Just when you thought the hard disk drive (HDD) was a relic of the past, destined for the same dusty shelf as the floppy disk, it’s making a surprising comeback. The engine behind this revival? You guessed it: AI. The insatiable demand for mass data storage from data centers is breathing new life into this legacy market, and Seagate Technology (STX) is at the forefront.

Back in April, when we released our memory chip IDM video, we focused on DRAM and NAND flash, largely setting aside the HDD market. Let’s right the wrong and talk a bit about HDDs.

The HDD landscape: Old dogs, new tricks?

The HDD market has consolidated to just a few key players: Western Digital, Toshiba, and Seagate.

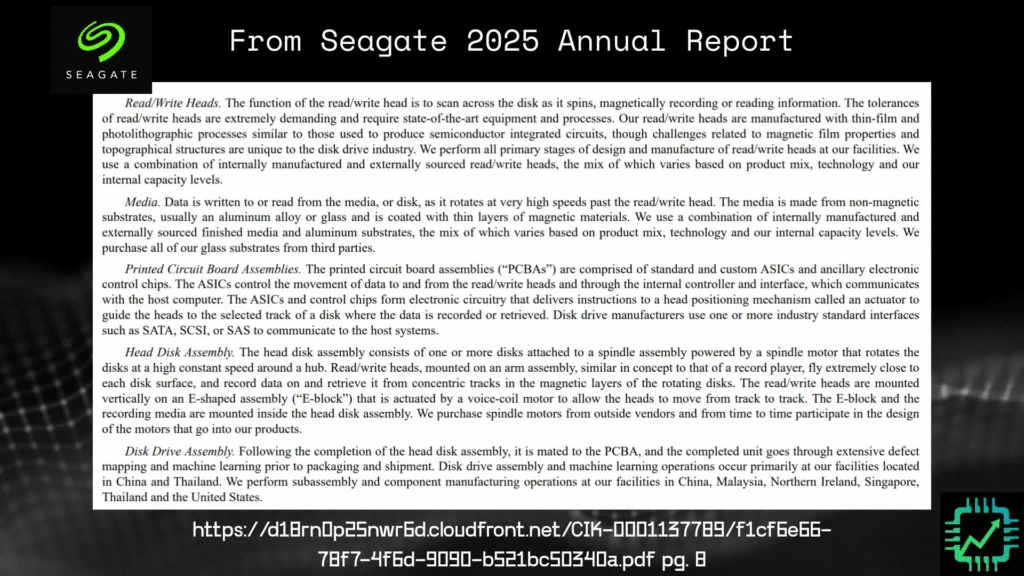

For those unfamiliar, a hard disk drive is a data storage device. If you open one up, you’ll find one (or more) circular magnetic discs – the platters – and mechanical arms that read and write data. It looks something like a record player.

HDDs have been around a long time, and they’ve gotten cheap, but the mechanical nature of how they work comes with trade-offs. Compared to modern solid-state NAND flash memory chips, HDDs are slower, use more power, and can have less longevity. And as we know from firsthand experience, their mechanical parts make them particularly fragile. Don’t drop your HDD.

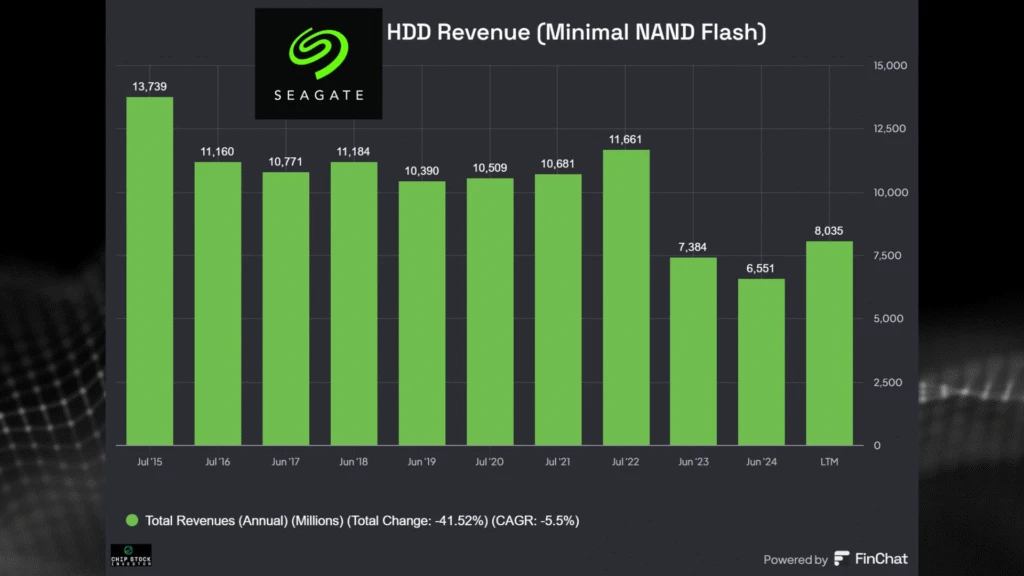

Historically, this has put Seagate in a tough spot. A look at the company’s long-term revenue trend reveals a picture of secular decline. Flash memory has gotten cheaper to manufacture, and its higher performance has led enterprise and data center customers to increasingly utilize these over HDDs. And yet, despite this trend, a revival is underway.

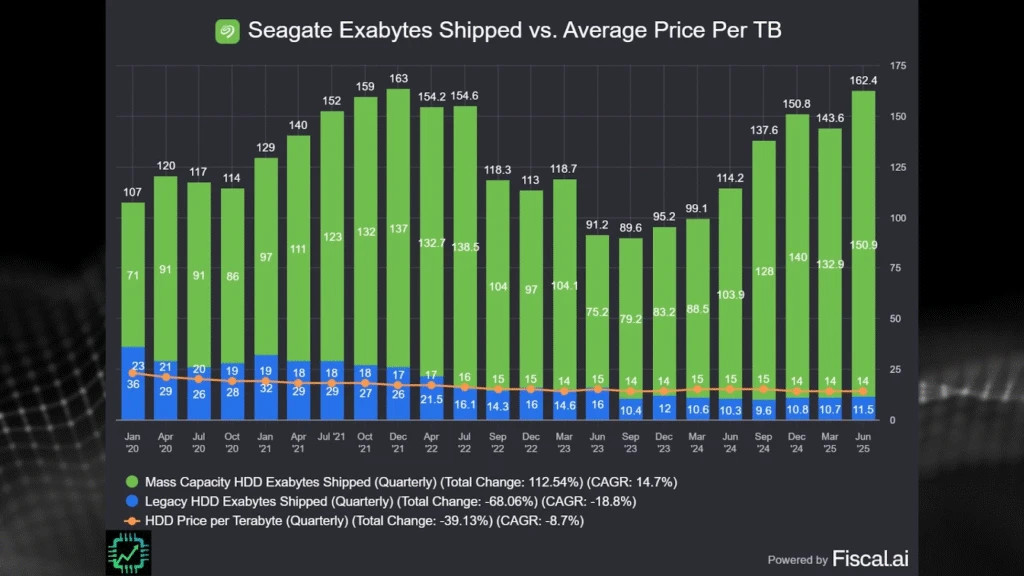

Want to do in-depth company analysis and make great financial visuals like the one above? Check out fiscal.ai, and use our link to get 15% off any paid plan! Fiscal.ai/csi

What just happened

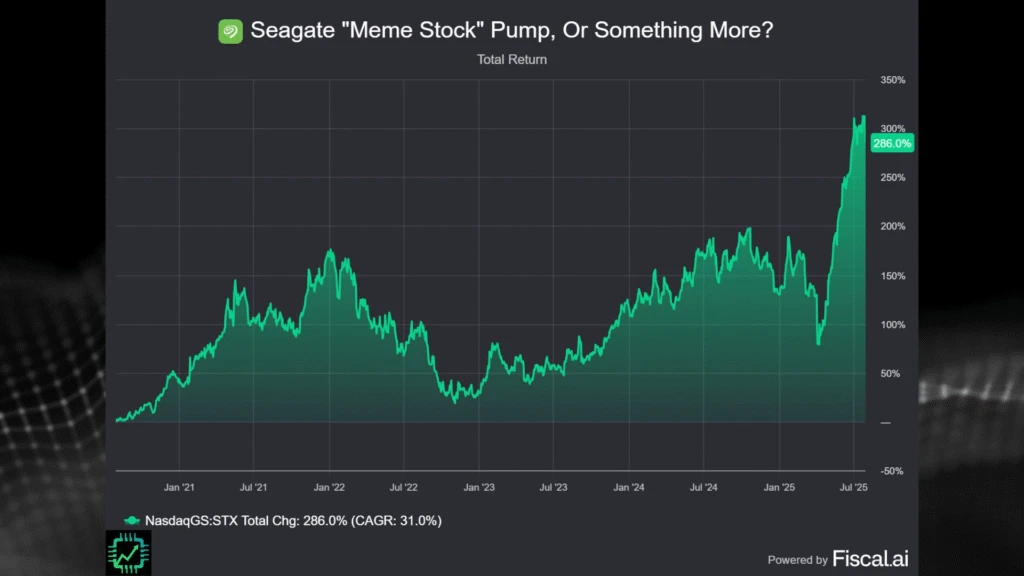

Around April 2025, just as we were dismissing the HDD market, Seagate’s stock went on an incredible run, more than doubling in just three months. So, what changed?

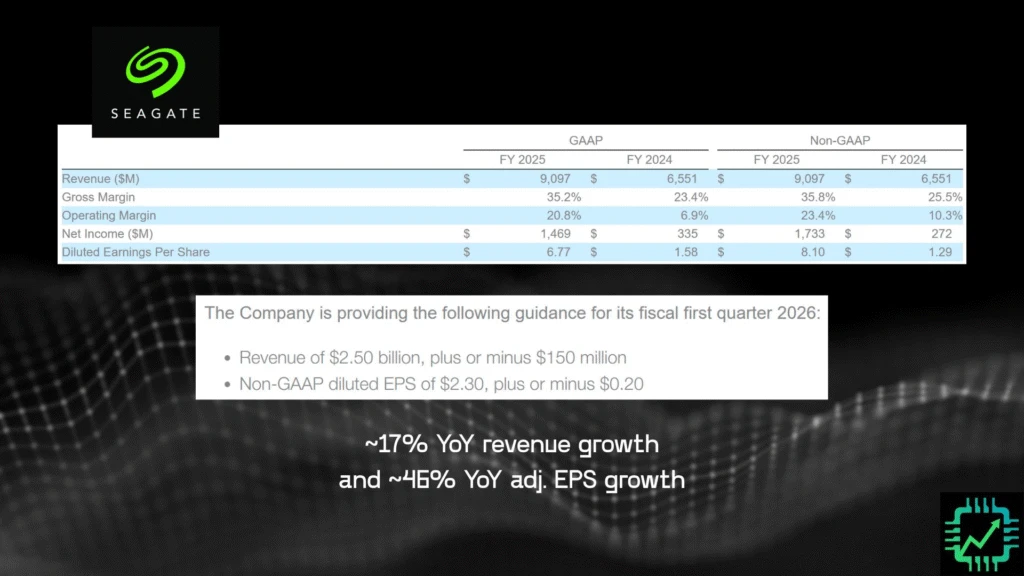

The company’s recent guidance certainly provides a clue. For the first quarter of Seagate’s fiscal year 2026 (corresponding to the three months that end in September 2025), Seagate projects:

- Revenue of $2.5 billion (plus or minus $150 million), implying 17% year-over-year growth.

- Non-GAAP earnings per share of $2.30, implying 46% year-over-year growth.

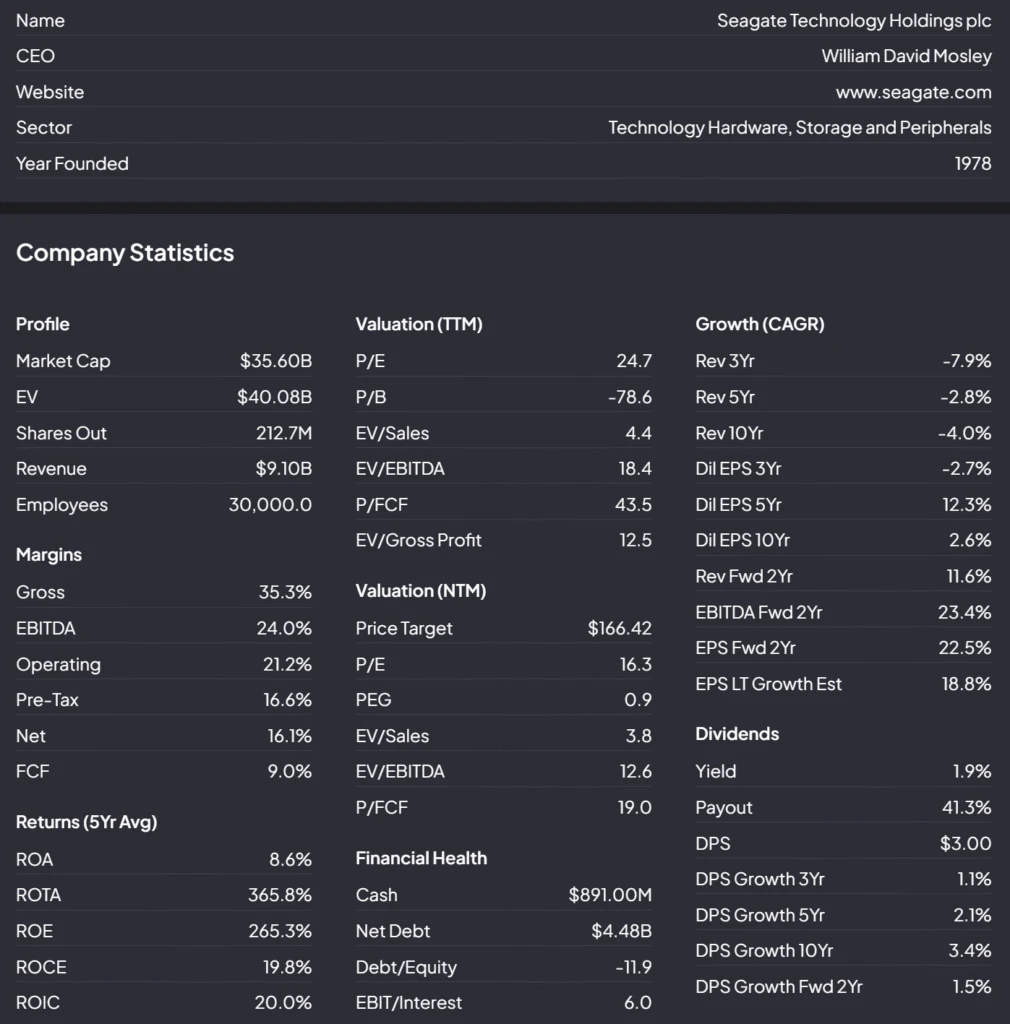

Those are epic numbers for a company supposedly in decline. After finishing fiscal year 2025 with $9 billion in revenue – a significant rebound from the $6.5 billion in fiscal 2024 – this guidance points to powerful momentum. But even these figures don’t fully explain why the stock exploded.

The full story involves a series of strategic maneuvers and a technological breakthrough.

A tale of two deals

Two key transactions set the stage for Seagate’s resurgence.

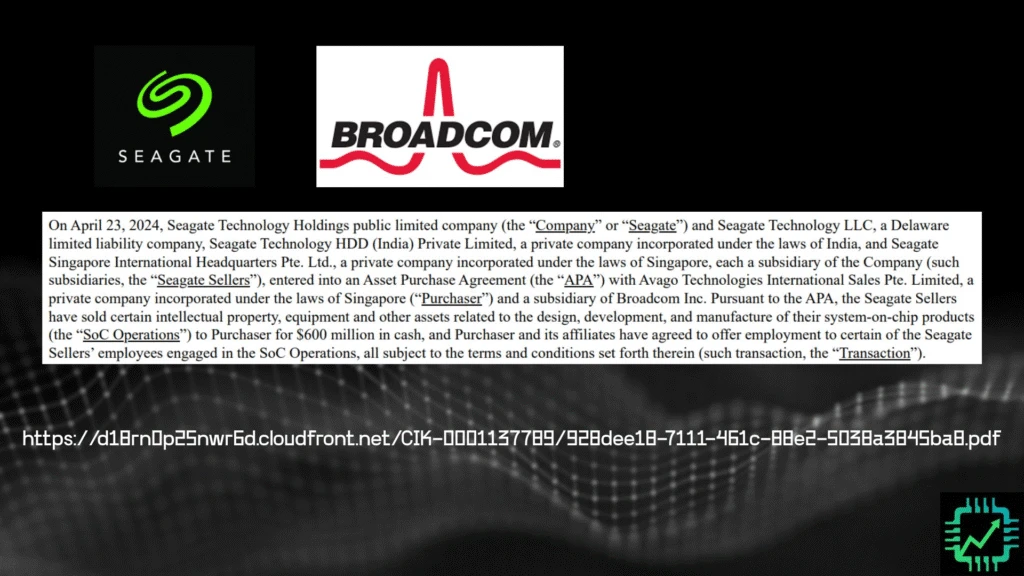

- The Broadcom Deal: Last year, in a deal that drew little attention, Seagate sold some of its intellectual property (IP) and a small development team to Broadcom for approximately $600 million. This likely involved IP related to the 12nm-based controller chip in their new HDDs, allowing Seagate to monetize the asset and source the component from a specialist.

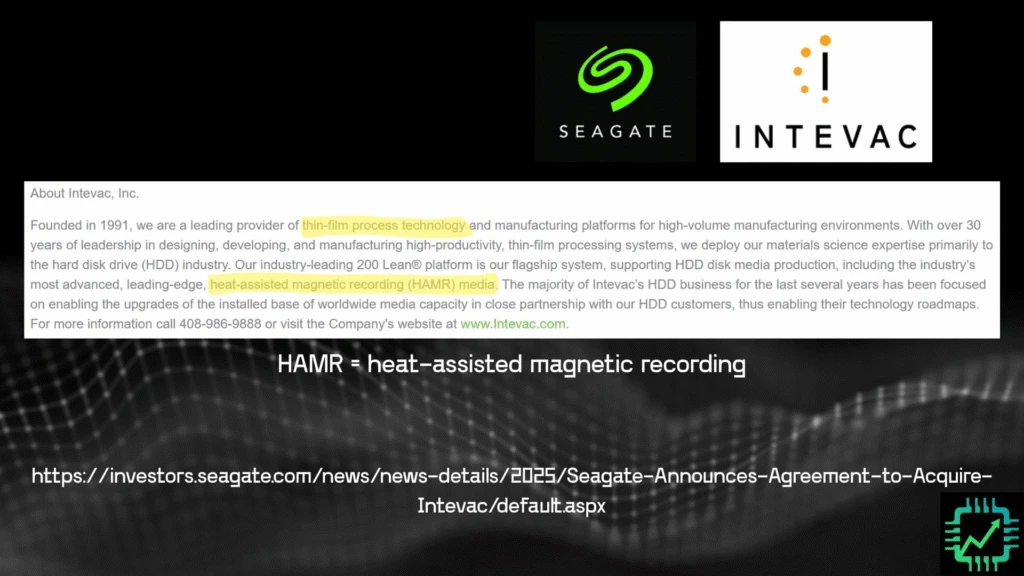

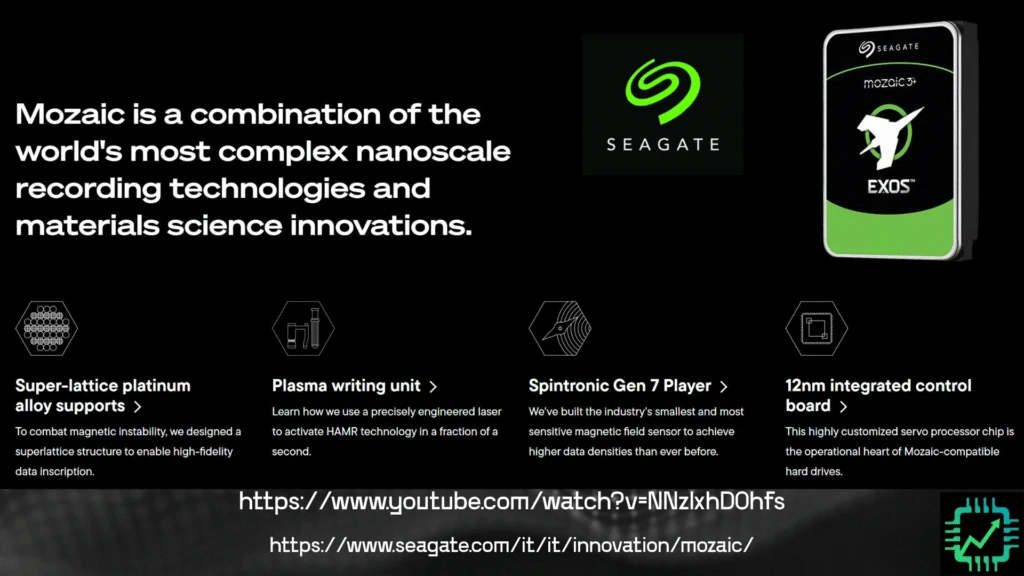

- The Intevac acquisition: Early in 2025, Seagate announced it was buying Intevac, a tiny company specializing in thin-film deposition equipment. This acquisition was a strategic move toward vertical integration, specifically for a newly commercialized technology called HAMR.

It’s HAMR time

HAMR, or Heat-Assisted Magnetic Recording, is one of the core innovations driving Seagate’s turnaround. This technology dramatically increases the amount of data that can be crammed into a standard HDD form factor.

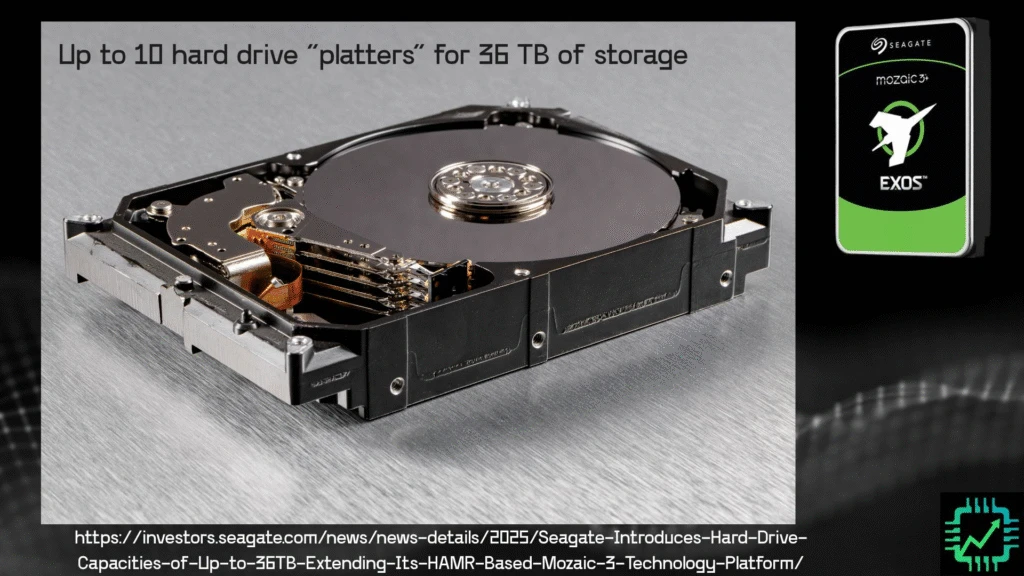

Inside Seagate’s new Mosaic 3+ drives, there are stacks of up to 10 platters. Thanks to HAMR, each platter can hold 3.6 terabytes of storage, for a total of 36 terabytes in a single, compact device. Data centers can simply swap out their old drives and plug in these new, higher-capacity ones.

This leap in density is achieved through several innovations:

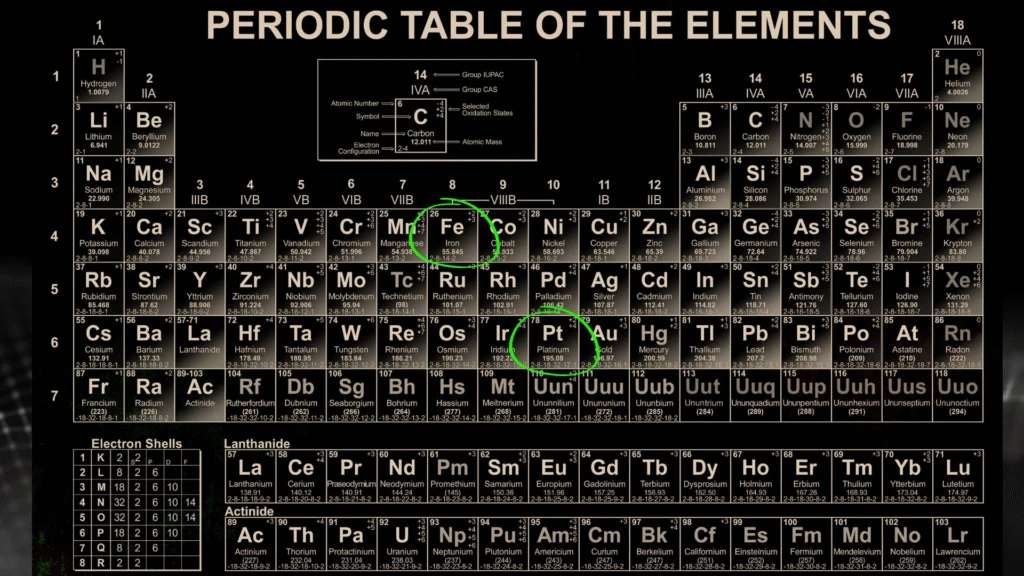

- Iron-Platinum Alloy: A new magnetic thin film made of an iron-platinum alloy coats the platters. This is where Intevac’s deposition technology comes into play.

- Plasma writer: A tiny laser on the read-write arm momentarily superheats a spot on the spinning disk. This allows data to be written to a much smaller magnetic area, drastically increasing storage density.

- Advanced mechanics: A new, more precise assembly allows the read-write arm to move faster and more accurately over the denser data tracks.

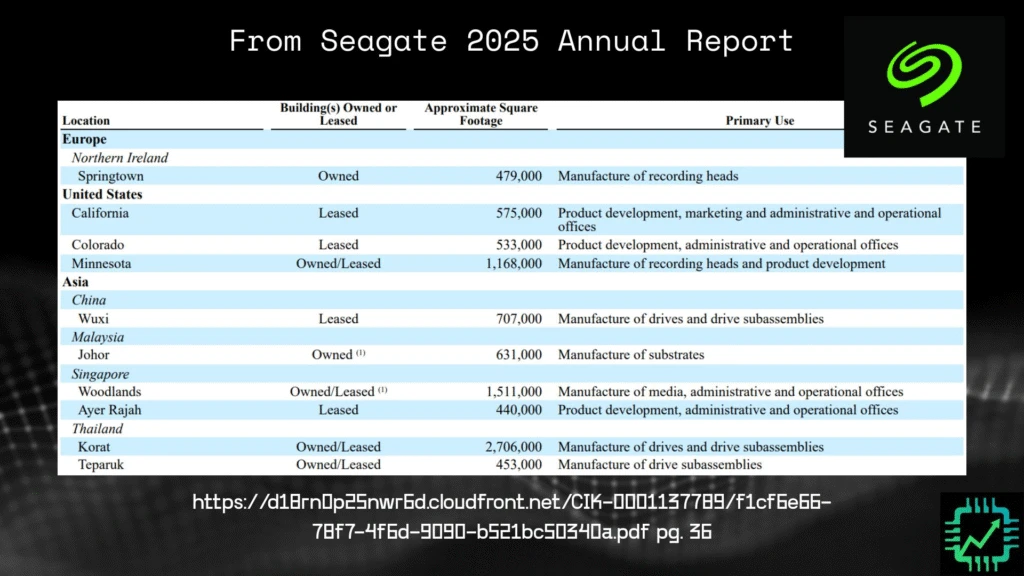

- Seagate’s vertically-integrated manufacturing and supply chain allows it to keep its new tech development mostly in-house, control costs, and make HAMR an accretive opportunity.

The investment thesis

The business case for Seagate is straightforward. AI data centers require an astronomical amount of mass storage. Much of this data doesn’t need the high-speed performance of flash memory (like systems provided by Pure Storage, one of our investments here at Chip Stock Investor), making ultra-cheap HDDs a viable solution.

The key metric to watch is exabytes shipped. As data centers continue their massive build-out, the total volume of storage shipped is returning to growth. The challenge for Seagate has been the historically declining price per terabyte for their HDDs (orange line plotted against exabytes shipped in the chart below below).

The story for the next few years hinges on two factors: The longevity of the AI data center build-out, and the stabilization of HDD storage prices. If the demand for exabytes from hyperscalers continues to grow, and the price per HDD stabilizes, Seagate is positioned for a solid growth story.

There was a similar dynamic at work for Seagate starting in April 2020, when the stock quickly doubled following the initial shock of the pandemic. That phase lapsed into a downturn. What could be different this time is the powerful, secular megatrend of AI. For investors, Seagate represents an interesting ancillary play on the data center supply chain – a legacy company reborn for a new era, and perhaps trading for a reasonable valuation.

2 Responses

Do you like Seagate more than Western Digital? If so, why?

Wow! What a comeback, I thought this industry was dead like Kodak. I think I’ll stick with Pure storage. Fascinating piece, thanks!