The following is a Marvell Technology Group (MRVL) summary of several posts from Chip Stock Investor’s Semiconductor Insider over the last few weeks.

Why do a review of Marvell Technology Group now? Besides being over a year since our decision to begin selling and re-allocating some of the proceeds into more Broadcom (AVGO)(see the last video on that decision linked above), we’re also at a new inflection point for the semiconductor industry – Marvell included.

Also, we just got around to reviewing the MRVL fiscal year 2025 annual report filed a few months ago…

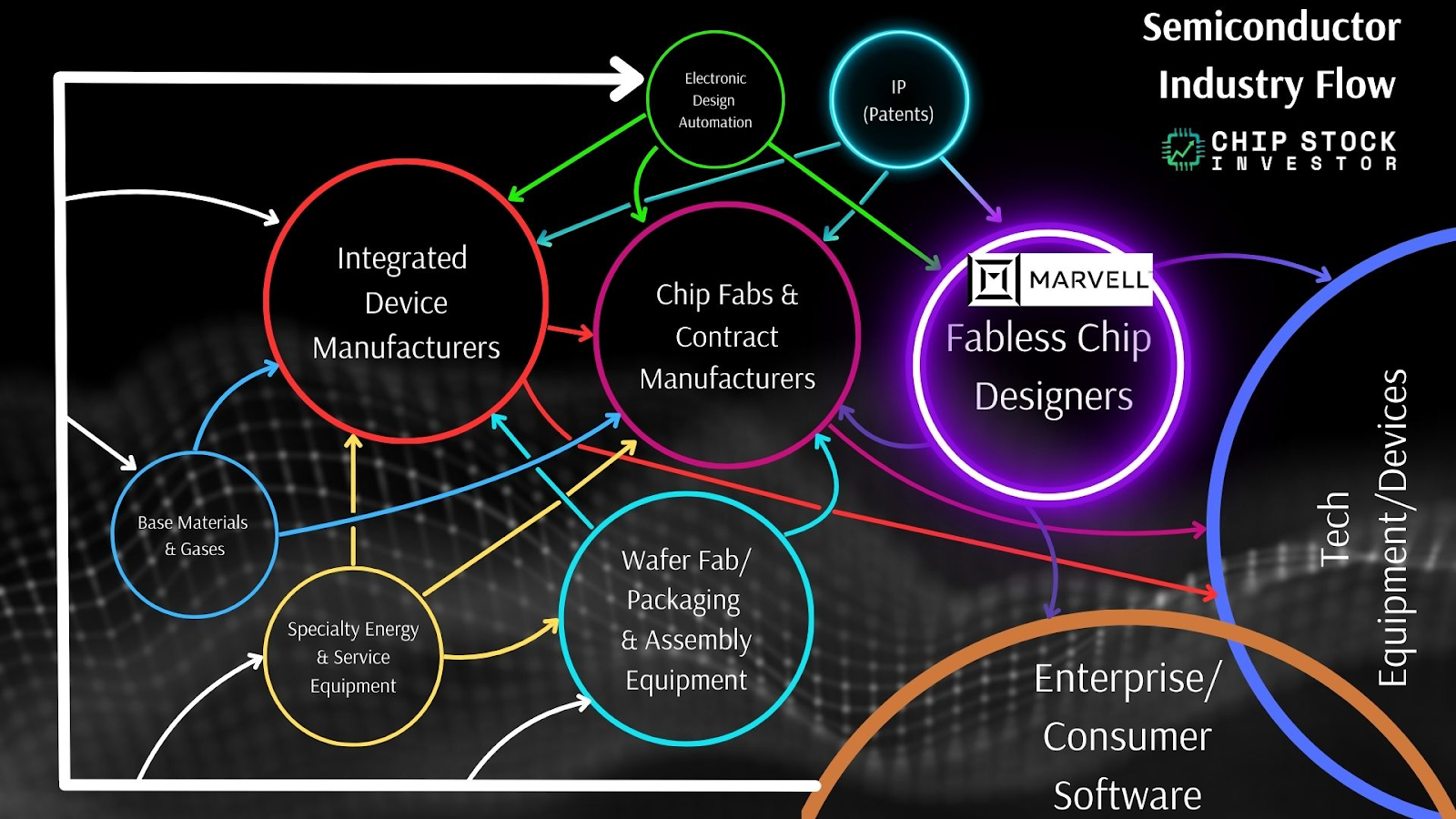

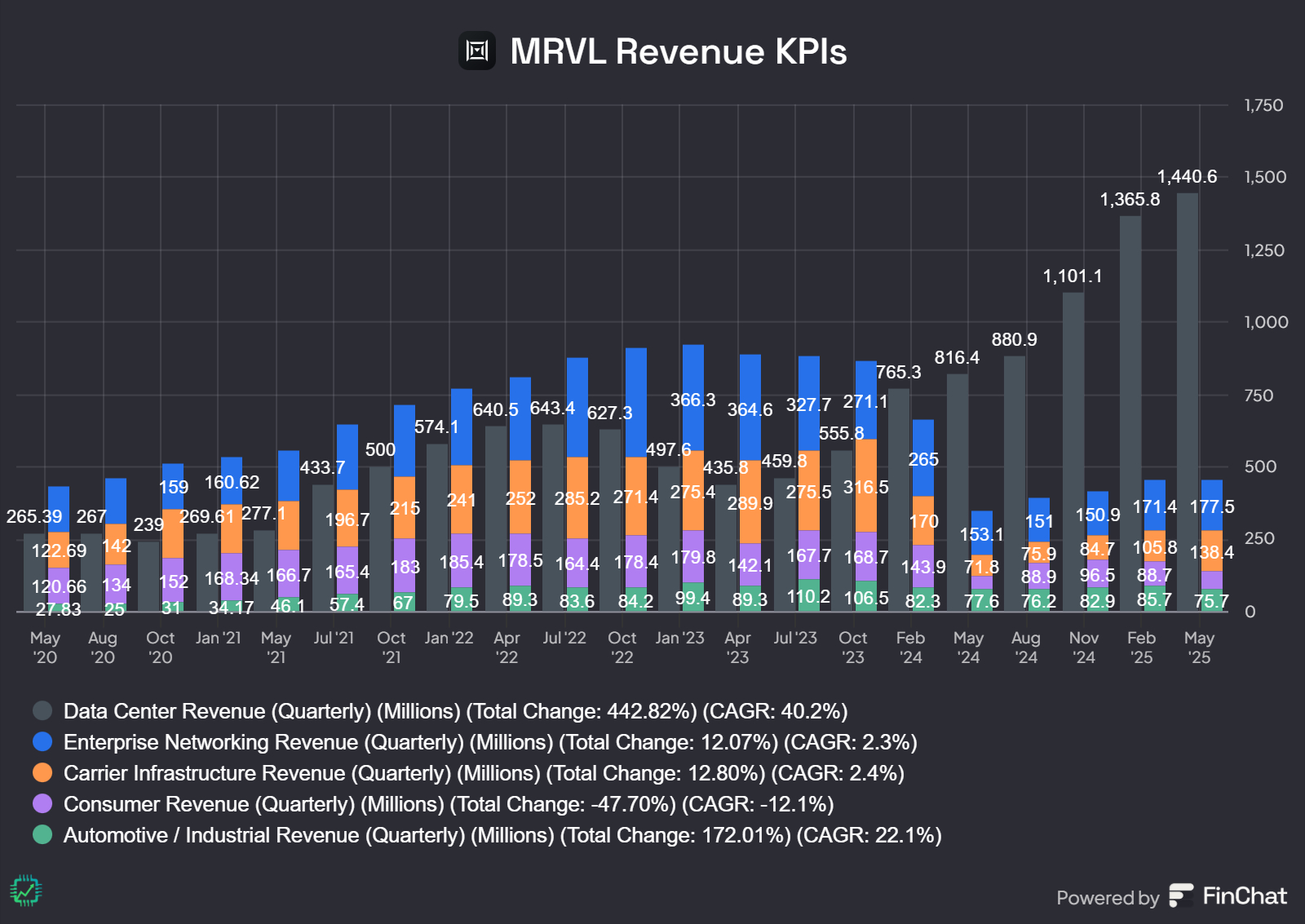

Anyways, Marvell is a fabless chip designer and extensive owner of semiconductor IP – especially for data centers and enterprise computing. In fact, Marvell has been undergoing a massive pivot in recent years, and paired with a near-across-the-board decline in its other end markets (like auto/industrial), data centers comprised over 70% of revenue in fiscal year 2025 (12 months ended in January 2025).

If you’re wondering, no we are not going to buy MRVL stock. But that’s simply because we don’t have a need for it in our portfolio. Your portfolio is naturally going to be different, so don’t skip the update simply because Chip Stock Investor isn’t buying right now.

So… what went wrong for Marvell the last couple of years?

It’s less a matter of what went wrong in late 2024 and early 2025 (the share price boom then bust culminating in April), and more a matter of what went wrong starting about 5 to 7 years ago.

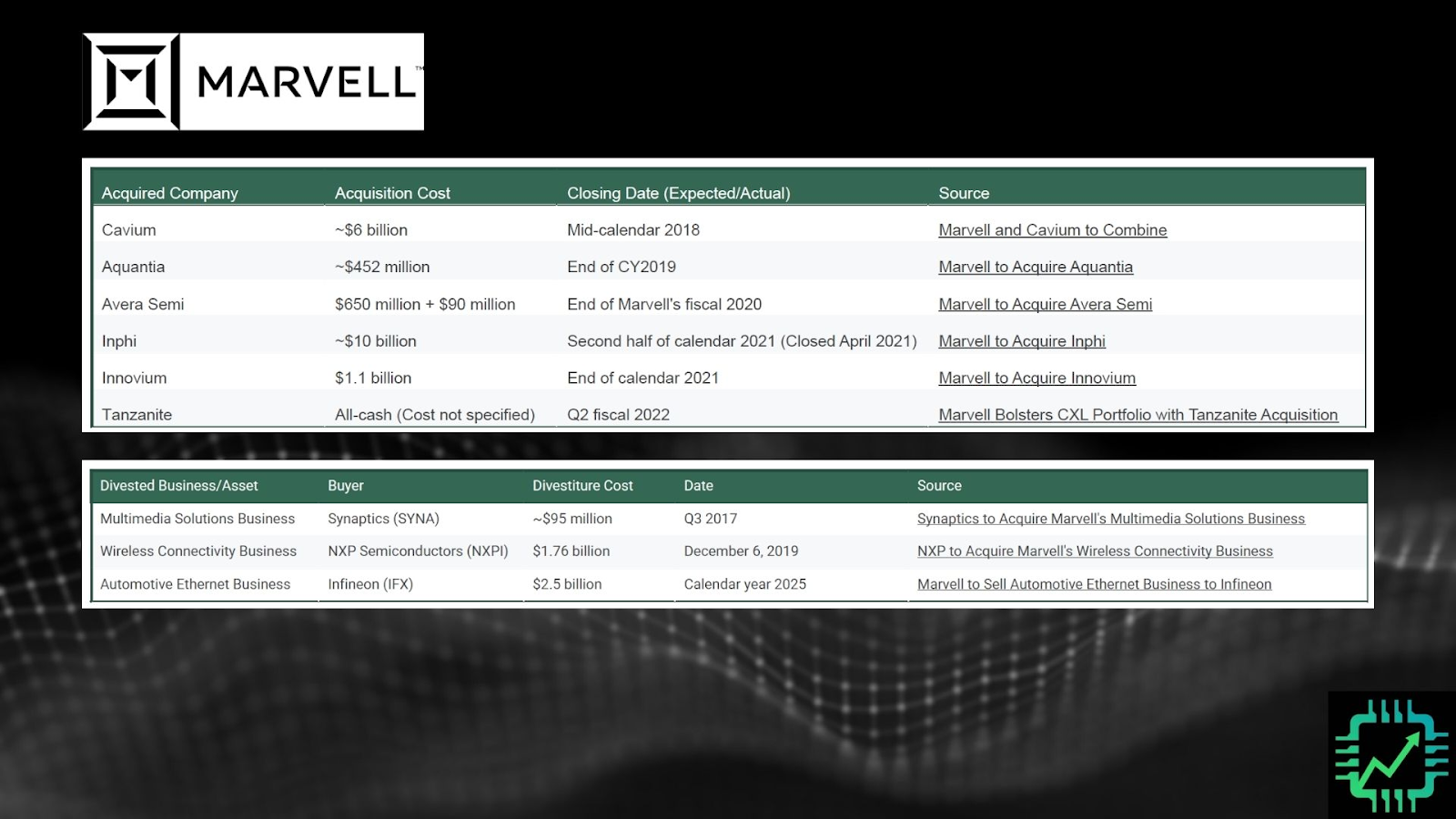

Marvell wasn’t a great business when current CEO Matt Murphy took over in 2016. But starting in the late 2010s, after some legal issues had been cleared, Murphy started going on the merger and acquisition hunt. The purchase of Cavium, an Arm-based processor designer for networking systems, is when we began following Marvell and made our initial investment.

But Cavium was just the start of Marvell’s big bet on high-performance networking and compute. The biggest acquisition was optical networking systems and component designer Inphi, completed in late 2021. Paired with a couple divestitures of older and commoditized assets, Marvell had all the pieces in place to compete in networking for what we now know as “AI data center infrastructure” and “custom silicon” (aka. ASICs, or application-specific integrated circuits).

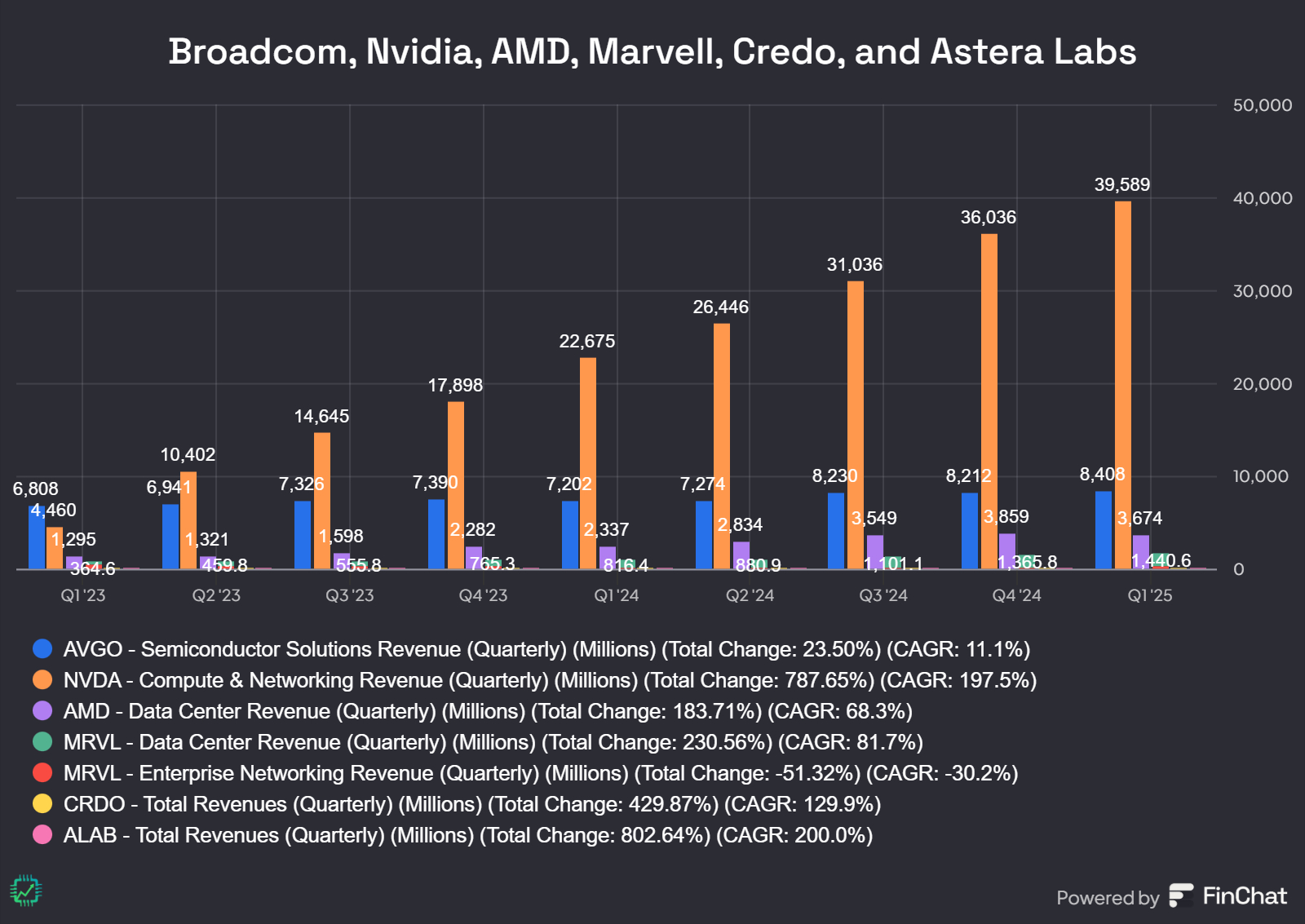

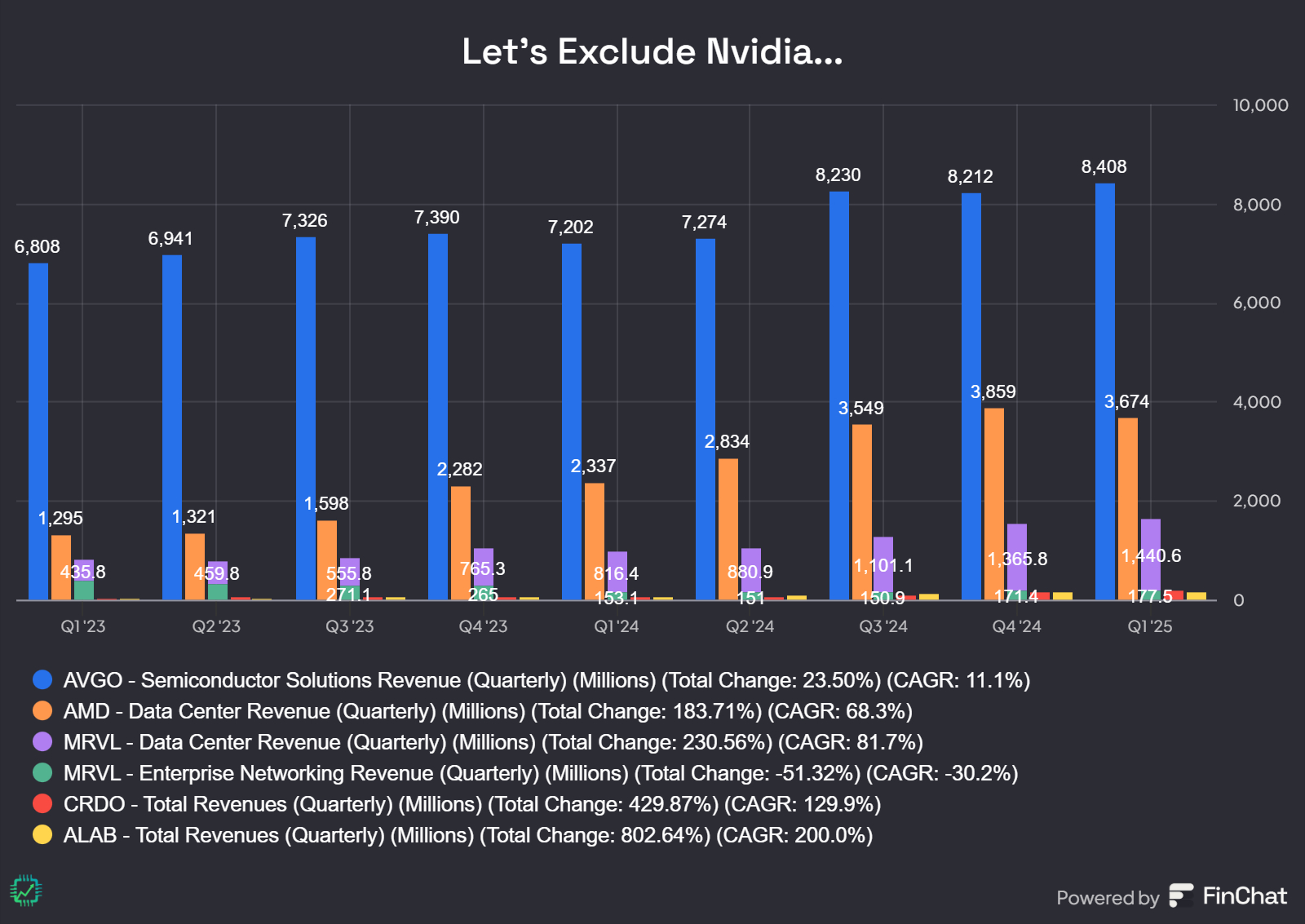

With these assets now in-house, this is about the time we started calling Marvell “baby Broadcom” – of course, minus Broadcom’s big infrastructure software business.

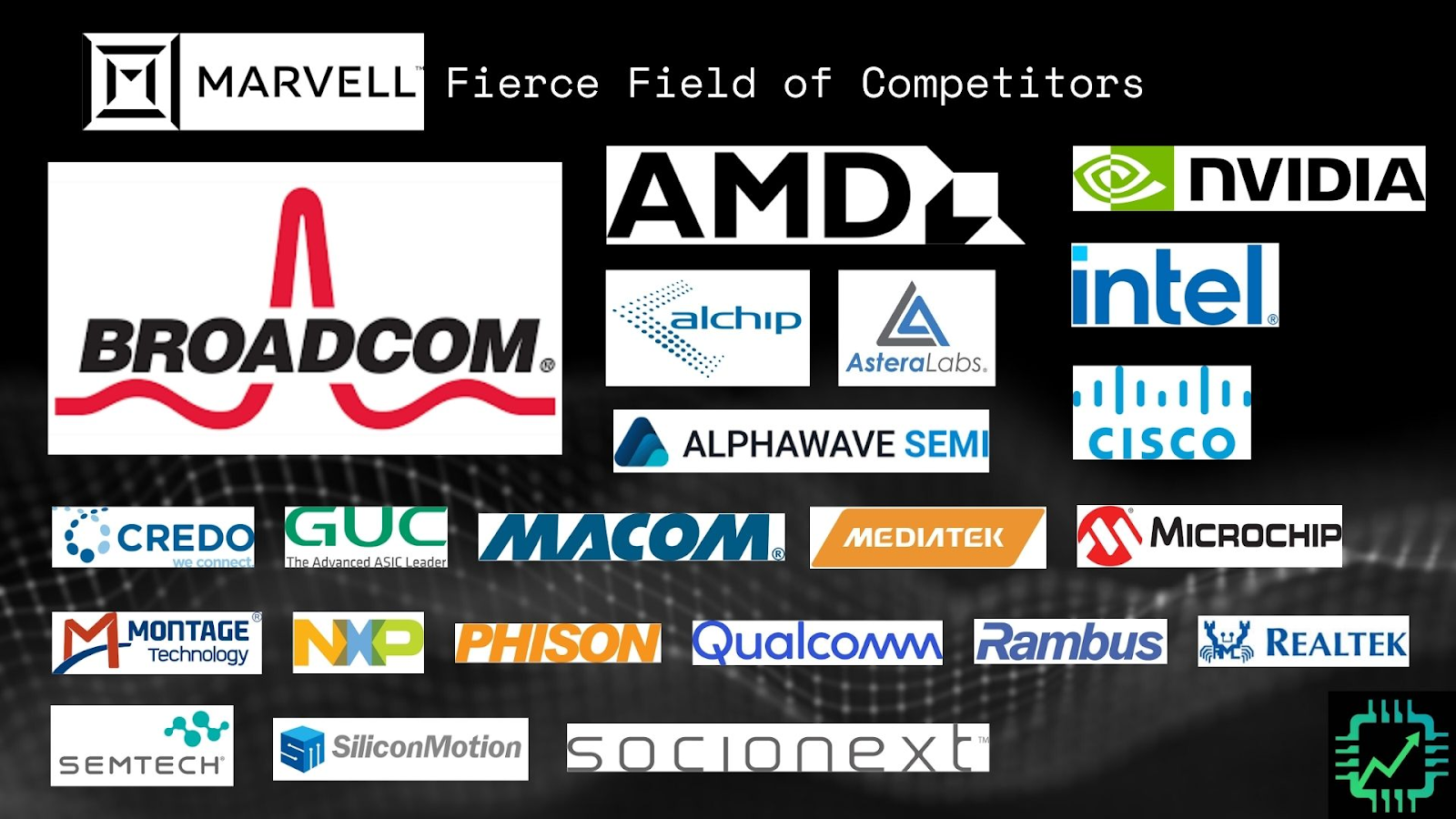

The problem, though, is Marvell’s pivot to the data center market put it in competition with a fiercely competitive field of players. Even before “AI,” data centers were a massive market worth upwards of a couple-hundred-billion-dollars per-year in spending. And in this market, as is the case with any business, players with large scale and diversified products (Broadcom) do really well. Everyone else can end up fighting for scraps, which often also means spotty profitability.

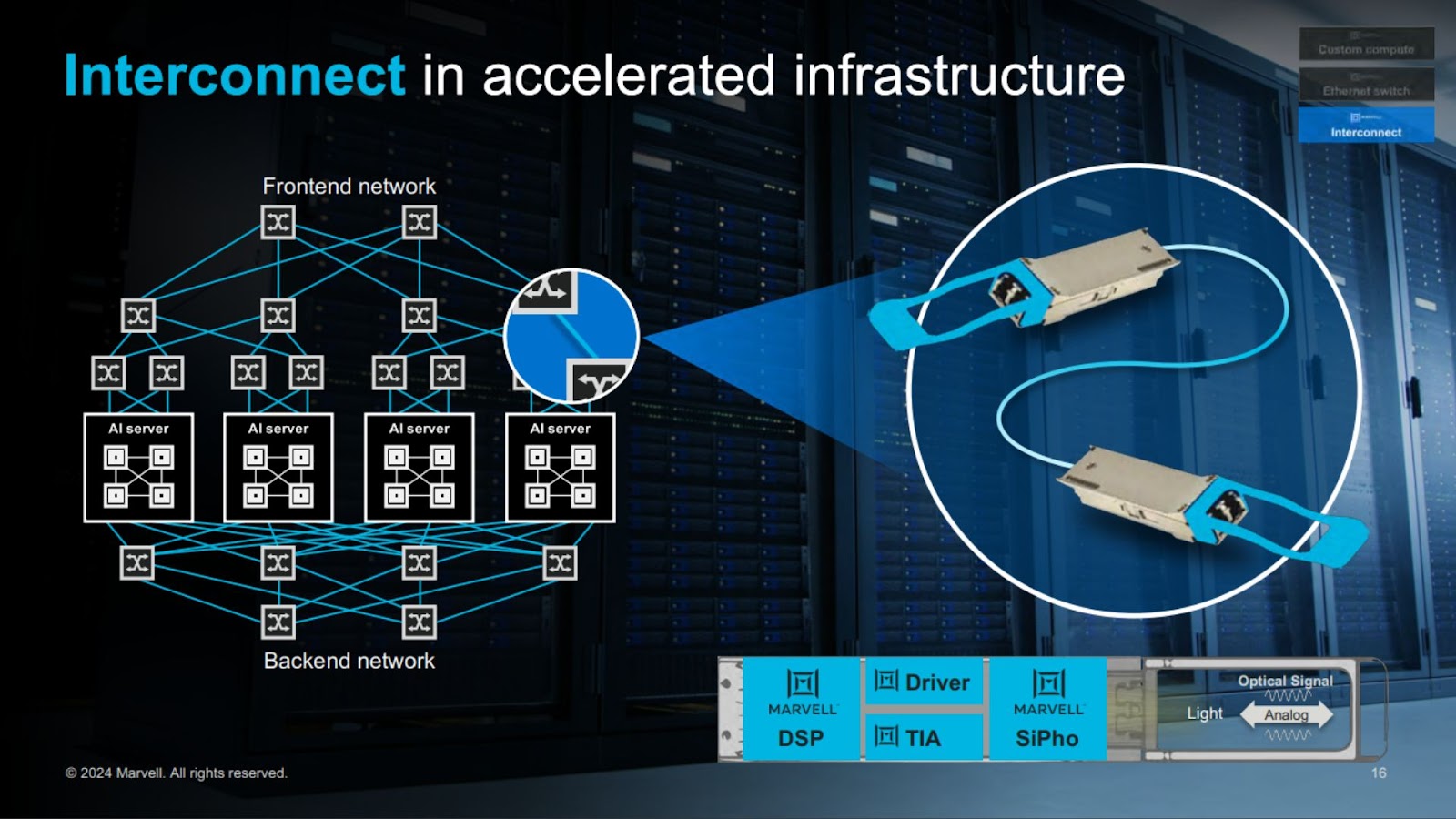

To illustrate the competition, we can pick up on Marvell’s own description of its two broad key product types from the last annual report: Interconnects and custom ASICs.

1. Interconnects (for data center and AI networking)

Coherent-lite DSPs (digital signal processors) for distributed campus data center interconnects.

CPO (co-packaged optics) solutions leveraging advanced silicon photonics, integrating numerous components into a single device for next-gen data center compute and connectivity.

LPO (linear pluggable optics) chipsets for short-reach, compute fabric connectivity in AI datacenters.

AEC (active electrical cable) DSPs for high-bandwidth copper data transmission in AI and general-purpose server connectivity.

PCIe (peripheral component interconnect express) retimers leveraging PAM technology for high-bandwidth copper and optical PCIe data transmission within server systems. (A Pure-Play Bet On Nvidia Blackwell Growth? Astera Labs (ALAB) Deep Dive)

What are all these interconnected parts and pieces? Think of them like the building blocks of freeway interchanges, connecting different parts of road and handling the flow of traffic. But instead of cars, the traffic in this case is digital data – for things like training new AI, or operating AI once it has been deployed in a software program (inference).

These various chips are used by network server companies – like Arista Networks (ANET), for one, a top Broadcom customer – to increase the number of lanes and increase the speed limit of the “roads” within the data center (the copper and optical cables that hook up all the servers to each other).

2. Custom ASICs

Then there’s the XPUs, or custom accelerated computing processors (a type of ASIC) that “compete” with Nvidia. These are the engines of the data center that process the data, either for training or for inference.

Much like Nvidia and Broadcom, Marvell ASICs and XPUs can be co-packaged with the networking chips to improve system performance. Marvell’s advanced 2nm generation platform (manufactured primarily by TSMC) and innovations leveraging backside power for 2nm and below architectures are coming. They also include “co-packaged optics (CPO) and custom high-bandwidth memory (HBM)” in the IP portfolio, an area dominated by Broadcom, and a key technology Nvidia is working on too.

See our Broadcom notes from March 2024 where CPO and ASICs were discussed at length. Nvidia’s new NVLink Fusion will enable them to monetize more of this “custom silicon” data center development. Does Broadcom’s AI Event Spell Trouble For Nvidia Stock? (AVGO & NVDA)

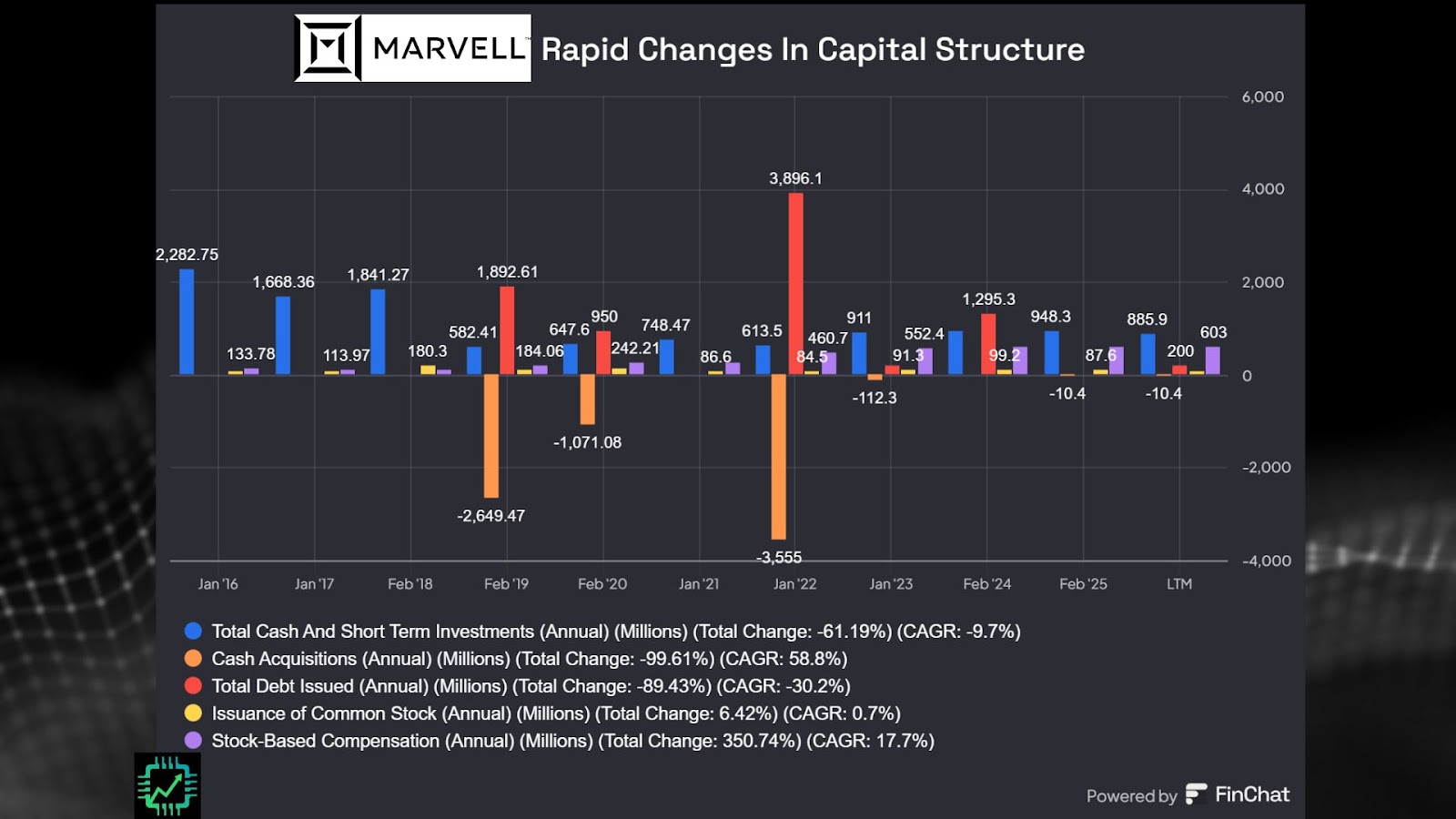

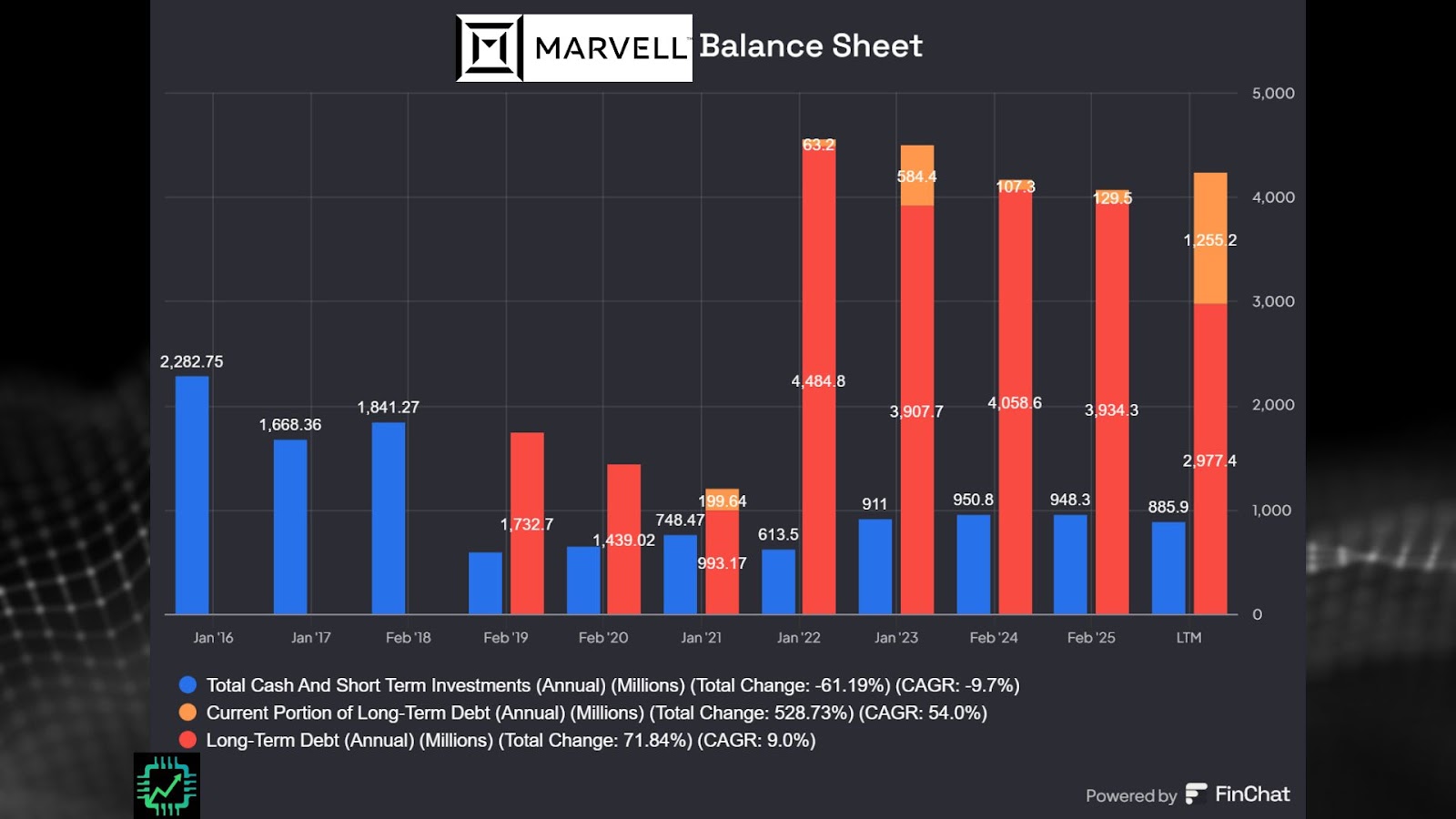

Marvell’s pivot was costly to the capital structure

The shift to data centers by Murphy and team was prescient, but also costly given how diminutive Marvell was in the late 2010s (like… no one was covering Marvell when we started writing about it, let alone did anyone know the name; at the time, investors were like “oh Marvel, superheroes…”).

In addition to piecing together the IP to be able to compete, Marvell then had to deal with the pandemic digital economy boom-bust, then the Fed interest rate hike cycle of 2022-23, and finally the general chip market decline that started in 2023 (basically, everything was down except accelerated computing).

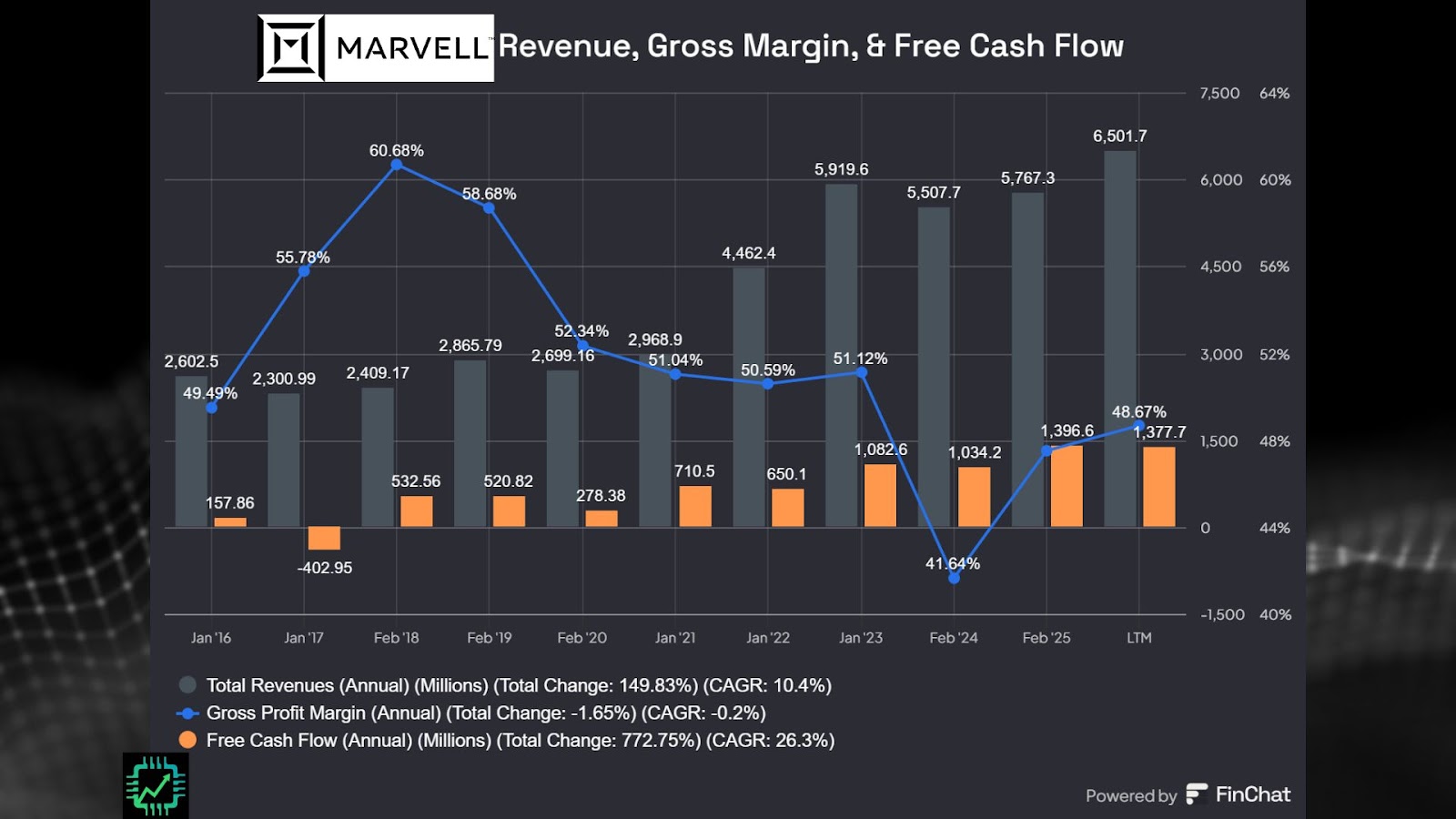

You can see this wild roller coaster reflected in the revenue, and especially gross profit margin.

We use Finchat.io for business-level research and for visualizing financials. Get 15% your own paid plan using our link! Finchat.io/csi

Nevertheless, the acquisition streak was expensive. Ample amounts of debt were raised, especially for Inphi. New stock was issued to help pay the bills. And new employees also needed to be paid (including in stock) as the acquisitions were gradually integrated and “synergized” (cost-cutting).

The result? The balance sheet has been inverted from what a healthy high-growth company ought to look like (with lots of interest expense to go along with it). The most recent announced sale of the automotive networking business to Infineon (IFX) for a couple billion dollars will help straighten things out – as well as further narrow Marvell’s focus on just data centers.

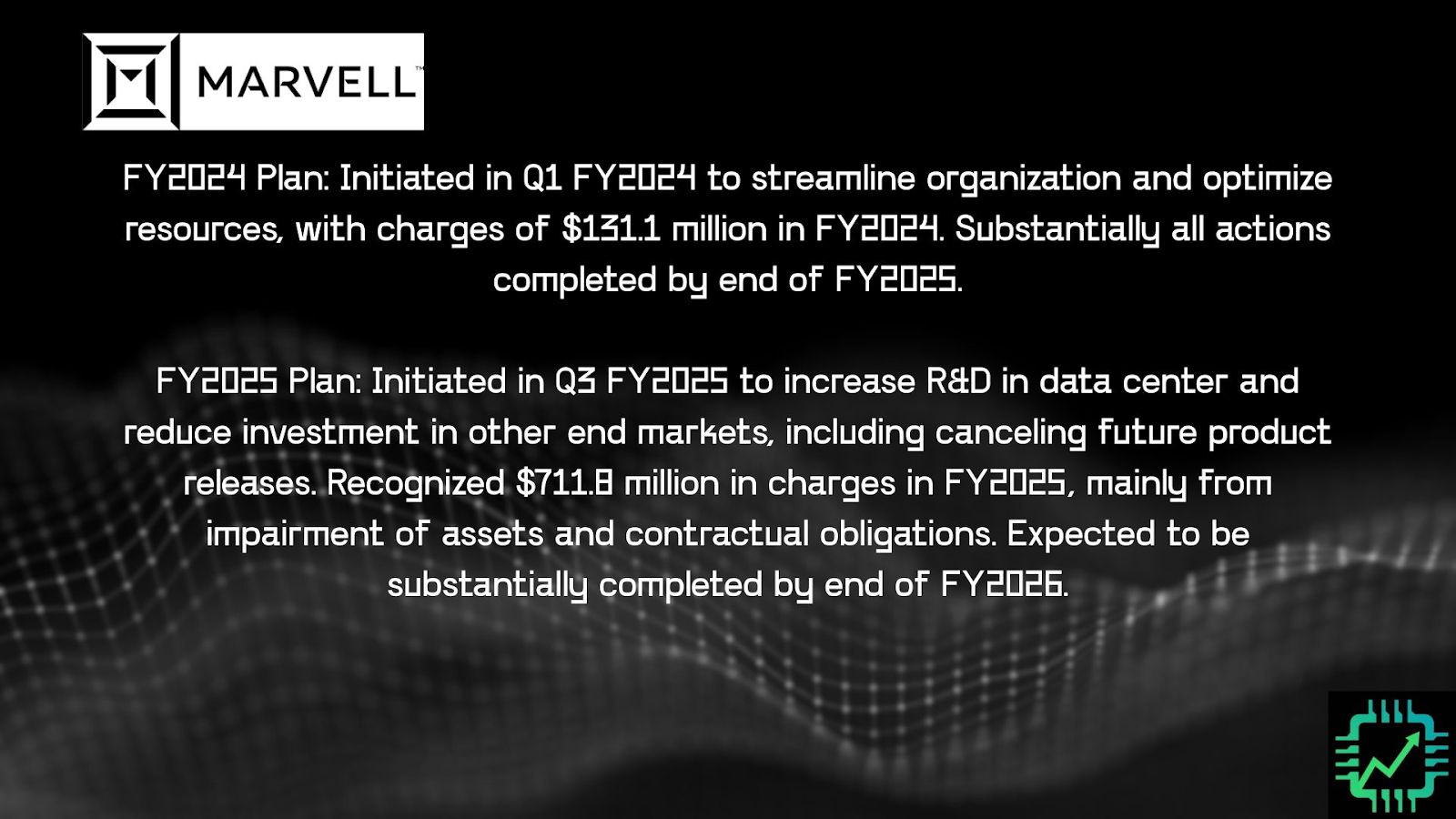

Oh and two more things. In the midst of Marvell’s data center business scale up, it initiated two re-organization plans (synergizing…) that racked up some severance expenses and non-cash impairment charges (they overpaid for some of the acquired assets).

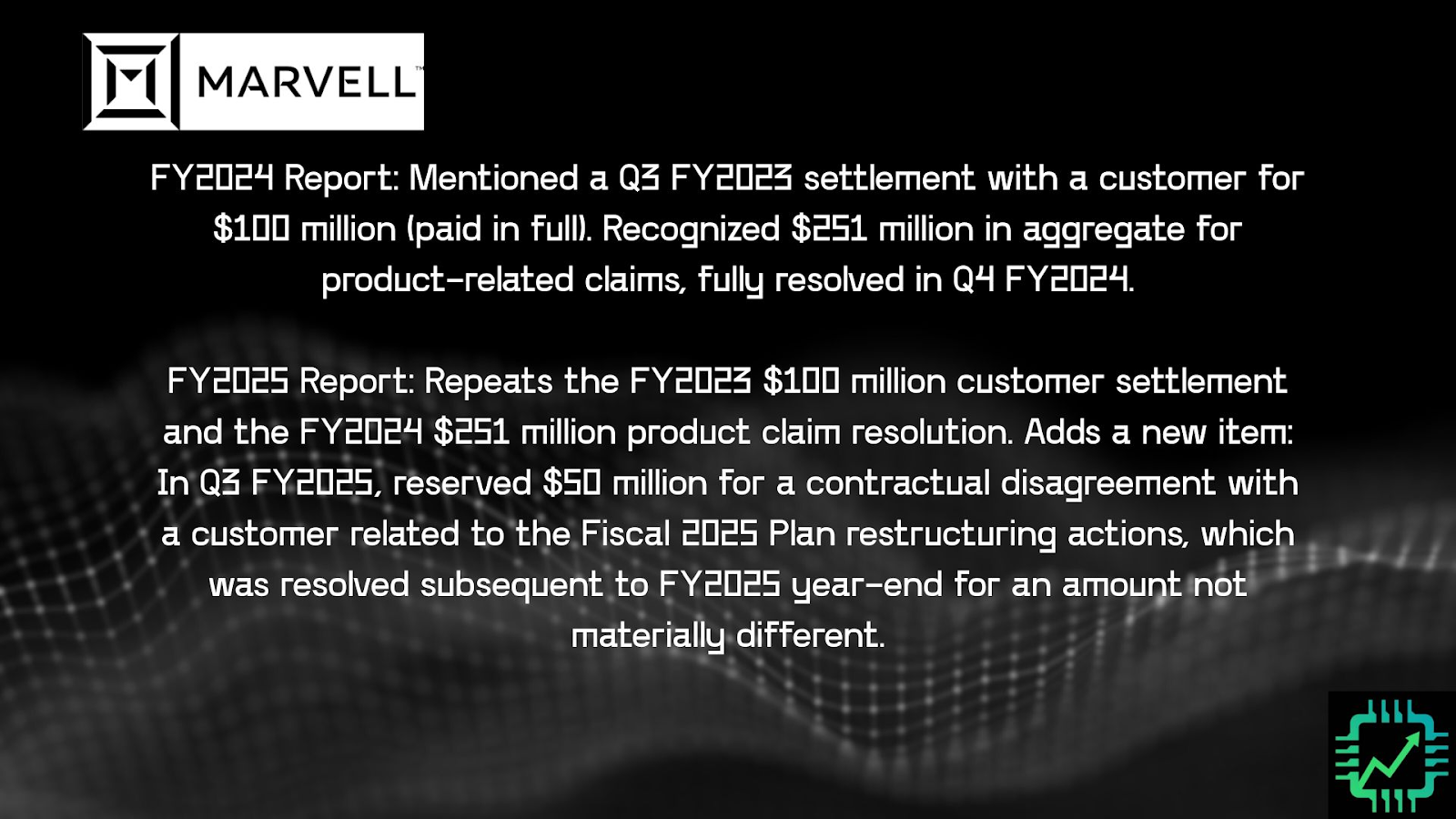

There were also some product disputes (likely with a big data center customer, Microsoft or Amazon perhaps?) that led to Marvell settling some contract disputes. One of these charges was related to the “synergy plan” as well, perhaps indicating a Marvell design team got axed and the company wasn’t able to deliver on a prior agreed-upon design obligation.

It seems these items are now complete, and as far as the 2025 annual report indicates, neither should be a recurring issue in the current fiscal year 2026.

All of the above issues and Marvell’s longer-than-expected payoff on the acquisitions is why we decided to re-allocate that position to AVGO last year.

What happens next? Q1 fiscal 2026 and expectations

If you like Marvell, bear in mind that Nvidia eats first, followed by Broadcom, and then leaving maybe AMD and Marvell and others to clean up the crumbs. That’s saying something, because as we discussed over on Semi Insider, three-quarters of Marvell’s revenue is now directly tied to the data center end market – and it’s not like Marvell is a small cap up-and-coming disruptor. And remember, later this year when the Automotive Ethernet biz is sold to Infineon, data center will become an even bigger portion of Marvell’s dinner.

Here’s Marvell’s updated segmentation. Total revenue grew 63% year-over-year (YoY), driven by the 76% increase in data center sales (including hardware for AI):

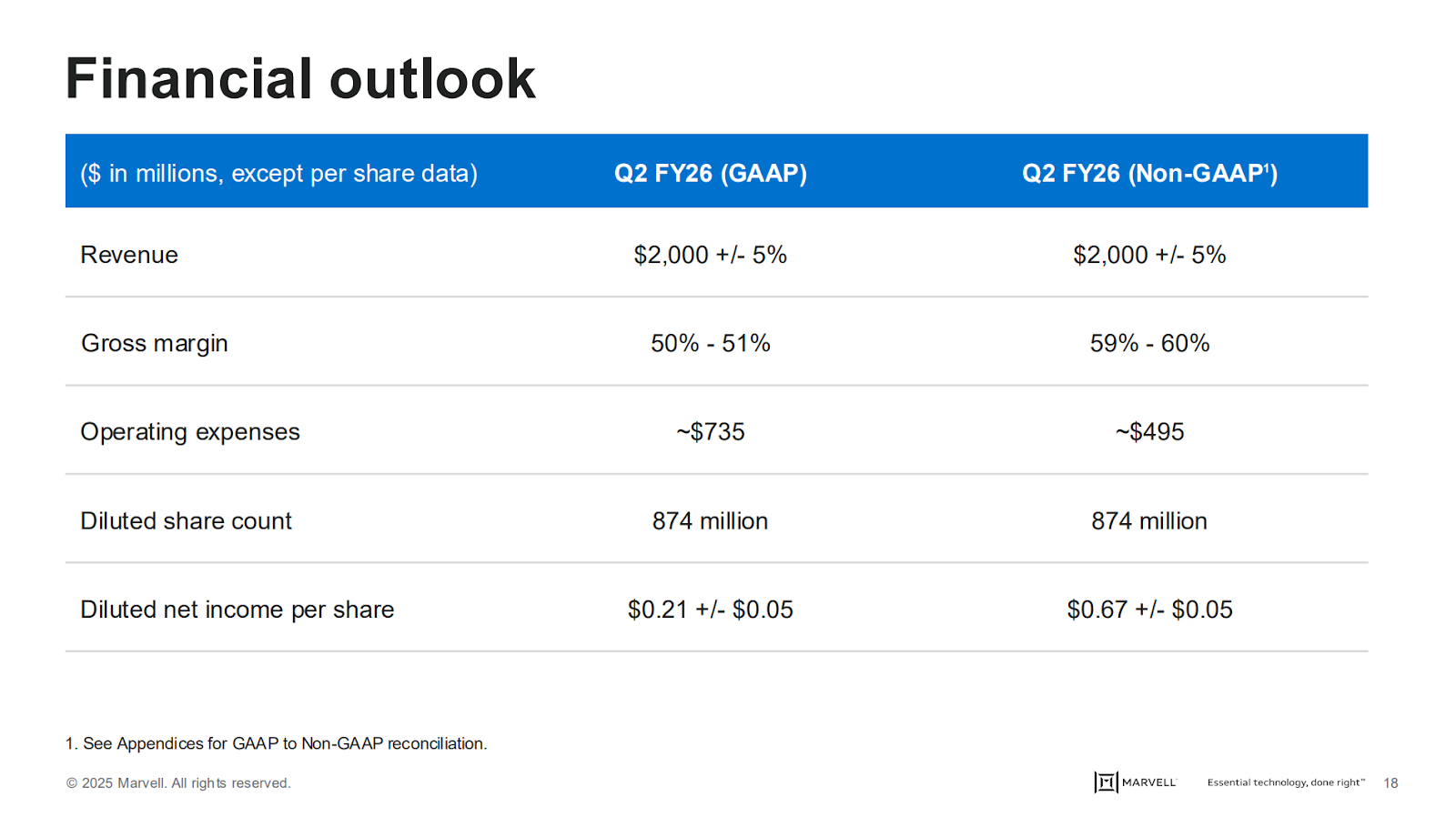

When it comes to valuing Marvell, as per usual the future guidance is far more important than previous quarter results. Below is Marvell’s outlook for Q2. The top-line number says it all: Revenue growth of 57% YoY implies a sequential slowdown (vs. 63% YoY growth in Q1). Will Nvidia’s Blackwell ramp-up help Marvell re-accelerate the second half of this year as well? We’ll see.

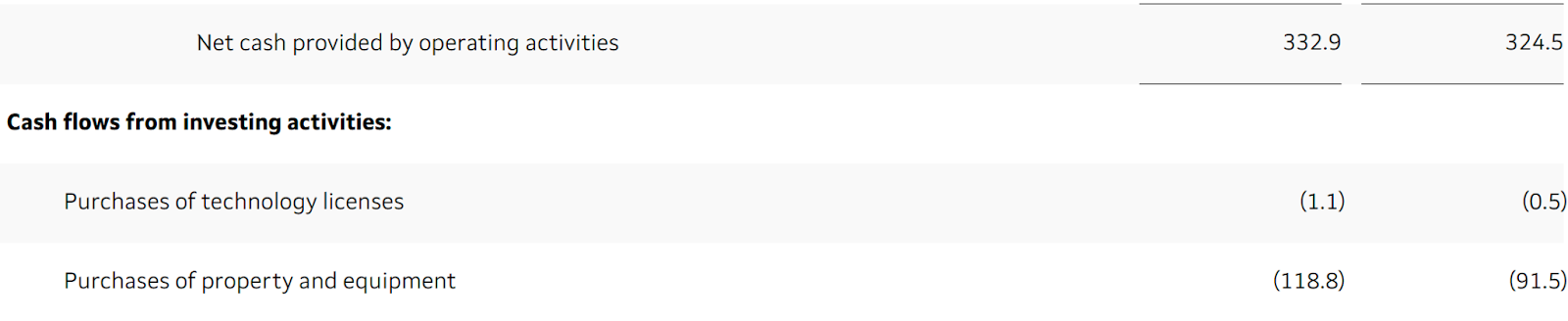

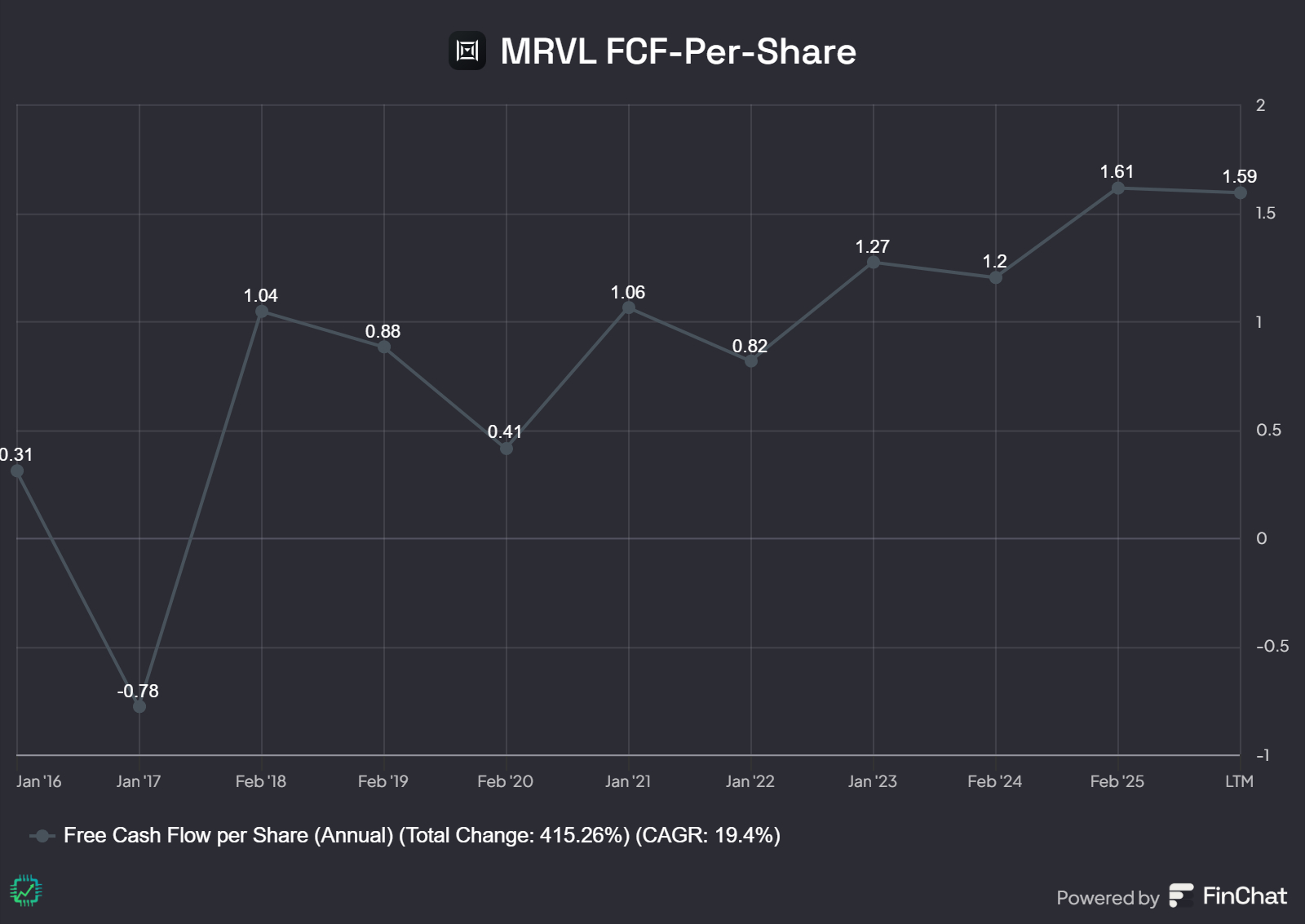

Another reason for some investor angst, free cash flow (FCF)-per-share of $0.24 in Q1 was down from the $0.27 in Q1 last year. Blame higher R&D and CapEx compared to a year ago. We’re also still lapping some of the restructuring charges outlined in our last update that Marvell announced last year. But the FCF-per-share metric could also be about to accelerate.

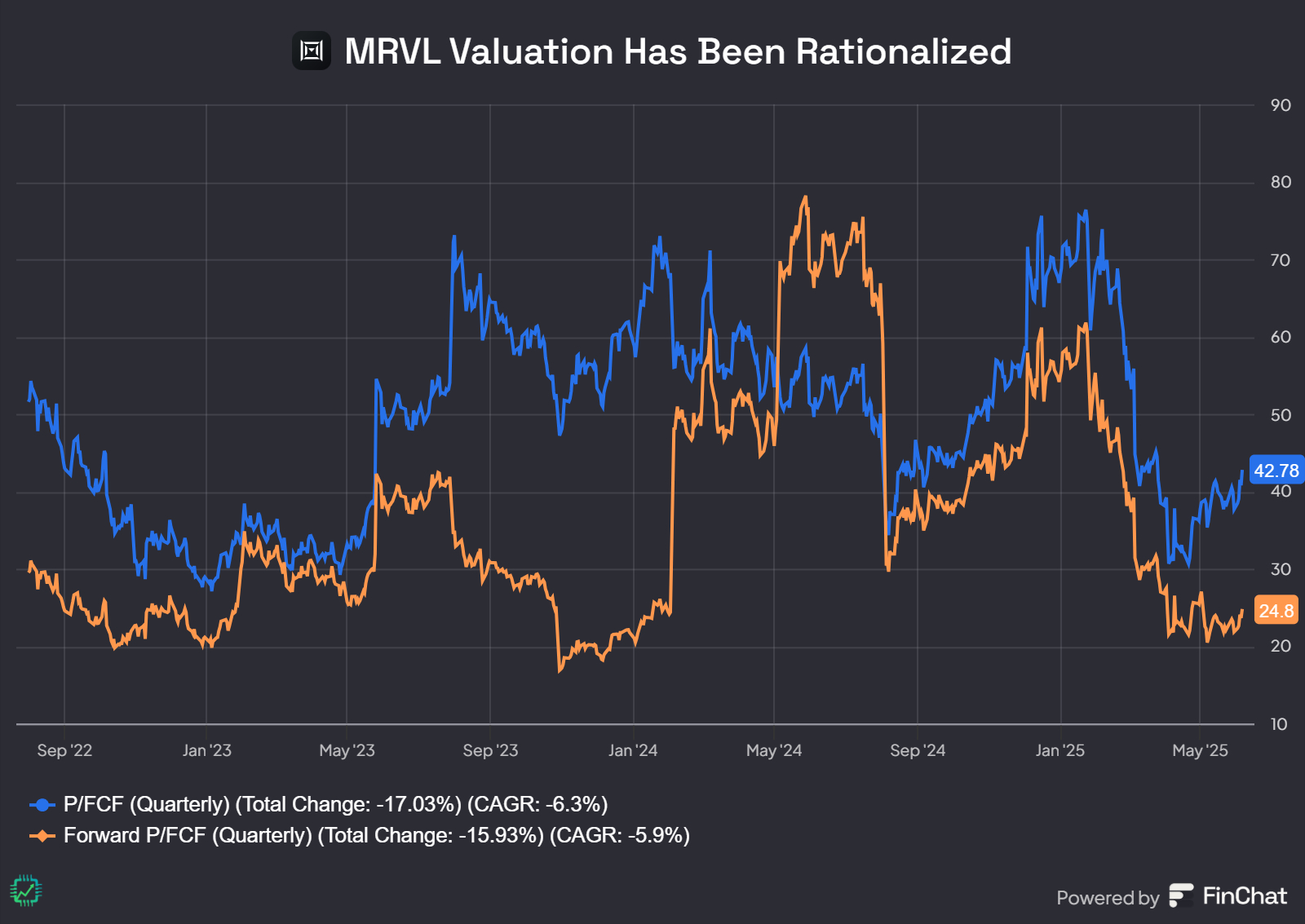

As previously mentioned, through all of this pain the last few years, Marvell shareholders have continued to enjoy modest rising FCF on a per-share basis. Mate that with the stock price collapse so far this year, the valuation has been finally reset after all of the AI hype nonsense since 2023 (seriously, there’s only one Nvidia).

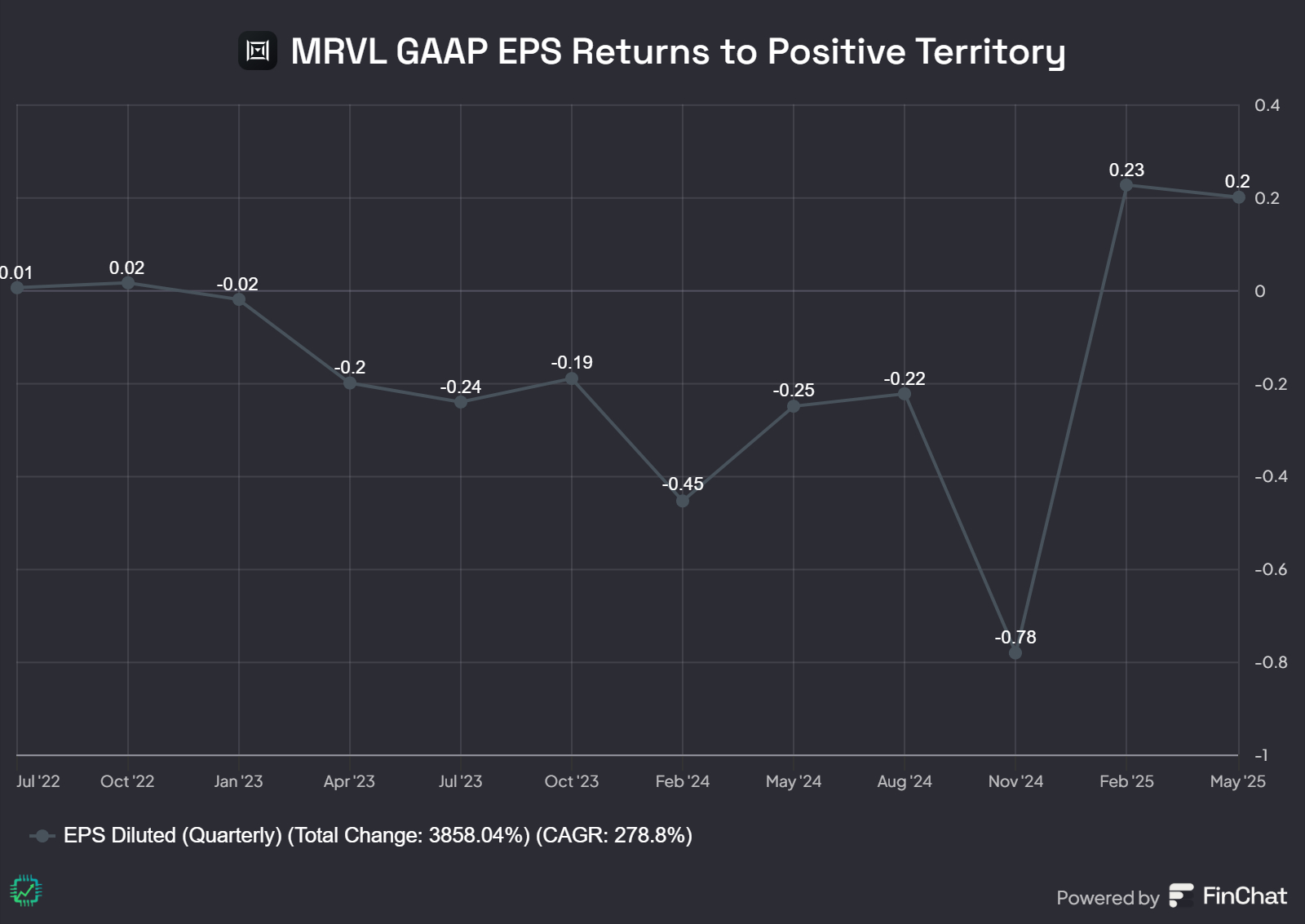

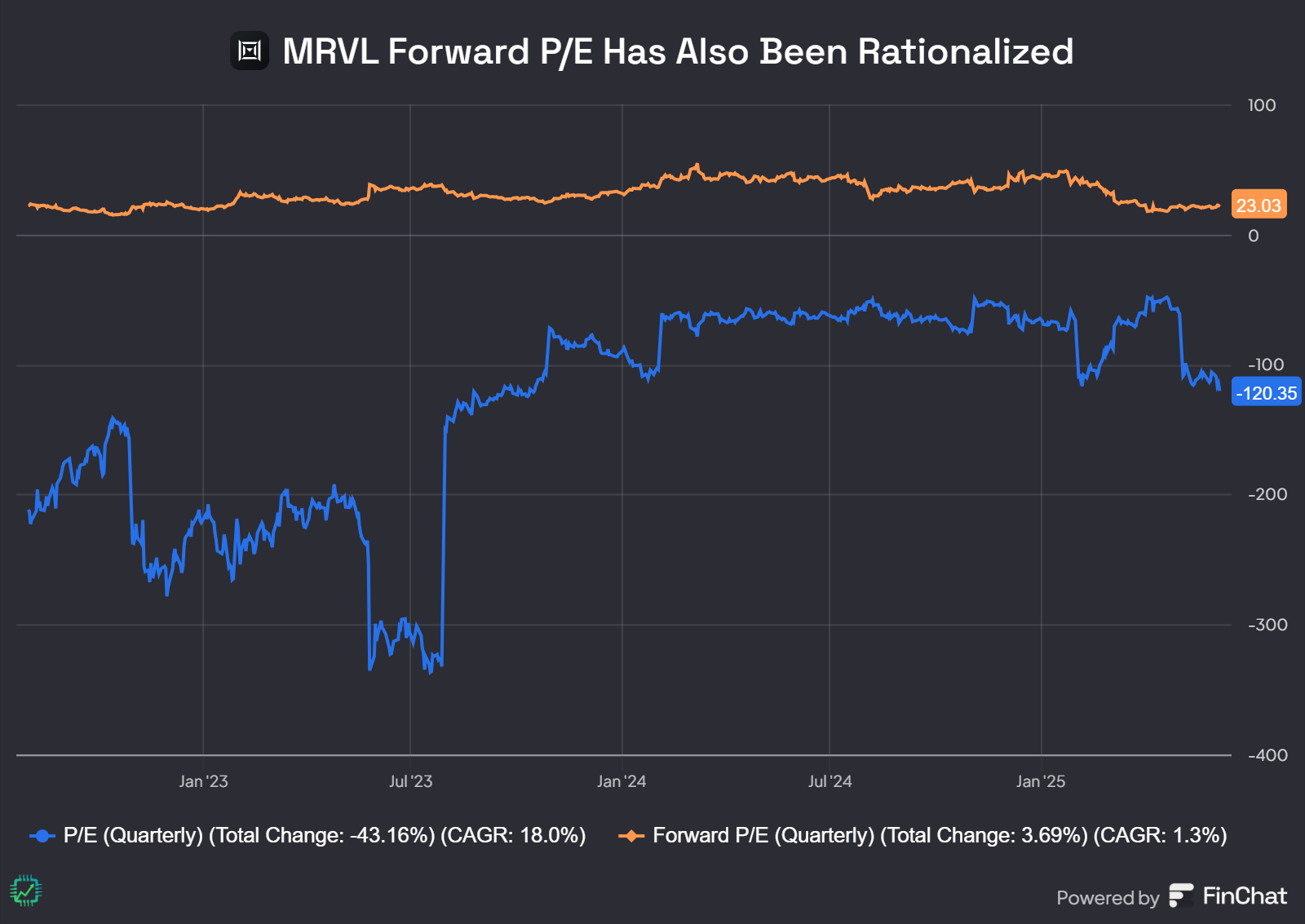

In Q4 FY25, Marvell finally turned a quarterly GAAP profit again! The road has finally been paved for this profit metric to return to full-year positive territory again.

Do note, the forward P/E is based on adjusted net income expectations from Wall St. analysts (since Marvell provides adjusted profit guidance); and the trailing-12-month P/E is based on GAAP EPS. But still, you get the idea. At this stage, the FCF-per-share still seems like the more meaningful metric, but here’s the GAAP EPS chart anyways, in case that’s your preferred valuation.

It’s been a crazy few years for Marvell, but we see potential upside for the company following the Q1 FY26 report.

Marvell now trades for ~38-39x TTM P/FCF as of this writing. We expect this valuation, assuming we freeze the stock price/market cap at ~$61 a share, to decrease into the ~25x range this year as free cash flow continues to grow during this next cycle of growth. The valuation has been rationalized. But is MRVL a “better buy” than NVDA or AVGO? Up for debate. Personally, we are holding our positions steady as they are right now. See you over on Semi Insider for further discussion.