In May 2025, we put out a public video (link above) outlining how Intel‘s (INTC) majority stake sale of Altera could benefit Lattice Semiconductor (LSCC) — the small last pure-play stock left standing in the FPGA semiconductor market. To this day, most chip investors continue to overlook Lattice, although after the Q4 2025 update, that could change.

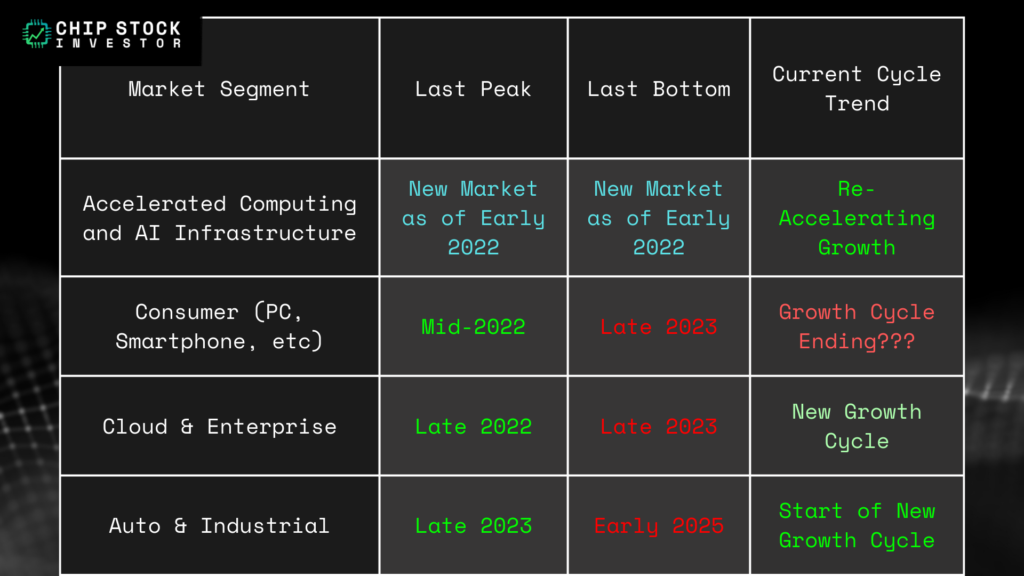

Lattice is benefitting from increased market share as it moves from small-format power-efficient FPGAs and more onto the turf of the mid-sized FPGA market (Intel and AMD, the latter via mega-acquisition of Xilinx in 2022). But the end-market sales cycle for FPGAs in general — auto/industrial/power, finally in recovery, as well as ramp-up of FPGAs in data centers — are also improving.

We own shares in two FPGA companies here at CSI: The integrated device manufacturer Microchip (MCHP, makes FPGAs among many other types of semiconductor products, including microcontroller units, or MCUs); and the much smaller FPGA pure-play Lattice.

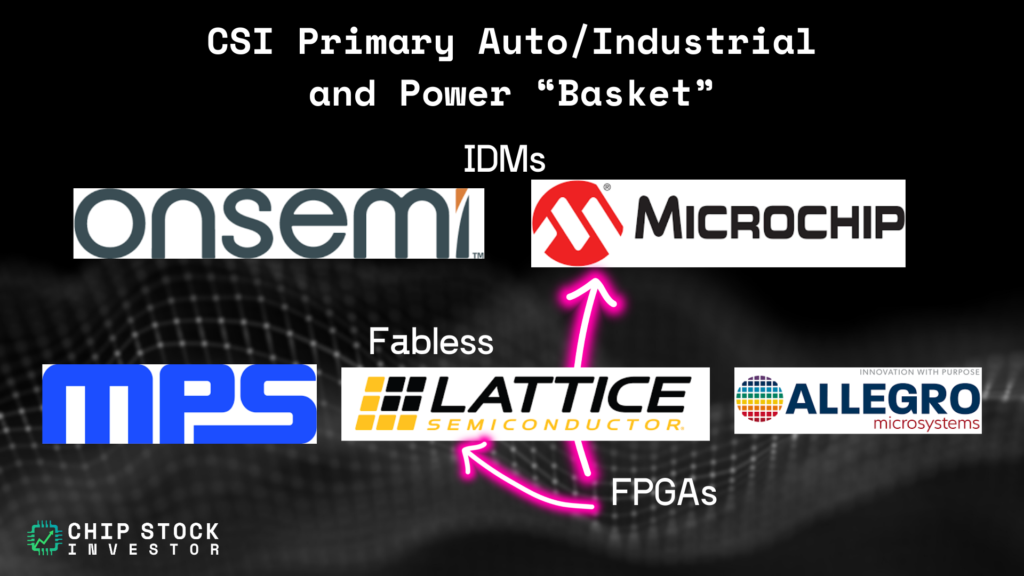

Join us on Semi Insider for more on this discussion. In the coming weeks, we’ll have a more in-depth write-up on the different companies that comprise the auto/industrial/power analog chip markets.

What is an FPGA?

- FPGA = field-programmable gate array, as the name implies, a type of chip with reprogrammable logic blocks and interconnects, ideal for high-performance applications where flexibility and post-deployment updates are important.

Ok great, but what does they do? Lattice CEO Ford Tamer came through with a great analogy on the Q4 2025 earnings call. And yes, FPGAs fit into the artificial intelligence (AI) landscape.

“As we begin 2026, I’m most excited to see that low-power FPGAs are being widely adopted at an accelerating rate, becoming the everywhere companion chips. With the Super Bowl still fresh on everyone’s mind, I will use a sports analogy. The primary processors — GPUs, custom AI accelerators, CPUs, and NPUs — are the system’s most valuable players, or MVPs. These MVPs are powerful but cannot win a game, let alone a championship, without a team. And Lattice is that team.

We provide the FPGAs, those everywhere companion chips, that perform many of the critical system functions. These include boot, power sequencing, security, control, I/O expansion, board and rack management, leak detection, power and cooling, bridging, sensor aggregation, sensor fusion, pre-processing, and many other valuable system functions.

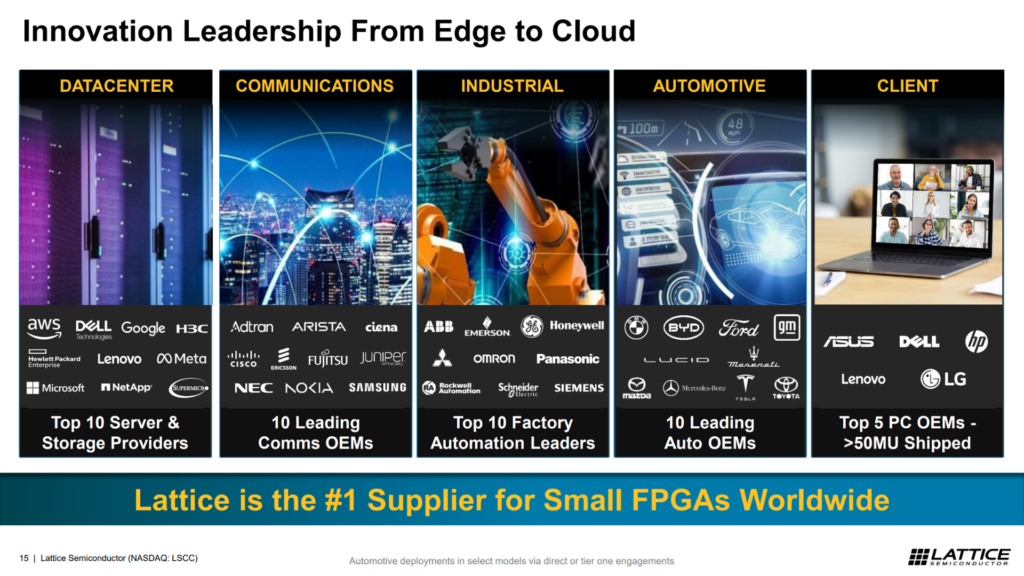

We do this across both Data Center AI and Physical AI. We do this across all major markets: Communications, compute, industrial, automotive, aerospace & defense, medical, and consumer. And we do this across some of the world’s fastest-growing applications: Security, rack management, communication, quantum cryptography, humanoids, industrial automation, logistics, robotaxis, space, and AR/VR wearables. Those powerful companion chips provide pervasive interoperability across all these vital functions, markets, applications, and diverse suppliers. You can consider Lattice as Switzerland for data center and physical AI applications.”

Alluding to the MCUs, like from peer/competitor Microchip earlier, FPGAs are generally more flexible (circuit-level reconfigurable, vs. just software-level reprogrammable) and capable of handling more complex tasks like parallel computing. Tamer continued on the earnings call, regarding FPGAs growing importance in different AI applications, including edge AI:

“And instead of software running on a microcontroller, Lattice FPGAs do this in hardware, making it easier to guarantee the same cycle-accurate responses every time. Finally, in some cases, FPGAs can also serve as the primary compute, such as signal processing, real-time networking, and what has become to be known as far-edge AI. We at Lattice define far-edge AI as near-sensor contextual AI with tiny or small self-contained models. And our momentum is building. For example, we recently won a design in a human-machine interface, or HMI, industrial robotics, and we are seeing the pull for applications under 1 TOPS and under 1 Watt.”

We’ve of the belief that the low-power, small footprint, and software capabilities of Lattice FPGAs are a differentiator. And it would seem that as computing tasks get more complex, FPGAs are becoming much more than just small-niche hardware, evolving into a type of do-anything workhorse in support of those logic chip “MVPs,” per Tamer on the earnings call.

What about the competition?

We’ve discussed Microchip in the past; it was one of the harder-hit IDM businesses when the chip shortage of 2022 flipped to over-supply in 2023. Microchip is making progress digging itself out of that deep hole.

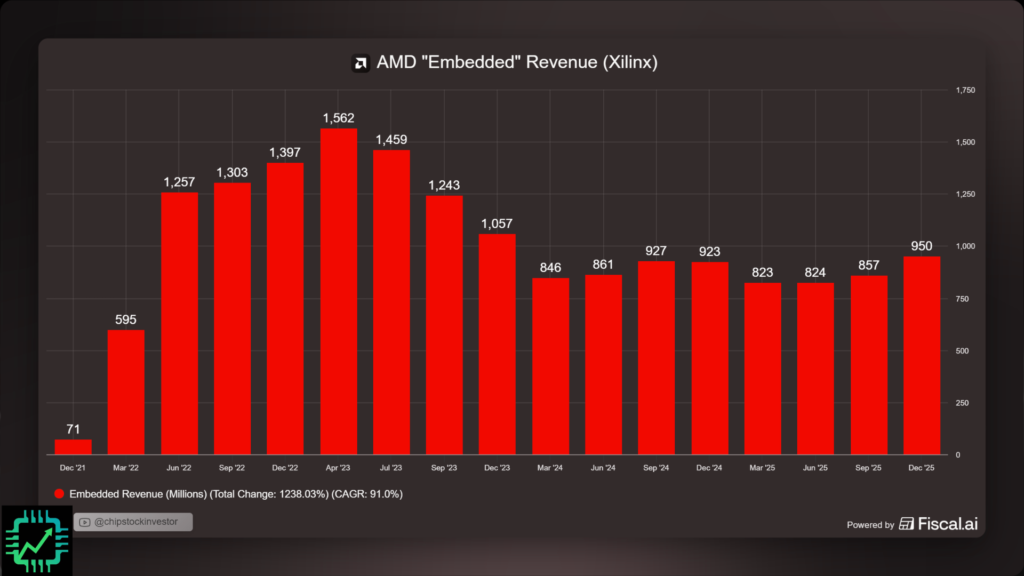

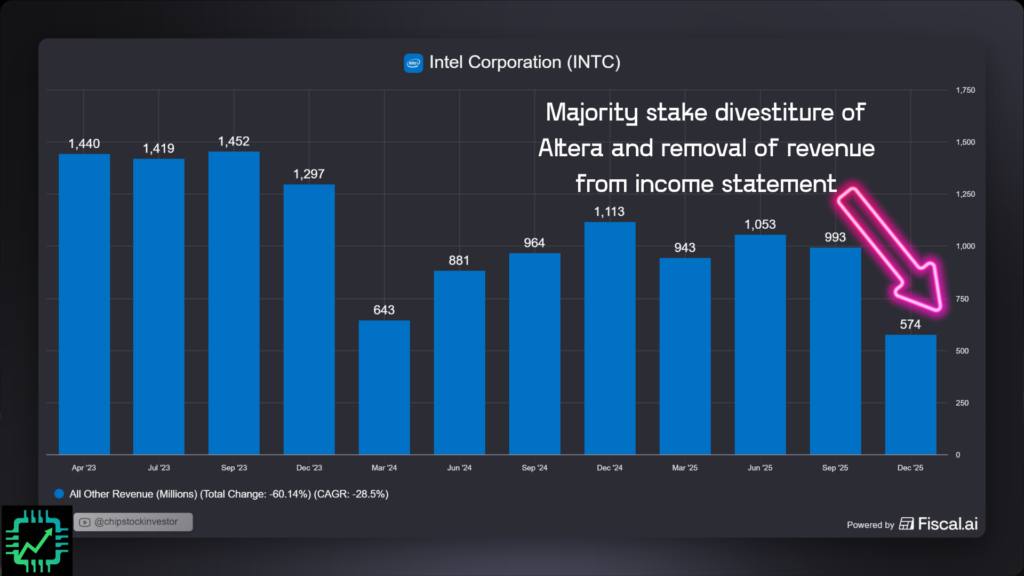

And meanwhile, AMD (now owns FPGA market-leader Xilinx, reported as “Embedded” revenue in first chart below) and Intel (now minority-owner of second-place FPGA company Altera, with private equity group Silver Lake now taking the lead at Altera) have been distracted by the AI data center race, trying to play catch-up to the actual industry MVP Nvidia. The distraction has left the door open for a small scrappy pure-play like Lattice to make some moves.

Note in the chart above, Intel’s “other revenue” segment fell from $993 million in Q3 2025 to $574 million in Q4 2025 when it completed the divestiture of Altera. The remaining “other” revenue in Q4 is primarily from Intel’s majority stake it still owns in Mobileye. However you slice it, Altera + Mobileye have struggled the last couple of years.

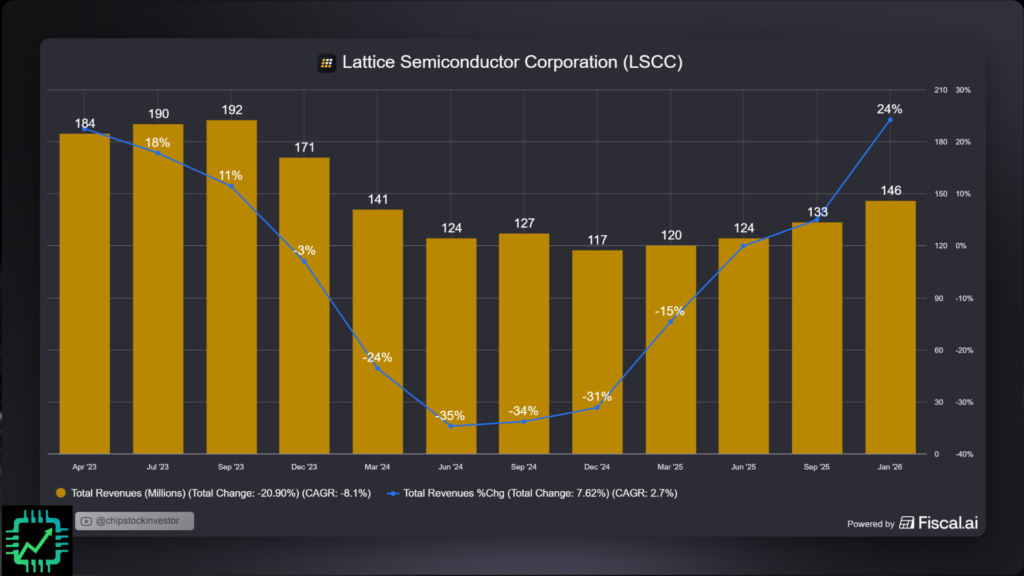

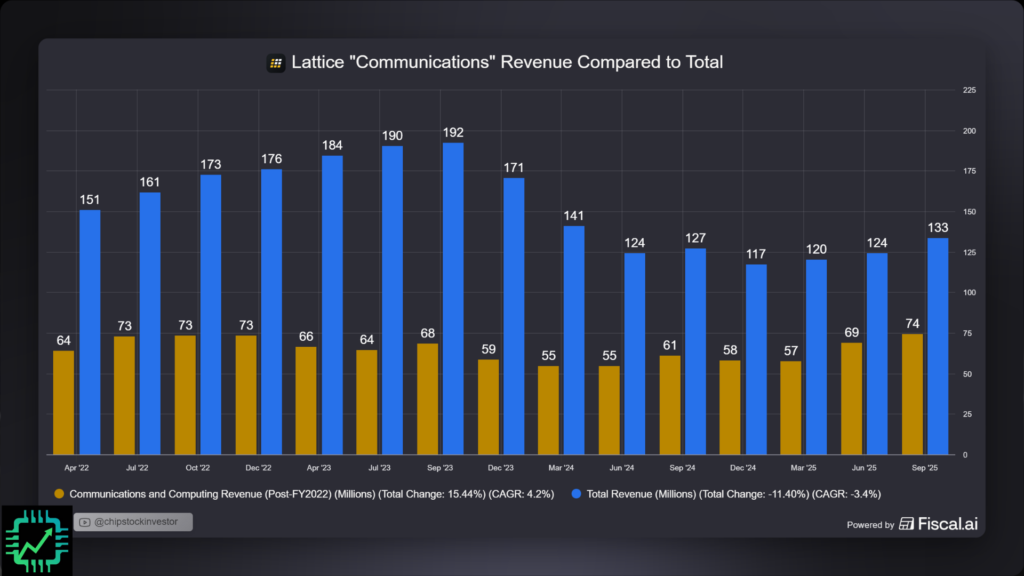

While Lattice hasn’t exactly been setting the world on fire either, its momentum has been slowly re-building through 2025 — culminating in a solid Q4 2025 with 24% year-over-year revenue growth. No surprise, increasing market share in high-performance and AI data center servers (included in the “Communications and Computing” segment in the second chart below) is the big reason why.

Want to make financial visuals for your research like the ones above? Check out Fiscal.ai, and get 15% off any paid plan when using our link: Fiscal.ai/csi/

The stock is now at a premium — but how much premium?

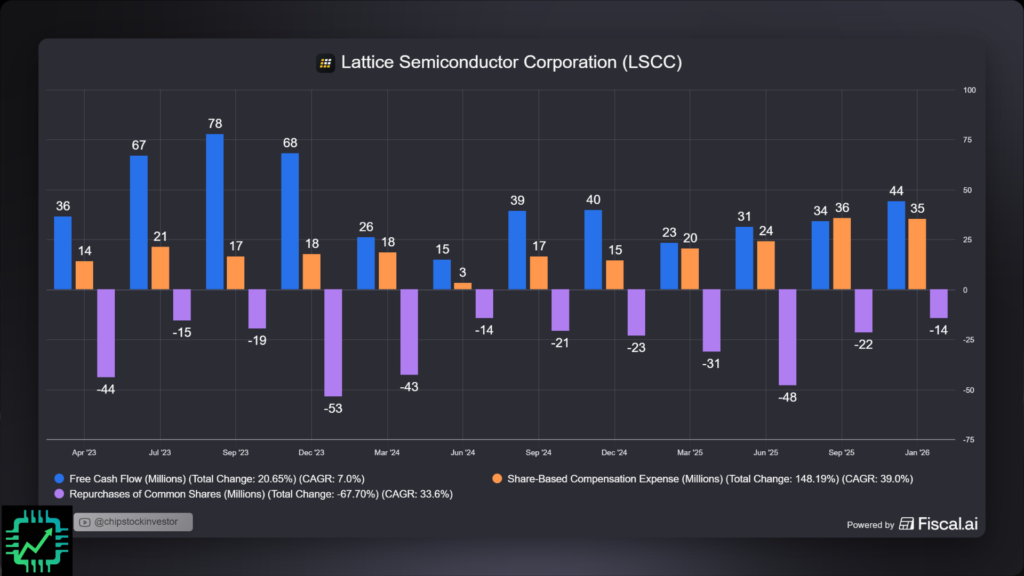

In tandem with the revenue recovery, profitability has also risen. Free cash flow (FCF) generation, in particular the first half of 2025, was used to repurchase plenty of stock to offset stock-based compensation (fabless designers tend to have higher employee SBC; engineers want to get paid).

But now trading at ~84x trailing-12-month free cash flow as the growth cycle heats up, Lattice certainly looks like more of a premium than it was this time a year ago.

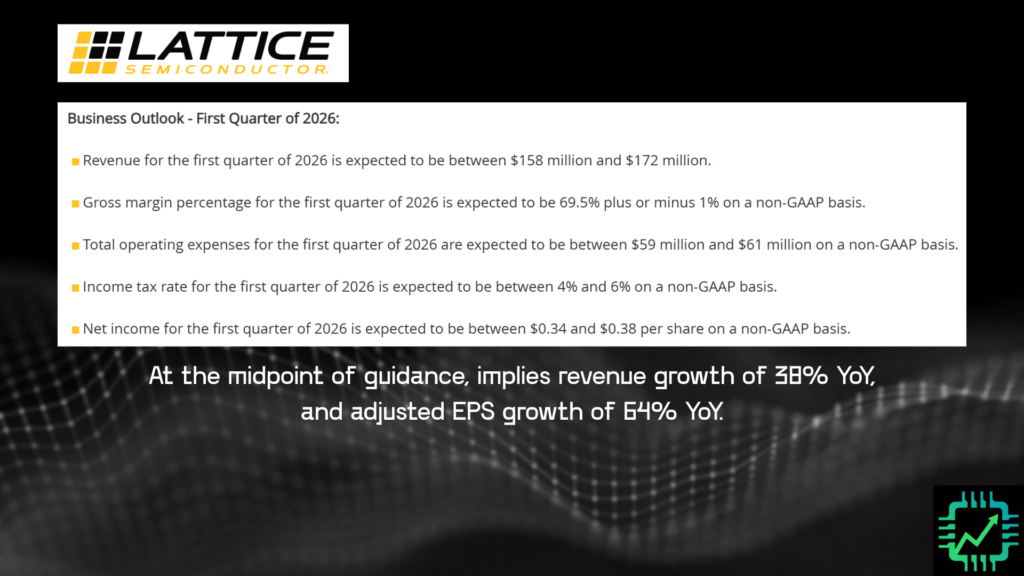

The big caveat, though, is that early on in a new growth cycle, profitability can do the “hockey-stick-shaped” (or “U-shaped”) rally. Note for Q1 2026, midpoint revenue guidance is for a 38% year-over-year increase, translating into adjusted earnings growth of 64%. If the cycle heats up further in 2026, profits could rally even more dramatically. Case in point: Lattice management indicated customer inventories are now fully corrected after a multi-year period of over-supply, and all end-markets are expected to return to growth along with strong data center demand.

If management’s outlook on revenue for Q1 2026 works out as expected, this would put Lattice within striking distance of reaching all-time-high sales again. The previous peak quarterly-sales level of $192 million was back in Q3 2023.

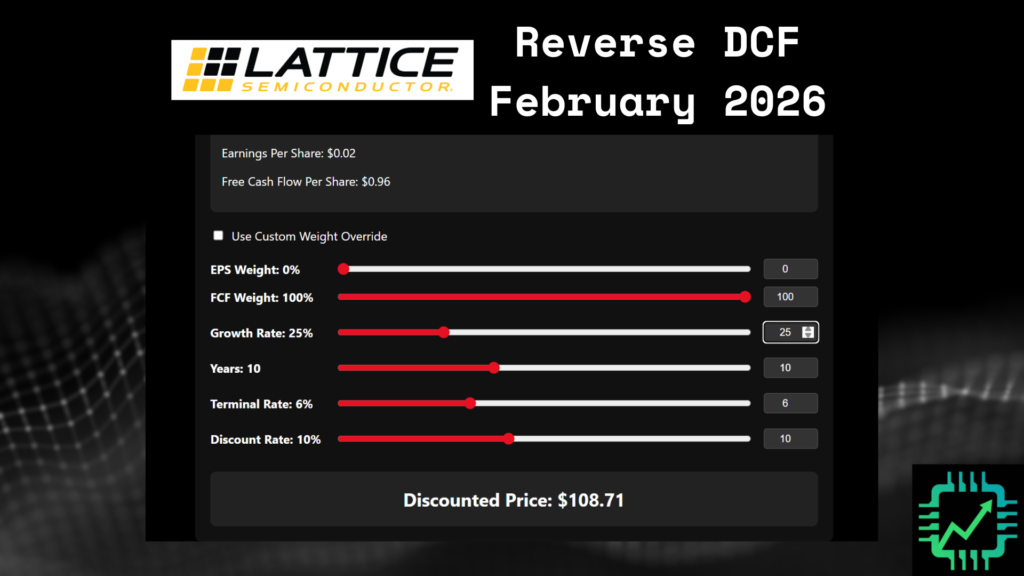

But an earnings multiple has limited usefulness without assessing for future cash flow generation of a company. So we ran a reverse DCF (discounted cash flow) to see what type of growth scenario might be baked into the stock price as of this writing (around $106 in pre-market February 12, 2026).

- 2025 FCF-per-share of $0.96 as a starting point (normalized earnings potential, given GAAP earnings were still depressed last year)

- 25% per-share growth rate for 10 years

- Terminal growth rate of 6%

- Discount rate of 10%

Suffice to say the bar is now quite high after the jump following the Q4 report. We aren’t adding to our position here, as our expectation is for elevated volatility for at least a quarter or two following the big run in stock price. Nevertheless, we’re on the lookout for any buy-the-dip opportunity.

Plus, with FPGAs and related auto/industrial/power semiconductors in early stages of recovery, Lattice could be an indicator for opportunities elsewhere amongst its peers. As mentioned at the outset, stay tuned for a deeper dive into these end markets, especially for FPGA and MCU-adjacent analog chips, historically tied to industry-specific, automotive, and power applications.