SaaS-pocalypse isn’t over, at least not for select software industry verticals. Digital payments are still down in the dumps (slowing growth, higher competition, profitability questions), even dragging down the dominant infrastructure providers Visa (V) and Mastercard (MA) this year.

The creative software market is another key area of weakness in the world of software. And Adobe‘s (ADBE) chief financial officer (CFO) just added fuel to the fire. Or shall we say, former CFO.

A semi industry veteran returns

Dan Durn has been serving as Adobe’s CFO since 2021. He’s had an incredible career, serving as the financial head of other companies at critical points in their journey:

- Applied Materials (AMAT) from 2017 to 2021

- Freescale Semiconductor from 2014 to 2015, and then CFO of NXP Semiconductors (NXPI) from 2015 to 2017 after NXP acquired Freescale

- GlobalFoundries (GFS) from 2011 to 2014 in the early years after its spin-off from AMD (AMD)

Similar to his moves at his last gig at AMAT, Durn has been overseeing massive stock repurchases at Adobe (we were big fans of his work at Applied too). It thus came as a surprise that Durn’s departure was abruptly announced during Adobe’s Q2 fiscal 2026 earnings update.

In a sign of the times, Durn is returning to the semiconductor world. Marvell Technology (MRVL) to be specific, Jensen’s now famously declared “next trillion-dollar company.” Marvell scoring Durn could be even better news than the “Jensen pump,” in our opinion.

We’ll be discussing Marvell and AMD on Semi Insider‘s CSI Live next week.

What does this mean for Adobe?

Losing its top-shelf CFO isn’t great. Adobe’s long-running chief executive officer (CEO) Shantanu Narayen announced his retirement earlier in 2026, and a search for a successor is underway.

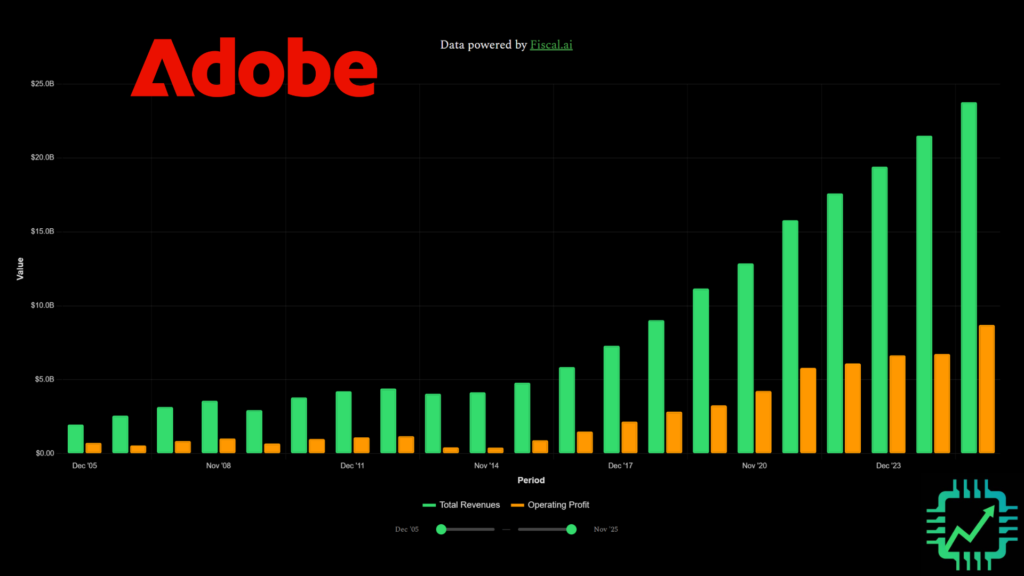

Narayen helped orchestrate Adobe’s transition to a cloud-based subscription company in the early 2010s, a period of revenue and profit disruption as the business model was radically overhauled (see chart below). Since then, Adobe’s revenue and profit has been an incredible up-and-to-the-right story.

The AI era threat is that another overhaul will be required. And losing both Durn and Narayen at this crucial moment is causing a lot of investor angst. Which leads us to another key point from the Q2 fiscal 2026 update: Adobe is sacrificing revenue growth to invest in AI.

More “freemium” Adobe is coming

Per Narayen on the Q2 earnings call:

“Based on the early success and MAU adoption of freemium journeys for Acrobat and Express, we’re ready to expand this experience more aggressively. For next-generation creators, the opportunity is to deliver an AI production studio across web and mobile that seamlessly integrates with the power and precision capabilities of Creative Cloud. We have increased our creative freemium MAU from 50 million to 90 million year-over-year. The opportunity is to attract hundreds of millions of additional creators through a freemium funnel based on the early success of Firefly…

…Adobe’s AI innovation has driven an impressive 3x year-over-year increase in AI-first ARR to greater than $500 million. We believe now is the time to aggressively acquire the next generation of Adobe loyalists. The strategic shift to acquire more freemium customers through Adobe and Firefly lowers our second half ARR growth expectations from individual subscribers.”

In recent years, Adobe has filled up its paid-customer funnel with free-to-use versions of Acrobat (software for PDF file management) and Express (easier to use content creation app). Adobe is going to adopt the same “freemium” strategy it’s been using with Acrobat and Express with its new AI tools, like the genAI service Firefly.

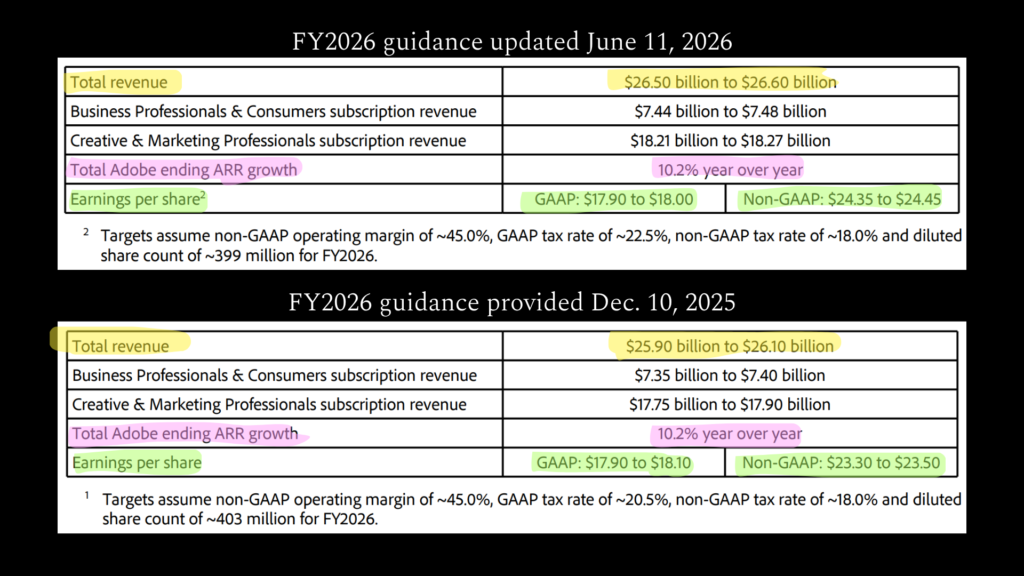

The catch, though, is lower revenue growth through the second half of fiscal 2026 (ends in November 2026). This short-term hit will lower expected annualized recurring revenue (ARR, a metric measuring subscription sales) by about $500 million.

Management believes this short-term sacrifice will keep the business in growth mode for years to come. The market is worried, because slower-growth and profit margin compression has been exactly the worry as new AI lab tools for creatives keep releasing at a torrential pace. Adobe will need to prove the freebies to attract new customers can pay off.

And yet, the guidance would seemingly indicate otherwise. Total expected revenue for this year was actually increased by $500 million to $600 million, and ARR growth was left unchanged at 10.2%. Adjusted (non-GAAP) earnings per share (EPS) were also increased about 4% from a prior range of $23.30-$23.50 to a new range of $24.35-$24.45. So what gives? Are expectations lowered or not?

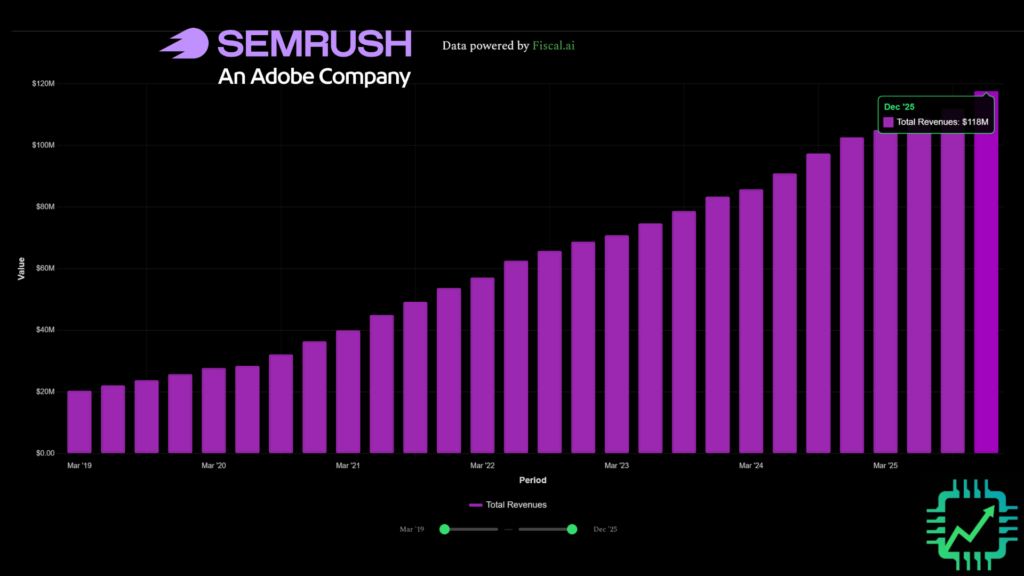

The key to understanding the guidance “increase” is the social media marketing management software acquisition Semrush, just completed in April 2026. Semrush exited 2025 generating $118 million in quarterly sales and counting (likely on course for $500 million or more in 2026 sales).

So the raised revenue guidance at Adobe essentially accounts for this acquisition, which is why the ARR growth rate remained unchanged. Semrush is filling in the expected loss in ARR as Adobe’s core creative software starts giving away freemium features later this year.

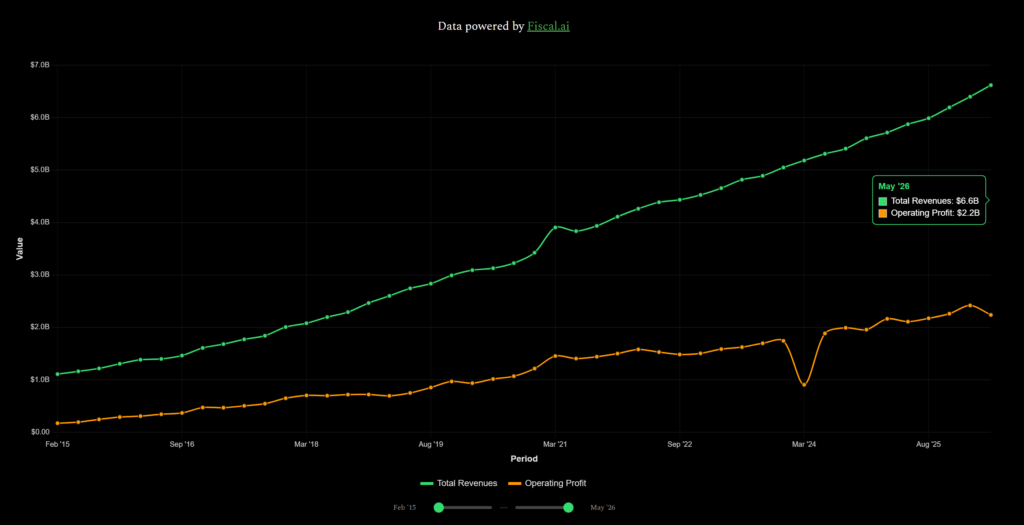

SaaS-pocalypse isn’t over. Adobe is still growing a bit, though the core business is slowing. And the profit margins are still incredibly lucrative. Operating profit margin was 33% in Q2. But that’s the point of concern. Margin is compressing again. The AI “disruption” appears to be having an early effect on the business, and proven highly-talented leadership is exiting.

CSI doesn’t own Adobe, and we’re reluctant to try and call a bottom on this one.

Join us on Semi Insider for more on this topic, weekly live Q&A events, and a growing set of investment tools like the reverse DCF calculator with price alerts!

One Response