After spending a couple of years urging AMD (AMD) to spend less time talking about GPUs and more time focusing on its actual money-making hardware — CPUs specifically, as well as FPGAs via the Xilinx acquisition — 2026 has been a moment of vindication. As AI goes into production (inference, or in other words, more usable software), the CPU is back en vogue in 2026.

AMD is nearing the (arbitrary) $1 trillion market cap milestone as a result of the “CPU shortage.” But, so is resurgent Intel (INTC).

Contrary to what Nvidia (NVDA) CEO Jensen Huang said a couple weeks ago, Marvell Technology (MRVL) likely isn’t “the next $1 trillion company.” By way of proximity to the market cap landmark, AMD is. And second behind AMD, probably Intel.

We’ll address Nvidia’s interest in boosting Marvell separately another time. However, we’ve discussed this at length in lots of other posts, and it’s not so hard to imagine why that is: Data center networking is migrating to more optical components, and Marvell is in fighting shape to battle against that networking semiconductor market share leader Broadcom (AVGO). Nvidia thus invested in Marvell and its continual networking design improvement.

Anyways, back to our AMD and Intel trillion-dollar discussion. What gets each of these companies to that point, and then beyond?

Two very different supply chains

By way of review, AMD is still going the fabless design route. Its wafers for CPUs and GPUs are manufactured by TSMC (TSM), it invested in Sanmina (SANM) (in tandem with the ZT rack-scale design acquisition) for help with downstream manufacturing, and continues to invest in other architectural and software companies like last week’s announced acquisition of Mext for data center memory.

Intel of course also currently uses TSMC for its most advanced processors. But that will begin to change as Intel’s internal fab and Foundry model finally get into shape the second half of this year. The problematic 18A process has finally begun ramping up production. And its 18A-P process has entered risk production and improves greatly on 18A. New customers are finally lining up, including Apple (AAPL) which may use 18A-P for some of its laptop and tablet processors (no official announcement outside of the one on Truth Social).

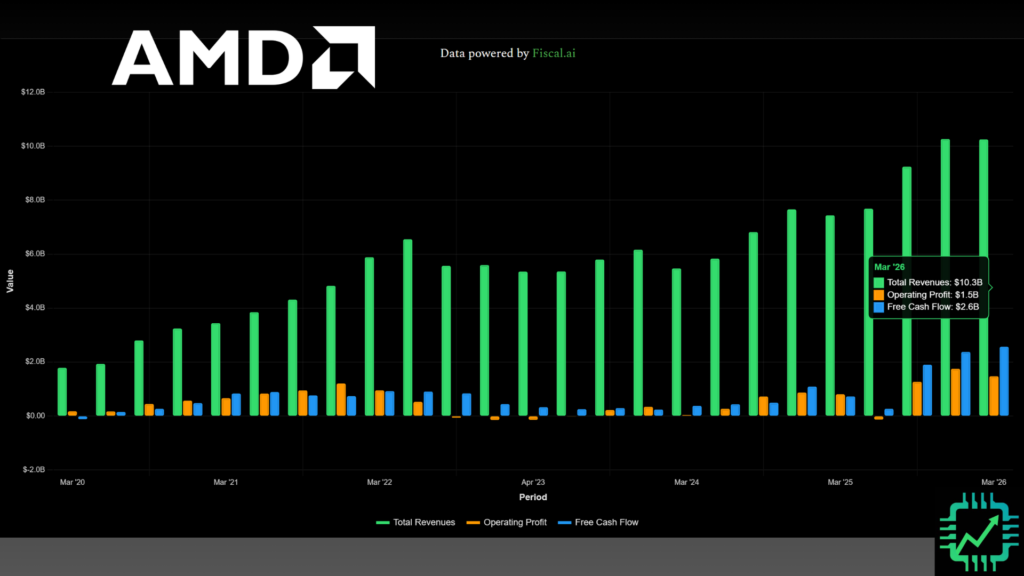

AMD has said its next-gen EPYC “Venice” data center CPUs are now ramping up production at TSMC, paving the way for a step-up in revenue growth later this year. And as these CPUs and other hardware like the GPU technology matures, profit margins should continue to gradually improve.

Image source: AMD.

In contrast, Intel 18A will begin cranking out the long-awaited “Clearwater Forest” Xeon 6+ chips later this year. And in 2027, the improved 18A-P process will begin work on “Diamond Rapids” Xeon 7 processors. In addition to utilizing Intel’s in-house advanced packaging, the company also recently announced new Ethernet-based networking hardware, and an agreement with manufacturing and assembly titan Foxconn to build rack-scale solutions (akin to what Nvidia and AMD have been doing).

Image source: Intel.

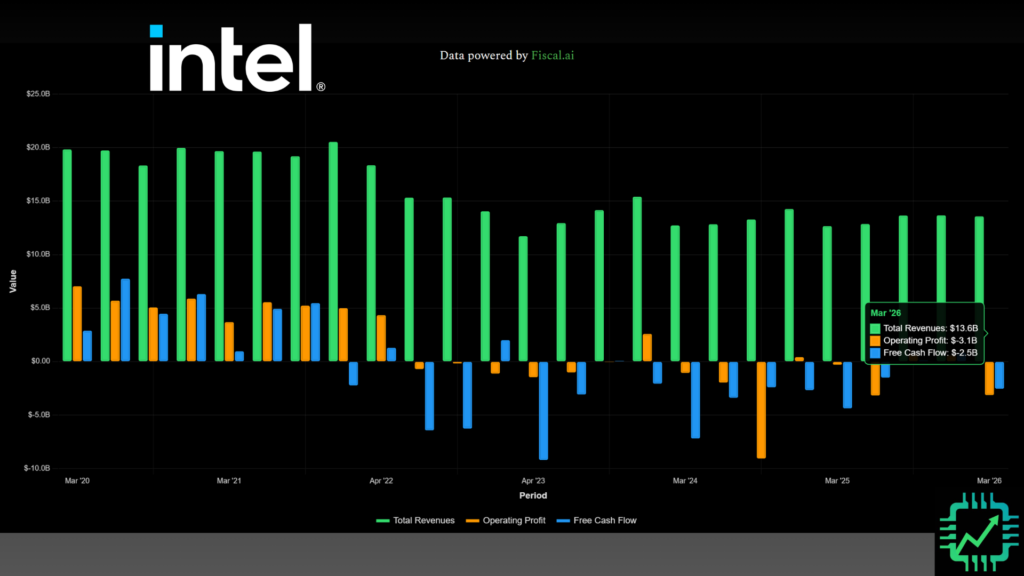

These developments at Intel have the company back in growth mode, and expectations are the persistent cash hemorrhage situation of the last few years will stop sometime in 2027. This is the financial reason why Intel has outperformed relative to AMD in the last 12 months.

AMD has been a pretty good “consolation prize” with a more than 300% gain in the last 12 months alone. But still, what went wrong in our analysis, and will Intel continue to outperform?

What we got wrong at CSI, and what will push both companies to over $1 trillion

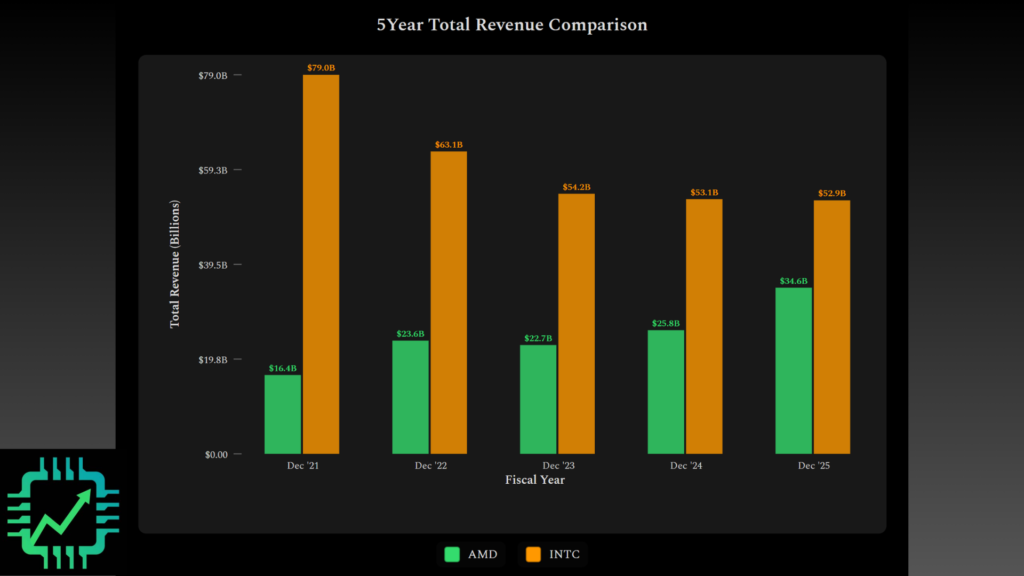

After years of AMD not just eating up market share in % terms, but also quickly narrowing the gap with Intel in terms of dollars-and-cents revenue, this trend appears to be coming to an end. Intel’s guidance for Q2 2026 implies revenue of $14.3 billion, compared to AMD’s guide for $11.2 billion. Amidst high and rising demand for data center CPUs, both companies’ financial results could begin to move in lockstep going forward.

This market share dynamic, especially paired with Intel persistently losing money and a total mess of a Foundry business, is why we exited a tracking position in Intel in 2025 and decided to just stick with AMD. Hindsight is 20/20, although we certainly aren’t upset with the results.

But what could have been improved on? It goes back further than just the last 5 years.

(Nick alone speaking here.) My formative years as an investor (starting in 2005) were heavily shaped by the Great Financial Crisis of 2008-9, and the ensuing years of recovery. U.S. government intervention in capital markets had limited benefit for shareholders of publicly-traded companies long-term. I’m thinking in particular of the auto and airline industries.

Thus, while we discussed at length about the U.S.’s desire to get Intel back on track, we didn’t make the connection that these actions would lead to more immediate upside in Intel stock. Basically, the market cares less about Intel vs. AMD’s financials, and more about Intel getting the government boost. Why?

I have to acknowledge that 2008-9 government activity was dealing with a crisis, and staving off some sort of financial system collapse. The U.S. actions today are not the same. The world is at economic war, especially so since 2017. And while the intensity of this economic war has ebbed and flowed and taken on different forms (the “U.S.-China trade war,” AI export restrictions, onshoring and friend-shoring of manufacturing, etc.), the overall trend appears to be intact for the foreseeable future.

Intel is near the heart of U.S. economic planning. For example, a more competitive Intel keeps pressure on TSMC and its related supply chain to migrate more manufacturing to U.S. soil. And it signals to other companies to do the same and invest in American manufacturing capacity.

The era of central bank money printing certainly isn’t over. But that isn’t enough anymore. The major economies of the world are competing to keep, and earn, more economic activity flowing through their system. Intel is part of that strategy. And this is why the stock price keeps going up.

And it’s likely, in our revised opinion, to keep marching higher along with AMD, towards a $1 trillion market cap… and maybe even beyond.

Join us on CSI Semi Insider for more of the discussion, weekly live Q&A sessions, and an expanding set of tools for investors! chipstockinvestor.com/pricing/