The AI bubble topic is one we address frequently. For years now. Never gets old. The TRUTH About the AI Bubble, Alphabet GOOGL Stock, and What It Means For Nvidia

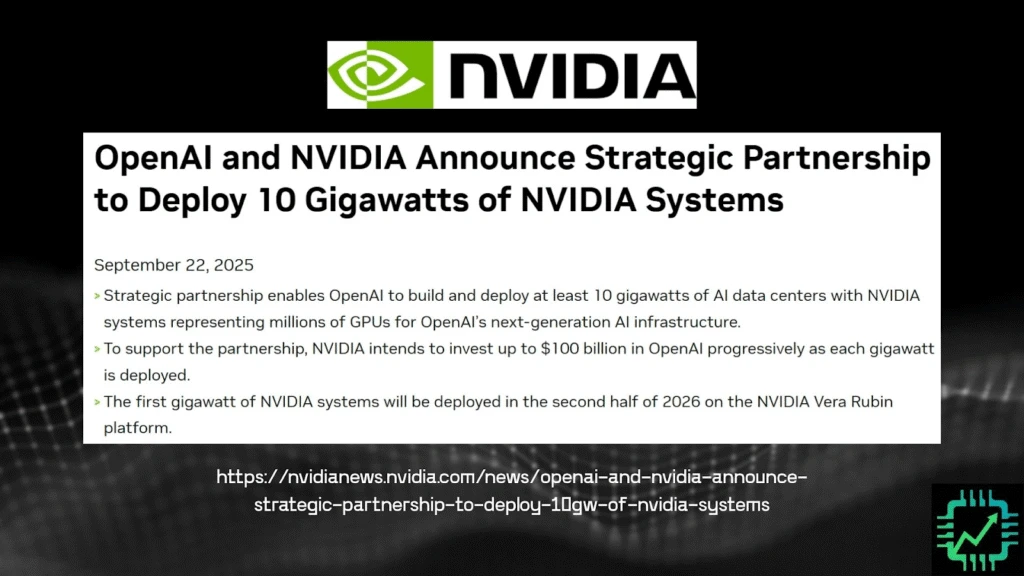

Back on September 22, 2025, Nvidia (NVDA) announced a $100 billion investment into OpenAI – details of the deal still pending, so no SEC filing yet. Just weeks later, AMD (AMD) announced a co-development deal with OpenAI, and gifted OpenAI a huge future equity stake. What just happened? Let’s break it down.

Nvidia dealing from a position of strength

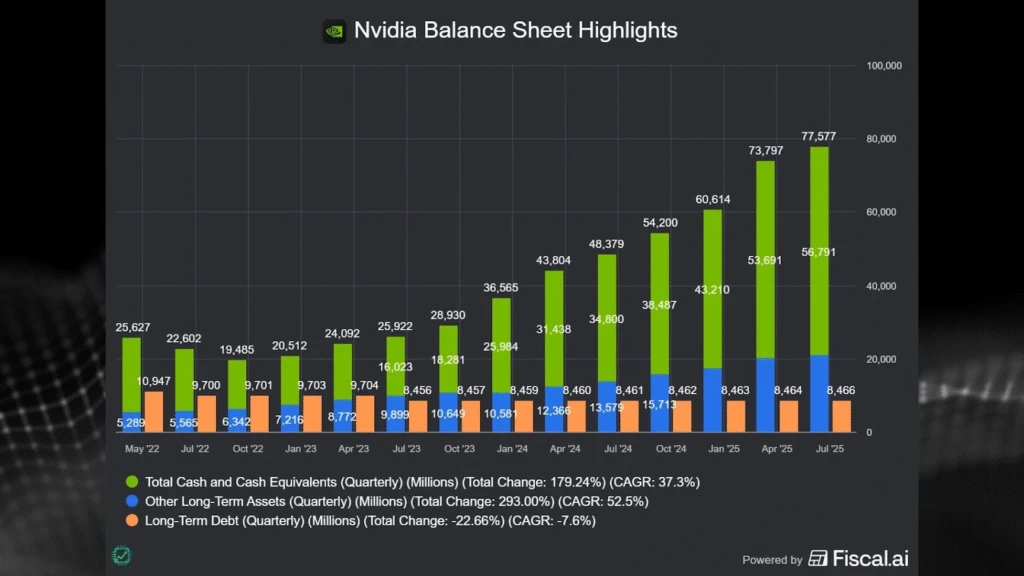

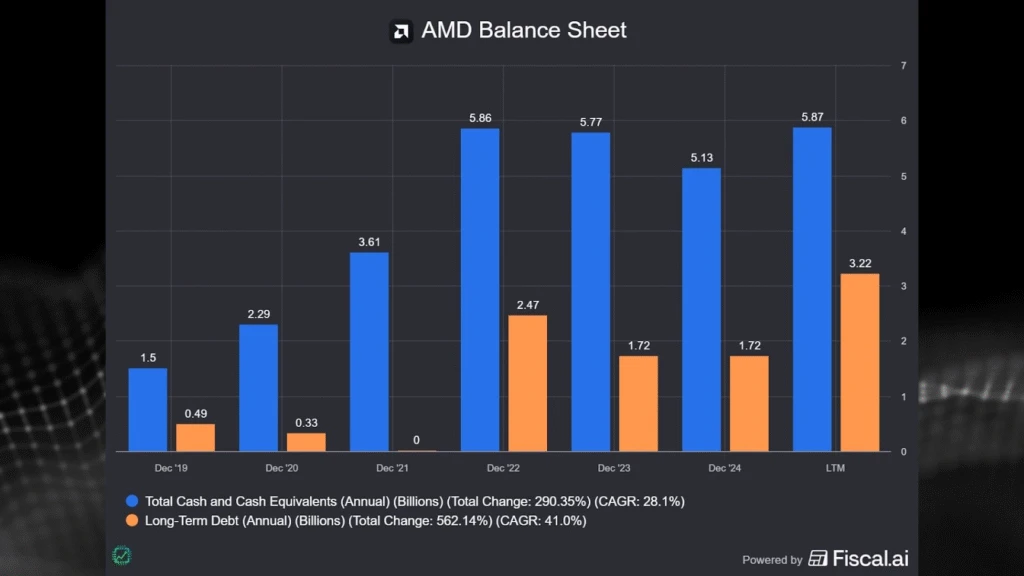

Nvidia agreeing to a $100 billion investment? That’s a wild number, but take a look at the balance sheet.

Want to make financial visuals for your research like this one? Check out Fiscal.ai, and get 15% off any paid plan using our link: Fiscal.ai/csi

With $57 billion in cash and equivalents and climbing, it’s not inconceivable to imagine $100 billion invested through 2030 (that’s the timeline we’re estimating for this deal, which we’ve inferred from AMD’s deal that we’ll discuss next).

We discussed Nvidia’s investment strategy a few weeks ago here: https://chipstockinvestor.com/nvidia-is-not-a-ponzi-scheme-ai-investments-prove-it-so/

As well as here (https://www.nasdaq.com/articles/1-overlooked-reason-nvidias-profits-could-soar-over-the-next-decade), two years ago. In summary, there are three basic reasons why Nvidia might make an equity investment in a company:

- Bet early on a startup that could become a future software/AI leader.

- An early investment could lead to a future acquisition (as in the example linked above with Enfabrica).

- Wield control over its supply chain, including over customers.

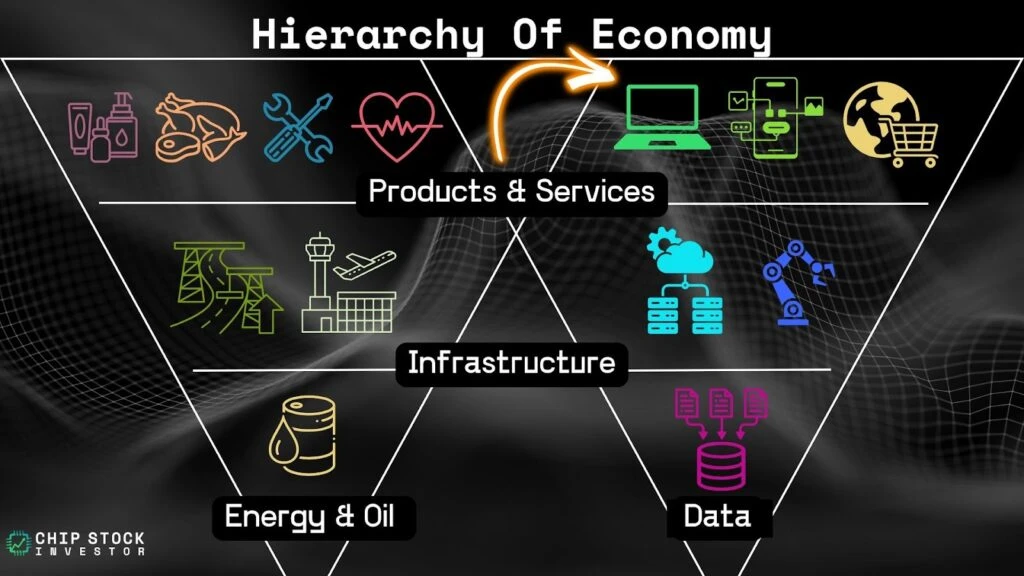

But there’s investing in early startups and small public companies. Investing in OpenAI, a private organization now valued at $500 billion – Nvidia clearly thinks future AI applications are going to be very large, and wants in early on that software end market (the top of the “economic hierarchy”).

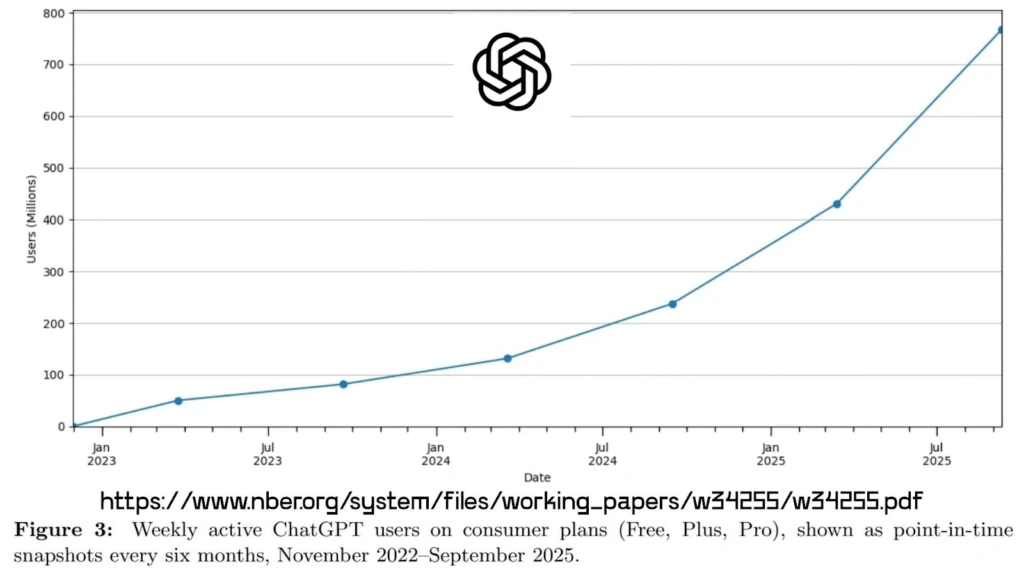

OpenAI has been forecasting massive revenue growth this year and into 2026, expecting tens of billions of new annual sales. This growth is being driven by overall users (Sam Altman just said ChatGPT surpassed 800 million users) and an expanding number of new use cases (like the announced integration with Figma (FIG) a couple days ago, as an example: https://www.figma.com/blog/turn-your-chatgpt-brainstorms-into-figjam-diagrams/).

Nvidia gets to participate in that future growth if it follows through with that $100 billion investment.

AMD says “me too,” sort of

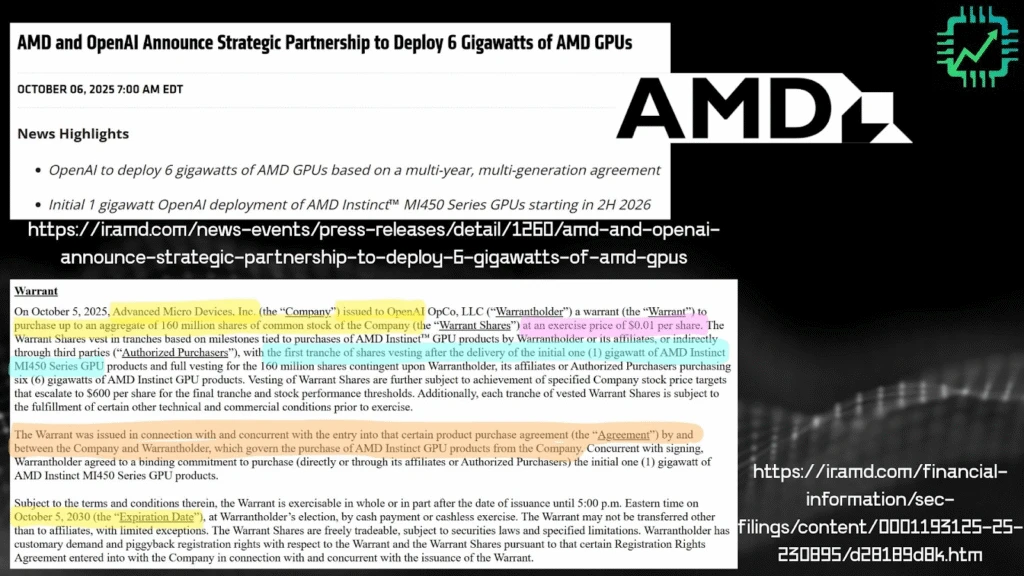

Now AMD’s equity deal, which is an inverse of what Nvidia just did. The agreement is for up to 6 gigawatts-worth of AMD data center GPUs, starting with MI450s in the second half of 2026 (similar to Nvidia’s 10 gigawatts install, also beginning in second half 2026). The full SEC filing is here: https://ir.amd.com/financial-information/sec-filings/content/0001193125-25-230895/d28189d8k.htm

Besides the install size, this deal is actually very different from the OpenAI deal with Nvidia. Firstly, this is AMD participating in the infrastructure buildout (as a chip designer), not the end market software/AI product participation. So, a different part of the economic layer is being developed with this equity deal.

To do that, AMD needed to sweeten the deal. AMD is behind Nvidia’s capabilities, and so they are giving away a lot of equity to get OpenAI to co-develop products with them, get their products to work with OpenAI software, and incentivize future OpenAI purchases of AMD products beyond 2026.

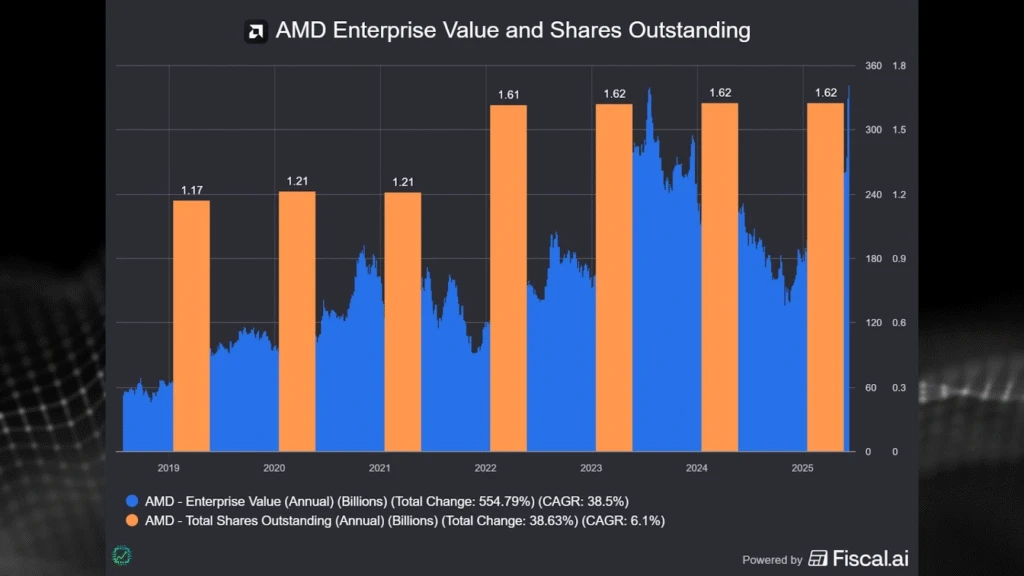

A warrant is a type of stock option that grants the owner the right to buy. At just a $0.01 exercise right, why wouldn’t OpenAI do it, if the technical milestones are met? The option is on 160 million new shares of AMD, representing 10% equity dilution through 2030 (which is why we roughly estimate Nvidia’s option to invest in OpenAI is 2030 too). Think of it like employee stock-based comp, except in this case OpenAI is the “employee” getting the equity award – potentially tens of billions of dollars-worth of SBC.

Put another way, AMD couldn’t afford to offer OpenAI cash incentives, so AMD stock owners are footing the bill. By granting a big equity stake, AMD is essentially pulling off a product discount to OpenAI (for the company’s co-development work) without lowering margins, which would make the market unhappy. Since AMD doesn’t exactly have deep pockets like Nvidia does, offering a cash-for-equity deal wasn’t going to happen.

Circular relationships and Dot-Com bubble 2.0?

Ultimately, this deal has the investment community (especially on social media) abuzz with “circular relationships” and comparisons to dot-com era customer funding accusations. At least the talk of Ponzi has eased up.

But are these deals – Nvidia investing in OpenAI, and OpenAI in turn landing a big investment in AMD – going to lead to a market crash? Maybe. But it’s too soon to say how (we continue to maintain that all good things do indeed come to an end, but bear market “crashes” ultimately pave the way for future good times).

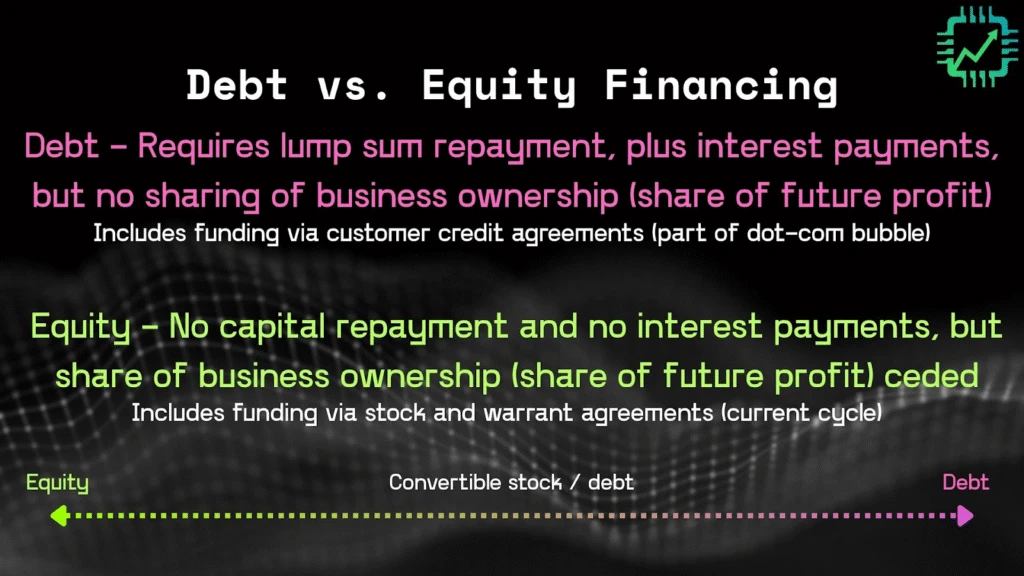

To understand why right now isn’t dot-com 2.0, here’s a simple primer on debt vs. equity financing (many companies, like Cisco, used a type of debt financing, like credit extensions, to customers buying their hardware).

In other words, equity financing is cheap early on, expensive later. Debt financing is expensive early on, cheap later.

But is debt and equity financing itself of big infrastructure products and resulting software what causes crashes and bear markets? No.

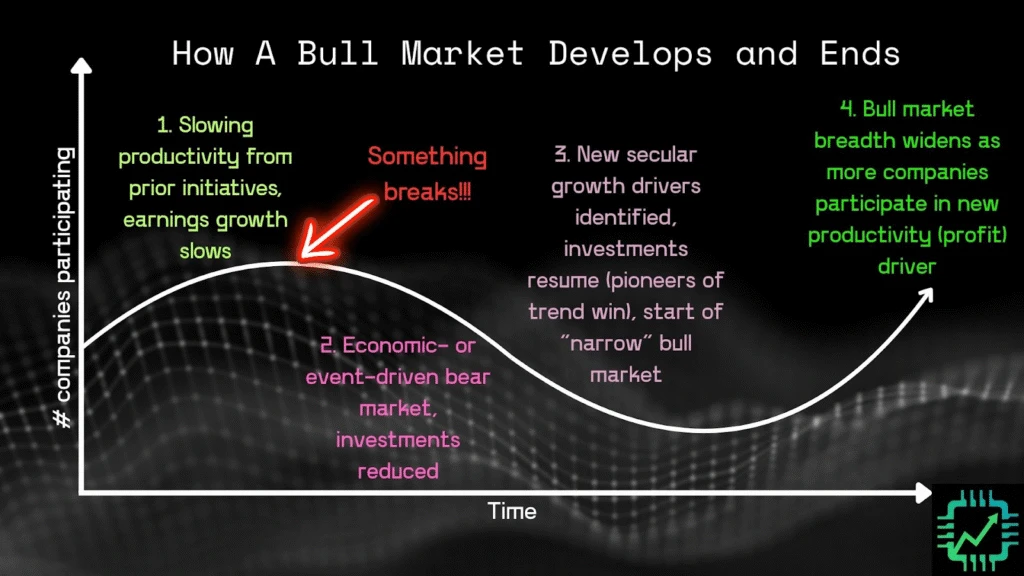

What causes a market crash and ensuing bear market is this, more or less: As more companies (and consumers) join in on a productive secular growth trend (accelerated computing and AI, in this case), increasingly less economically productive investments are made. Earnings growth slows. And with more companies participating, the chance that one or more of them “breaks something” increases.

As of right now, and as far as we can tell in our assessment, new investments being made by big tech are indeed productive – leading to lots of earnings growth. That can and will change at some point. “Circular” equity investing plans could lose their effectiveness, especially if more low-quality businesses enter the fray.

This is all conjecture, of course. We’ll know how it all goes down in real time… and hopefully, just before the real time bear market event triggers. We’ll remain vigilant, and so should you.

In the meantime, if OpenAI does deliver tens of billions of incremental revenue through next year, the coast could be clear.

An additional comment on AMD

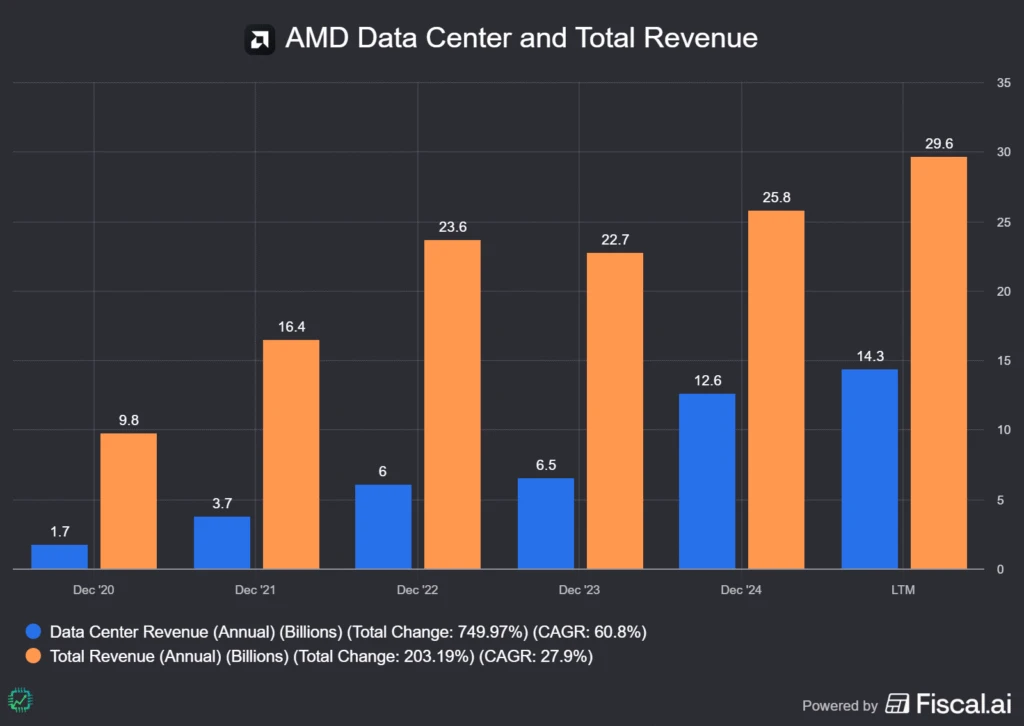

With the last tranche of the warrant requiring AMD stock be at $600 minimum by October 2030, clearly both companies (AMD and OpenAI) think there’s a possibility this happens as a result of this deal. And indeed, at 6 GW of installed MI450 and later gen GPU systems and no cash discounts (discount via the warrant), this could very easily double AMD’s data center GPU business (separate from the CPU business, which is roughly a 50/50 split as of right now) by Q4 of next year (reported January 2027 during Q4 2026 earnings).

That would be a significant growth driver for AMD’s overall revenue if the entirety of the co-development and install is executed through the next five years, as the data center segment is nearing half of trailing-12-month sales.

The only problem, as we see it right now, is the market is now pricing in the first tranche (second half 2026 MI450 install) right now, and then some, before anything has even happened yet. Besides needing to get its systems to work for OpenAI, AMD will have to contend with too-little capacity at TSMC, battling Nvidia for allocation of manufacturing output, not to mention avoiding any manufacturing hiccups that frequently occur with new product launches. The good news is, the MI series isn’t brand new, so perhaps this won’t be a major event (like Nvidia’s tough time rolling out Blackwell starting second half last year).

The question you now need to ask yourself is whether AMD can average a nearly 50% per-share profit CAGR for the next five years, including an ~2.5% share dilution event in each year starting in 2027 (about the time OpenAI would be able to exercise the first tranche of the warrant).

It’s a high bar, but doable. And one the market is, as of this week, very optimistic AMD will pull off.

One Response

You have not mentioned China’s curbs on Rare Earth Elements. Have you started analysis of that impact to the industry? I don’t follow the site much. Great work by the way.