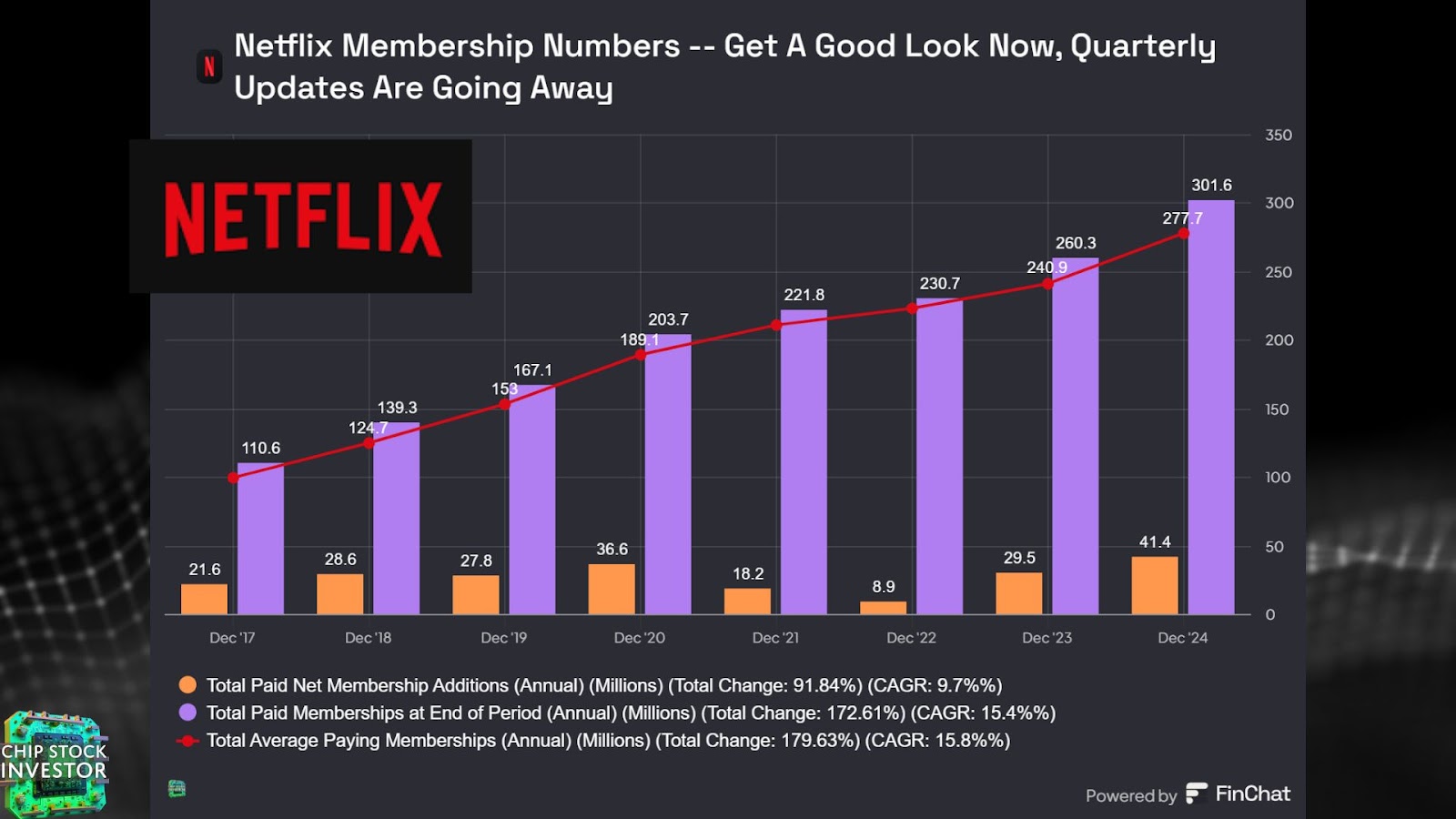

Ok, by now you probably know all about Netflix’s (NFLX) epic finish to 2024 (they added over 40 million net new subs in 2024, topping 300 million worldwide for the first time, but also raised plan prices across the board). Suffice to say Q4 earnings were very good.

But far and away the most important information when deciding whether a business is a good investment or not is the future, not the past. So what is Netflix anticipating for 2025? And is the stock still a decent valuation after increasing some 80% since the start of 2024 alone?

Netflix the KC Chiefs of entertainment?

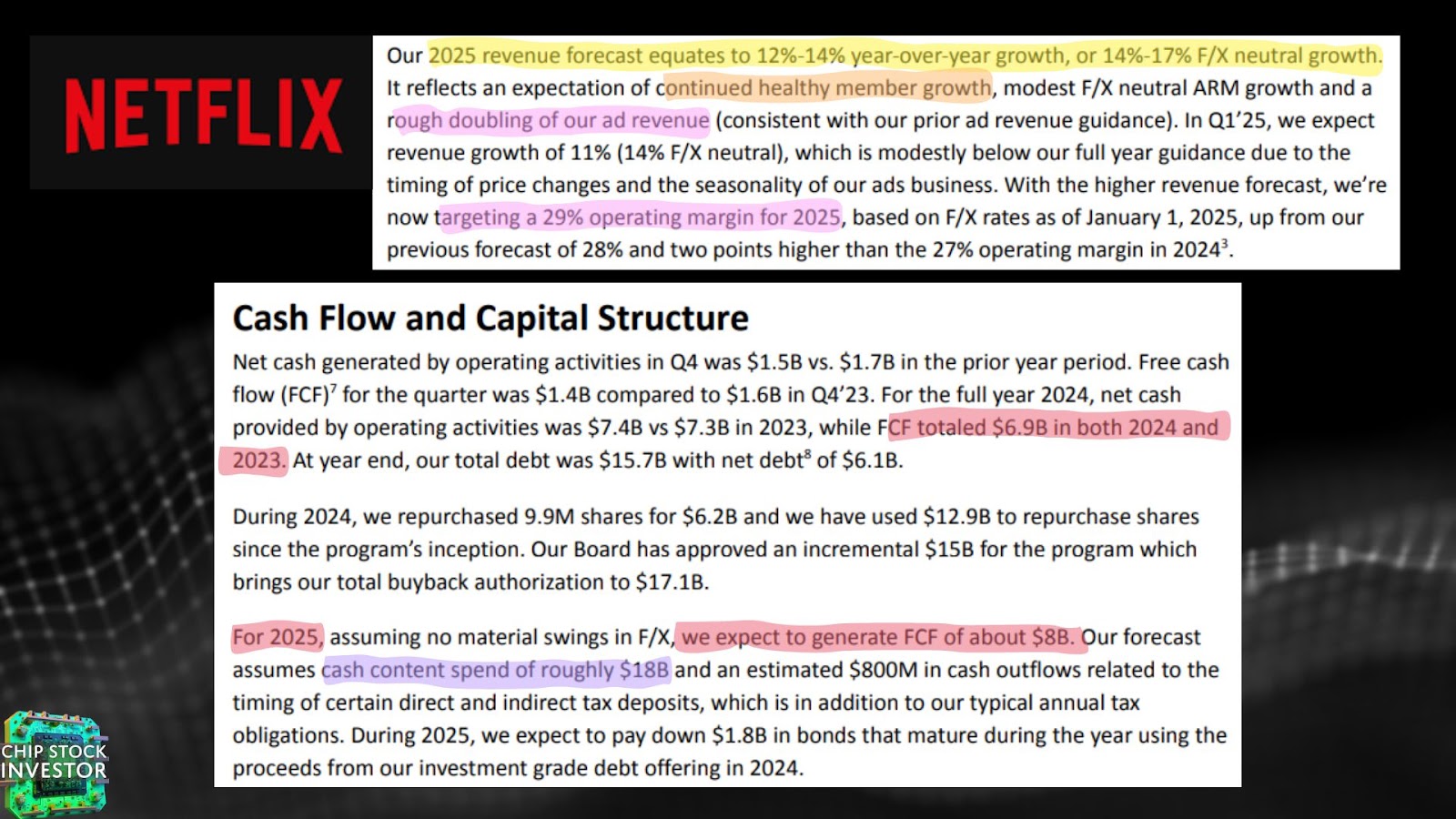

Netflix’s top team is forecasting 2025 revenue growth of 12% to 14%. Growth would be a bit higher when excluding foreign currency exchange rates, remember that over 60% of Netflix revenue is outside the U.S., and the company only seeks to hedge about half of that against currency fluctuations).

More momentum in memberships, plus a double in ad revenue, is expected to drive this revenue growth. And more importantly, Netflix believes its operating profit margins will keep rising. Free cash flow (FCF) margin could be flat, or be under a bit of pressure. Hold that thought.

Notice some of the spending increases outlined above will be on content. “Additions to content assets” pulled from the cash flow statement were $12.6 billion and $16.2 billion in 2023 and 2024, respectively. Cash content spend is anticipated to increase to ~$18 billion in 2025, so a bit less of an increase than in years past. Still, with linear TV (cable, broadcast, basically non-internet based) in decline, the movie theater business in total disarray, and live sports moving to streaming too, Netflix has ample opportunity to consolidate old media to itself by expanding into more content categories and geographies.

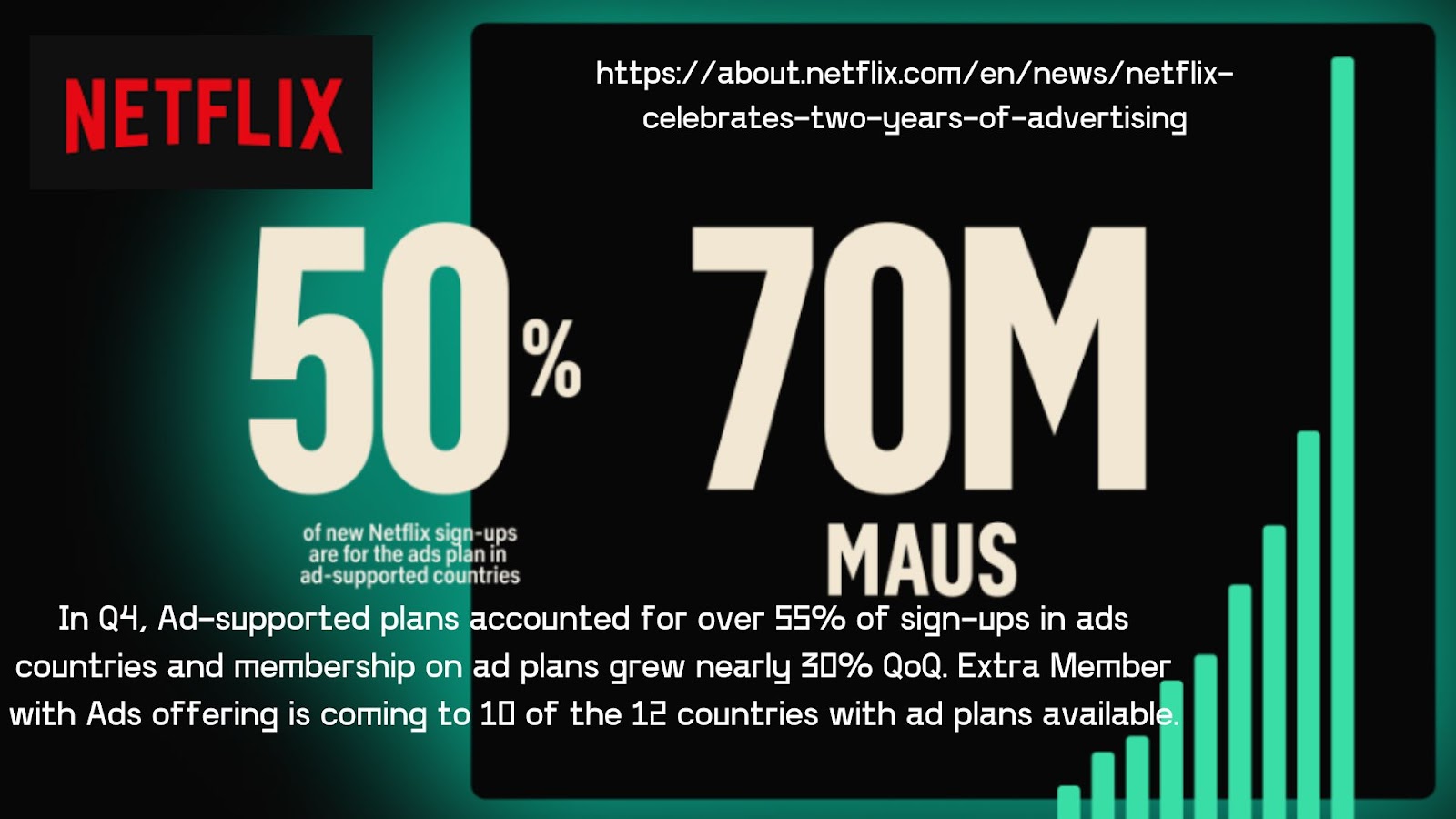

Additionally, the ad-supported plans – still only available in a dozen or so countries – is also fueling new subscriber growth. As more ads get delivered, Netflix should eventually see some profit margin contribution from this newer area of the business too.

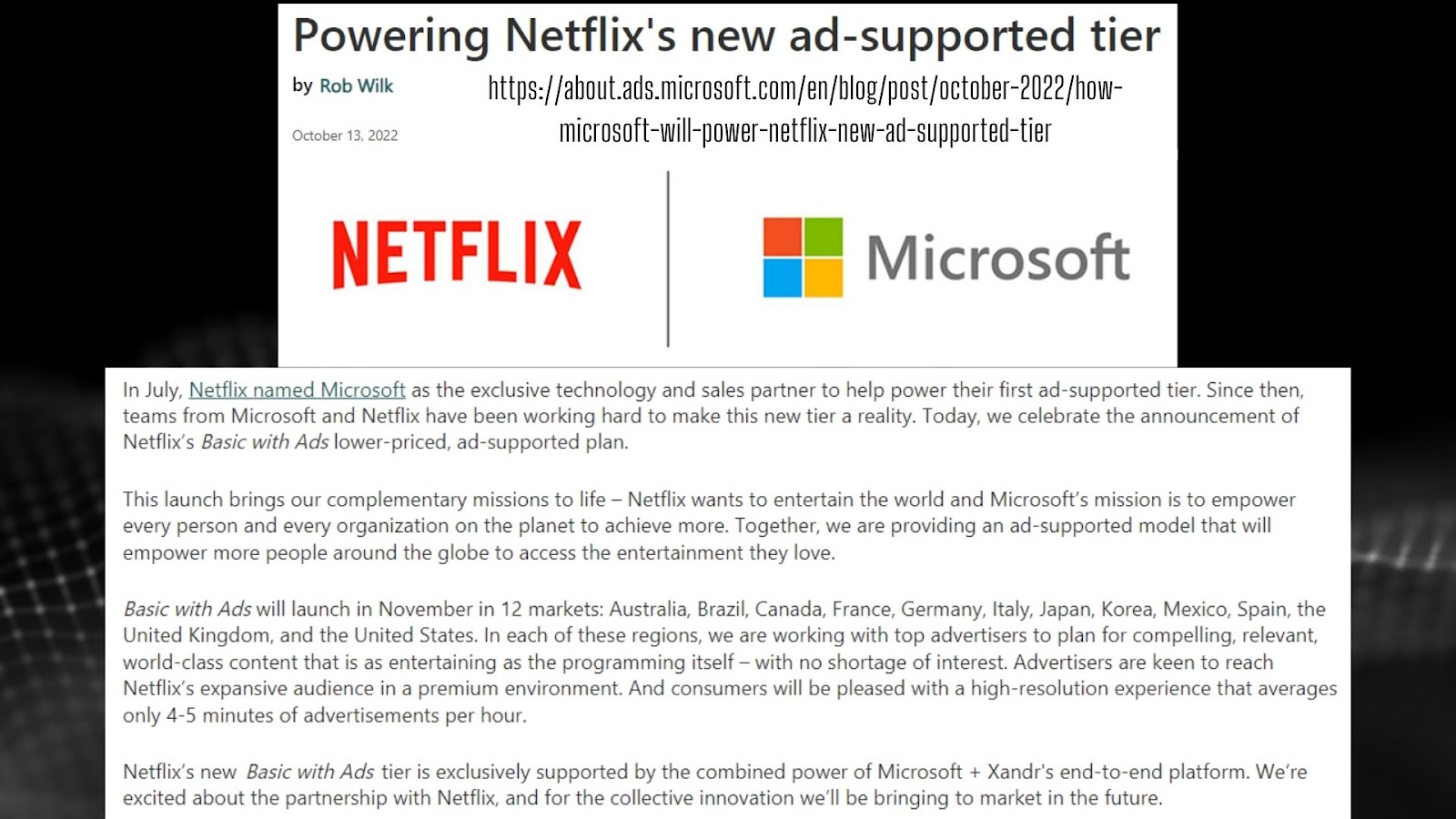

Just as a reminder, Netflix celebrated the two-year-anniversary launch of its ad business (using Microsoft ad tech) in November 2024. There’s a very long onramp to growth remaining in ads. It seems this is one of the primary factors contributing to Netflix’s strong closeout in global subscriber count last year. Ad-supported plan sign-ups grew a whopping 30% quarter-over-quarter from Q3 to Q4 2024.

If you want to make cool financial charts and models, check out FinChat.io. Here’s a link that gets you 15% off a membership: https://finchat.io/csi/

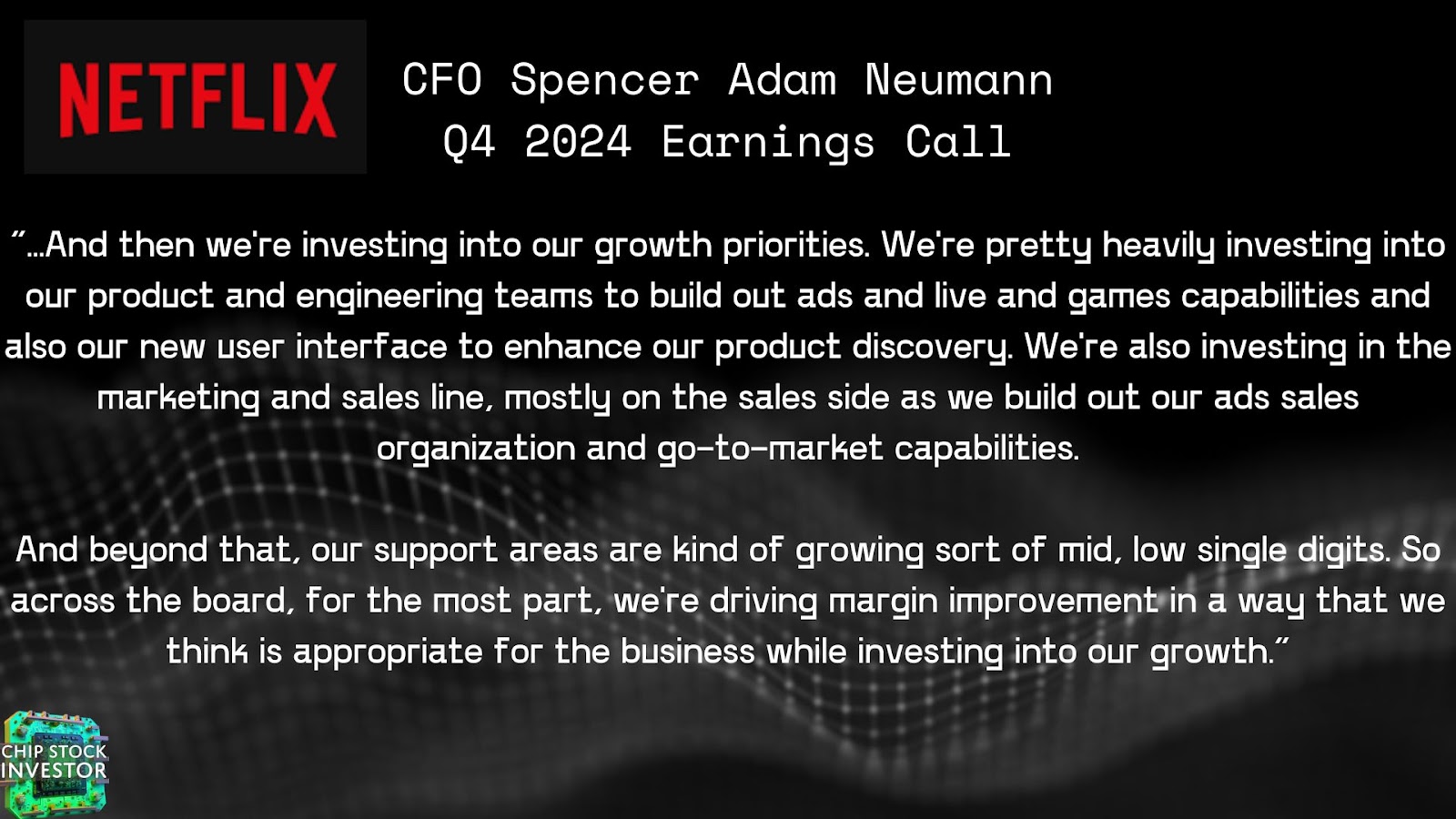

Margin expansion is the real name of the game

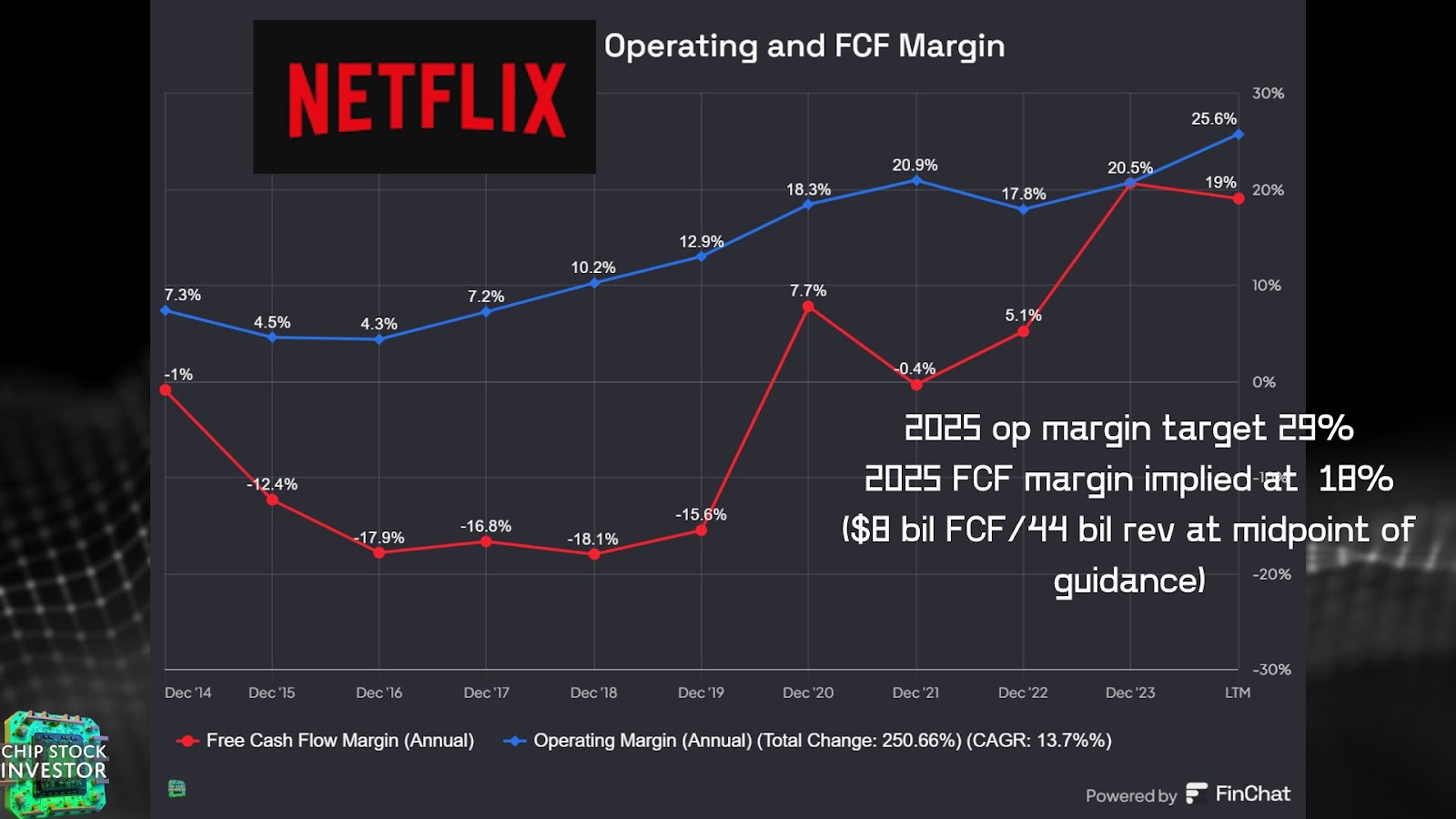

A bit more on the margin expansion story. Just a few years ago, Netflix was still operating as a young technology company generating little in the way of cash profit. That story has been closed. Operating income and FCF margins have soared, and especially op margin should have another field day in 2025 based on initial guidance from management.

Here’s a breakdown of how the company is arriving at its 29% op margin target for the new year, as per the CFO:

The case for Netflix being named a “tech giant”

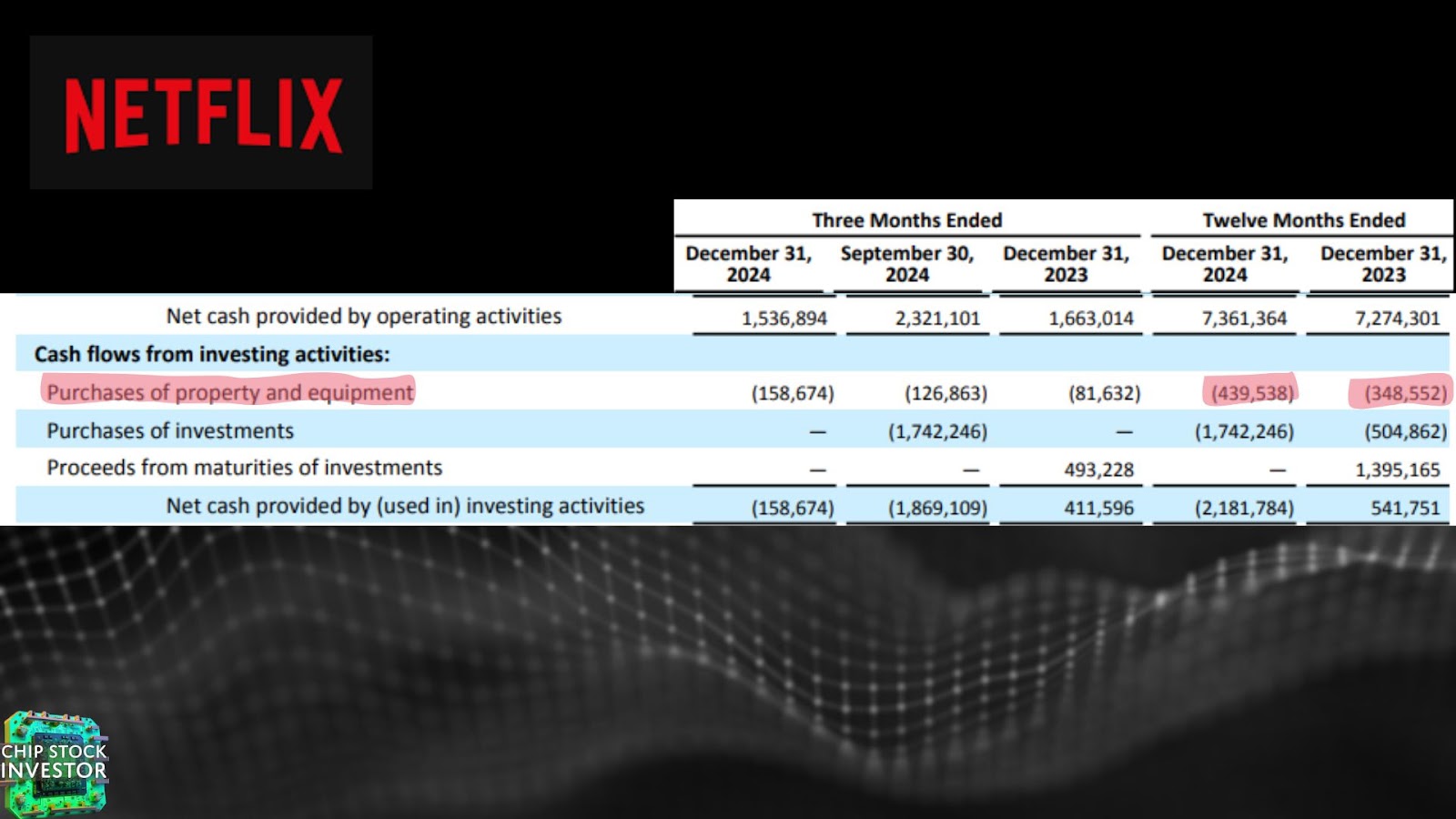

But there’s another expense weighing on the business short-term, especially showing up in the sluggish FCF growth expectation (just $8 billion, only marginal growth after flat FCF growth in 2024). Capital expenditures (CapEx), or spending on property and equipment.

What’s that CapEx for? A lot of it is likely the aforementioned ad portion of the Netflix business.

We mentioned Netflix just recognized two years of ad-supported lower-cost subscriptions, which it launched with the help of Microsoft’s ad server (definition of an ad server below). But Netflix has been busy building its own ad server, which we discussed a few months ago here on the blog and on our YouTube channel: https://youtu.be/re8FOz58x1k https://chipstockinvestor.com/the-most-obvious-digital-ads-investment-to-buy-hiding-in-plain-sight-netflix-nflx-stock/

As Netflix has expanded its content reach, it makes financial sense to bring the ad server in-house. The new Netflix ad tech platform is now live in Canada, is soon coming to the U.S., and will gradually expand to the other ad-subscription countries in the coming years.

Management has been explaining this in-house ad tech gives them more flexibility and creativity in cutting deals with content creators and managers (like the National Football League) and marketers (like a Kia ad partnership in South Korea with the debut of season two of Squid Game).

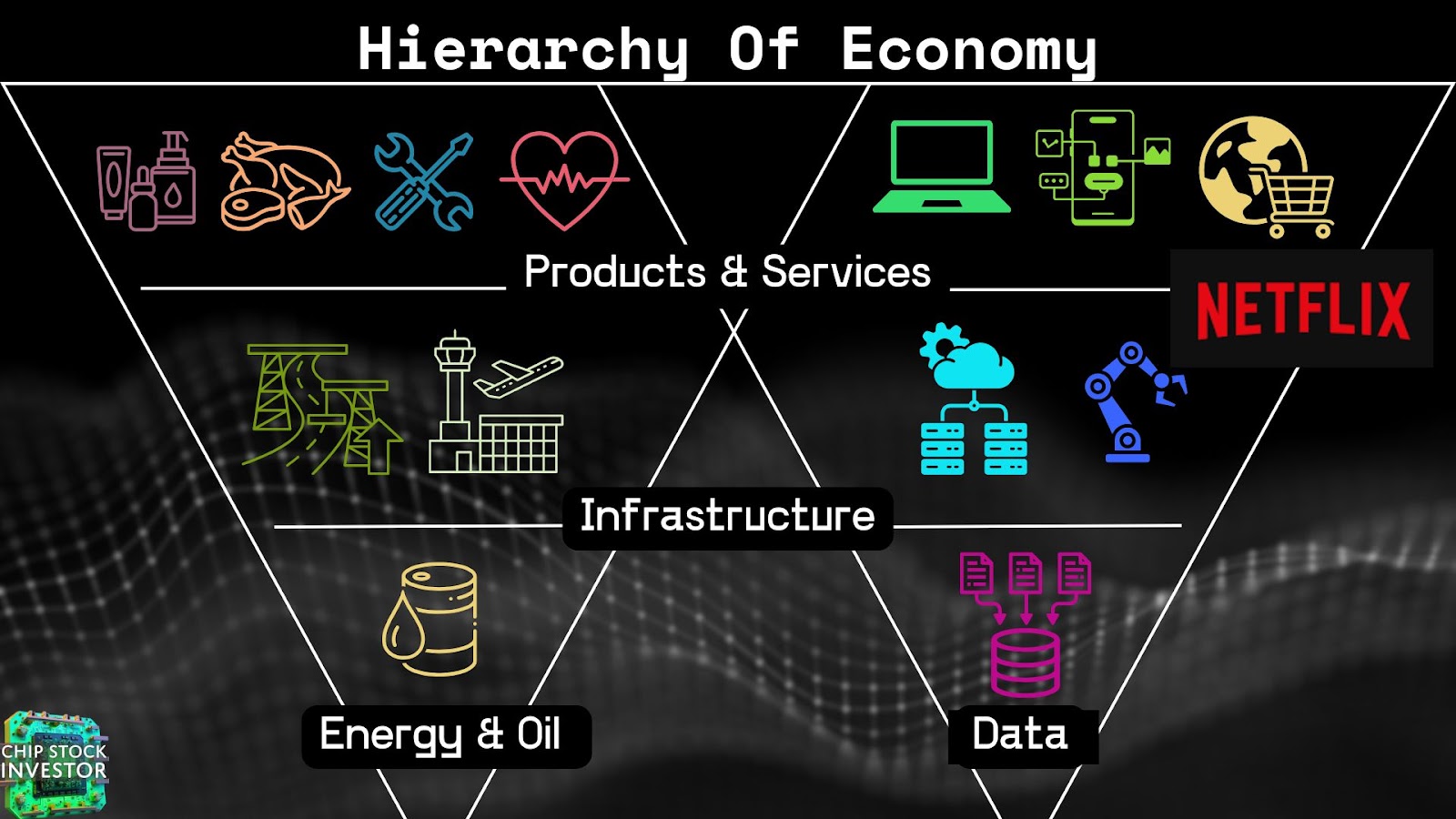

In other words, Netflix is building out more of its own infrastructure to manage and expand its slice of the very large and fast growing digital advertising pie. More than just a software-based media company, Netflix is taking a queue from other big tech companies and getting more into the self-managed data center equipment game. This explains the recent uptick in CapEx, which will likely sustain into 2025 and keep a bit of a lid on FCF conversion for at least another year.

However, as the other tech giants have proven for a couple decades now, vertically integrating across network infrastructure and end-market software is incredibly powerful. Netflix could have many years’-worth of fast profit growth ahead of it, just from the new ad business alone.

We’ve been discussing the digital ads industry more in-depth with our Semi Insider members (link to join here: https://ko-fi.com/chipstockinvestor/tiers). Below is one of our new charts breaking it down, where we explain all that confusing ad tech terminology.

Is it too late to buy Netflix stock?

Netflix stock is up significantly, well over 30%, since our last update. Surely the stock price is too hot to handle right now. Or is it?

Based on the guidance for mid-teens percentage revenue growth and more margin expansion, Netflix may not be as expensive as it appears. And if we factor for an eventual catch-up in FCF margin once the ad server spending starts to pay off, the valuation may actually still be closer to reasonable than not.

Here’s our updated reverse DCF (discounted cash flow). Bear in mind, a reverse DCF isn’t our outlook for Netflix’s profit growth. It’s one scenario (in our estimate, the most likely one) that makes the stock price a fair value to pay. When running these reverse DCFs, it’s now up to you the investor to decide if this scenario is a doable hurdle for Netflix to clear or not.

Our style here at CSI isn’t to chase hot stocks, and so we aren’t adding more Netflix at this particular time. But we’ll continue watching closely as 2025 progresses. Whenever a business valuation is elevated, there’s a higher chance of significant swings and corrections. Assuming the story doesn’t change, we’d consider it a buying opportunity for Netflix.

Stay tuned, we are steadfast in the belief that the digital ads market remains one of the most important for the semiconductor and AI industry in 2025 and beyond. Check us out later for more updates on other ad tech companies like The Trade Desk (TTD) and AppLovin (APP) when they provide their financial guidance for the new year.