It’s been almost a year since we did a public CSI video where we called out Ubiquiti (UI). At the time, everyone was worrying about tariffs if (then re-presidential-hopeful Trump) won the election, so we suspect not many watched this video to the end. (There was also some additional CSI Live coverage on Semi Insider at the time too.) https://youtu.be/iEDvfAWmZtA

We revisit UI infrequently, and for various reasons, never quite have room to buy ourselves. Hopefully our lack of saying “yes we’re buying UI stock” didn’t prevent you from adding this to a small-bet basket (seriously, we’ll keep saying it, our buys or sells shouldn’t be indicative of what you buy or sell, we’re not running a copy trade service, and certainly not portfolio management).

At any rate, let’s circle back to UI, because this continues to be a great, but oft overlooked, business that competes in the unified hardware/software market. And given that’s such a huge market, even a current enterprise value of ~$35 billion makes UI still sorta small in the grand scheme of things.

What does UI do?

Ubiquiti (a play on the word “ubiquity,” meaning something is present everywhere, in this case referring to the internet) provides small network and internet connectivity equipment, as well as a growing list of ancillary hardware (security cameras, smart home devices, etc.) and bundled software. Founder, CEO, and majority shareholder Robert Pera left Apple to start his company in 2005, and took a no-frills no-ads approach, targeting IT network power users and word-of-mouth growth.

Ideal customers primarily fit into the small internet service provider or small network engineer category, as well as other IT enthusiasts and small business owners worldwide.

Take a look at the company’s “what’s new” page for some ideas (https://ui.com/whats-new), as well as the lo-fi ad campaign targeted at their nerdy network architect customers. (Those some avid fans are also some of the harshest critics, ie. this Reddit forum bashing one of the ads! ???? https://www.reddit.com/r/Ubiquiti/comments/1dco6oz/meet_unifi_the_it_sales_model/).

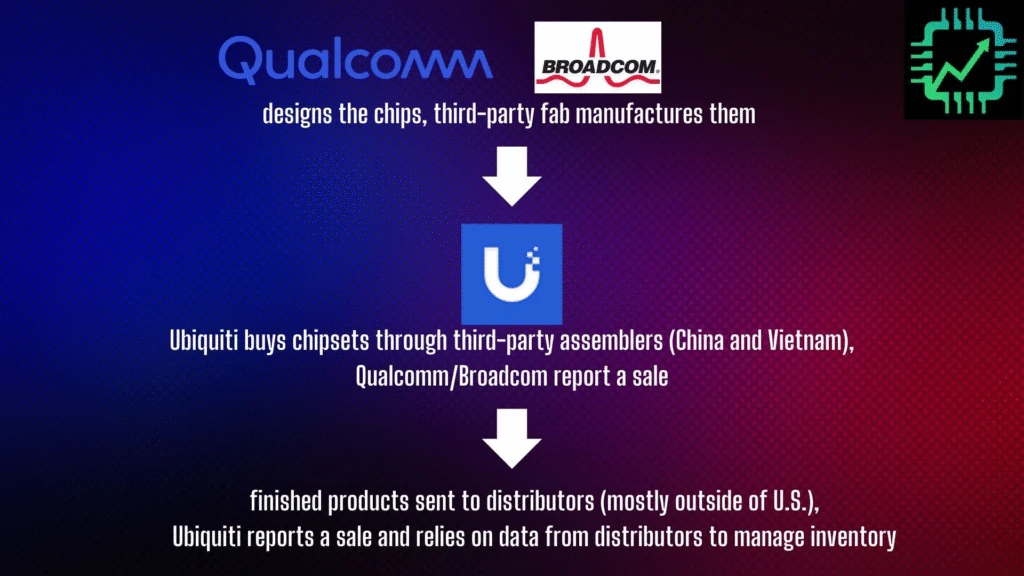

Anyways, in a nutshell, Ubiquiti buys chips and hardware from companies like Broadcom or Qualcomm, hires device manufacturers in SE Asia to finish the products, and then sells them to distributors or direct-to-nerd via its website.

For a better grasp of the business, UI has one of the shorter annual reports (10-Ks) out there at just under 90 pages. If you’ve never read an annual report without an assist from AI, give it a try. It’s a must-know-how skill. https://ir.ui.com/sites/ubiquiti-ir/files/2025-08/ubnt-06-30-2025-10k-2025.pdf

Continuing on, given this is a network hardware business targeting internet providers, local networks, and small biz IT departments, we can file UI into the “Enterprise” segment of our semiconductor end market sales chart. Enterprise has been showing signs of early recovery, and UI has been off to the races since our callout a year ago.

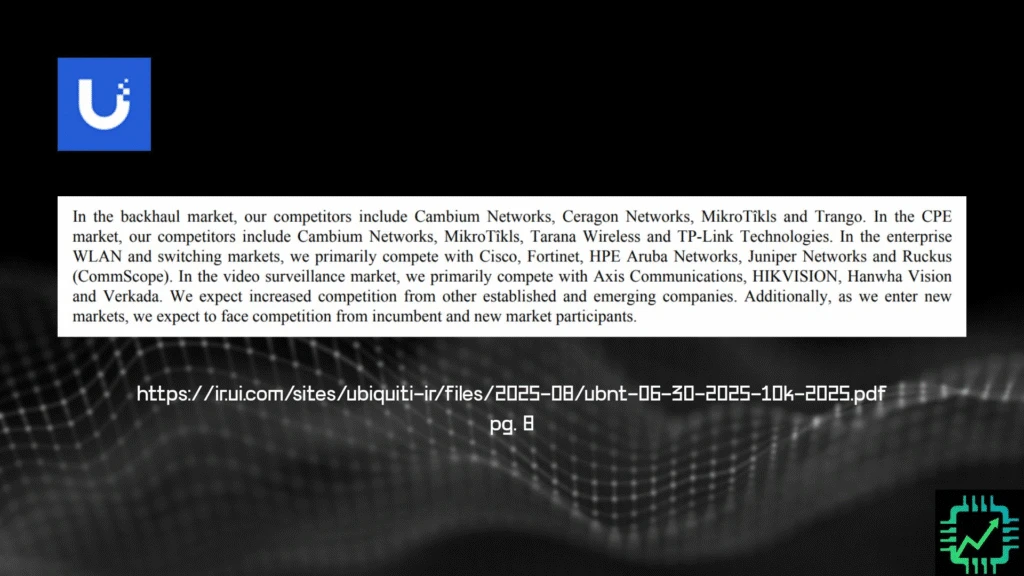

Competitors in these markets are numerous, and as you can see from the below list (pg. 8 of the annual report), there are some very large and very well-known names UI goes up against. And yet, they’ve made steady progress over the last 20 years since founding.

Fiscal 2025 financials

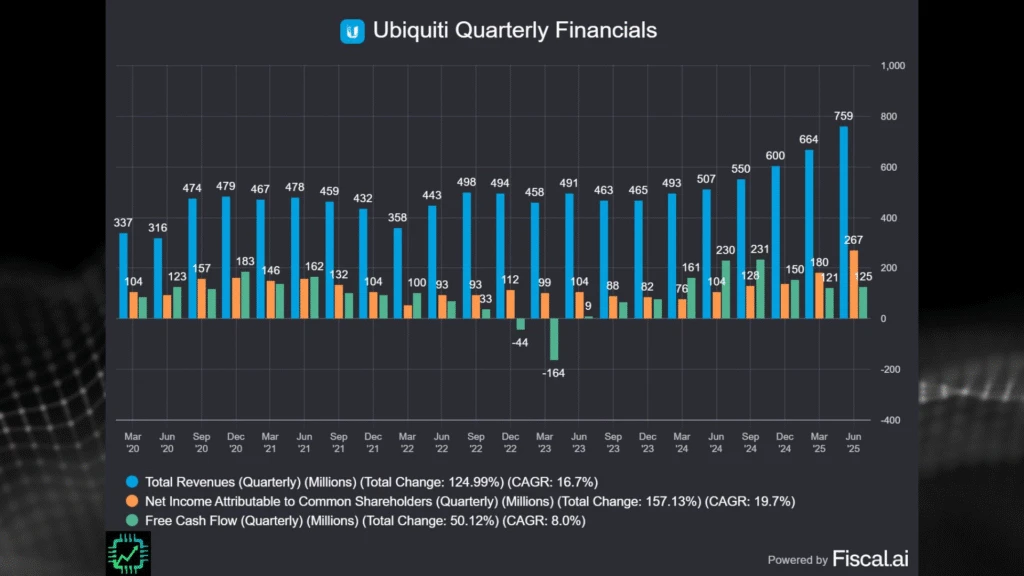

Fiscal 2025 was indeed a big bounceback year for UI as customer inventories normalized after the post-pandemic downturn. Paired with low inventory, customer demand has been on the rise again (normal bull market growth), and UI has been expanding its product portfolio. Fiscal Q4 revenue jumped nearly 50% YoY as a result.

GAAP net income more than doubled YoY, while the more lumpy FCF metric (note this high FCF we called out last year due to inventory burn off) was down by half.

Seriously check out Fiscal’s research platform if making visuals like the one above is your thing. And get 15% off any paid plan using our link! Fiscal.ai/csi

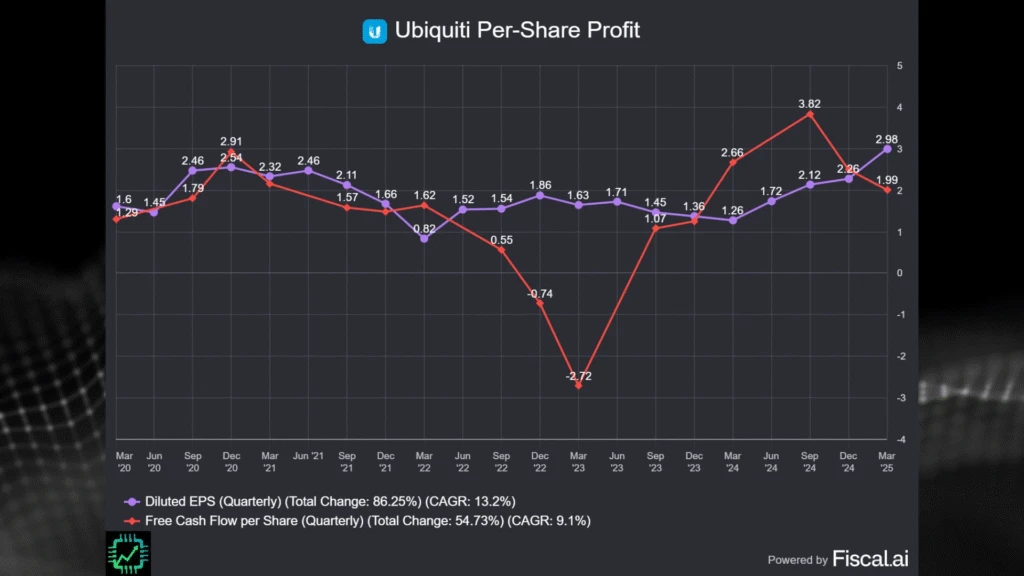

We’ll circle back to the FCF-per-share at the end of this article, but do note the gradual growth in GAAP EPS and FCF-per-share over the last five years despite some wild times from the pandemic, a multi-year downturn, and the start of a new growth cycle this last year.

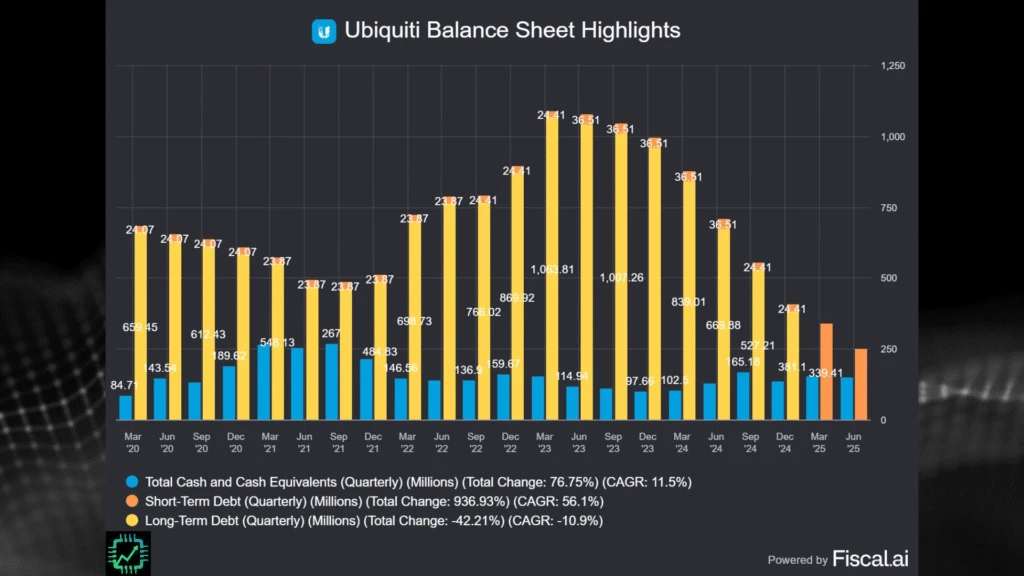

Also of interest, UI took out a lot of debt during the last downturn to bridge what it thought would eventually be a temporary decline is fortunes.

Pera and company were right, and have been using ample FCF in recent quarters to pay that debt off. Only $250 million remained at the end of fiscal 2025, which matures later this year. We’d expect management to continue to pay this amount down, perhaps in full from positive FCF generation. However, we can’t say for sure, given Pera and his management team have not hosted any quarterly earnings calls in many years. Pera has a particular disdain for Wall St. sell-side analysts, it seems, and has said in the past his time is better spent building his business than pandering to short-term investor whims. Bold talk, but not sure who’s arguing with him right now.

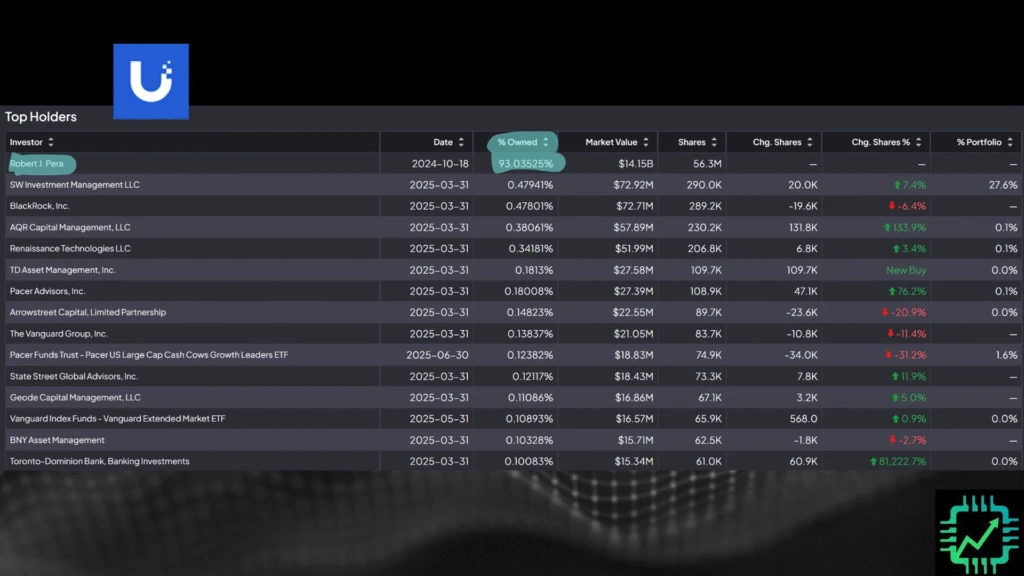

Which brings us to another UI particularity: Pera himself owns 93% of the stock. Yes, 93%! Talk about insider ownership. And given UI has repurchased a lot of stock over the years, Pera’s ownership has continued to creep towards 100%. Will he just buy out the rest of the company at some point and take it private? He certainly could. (Pera’s net worth is hefty; you might also happen to know him as the owner of the NBA’s Memphis Grizzlies.)

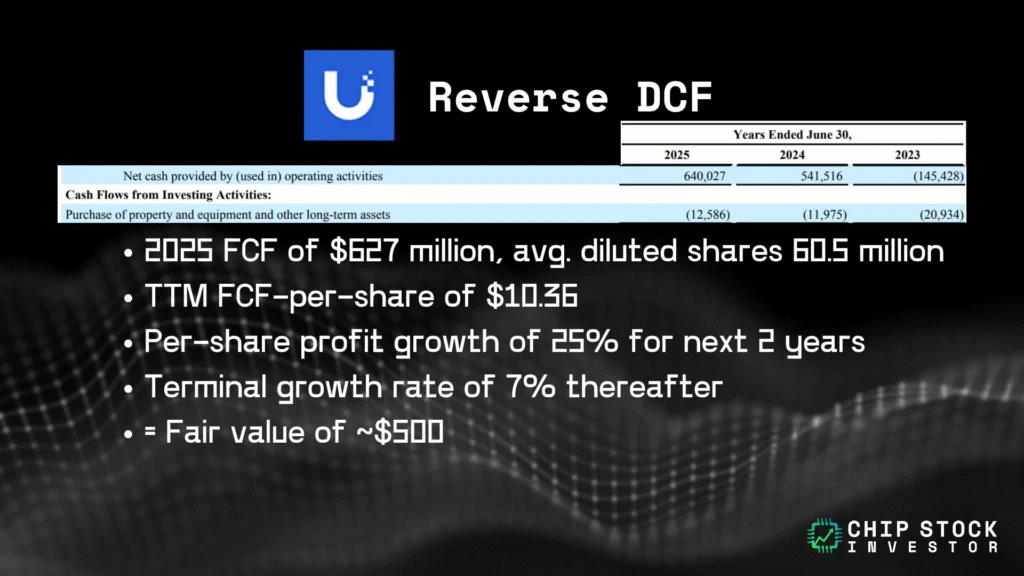

As for valuation, we’ll let you look up those numbers (P/E, P/FCF, PEG, whatever) as you wish. But here’s our reverse DCF to try and gauge what kind of expectations the market has baked into the current stock price. We’ve penciled in 25% FCF-per-share growth for 2 years (business is cyclical, after all), and a terminal growth rate of 7% thereafter (yes, it’s high, but as a reminder, the market does not use GDP as a long-term discount rate in valuing businesses, so we don’t either when doing a reverse DCF).

Based on this alone, UI still looks pretty compelling to us, if you believe the network hardware growth cycle has some legs under it for some time. But even then, though UI is cyclical, it has been growth cyclical for a long time now. And Pera has found numerous ways to deepen relationships with customers and expand into new adjacent markets. Do some digging on this one, if you haven’t before.

2 Responses

After researching this business, I’m smitten. Talk about skin in the game, I’m actually ok with the 93% ownership.

Great snapshot. Thanks for the easy-to-understand analysis.