The next phase of the AI data center buildout, AI inference, has sent two semiconductor sub-industries skyrocketing. Memory chipmakers and silicon photonics started an epic run higher during the second half of 2025, and optimism is high that these companies are on course for a multi-year growth cycle.

As with hype cycles like this one, the market is efficient at unearthing even the most niche participants and running valuations up there too. Semiconductor wafer suppliers are one of those areas, and long-term investors should be cautious. Let’s briefly look at a couple small compound semiconductor wafer companies that have been cooking thanks to silicon photonics.

We’re building a new set of investor tools including industry supply chains and industry stock indices, financial data, and more. Join us over on Semi Insider to get started using the new Research Dashboard! https://chipstockinvestor.com/pricing/

Raw semiconductor wafers aren’t a “bottleneck”

A couple years ago, we discussed this portion of the semiconductor manufacturing process when doing a deep dive on DISCO Corp. (TSE:6146, OTC:DSCSY). DISCO, along with smaller participants Tokyo Seimitsu (TSE:7729) (Accretech)and KLA Corp. (KLAC) – the latter primarily focused on metrology and PDC equipment niche – are leaders in wafer dicing.

But at the very front end of this process are the companies that produce the raw wafers themselves. We do not view this sub-industry as a bottleneck or chokepoint. There are multiple regional suppliers, and plenty of niche suppliers of compound and specialty wafers.

Nevertheless, there’s been significant stock price action for these companies due to elevated expected demand, especially for epitaxial wafers. One particular case is U.K.-based epi wafer “pure-play” IQE PLC (AIM:IQE), one of Lumentum’s (LITE) suppliers for indium phosphide (InP). IQE is in financial distress and is undergoing a strategic review (possible sale of the business or business assets). https://www.iqep.com/media/2zuhdt1y/iqe-trading-update-q4-2025-final.pdf

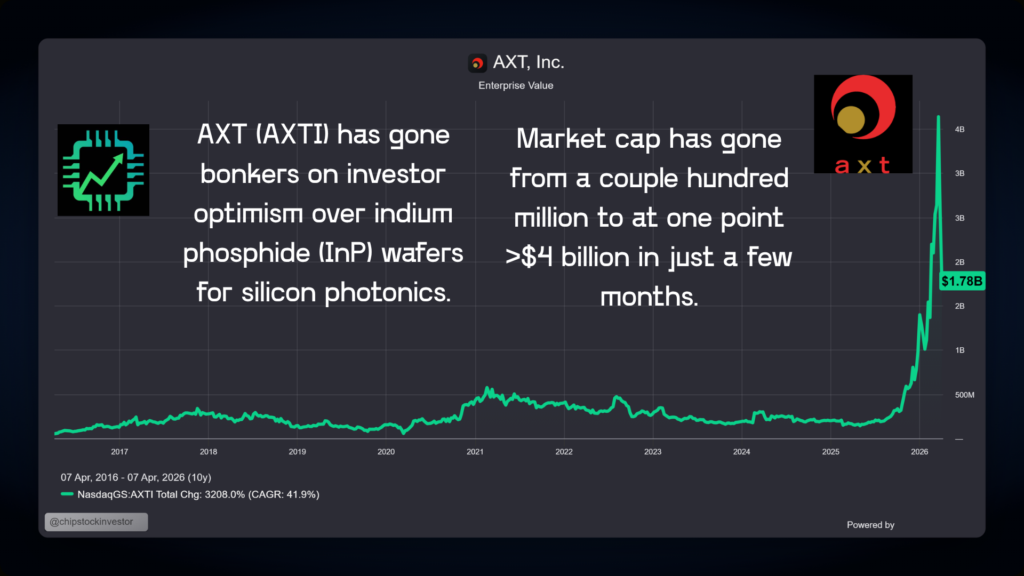

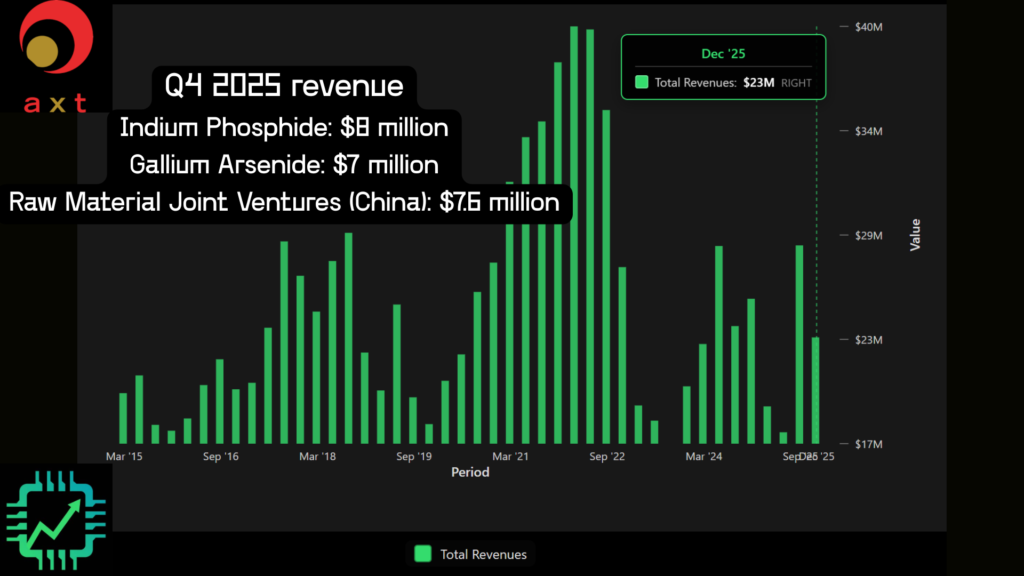

Another is AXT Inc. (AXTI), another small specialist providing InP and gallium arsenide (GaAs) compound wafers, used in applications like silicon photonics. From a market cap of just a couple hundred million dollars to over $4 billion in Q1 2026, investors are betting the company will cash in big time on data center AI buildout.

Why we’re cautious and avoiding the wafer suppliers

This AI data center CapEx cycle might be tricking some into thinking semiconductor wafer companies are price-makers – companies that wield control over product pricing. In reality, though, due to multiple suppliers and new market entrants (particularly in China), wafer suppliers are price-takers – they do well in boom times when supply tightens, but large buyers (like TSMC) wield great control over the manufacturing supply chain.

Take AXT as an example again. Though it’s a top supplier of InP and GaAs wafers, this market is actually quite small. Total revenue was just $23 million in Q4 2026, made up of $8 million in InP, $7 million in GaAs, and $7.6 million in joint venture (the company’s manufacturing segment in China) sales.

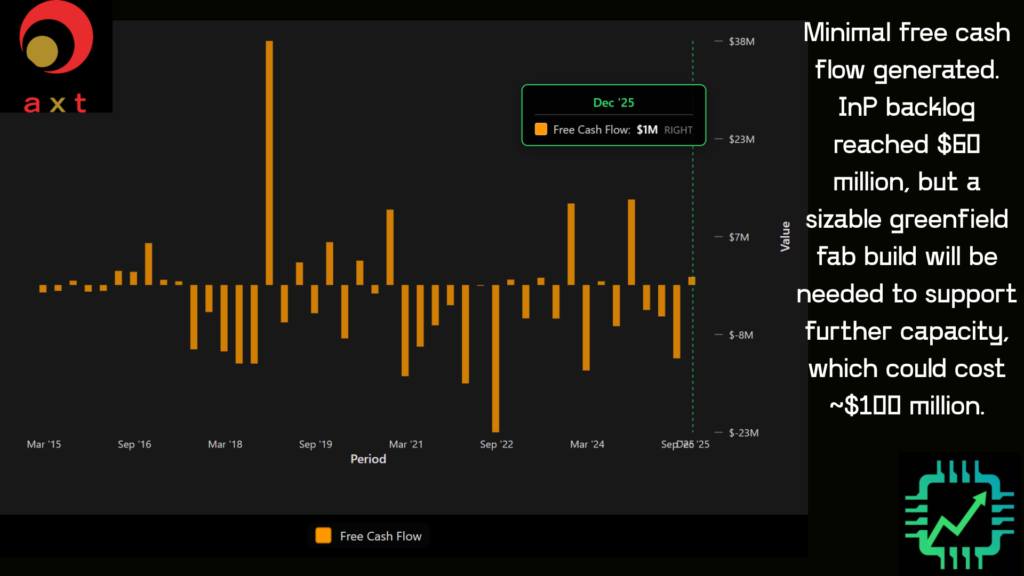

All of this equates to minimal, if any, free cash flow generation as AXT lacks scale of its larger wafer supplier peers or the vertical product integration of companies like Lumentum, Coherent (COHR), or even Broadcom (AVGO) which has quietly retained some of its own InP wafer manufacturing in-house for its photonics and networking products.

Further, while AXT expects significant growth in 2026 from photonics and data center networking demand, the InP backlog in particular was at $60 million. And to support future demand growth, AXT will need to break ground on a new greenfield fab that could cost around $100 million. The company issued new shares late in 2025 to bolster its balance sheet.

All of this should also be compared against the fact that the largest InP wafer supplier is Sumitomo Electric (TSE:5802). No, Sumitomo isn’t a pure-play. But that’s ok. Sumitomo is a highly-profitable electronics manufacturing conglomerate.

In the meantime, AXT is valued at 33x trailing sales, and still over 20x sales on one-year forward expectations, and has no clear path to sustainable profitability.

It all adds up to a tough position for the wafer suppliers, particularly the small ones. If this growth cycle does continue for a few years, we’d expect a round of consolidation to take place, with the bigger wafer companies or the IDMs scooping up smaller companies and/or their assets to support their operations. During this period of elevated hype, though, long-term investors should be weary of chasing extreme valuations.

See you over on Semi Insider for more of the conversation on silicon photonics, and an indexed list of semiconductor wafer suppliers and CSI’s allocation.

One Response

Interesting read, would love for you guys to discuss Soitec more and how much revenue their wafers in the photonics space could bring them in revenue because of CPO being on the GPU reportedly.