles, we discussed Nvidia’s $216 billion in revenue last year (fiscal 2026, the 12 month period that ended in January 2026) and its outlook for possibly well over $300 billion in revenue this year (fiscal 2027).

Starting with that base of $216 billion in sales last year, Nvidia was already at a whopping 45% free cash flow (FCF) profit margin, nearly $97 billion in FCF. And that is just a preview of coming attractions. If those margins hold in fiscal 2027 (the early outlook for Q1 indicates it will), Nvidia could be generating ~$150 billion in FCF.

We are building investing tools, powered by Fiscal.ai data, over on Semi Insider. Get access to those, all our research articles and slides, portfolio updates and thematic stock indices, and weekly live Q&A sessions! chipstockinvestor.com/pricing/

Shareholder returns already approaching 50%

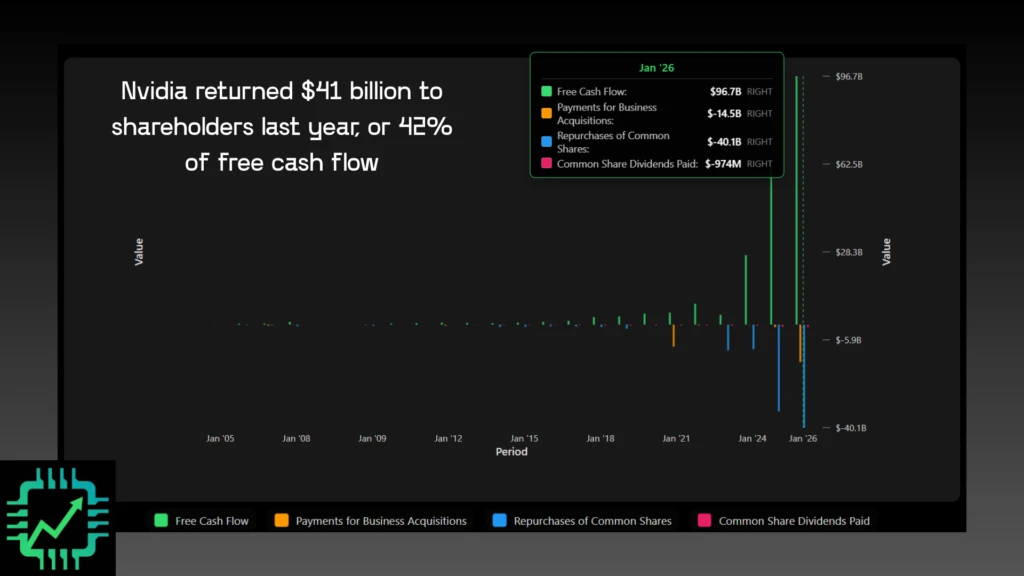

Now about the “50% of free cash flow returned to shareholders” comment. Jensen isn’t exactly making some outlandish, pie-in-the-sky prediction. In fact, NVDA has been pretty generous in returning that cash to shareholders in the form of share repurchases, which handily offsets share dilution from employee stock-based-compensation, and reduces share count (leaving more profit for remaining shares outstanding). Additionally, there’s a tip of the hat to those investors that still love dividends.

In total for fiscal 2026, stock repurchases were $40.1 billion and dividends paid $974 million. At $41 billion in total shareholder returns, that’s already a 42% shareholder return payout ratio (stock repurchases + dividends paid divided by FCF).

Nvidia is already well on its way to reaching that 50% of FCF return milestone.

The Nvidia balance sheet — another source of potential growth

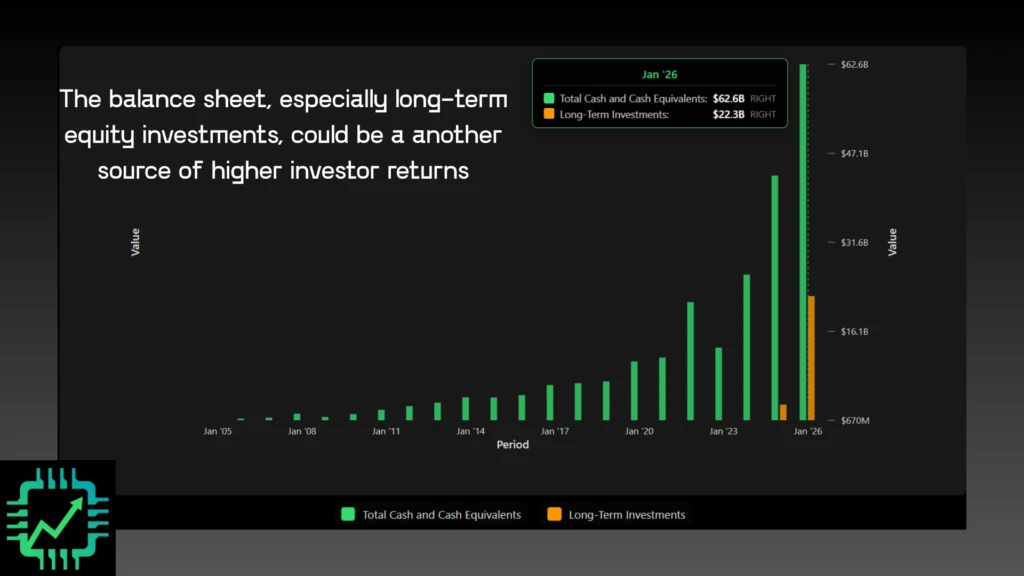

But what about the other half of FCF not being returned to shareholders? That’s where the balance sheet comes in.

First, left over cash after shareholder returns goes to cash on the balance sheet, which has begun to balloon the last couple years. Fiscal 2026 ended with $62.6 billion in cash and short-term investments on balance.

There’s more. Nvidia has also been a very active investor in leading AI companies, including some of its top customers. The term “circular relationship” got thrown around a lot in the last year regarding this practice (Nvidia buys stock/equity in a customer, and said customer uses the cash proceeds to buy Nvidia data center equipment). But this statement in our mind was a little (or a lot) over blown. Clearly $22.3 billion in long-term equity investments on balance at the end of fiscal 2026 isn’t responsible for $216 billion in annual revenue and counting.

Note: Those long-term investments listed above don’t include the $13 billion paid for the Groq licensing and acqui-hire (per the last 10-K annual report), since it wasn’t an outright acquisition or purchase of equity.

Nevertheless, we’ll acknowledge this investment practice is a risk. Equity investing (buying stock) is a highly variable asset purchase. “Stocks go up, and stocks go down.” Volatility, and especially the kind that leads to a decrease in equity value that doesn’t quickly recover (or worse, permanent loss of capital), is a risk factor.

However, if Nvidia’s investment strategy in emerging AI leaders and other strategic ecosystem partners is successful, this could be a large source of future shareholder growth as much as it could be a risk. At GTC, Nvidia said it will continue investing in equity in its AI ecosystem and partners, even as it ramps up shareholder returns too.

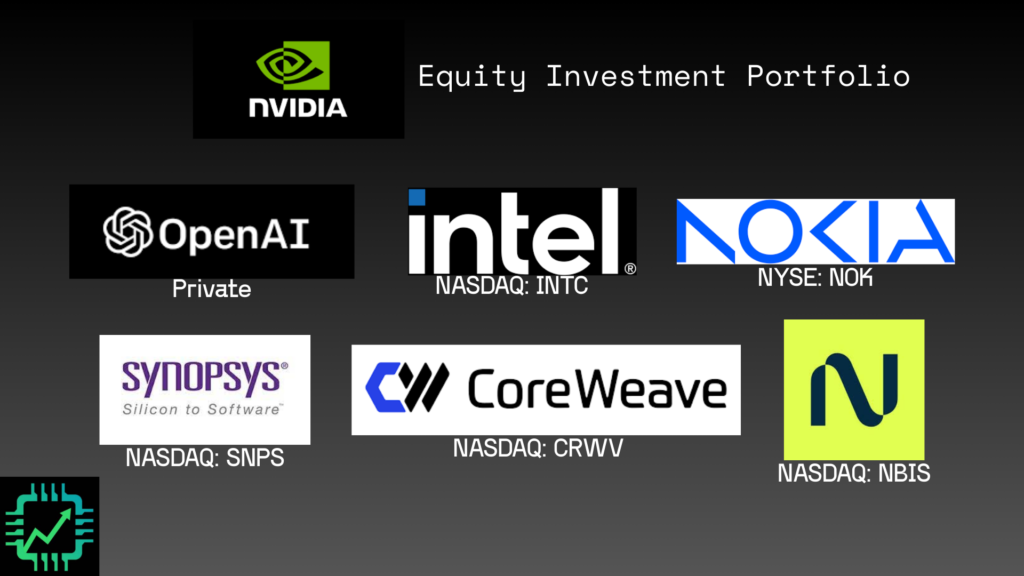

Listed below are some of the bigger companies that Nvidia has taken a vested interest in. Included below are the reported $30 billion that might get invested in OpenAI, and $2 billion invested in Nebius, announced subsequent to the end of fiscal 2026 (both should show up in the “long-term investments” line item in coming quarters).

- OpenAI – ~$30 billion, part of a larger funding round valuing OpenAI at $730 billion

- Intel (INTC) – $5 billion

- Nokia (NOK) – $1 billion

- Synopsys (SNPS) – $2 billion

- CoreWeave (CRWV) – additional $2 billion stake announced in January 2026

- Nebius (NBIS) – $2 billion

Long story short, Nvidia isn’t just a high-growth AI story anymore. For the collective investor community, the AI story — and especially the fast CapEx growth from the hyperscalers — is getting wearisome. But Nvidia is taking shareholder returns seriously and doling out a higher amount of cash via dividends and especially stock repurchases. Jensen is trying to win over support. In our estimate, drawing attention to this seems like the logical next step to do so.