The term “TechBio” has been coined in recent years. It represents a fundamental shift in how we approach medicine—moving away from traditional biology and toward a data-driven, engineering-first mindset. One of the companies that is interested in leading this charge is Tempus AI (TEM).

Tempus has been a “hot button” stock for a while, particularly because it caught the eye of high-profile growth investors like Cathie Wood’s ARK Investment Management. But now that the initial IPO shine has worn off, it is time to look under the hood. Is this just another cash-burning hype machine, or is Tempus AI actually building the infrastructure for the future of precision medicine?

To understand the opportunity, you first have to understand the massive problem they are trying to solve: Healthcare data is a disaster.

The Origin Story: Personal Frustration Meets Big Tech

In the United States, medical records are siloes. Data lives in disconnected patient charts, dusty hospital basements, and incompatible electronic health record (EHR) systems. This fragmentation makes “precision medicine”—treatments tailored to a patient’s specific genetic and environmental makeup—incredibly difficult.

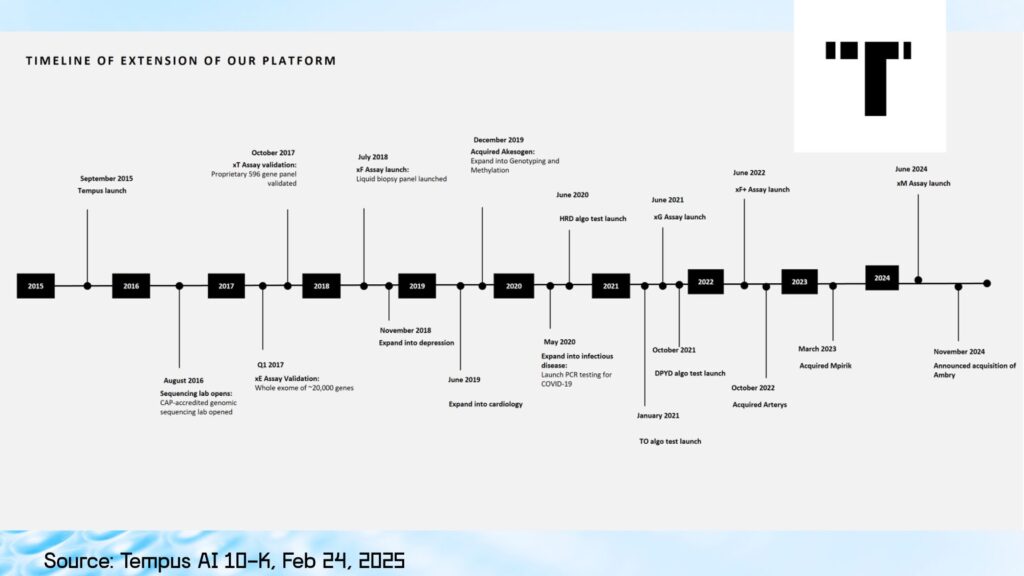

Enter Eric Lefkofsky. Best known as the founder of Groupon, Lefkofsky is a serial tech entrepreneur, not a biologist. He founded Tempus in 2015 out of personal necessity and frustration. After his wife was diagnosed with cancer, he was baffled to find that her treatment wasn’t being driven by data. He couldn’t understand why oncology didn’t function like modern tech, where data drives every decision.

So, he built Tempus with a singular mission: to ingest the world’s healthcare data, structure it, and use AI to make it useful.

The Core Strategy: Ingest and Generate

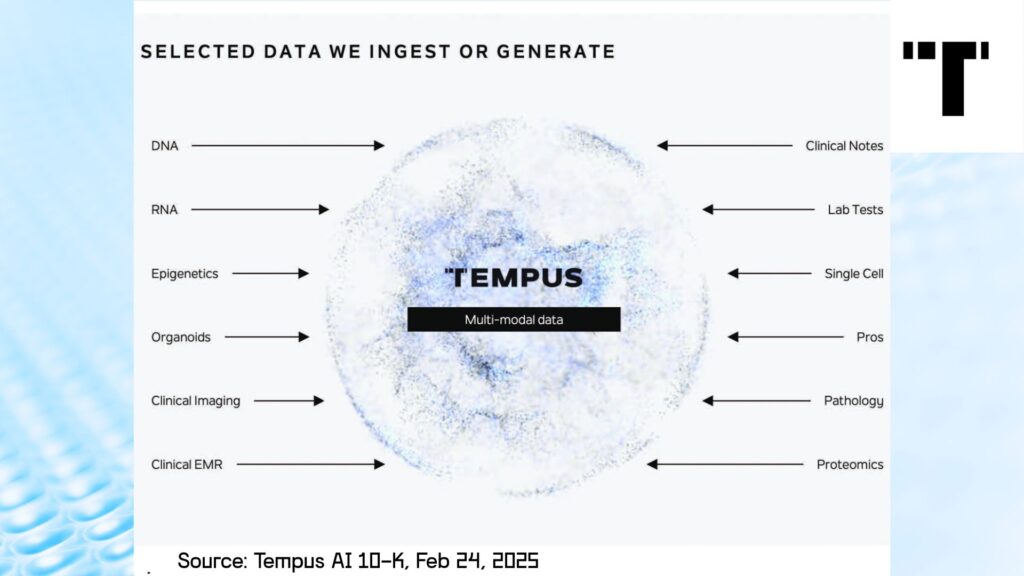

Tempus AI isn’t just a software company, and it isn’t just a lab. It is a hybrid engine designed to build what they claim is one of the largest proprietary datasets in the world.

Their strategy is two-pronged: ingest or generate.

- Ingest: They pull in clinical data from partnerships, licensing, and acquisitions.

- Generate: They run their own sequencing labs that create new molecular data every day.

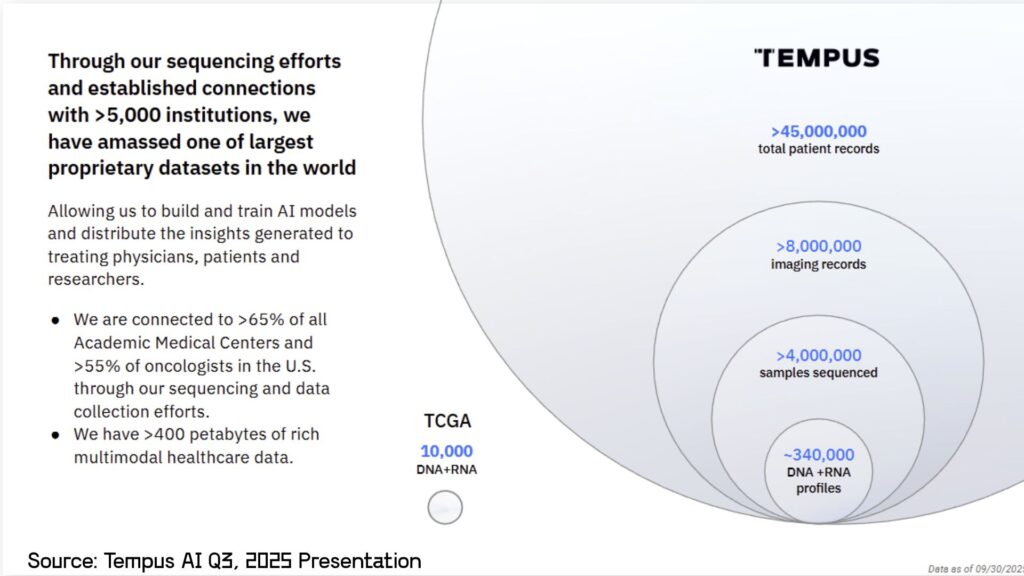

According to their latest filings, Tempus has amassed:

- 45+ Million total patient records.

- 400+ Petabytes of rich multimodal data.

- Connections to over 65% of all Academic Medical Centers in the U.S..

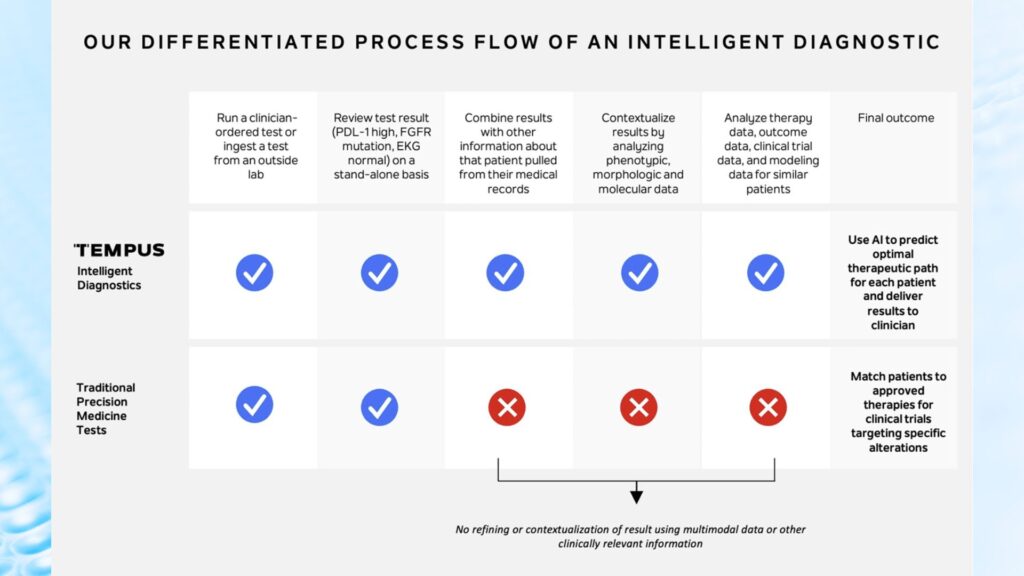

This massive data lake allows them to train AI models that can try to predict how a specific patient will respond to a specific treatment, creating what they call “Intelligent Diagnostics”. And the many connections made with academic centers and physicians can help match patients with treatment trials.

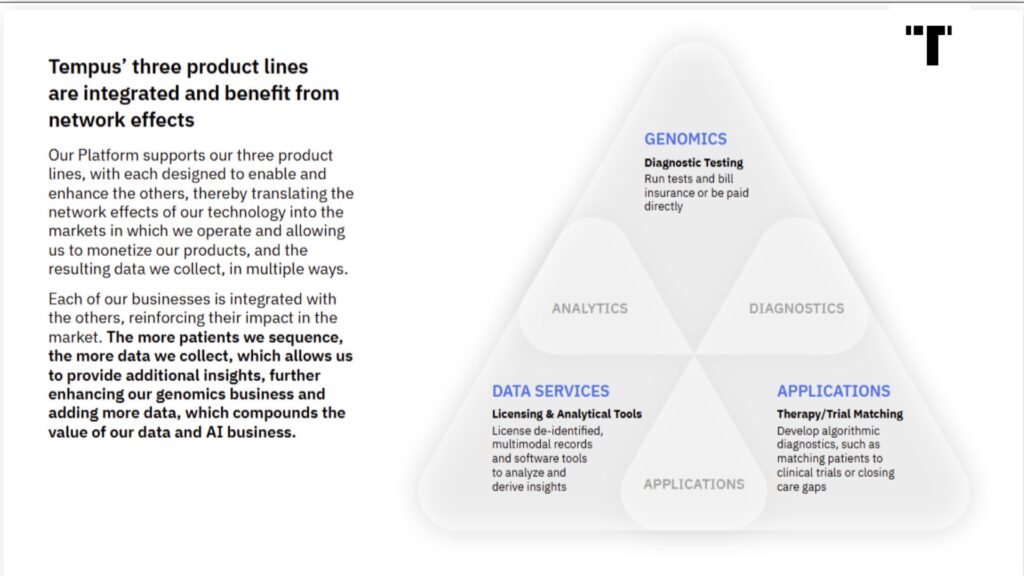

The Three Pillars of Revenue

Tempus monetizes this data engine through three distinct but interconnected business segments.

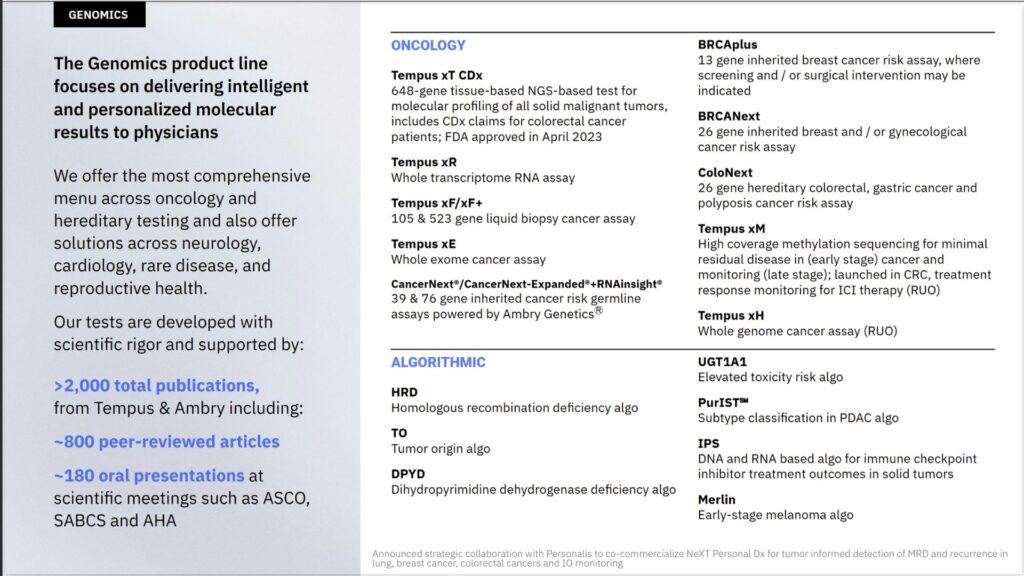

1. Genomics

This is the “hardware” side of the business. Tempus runs genomic sequencing tests—primarily for oncology (cancer)—for physicians and hospitals. Doctors send samples to Tempus, Tempus sequences them using tests like their xT CDx (a 648-gene panel), and provides a report.

This segment is growing rapidly, clocking $252.88 million in revenue recently, up significantly from previous years. Every test run in their labs adds more data to their proprietary database, making their AI smarter. Theoretically, this is a flywheel: more tests mean better data; better data means better insights; better insights lead to more tests.

They have also aggressively expanded this capability through M&A. The recent acquisition of Ambry Genetics expanded their testing menu beyond cancer into hereditary screening, pediatrics, cardiology and rare diseases.

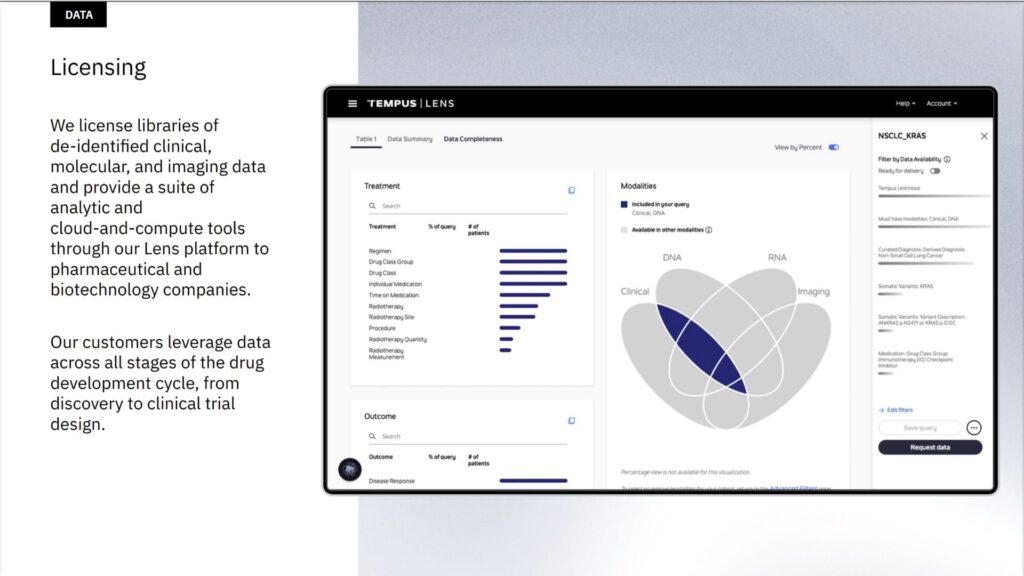

2. Data and Services

Tempus takes the massive amount of data they generate, “de-identifies” it (strips out personal info), and licenses it to pharmaceutical and biotechnology companies.

Why would pharma companies pay for this? Because drug development is expensive and prone to failure. By subscribing to the Tempus “Lens” platform, researchers can access real-world data to design better clinical trials, find new drug targets, and understand why certain drugs fail.

Think of this like the ARM or Synopsys model of biology. Just as chip designers buy IP from ARM to build processors, drug developers buy data insights from Tempus to build drugs. This is high-margin, scalable revenue that leverages work Tempus has already done in the lab.

3. AI applications

The third pillar is where the “AI” in Tempus AI truly lives. This segment focuses on algorithmic diagnostics and software. Their flagship product here is Next, an AI platform that layers onto routine care to identify “care gaps”.

For example, the AI might scan a patient’s records and flag that they are eligible for a specific clinical trial or that they missed a critical heart screening. This connects patients to trials (a service Tempus gets paid for) and (hopefully) improves outcomes. They are expanding this rapidly beyond cancer into cardiology (via the acquisition of Mpirik) and digital pathology (via the acquisition of Paige.ai).

The Financial Reality: Hyper-Growth vs. Cash Burn

The narrative is exciting, but the financials show a company in the messy middle of scaling.

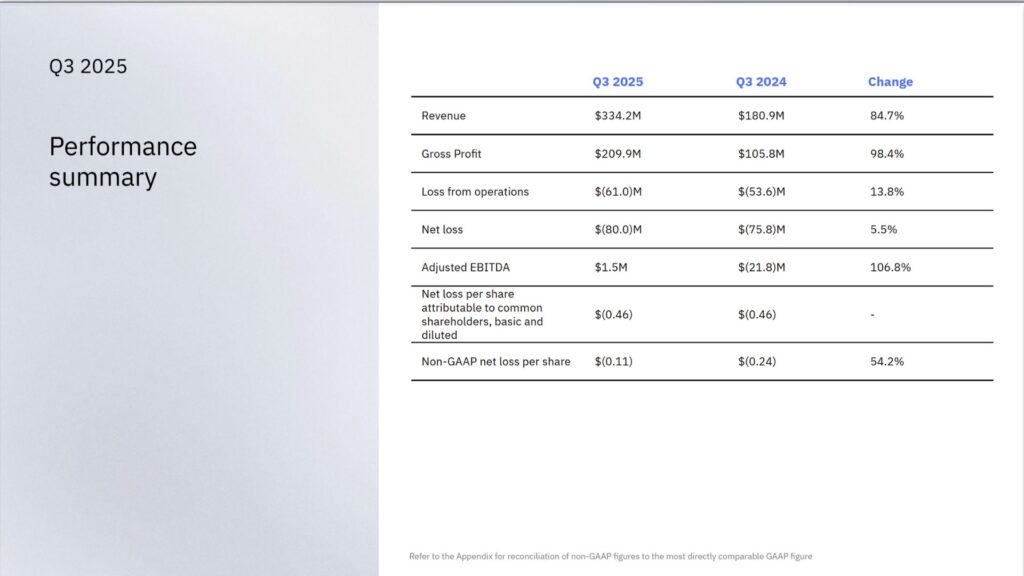

- Revenue is exploding: In Q3 2025, Tempus reported $334.2 million in revenue, an impressive 85% year-over-year increase.

- Profitability is close(r): They posted a positive Adjusted EBITDA of $1.5 million in the recent quarter. It’s a small number, but it proves the core business can generate cash.

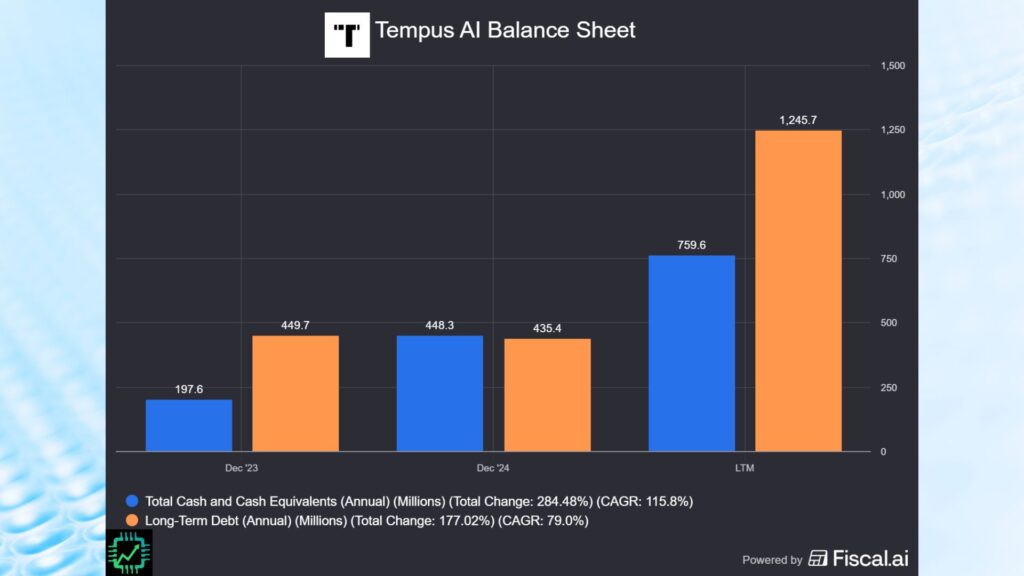

- The debt load: To fuel this growth and buy companies like Ambry, Tempus has taken on significant leverage. They currently sit on $1.25 billion in long-term debt.

- Cash Burn: Despite positive EBITDA, the company is still burning cash—reporting negative free cash flow of $127 million in Q3 2025.

Tempus is a classic “prove it” story. They have a strong cash cushion of roughly $760 million, but they need to keep revenue growing at a breakneck pace to manage their debt and eventually turn a real profit.

The Competitive Landscape

Tempus is not the only company trying to digitize biology.

- The labs: Massive labs like Quest Diagnostics and Labcorp have scale and deep relationships, though they lack the “tech-first” DNA of Tempus.

- The specialists: Niche TechBio rivals like Guardant Health and Caris Life Sciences are direct competitors in oncology. It’s getting scrappy, too—Guardant and Tempus are currently trading patent infringement lawsuits, a legal battle investors need to monitor.

- Big tech/pharma: Giants like Roche (which owns Flatiron Health) and Thermo Fisher are also playing in the data space.

However, Tempus does argue that their “multimodal” approach (combining clinical notes, molecular data, and imaging) gives them a “moat” (you know we hate that term) that single-focus competitors can’t cross.

Conclusion: Is the “Nvidia Moment” Coming?

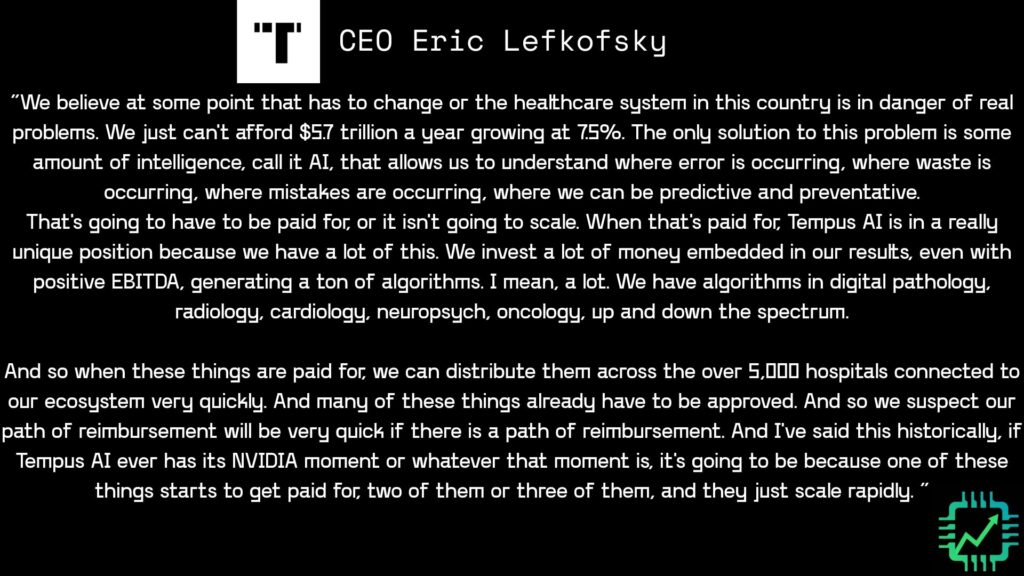

Tempus AI is betting that the U.S. healthcare system—which costs ~$5.7 trillion a year—is unsustainable without AI intervention. CEO Eric Lefkofsky believes that eventually, the system must pay for predictive data to stop waste and error.

He explicitly referenced an “Nvidia moment” in a recent call, suggesting that once insurers and the healthcare system start reimbursing for these AI algorithms at scale, the company could see exponential adoption.

For investors, the thesis is simple but risky: If you believe data is the “new oil” of healthcare, and that drug discovery will increasingly move from the petri dish to the server room, Tempus AI is a compelling infrastructure play in the market. But with high debt and a reliance on a slow-moving healthcare bureaucracy, it remains a volatile bet.