A few of you have been with us since before Chip Stock Investor was a thing. And so maybe you recall our bearish call in 2023, once in June and the next in December. Both calls, as it so happens, called the top in Symbotic (SYM). A couple of those articles are still floating around on the web – but essentially the same potential shareholder issues exist today as did two years prior.

Below is a high-level look at where SYM is today, still championed by some investors as a robotics pure-play that is worth paying attention to. And maybe it is. We’ve highlighted two very relevant issues, though, that we’ll come back to shortly, that we want you to bookmark in your head. Also note, the weird looking stock chart prior to summer 2022 is because Symbotic was brought public via SPAC. And without further ado, let’s discuss SYM’s investor proposition.

Check out Fiscal.ai/csi to get 15% off your own subscription so you can start visualizing business fundamentals too!

What does Symbotic do?

SYM is an infrastructure company. They make autonomous vehicle robots (SymBots, cute) and warehouse conveyor systems that help with order fulfillment automation. There is a software component to this, obviously, but SYM primarily makes revenue by selling the hardware-based systems – especially to key customer (and shareholder) Walmart (WMT).

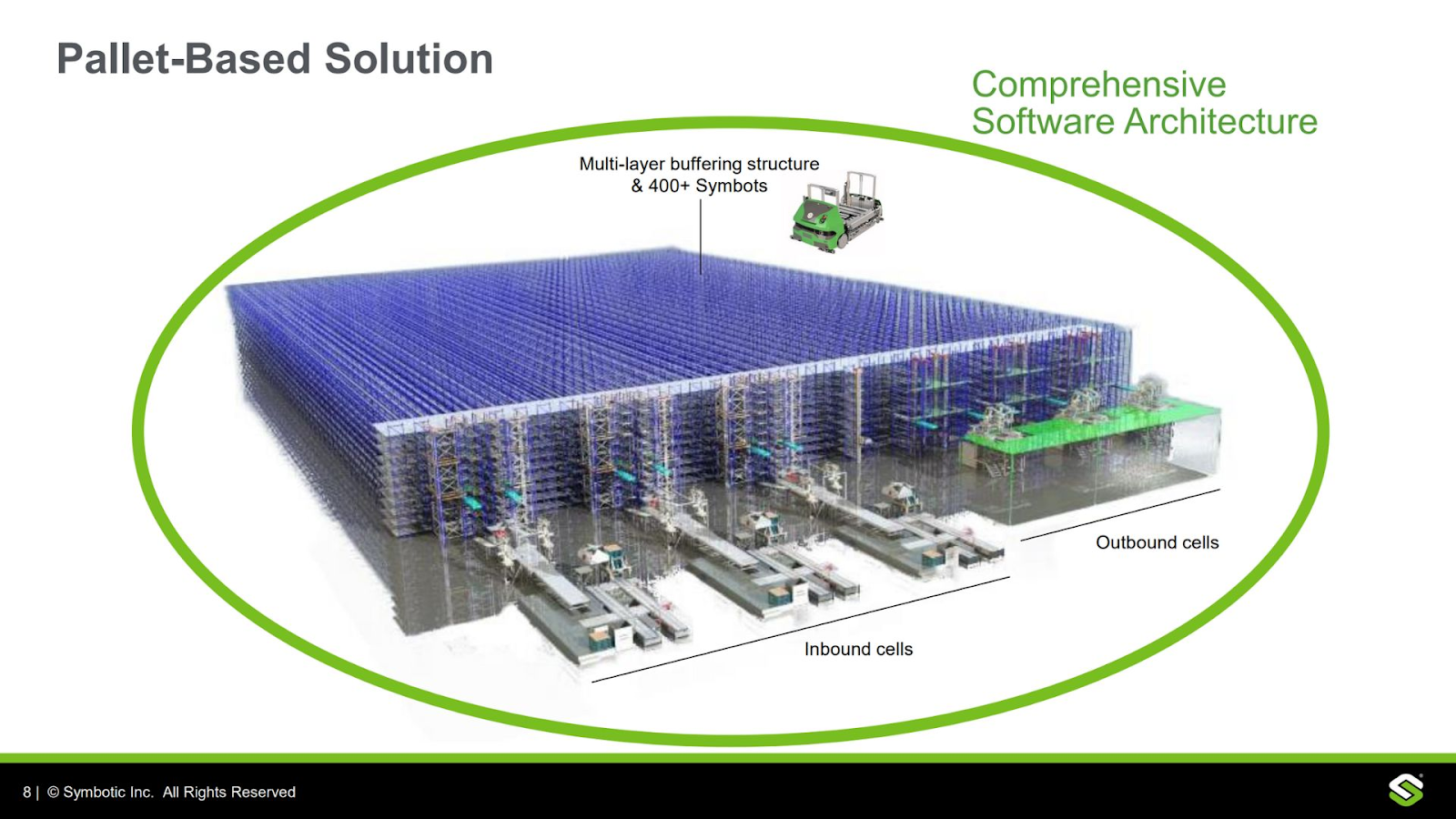

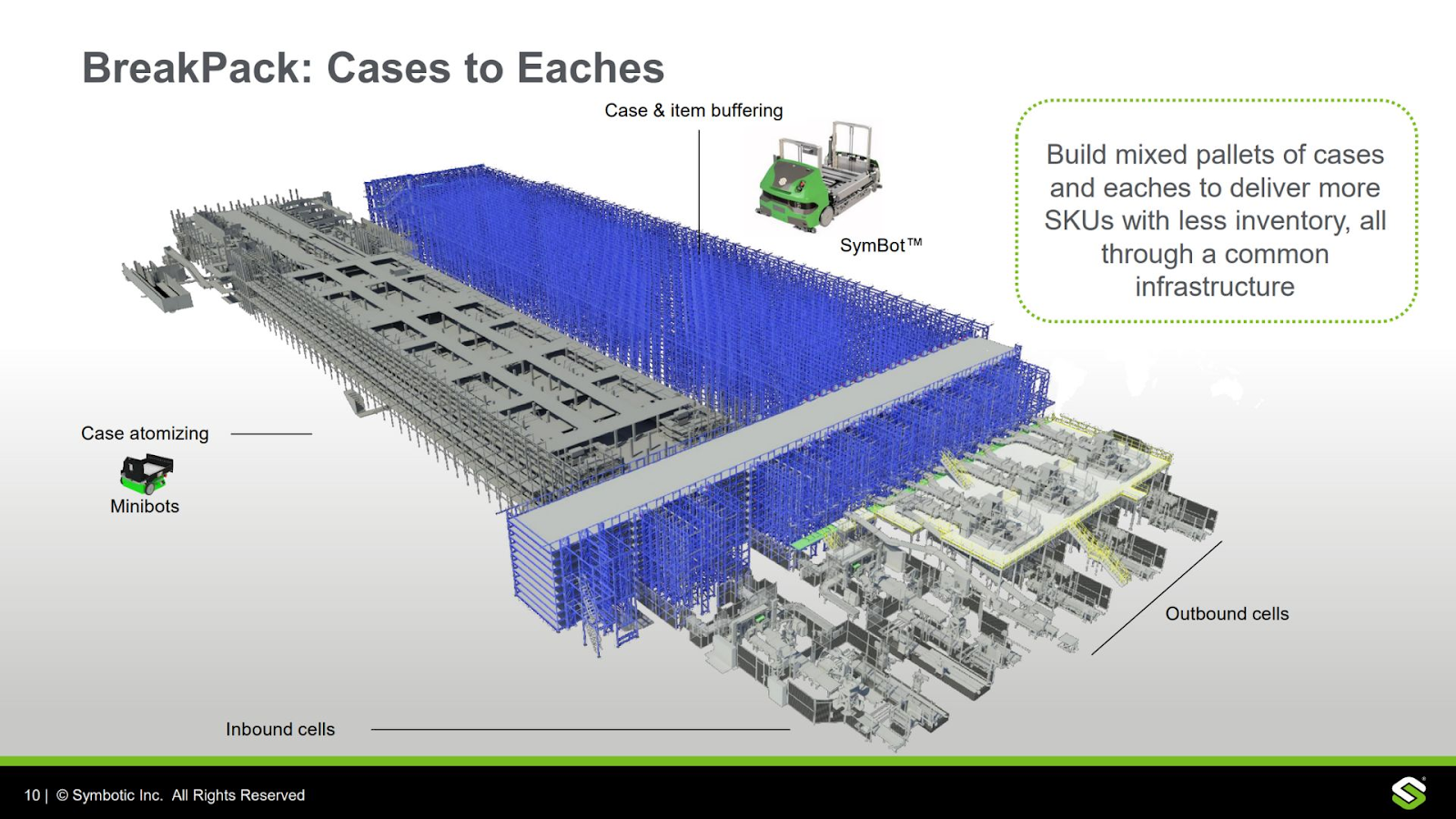

SYM has been at R&D in this field for a while, especially prior to its incarnation as “Symbotic” with founder Richard B. Cohen’s work leading his family’s wholesale grocery chain C&S Grocers (predominantly east coast U.S.). First, there’s an intake system for pallets, equipment to sort and dismantle, and organize the products that are unpacked.

Those products can be further organized into smaller packages and “eaches” for outbound delivery.

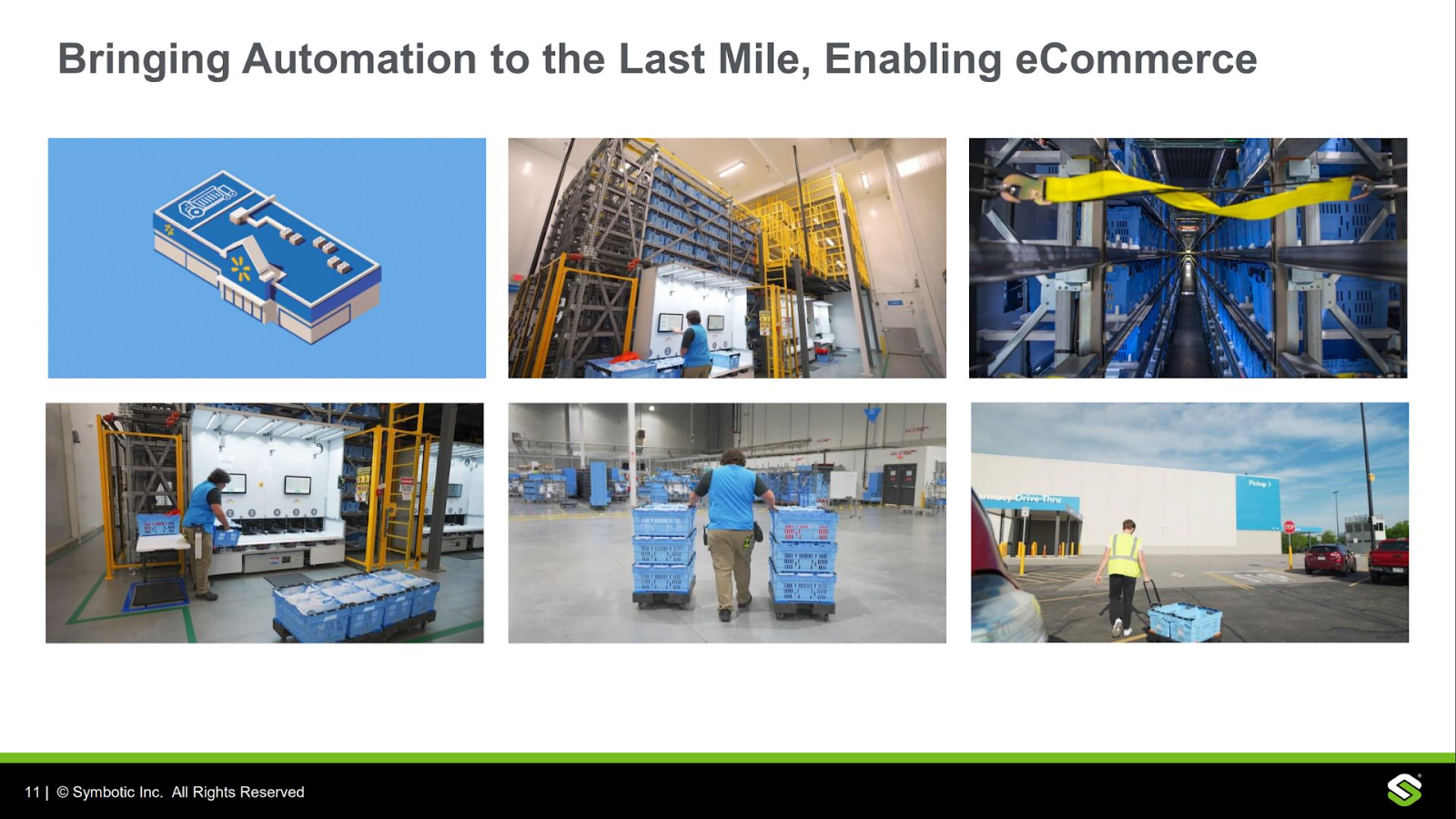

One key use is for Walmart’s e-comm order pickup system. If you live in N. America and have placed orders for pick-up, the below picture may look familiar to you. Basically, SYM helps build the back-end so Walmart’s order fulfillment to you is more efficient than a worker roaming the store or warehouse filling the cart on your behalf. What you see when you pull up to the curb is a Walmart associate pulling a blue cart with your order to your car.

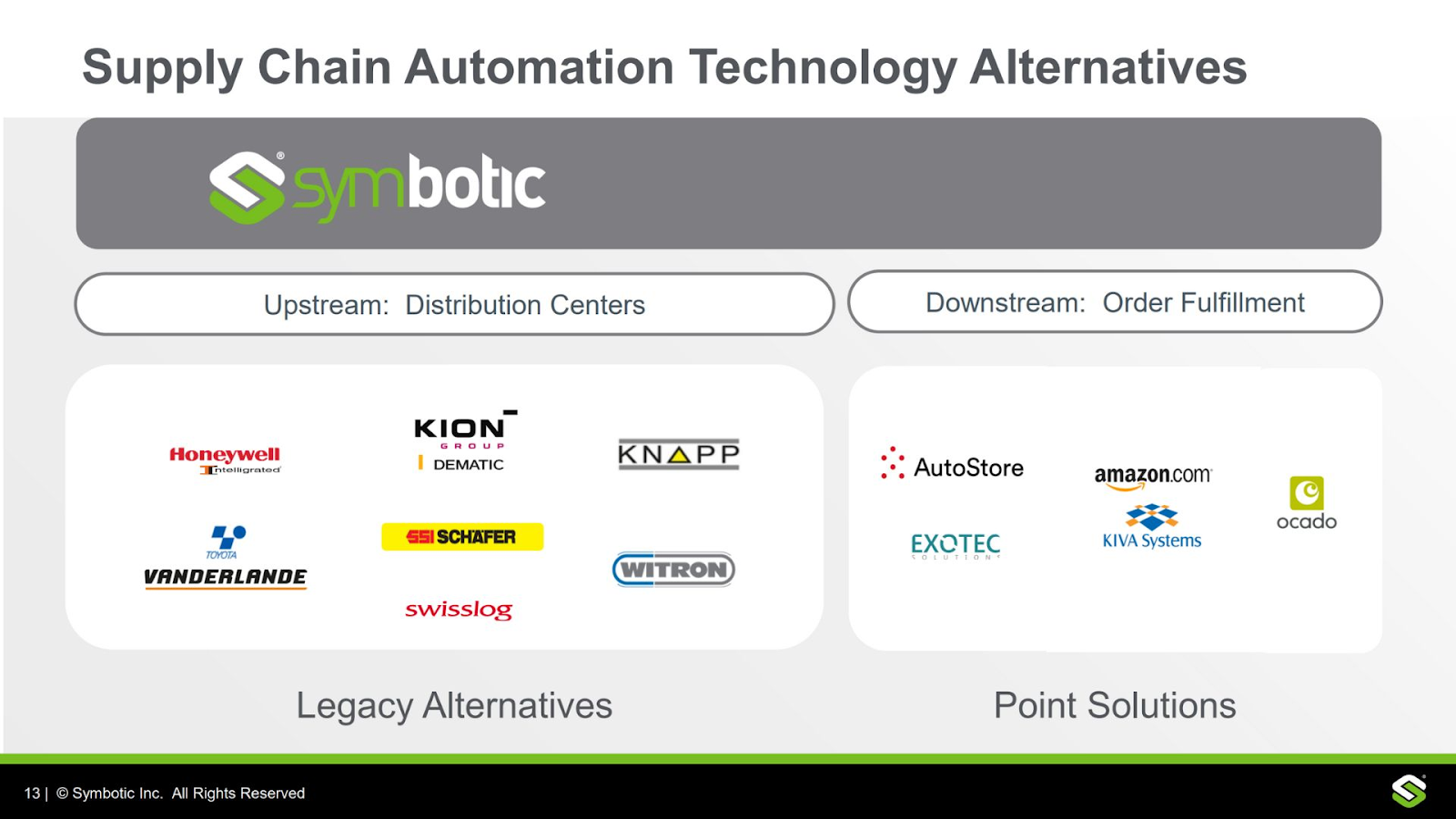

Here are the competitors SYM lists in its presentation. Amazon (AMZN) has its own in-house robotics system to automate its massive e-comm fulfillment empire. SYM’s pitch is its more modern and comprehensive, and offers (or would like to offer) its systems to other customers (Amazon is proprietary).

Besides Walmart, here are SYM’s primary customers. Earmark this as well, we’ll come back to it in a moment. But do bear in mind that one customer, GreenBox (GB), isn’t just a customer. It’s minority owned by Symbotic and majority owned by Softbank Group, and also sort of competes with SYM as well.

How does Symbotic make money? Primarily, it sells those warehouse systems and robots, and gets to realize the revenue (deferred revenue sits on the balance sheet as a liability during that time). Add in some annual recurring software use as well, plus some parts and system service.

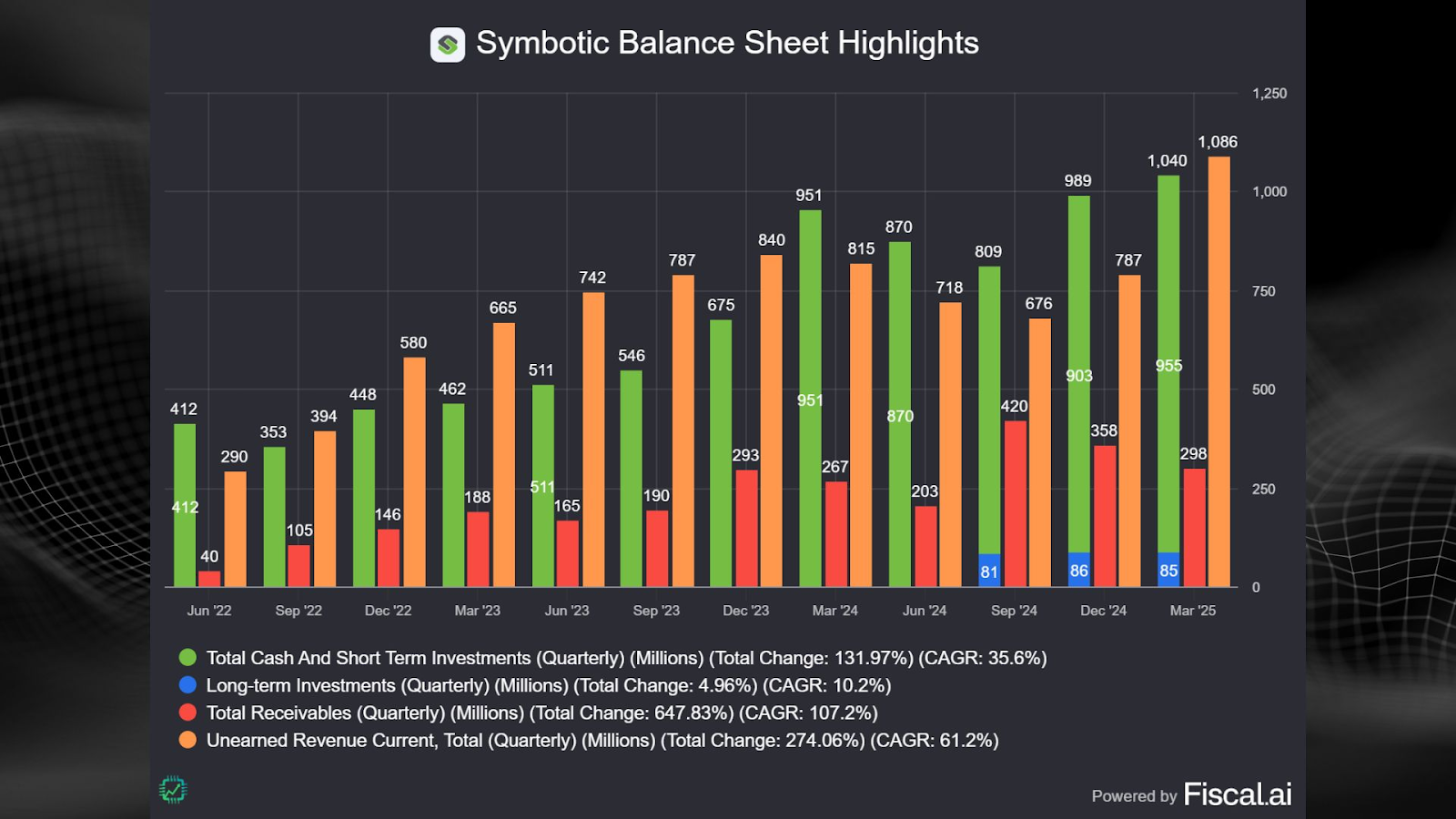

Below is the balance sheet, featuring cash and no debt. But also, we’ve listed the “unearned revenue” on the liabilities part of the balance sheet that SYM realizes over the course of two years after the initial customer deal (big orange bar). We also added in customer receivables, revenue invoiced but hasn’t been paid yet by the customer.

Your immediate takeaway from this alone is SYM is indeed a cyclical hardware-based business model. And it’s in the midst of a growth cycle, owing to the large growth in the orange “unearned revenue” item sitting on the balance sheet – predominantly from contracts with Walmart.

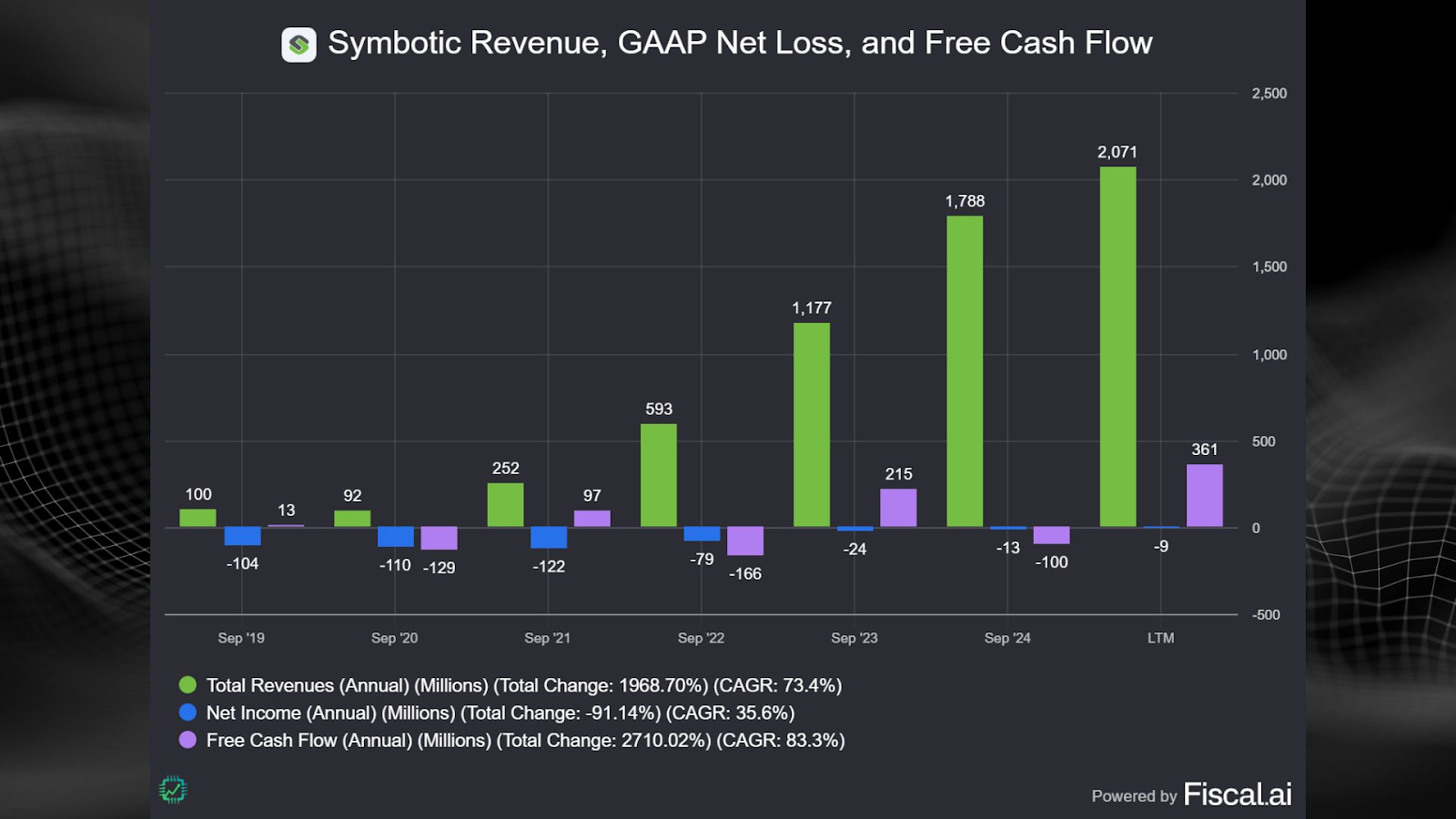

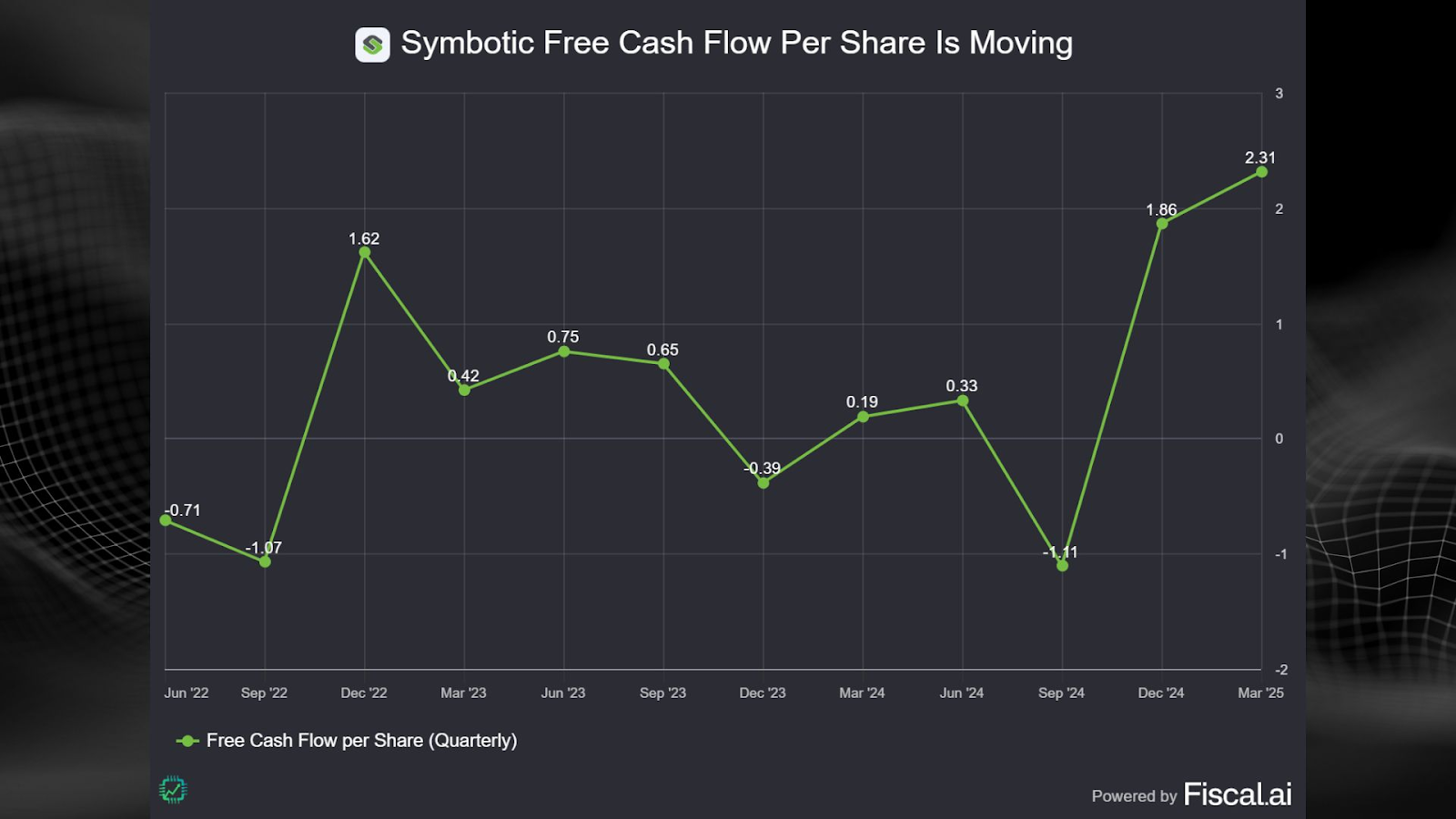

The deals are lumpy and come in waves, but owing to SYM’s two-year revenue realization methodology (deal inked, system installed, and revenue earned via use of the system for the next two years), the revenue has been smooth up-and-to-the-right. However, the free cash flow (FCF) cycle is where the lumpiness is captured. See the negative FCF in fiscal 2023 as SYM was ramping up building a deploying a new batch of systems?

All of that is fine and well. We understand what SYM does, we know Walmart is a real-life customer, and SYM is growing and scaling up its profitability (both FCF and narrowing the gap towards GAAP net profit). So far, all checks are green.

Digging a bit deeper into those customer relationships

First yellow flag is customer concentration, which has been the case for SYM since the beginning of its journey as a publicly-traded company. Walmart accounts for nearly all of the current revenue, and will remain that way for the foreseeable future. In fact, 87% of revenue was Walmart in fiscal 2024.

Walmart also sold its own robotics system business to SYM in January 2025. Vendor consolidation favoring SYM, awesome. But why is Walmart outsourcing this robotics thing? Could be simple asset allocation for the behemoth that is Walmart. Or it could be limited ability to scale, an ability SYM might have. https://ir.symbotic.com/news-releases/news-release-details/symbotic-completes-acquisition-walmarts-advanced-systems-and

But then again, if you’re a prospective e-comm customer, would you really want to open up your warehouse to SYM knowing that they’re tied so closely to one of your biggest rivals? Maybe, maybe not. But as an investor, it’s worth putting on your C-suite hat and thinking about.

Nevertheless, customer concentration of this magnitude is a risk even SYM prominently calls out in its annual report.

Most of the other SYM customers – especially C&S Grocers and GreenBox – are actually affiliates. And so is Walmart for that matter, as it also is a large investor in SYM (as is SoftBank). In other words, conflicts of interest abound for SYM stock shareholders. Let’s dive deeper still.

A conflicted shareholder structure

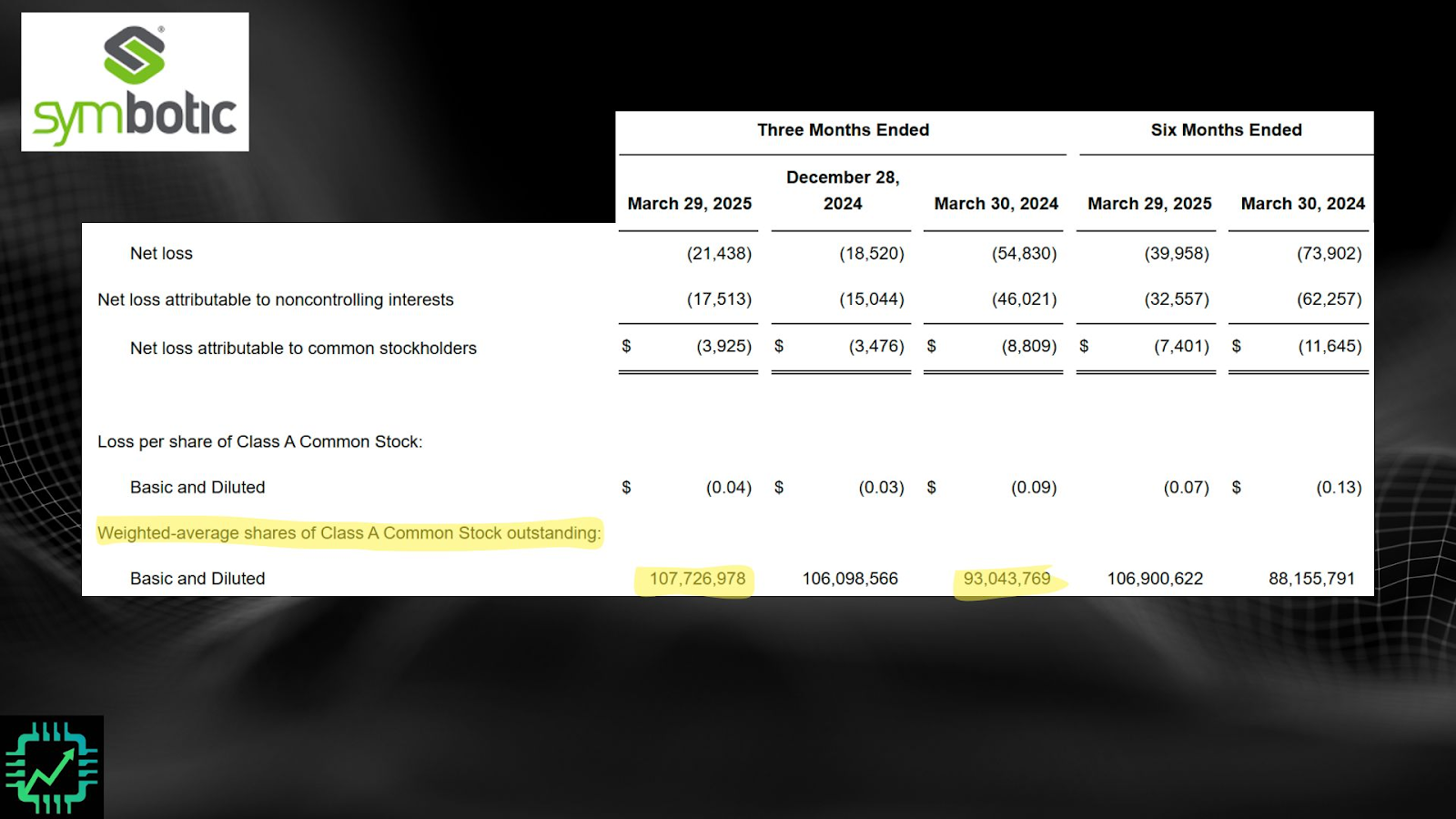

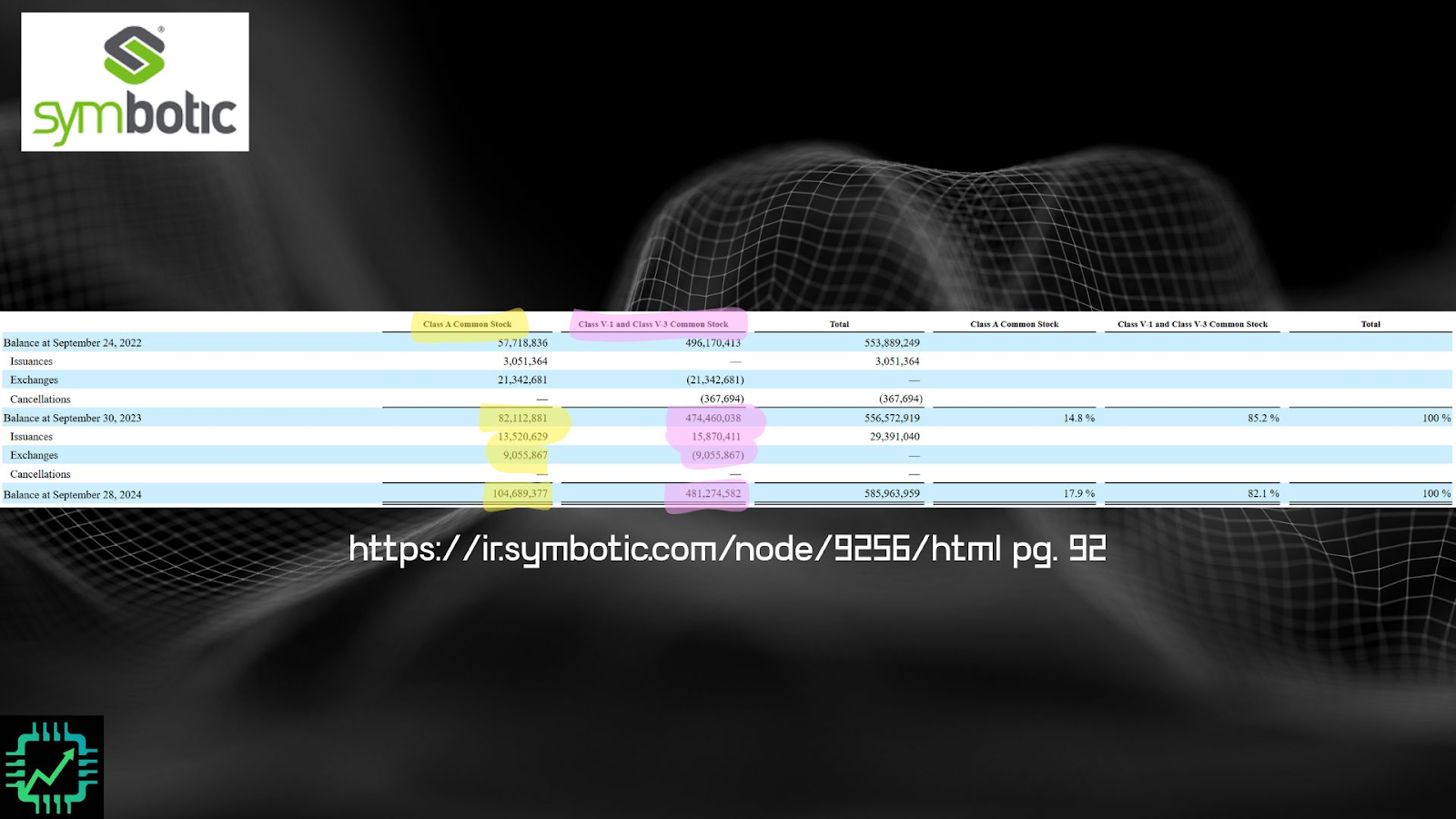

Take a look at the SYM share count from the last earnings report (Q2 fiscal 2025). Talk about dilution. What happened?

This is where the importance of shareholder structure comes in, and understanding (or trying to understand) how a company’s management team is incentivized to play on the same team as YOU THE PUBLIC EQUITY SHAREHOLDER.

Same as a couple years ago, SYM has a convoluted share structure including class A stock (shares available to you to potentially buy), and class V-1 and V-3 stock. Class V-1 is for some of the big investors in SYM (Walmart and SoftBank), and V-3 is for Richard Cohen and family. Both classes can convert to class A over time, but in the meantime due to voting structure, the Cohen family retains close to 90% voting power over SYM.

And because the Cohen family and other members of the SYM C-suite also manage and own privately held C&S Grocer, SYM is almost like a subsidiary of the grocery chain. Lots of stock-based comp has been shelled out benefiting this convoluted shareholder structure.

The story otherwise looks good, though

Yes, SYM is a growing business, and profitability is scaling. And the stock is heating up again as a result. This could be a great trade. But for long-term ownership, the yellow flags are notable.

The FCF-per-share story could also heat up as more of SYM’s unearned revenue becomes earned and flows to the bottom line during this cycle.

But let’s finish off with the first slide we started with, the one with the highlights we asked you to remember. See how SYM seemingly has a less than $3 billion enterprise value (market cap minus net cash on balance)? It doesn’t. Why not? We need to add in all the V-1 and V-3 class of stock, which is MOST OF THE SHARE COUNT. When we do, SYM’s enterprise value is in all reality more like $18 billion! This was the same issue as in 2023 that we called out.

As a result, SYM trades for more like 50x trailing-12-month FCF. It isn’t cheap. But yes, the company is growing fast in this cycle owing to the close Walmart relationship, and that story could have fresh legs under it. Just know what you’re buying, and the potential potholes down the road, before you jump aboard the SYM train.

For the full story and more discussion on Symbotic and other robotics stocks, see you over on Semiconductor Insider! chipstockinvestor.com/membership