We covered the Nvidia earnings update a couple weeks ago. It only seems fair to do the same for the world’s second-largest semiconductor company, Broadcom (AVGO), which just reported Q2 fiscal year 2026 results (for the three months ended May 3, 2026).

Record revenue. Record operating profit. Record free cash flow (still not back to record free cash flow margin, at least not yet). And the stock fell hard.

We don’t comment on short-term stock price moves. Law of Small Numbers, probabilities, and such. But there are a few items in need of explaining on this one.

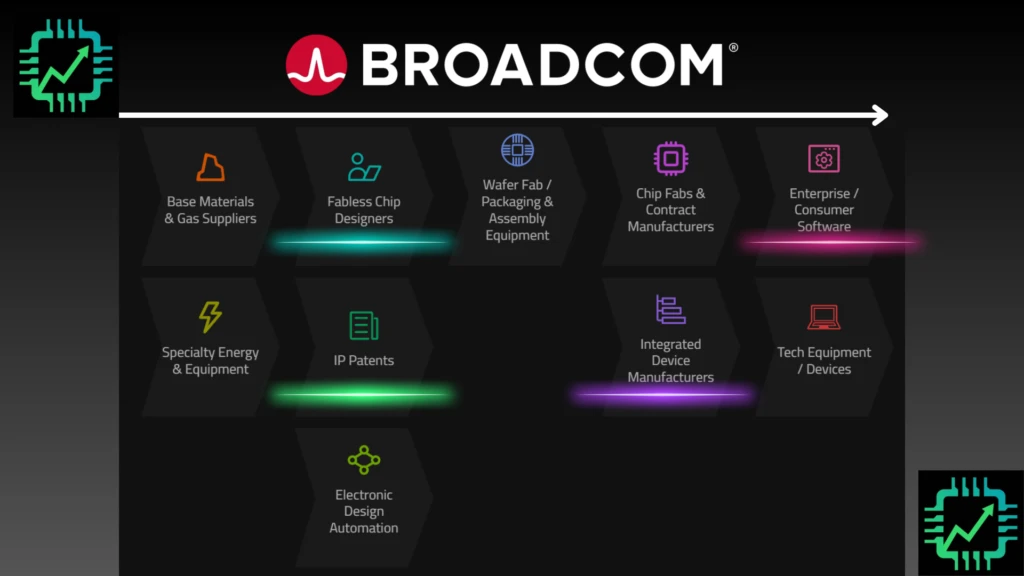

What Broadcom actually does

The business reports in two main parts: Semiconductor Solutions and Infrastructure Software (most of the latter being VMware).

The semiconductor business is where all the exciting AI stuff resides. Broadcom sells IP (intellectual property) blocks used to design custom AI accelerators (XPUs). Its biggest customers here are Alphabet/Google (GOOGL), for its Tensor Processing Unit (TPU) program, Meta Platforms (META) for its MTIA (Meta Training and Inference Accelerator), and a couple of other unnamed hyperscalers. It also counts Anthropic and OpenAI among its growing list of AI lab and hyperscaler customers.

Besides the IP business with Google being the lead customer, Broadcom is primarily a fabless chip designer, meaning it designs chips but relies on third-party foundries to manufacture them. Around 90% of its wafers come from Taiwan Semiconductor Manufacturing (TSM), and it uses these for its own products like the Jericho Ethernet switches for longer haul traffic management, and the Tomahawk switches for building low-latency high-speed clusters.

Broadcom also still does a bit of its own manufacturing (InP, or indium phosphide wafers) for optical networking products, making it a partial IDM (integrated device manufacturer) as well.

Q2 FY2026 earnings numbers for context

Here’s what Broadcom actually reported for its second fiscal quarter, which ended May 3, 2026:

- Total revenue: $22.2 billion, up 48% year-over-year.

- Semiconductor revenue: $15 billion, $10.8 billion of that being “AI semiconductors” including the IP sales. AI semi revenue specifically was up 143% year-over-year, beating Broadcom’s own forecast.

- Infrastructure Software revenue: $7.2 billion, up 9% year-over-year as the VMware price increases have mostly run their course.

- Free cash flow: $10.3 billion, a 46% FCF margin; note the convergence of GAAP EPS and FCF since the pre-VMware acquisition, this is totally normal and expected; FCF margin record was around 50% pre-VMware, and we expect Broadcom will get back to that mark again.

Check out Fiscal.ai/csi to get 15% off any paid plan! Make financial visuals to get a better understanding of the businesses you invest in.

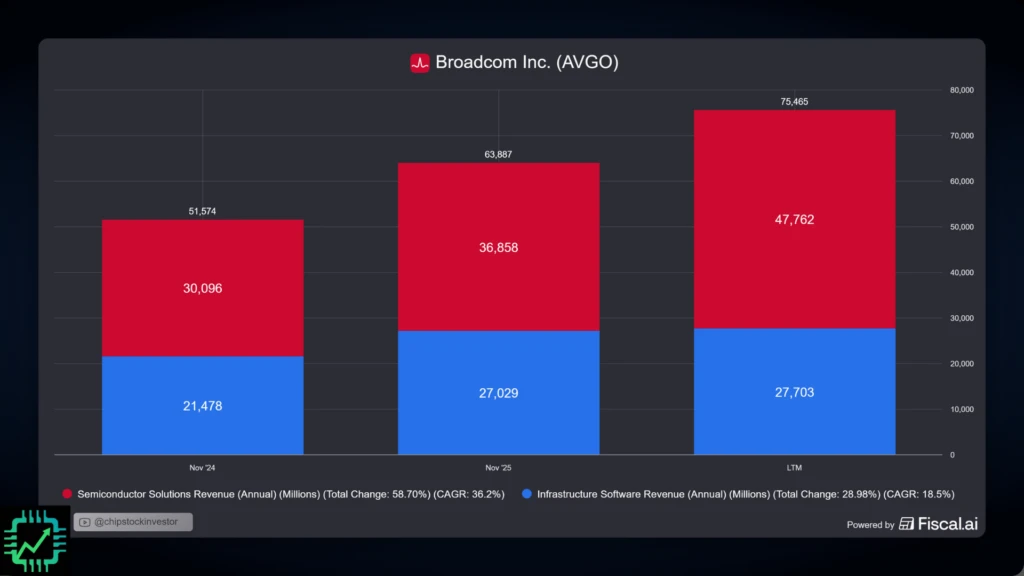

Of Broadcom’s trailing 12-month semiconductor solutions revenue of approximately $48 billion, we’re fast approaching three-quarters of that being attributable specifically to AI semiconductors — custom accelerators and the attached AI networking products.

Why did the stock drop 10%?

The simplest answer, as annoying as the answer may be, is: Stocks don’t go up in a straight line. Stocks go up, and then they sometimes go down. And with as high as AVGO has climbed the last few years, the downturns can be especially severe, even when the earnings report is really, really good.

But more specifically, in the 21st century, the market prices stocks not based on earnings results and next quarter outlook. Stocks get priced based on changes in longer term earnings revisions.

And on this note, there were a few items in the earnings call that led the market to walk back the most recent rally in AVGO stock.

The very first question Hock Tan fielded essentially asked: “You’ve already guided for over $100 billion in AI semiconductor revenue in fiscal 2027. Given the current trajectory, why aren’t you raising that guidance to $150 billion or $200 billion?”

And Tan’s response was measured: Broadcom is not going to revise its multi-year guidance every single quarter. The $100 billion-plus fiscal 2027 target stands as previously stated. Tan, as always, isn’t interested in pandering to analyst wants, sometimes to the stock’s short-term detriment.

Thus, without a meaningful upward revision to FY2027 expectations, the market didn’t have fresh fuel to push the stock even higher. So it pulled back. That’s it, it’s really quite simple.

And for the record, we’re fine with Tan and company’s method here. We’re fine with stock volatility. Mismatches in present and future expectations that cause stock volatility is how we make money.

Google TPU IP contract extended

Back in early April, Broadcom filed an SEC disclosure stating it has re-upped its IP licensing relationship with Google (GOOGL) to supply the IP behind the Tensor Processing Units (TPUs) through 2031. However, it has since been noted Broadcom is Google’s lead IP supplier, not the only one.

This isn’t new news. Google designs various TPUs – depending on specific workload – not just for its data centers, but also mobile TPUs for devices like the Pixel phone lineup. So there’s a diversity of use cases within that relationship. But the AI data center TPU are the headline products, and while Broadcom’s position remains firmly intact, there are other IP suppliers like MediaTek. Marvell (MRVL) is likely another one. Other companies are trying to get into this IP licensing game too (Intel, and we wouldn’t be dismissive of Nvidia either, as we discussed in early 2025).

IP licensing is a lower margin business than selling leading networking chips that Broadcom designs and sells itself. And the extra suppliers Google is reportedly bringing in could pressure that business even more, even as the growth soars for Broadcom.

This is why additional XPU customers are important for Broadcom. Google is diversifying, and therefore Broadcom needs to as well.

Anthropic is one such important new customer. The AI lab is also going to have access to Google’s TPU compute capacity. Tan confirmed on the earnings call that both Apollo and Blackstone are providing debt financing to help customers like Anthropic access this high-performance compute. Broadcom itself is providing a residual value guarantee on those TPUs (which effectively lowers the interest rate on the debt) should Anthropic encounter financial difficulties in the future. Expect more deals like this to be announced.

Google will get a cut of this deal too, since it’s the lead designer of the TPU. So that’s great for Google shareholders. But Google also needs cash. Thus the equity raise that was recently announced, with Berkshire Hathaway taking the lead on that. We like it when our unrelated and (we hope) still diversified portfolio holdings come together on a deal.

The next growth cycle is emerging

It’s easy to focus entirely on the big hyperscaler customers, but as we’ve noted recently, the enterprise IT market beyond the big cloud and AI providers is starting to join in on the AI party. Tan addressed a question about this third tier of customers that could sustain demand for many years to come.

Legacy enterprise IT has begun an even larger migration to the cloud, much of that happening via AI token consumption – through the big hyperscalers (Google Cloud, Amazon AWS, Microsoft Azure, Oracle Cloud) or through neo-clouds like CoreWeave and Nebius. Enterprises are increasingly accessing AI compute via cloud rent rather than owning it outright, but we can see a path to that eventually changing.

On-premises data centers and mobile and internet infrastructure provider upgrades are also underway. All of this is potential future customer diversification for Broadcom’s networking products, and for semiconductor companies overall.

We don’t do “earnings reviews” anymore, we’re trying to help you cut down on pointless market noise, but thought this report was notable. It’s now up to you, dear reader, to decide if it warrants any action.

For our full DCF model on Broadcom, detailed supply chain analysis, and access to our AI semiconductor stock index, join us over on Semi Insider.

6 Responses

Satisfied with your non-fee products. You guys seem reasonable, sensible video podcasters on semiconductor personal investing topics. Thank you.

Thank you for reading!

All of your content is truly top-tier and highly professional. It’s clear that you do your homework, know your material, and put real effort into delivering quality work.

Thank you Chris, glad you found it helpful!

Having watched you both for years, I can concur with the quality and accuracy of your updates. Wide ranging, but also the deep explanatory dives. Thanks for your dedication and I look forward to each new review. The AVGO update was timely, I needed it 😀

Awesome, thank you David! Happy the update helped!