A new competition is unfolding in the laptop arena. Apple (AAPL) unveiled its latest chip, the M3. Qualcomm (QCOM) is readying its Snapdragon X Elite, a rival to the dominant X86 processors, in mid-2024.

Before delving into the latest advancements, let’s take a quick trip down memory lane. Our previous videos on Moore’s Law (linked here in the video and description) provide a backdrop for understanding the evolution of microprocessors. These chips, like the CPUs in our laptops, are responsible for processing the ones and zeros that power our software. These binary codes are generated by the on-off switches, or transistors, on the chip’s surface.

As we explore Qualcomm and Apple’s new chips, you’ll often hear about the billions of transistors packed into each one. The magic happens through an Instruction Set Architecture (ISA), acting as an interface between the processor and the software it runs—our beloved apps on smartphones, laptops, and PCs. There are two main types of ISA: Complex Instruction Set Computer (CISC) and Reduced Instruction Set Computer (RISC), with the latter gaining prominence today, notably in ARM and RISC-V architectures.

Back in the 1970s, Intel introduced the X86, a CISC for microprocessors that became the industry standard for decades. Fast forward to the 1980s, and due to Intel’s monopoly, AMD became the second X86 provider, forming the X86 chip duopoly we have today. However, in 1990, Apple invested in ARM, a RISC company aiming for a simplified instruction set for energy-efficient yet powerful computing.

The energy efficiency of RISC, exemplified by ARM, played a pivotal role in the smartphone revolution initiated by Apple with the iPod and later the iPhone. But here’s the catch: CISC (X86) and RISC (ARM) architectures are not compatible. It’s like trying to combine Legos with knockoff Mega Blocks—they serve the same purpose but won’t fit together.

The question arises: why didn’t we adopt ARM from the beginning? The answer lies in the vast amount of software built on X86 architecture. Every Windows application, like Microsoft Word, is intricately tied to this foundation. Shifting to ARM would require extensive redevelopment to ensure compatibility. This legacy software is the stronghold of the X86 duopoly.

So, why did Apple, with its unique ecosystem, use X86 chips in MacBooks initially? The answer lies in the historical dominance of Intel’s chip empire. Only in 2012 did rumors emerge about Apple’s plans to develop its own PC processor, marking a potential exit from the Intel-dominated landscape—a move that has since reshaped the landscape of computer processors.

Fast forward to the last decade of events.

A Brief And Interesting History of Apple VS Qualcomm

You can see how it appears this showdown is between Apple and Qualcomm, and maybe to an extent it is. Competition means constant improvement in price-to-performance. Also notice both companies increasingly talking about AI capabilities – specifically, on-device AI inference. What’s going on here? Here’s my article on QCOM on-device AI early this year. https://www.fool.com/investing/2023/06/09/has-qualcomm-already-beaten-apple-to-the-punch-in/

They both want a cut of the next PC market growth cycle that’s just beginning. Apple is playing its own game and trying to tease early M1 MacBook adopters (and maybe holdouts still using their Macs with an Intel chip) to upgrade. And Qualcomm wants to finally get a good return on its long-suffering laptop development with Microsoft.

Apple’s Arm-based M-series chips have set off a new arms race (pun!). According to tech researcher IDC, Apple PC shipments in Q3 2023 were 10.6% of market share, down from 12.7% the year prior (it seems Apple market share peaked at about 13% to 14% during the last PC sales peak in early 2022). That compares to just 8.5% Apple market share in Q3 2020 and 7% in Q3 2019, before the M-series. Those M chips have done wonders for Apple’s MacBook lineup. https://www.businesswire.com/news/home/20201012005711/en/Traditional-PC-Market-Delivers-Another-Quarter-of-Double-Digit-Growth-in-Q3-2020-According-to-IDC https://www.idc.com/getdoc.jsp?containerId=prUS51295423

Data source: Apple. https://www.apple.com/newsroom/pdfs/fy2023-q4/FY23_Q4_Consolidated_Financial_Statements.pdf https://www.apple.com/newsroom/pdfs/FY22_Q4_Consolidated_Financial_Statements.pdf https://www.apple.com/newsroom/pdfs/FY21_Q4_Consolidated_Financial_Statements.pdf https://s2.q4cdn.com/470004039/files/doc_financials/2020/q4/FY20_Q4_Consolidated_Financial_Statements.pdf https://s2.q4cdn.com/470004039/files/doc_financials/2019/q4/Q4-FY19-Consolidated-Financial-Statements.pdf

Here’s what they want a piece of:

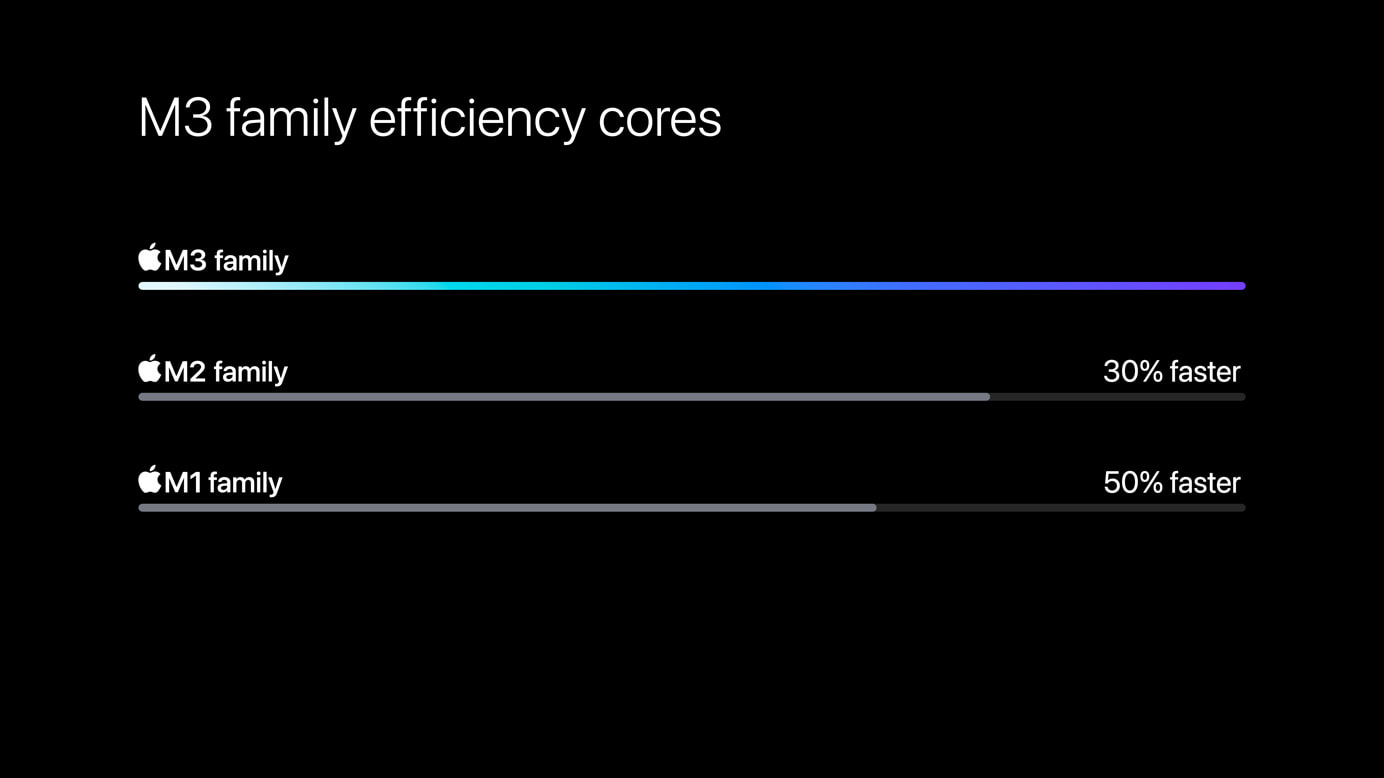

So what are the comps on Apple M3 vs. Snapdragon X Elite? We don’t know all the details yet. We’ll need to wait for benchmark tests once they’re available to the tech community to suss out IN THE REAL WORLD, especially the Qualcomm-powered laptops. But here’s what we know so far.

Qualcomm has attracted a number of OEMs, a few of them (like HP and Lenovo) making appearances at the Snapdragon Summit: Acer, Asus, Dell, Honor (Chinese smartphone company entering the PC space), HP, Lenovo, the Microsoft Surface brand, Samsung, and Xiaomi.

This is clearly the point in the PC upgrade cycle where media hype takes over as everyone jockeys for market share. The problem for Qualcomm is it’s arriving late once again. Devices with these chips won’t arrive until “mid-2024,” according to Qualcomm. That could mean June, but many PCs may not come until next autumn. That gives everyone, including Intel and AMD, time to dish out their own chip refreshes.

However, Qualcomm has the most to gain, and little to lose. And it still trades at fairly depressed valuations. Any pickup in PC chip sales could go a long way to boost profit margins and fuel the dividend and buybacks (which was always our main investment thesis).

And for what its worth, Qualcomm is also signaling a big uptick in sequential revenue too, just like Intel and AMD: $9.1 to $9.9 billion revenue to close out the 2023 calendar year, up from $8.6 billion last quarter.

Qualcomm trades for just 14 times TTM free cash flow. Apple trades for 29 times TTM free cash flow. If you’re looking for a value stock as a new consumer tech upgrade cycle possibly heats up, Qualcomm looks to us as the clear winner, even if its entrance into the PC world is flawed.