A year ago, we outlined why we were still optimistic about The Trade Desk (TTD) — assuming earnings results were positive through at least a couple quarters in 2025. The Trade Desk Flops — Is the Company In Trouble? Time to Buy TTD Stock In 2025?

Well, that didn’t happen, and the stock continues to be a value trap. We’ve been discussing this over on Semi Insider, and thought this also deserved a public update.

A myriad of issues have arisen, including the abrupt departure of CFO Alex Kayyal after only five months on the job. No real word on what happened, but abrupt exits like this are often indicative of internal issues and company growing pains.

At any rate, let’s narrow on some specifics of what has gone wrong, and how low the bar has been lowered after another selloff post-Q4 2025 earnings update.

1. Big tech might actually be taking market share

As we discussed on Semi Insider in January 2025, The Trade Desk is focused on the demand-side of the digital ads exchange — helping its marketing and brand customers find the best value and return on investment (ROI) from their ad purchases. But besides a few anomalies (like AppLovin), the very best digital ad investments have been big tech. Companies that play both sides of the exchange, the demand-side and the supply-side (ad inventory), as well as the network compute infrastructure in between, continue to demonstrate business model advantages. Alternatively, companies that manage an ads business as a part of a larger ecosystem (Netflix, Apple, big software conglomerates) have also done well.

DSP (demand-side) and SSP (supply-side) pure play companies have not fared nearly so well in the digital ads industry.

What had us convinced for so many years The Trade Desk would be different? Besides sustaining a high level of revenue growth, it was this long-running item in the annual reports:

We empower ad buyers by providing a self‑service cloud-based ad-buying platform that enables them to plan, manage, optimize and measure data‑driven digital advertising campaigns. Our platform allows clients to execute integrated campaigns across various advertising channels and formats, including CTV and other video, display, audio and native, on a multitude of devices, including televisions, streaming devices, mobile devices, computers and digital-out-of-home devices.

- We Are Focused on the Buy Side. We focus on buyers since they control the advertising budgets. The supply of digital advertising inventory exceeds demand, and accordingly, we believe it is a buyer’s market. We also believe that by aligning our core offerings with buyers, we are able to avoid conflicts of interest that exist when serving both the buy side and sell side. We provide and are developing additional offerings and features that work with publishers and supply-side partners to help ensure access to quality advertising inventory and to enable improved evaluation of such inventory and better decisioning capabilities for buyers of advertising. This focus allows us to build trust with clients, many of whom leverage their proprietary data on our platform. That trust and ability to use their own data on our platform, without worrying about it being used by other participants, enables our clients and their advertisers to achieve better results. This trust provides us with the benefit of long-term and stable relationships with our clients.

It’s a good story, and to an extent, we still believe the dynamic of serving and aligning with marketers and ad purchasers is working to The Trade Desk’s advantage. But as pointed out late last year, The Trade Desks consumer brand customers are pulling back on ad spend right now. Additionally, after plenty of debate about whether Amazon‘s (AMZN) DSP offering was a competitive threat or not, The Trade Desk CEO and co-founder Jeff Green all but confirmed the answer was yes on the Q4 2025 earnings call — citing a consumer brand customer that ran a test comparing The Trade Desk with Amazon’s DSP.

Green said the conclusion was The Trade Desk delivered more value than Amazon. But still, the mention was telling. The Trade Desk is under pressure right now from deep-pocketed diversified tech rivals.

2. Customer slowdown and competition throttles growth once again

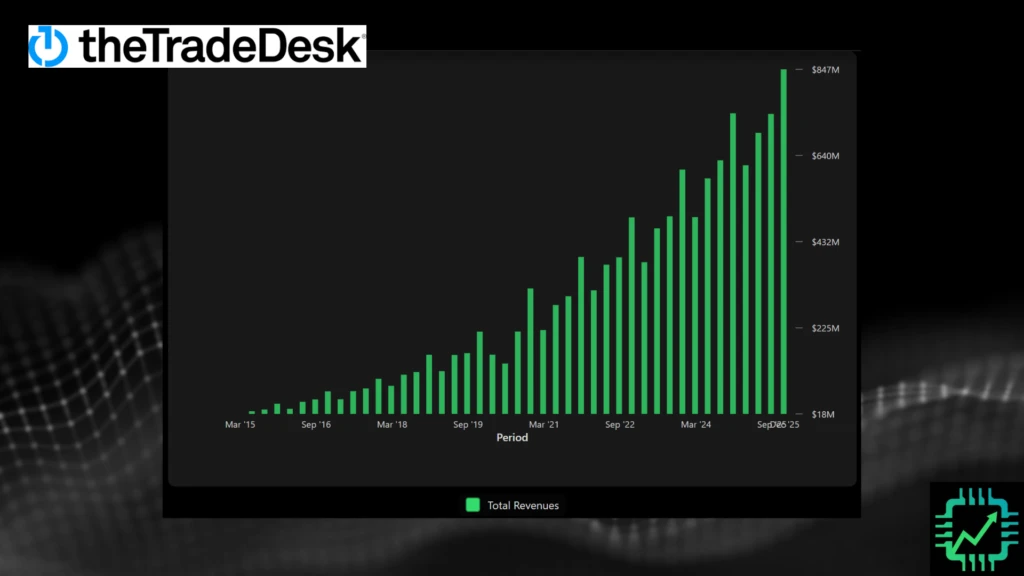

On the surface, all is well for The Trade Desk. Revenue in 2025 continued to slightly outpace the global ad industry average of about 9% (18% growth for The Trade Desk in full-year 2025, 14% growth in Q4). Revenue growing faster than secular growth industry-average is a positive.

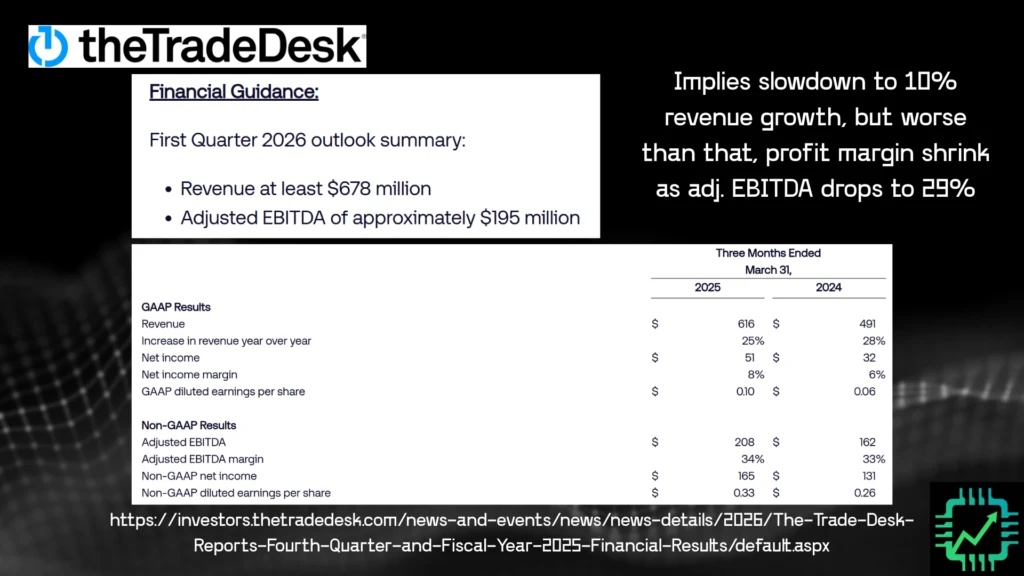

As a result of the above mentioned industry dynamics and The Trade Desk customer spending slowdowns, Q1 2026 is expected to get off to a sluggish start. In fact, the outlook for revenue of “at least $678 million” implies 10% (or more) growth from Q1 last year — putting The Trade Desk at just barely over total ad industry averages, and behind big tech ad business growth expectations.

Worse than that, though, is the profit margin compression that is expected. Adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) of “at least $195 million” implies a 29% margin, well below the 34% and 33% margins reported in Q1 2025 and 2024, respectively.

As a company’s revenue growth slows, the expectations is profit margins generally increase, so it’s no surprise investors are concerned with the outlook. One implication is, at least for the time being, The Trade Desk is making less productive investments in its business compared to years’ past.

3. Speaking of corporate capital investments…

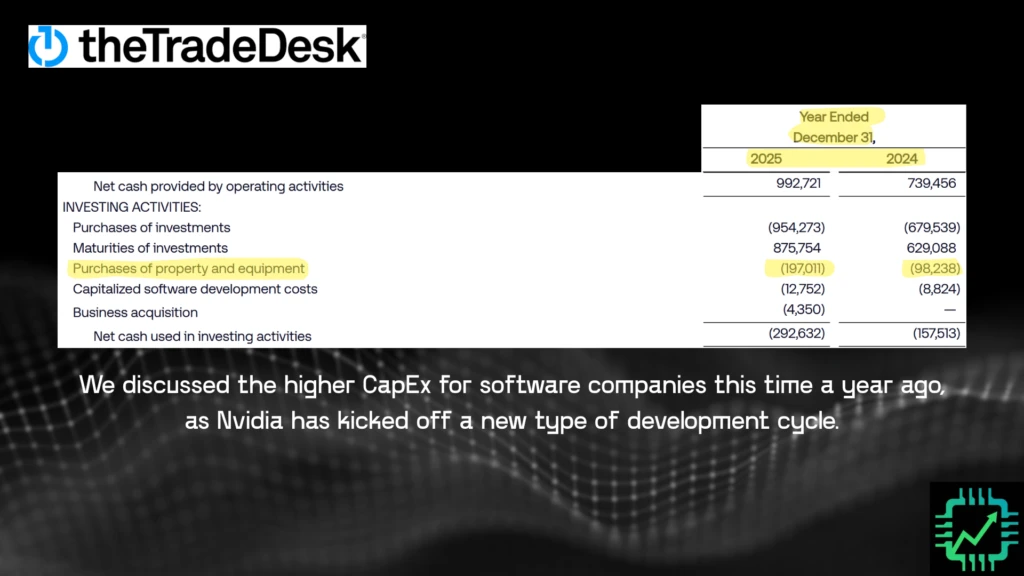

Third and final point regarding The Trade Desk’s lower investment productivity. We called out late in 2024 and in early 2025 that many “asset-light” software companies were beginning to report higher capital expenditures (CapEx, spending on property and equipment, very much the opposite of “asset-light”). The Trade Desk’s CapEx has indeed continued to increase, doubling in 2025 to $197 million.

What’s going on? We had speculated last year that Nvidia‘s AI data center party has spurred on a re-think among some software technologists in whether renting most of their data center compute was still a good idea (in the case of The Trade Desk, renting from Amazon, also its DSP rival; not hard to see the conflict of interest, see the supply chain diagram on The Trade Desk company page on the Semi Insider Research Dashboard).

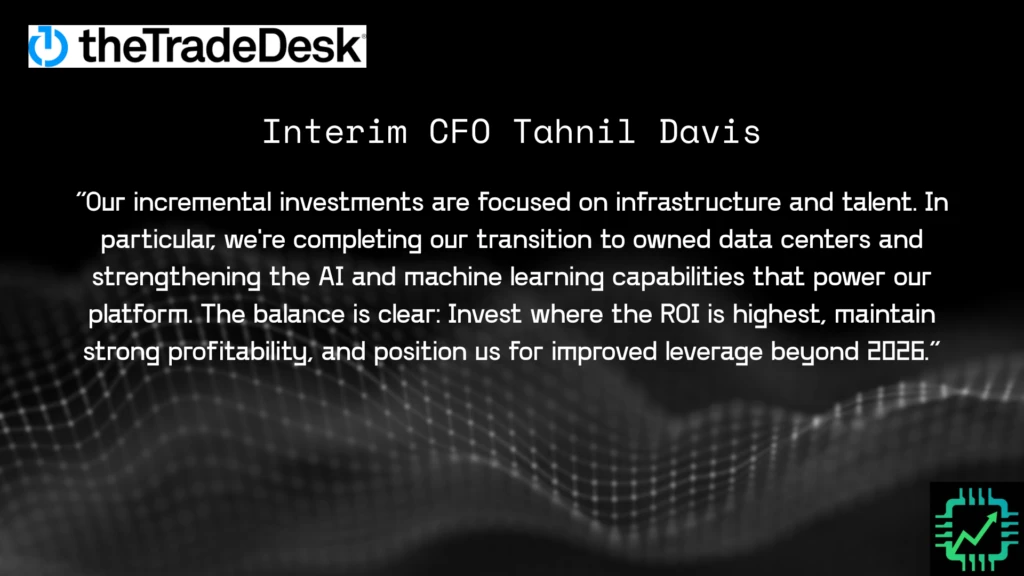

Sure enough, the company thinks purchasing and operating its own data center assets is a good idea. Per interim CFO Tahnil Davis:

“Our incremental investments are focused on infrastructure and talent. In particular, we’re completing our transition to owned data centers and strengthening the AI and machine learning capabilities that power our platform. The balance is clear: Invest where the ROI is highest, maintain strong profitability, and position us for improved leverage beyond 2026.”

This could be a great long-term move, but it nonetheless demonstrates the new R&D investment cycle software is engaged in because of AI. And buying and operating data center infrastructure is one reason why the profit margins are compressing. Data centers and servers aren’t cheap.

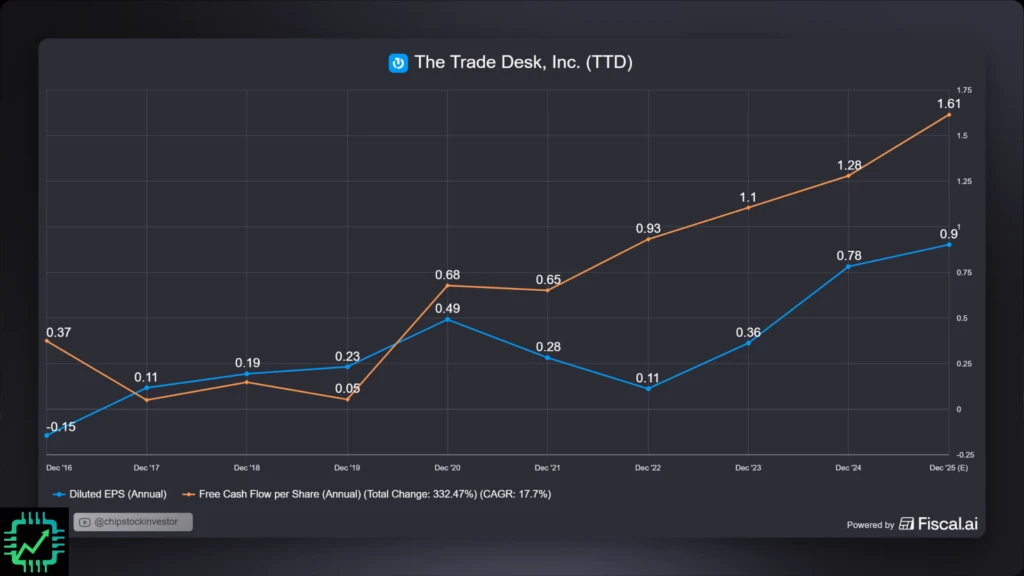

It’s going to take time to tell if the CapEx pays off. And in the meantime, the lower cash profit in the short-term also needs to be discounted. We expect their to be a falloff in free cash flow (FCF)-per-share growth to start 2026, hampering what has been a nearly 18% compound annual growth rate for the metric over the last decade.

How low has the bar been set?

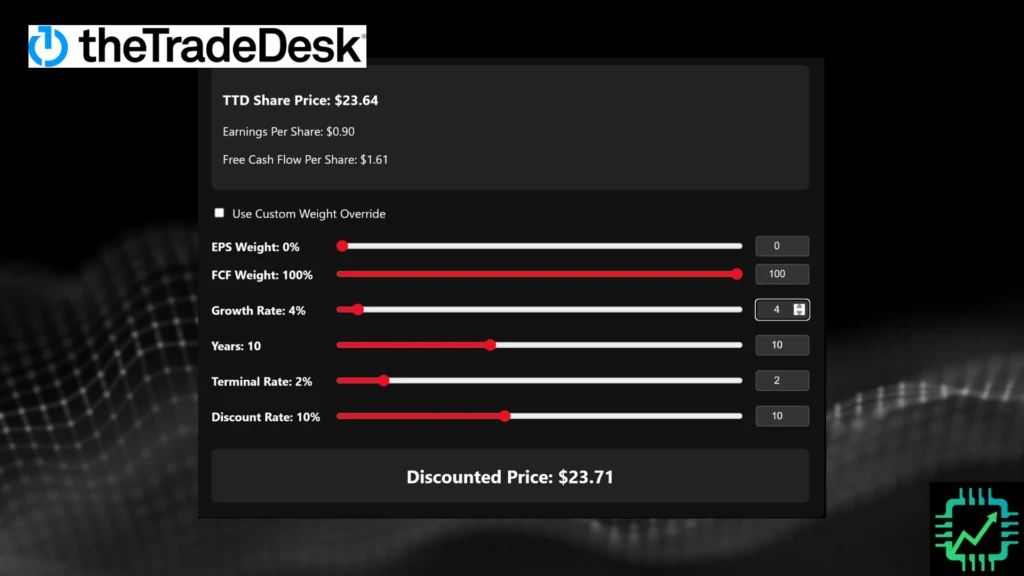

It would seem the market has indeed lowered TTD stock down to a level that accounts for a short-term drop in FCF profit. We ran a reverse DCF (discounted cash flow) scenario on our simple calculator:

- 2025 FCF-per-share of $1.61 as a starting point

- Per-share profit growth of 4% for 10 years

- 2% terminal growth rate

- Discount rate of 10%

Yes it would seem expectations will be easy for The Trade Desk to clear in the coming years. But will the company be a good long-term investment? That remains to be seen. For now, we will play wait-and-see, specifically on whether revenue can re-accelerate later this year, and if profit margin stabilizes and returns to growth (a sign that the data center infrastructure investments are paying off).

But at this point, we aren’t buying more. We’re ready to cut bait if we need to and move on to more productive digital ad investments if the revenue slowdown and margin compression doesn’t improve.

See you over on Semi Insider for more of the discussion, and to try out our growing investment tools to help investors navigate semiconductor, electronics, and end market supply chains. We have some exciting new features planned for this coming spring to help with navigating the large CSI company/stock universe.