As has become the norm in this bull market, Q1 2026 earnings season is once again a referendum on the AI infrastructure race. The video linked above, from late in 2025 amidst a selloff for the same reason, is proof.

Massive capital expenditure (CapEx, an accounting term denoting spending on property and equipment with an expected multi-year or more useful life) budgets of the hyperscalers, primarily in support of cloud and AI data center infrastructure, is being poured over with a fine-tooth comb. Is the return on investment real? The answer at this point still appears to be yes.

The “Big 4” hyperscaler Q1 and full-year 2026 CapEx guidance

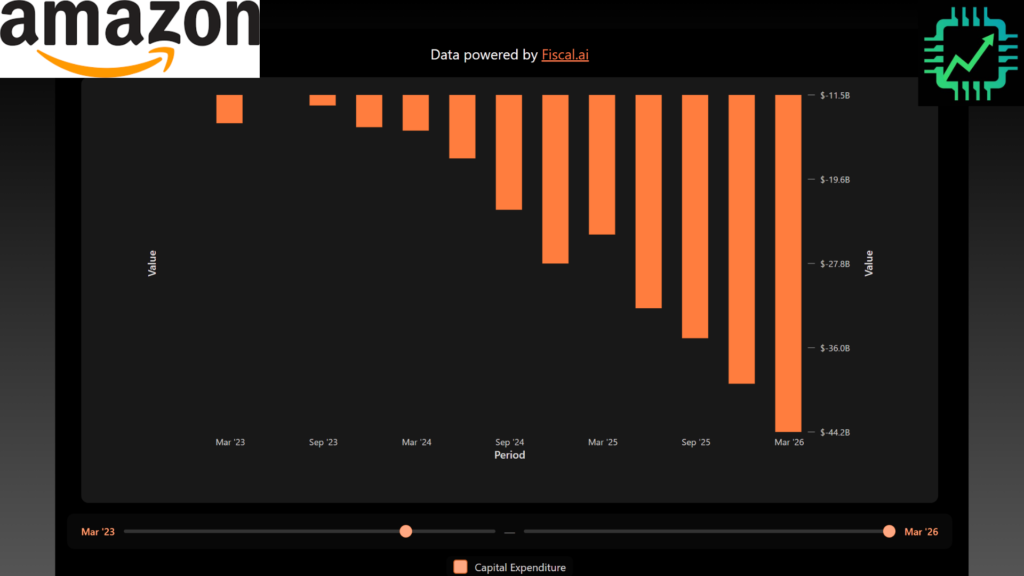

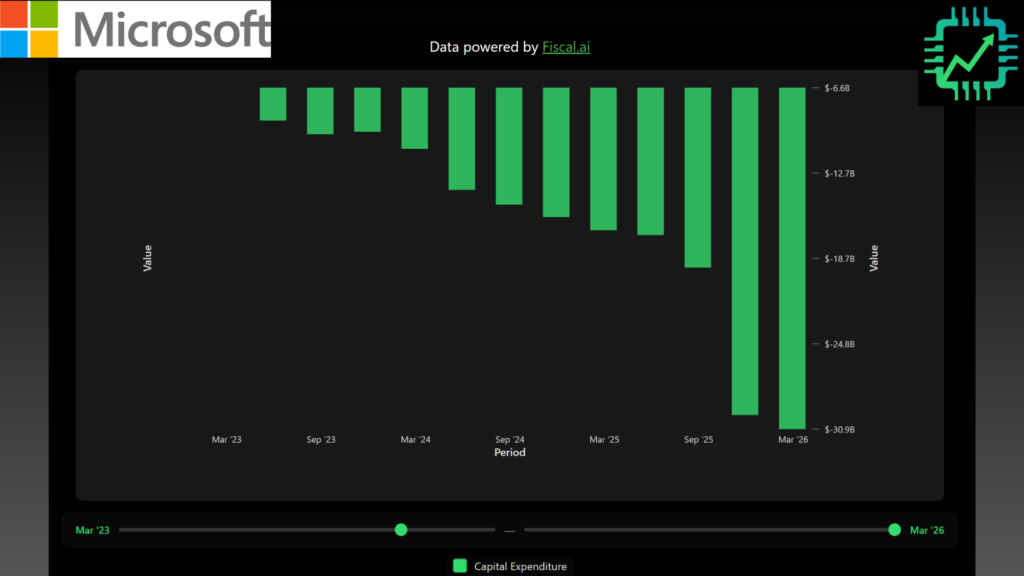

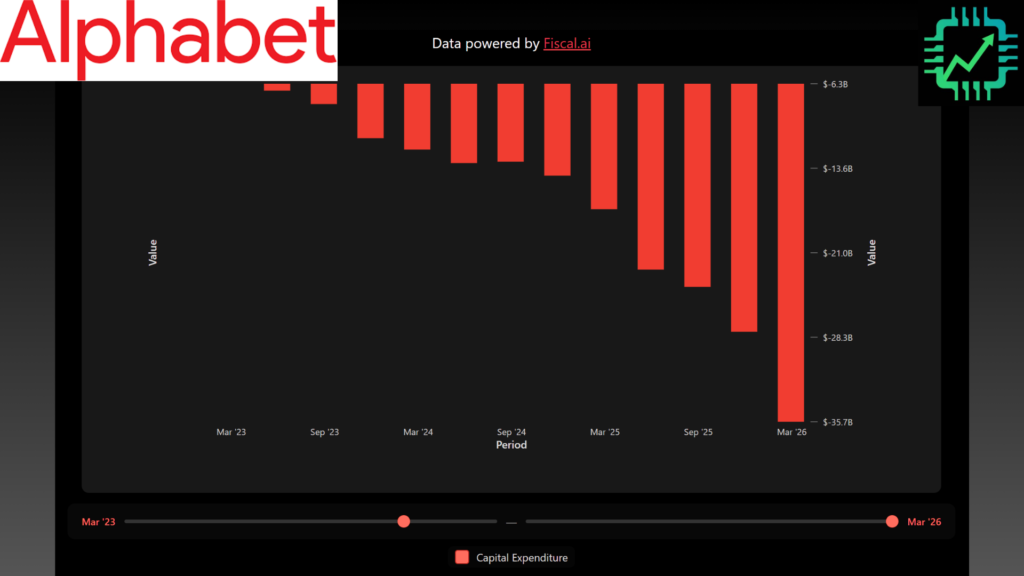

The acceleration in CapEx at Amazon, Microsoft, Alphabet, and Meta is staggering. In Q1 2026 alone, these four giants collectively spent $130 billion in CapEx.

The full-year outlook is even more eye-opening. Including Oracle, which has an off-kilter fiscal year and will report later in earnings season, total expected CapEx for 2026 is projected to exceed $750 billion — a nearly 70% increase over 2025.

| Company | Q1 2026 CapEx | Full Year 2026 Guidance |

| Amazon | $44 Billion | ~$200 Billion |

| Microsoft | $31 Billion | ~$190 Billion |

| Alphabet | High (Increased) | $180 – $190 Billion |

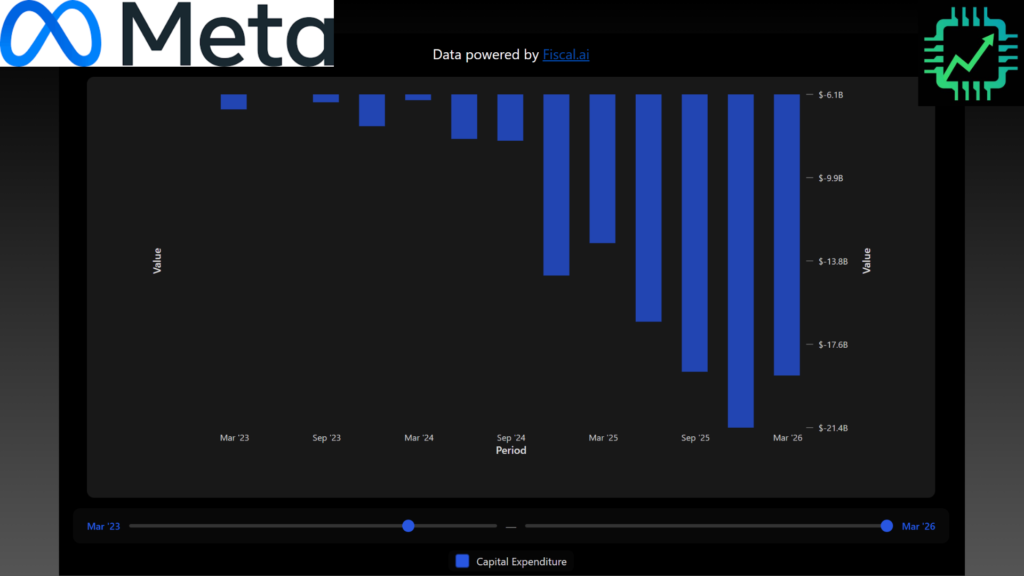

| Meta | $18 Billion | $125 – $145 Billion |

Based on the guidance, this implies CapEx will accelerate through the rest of 2026 and will progressively keep reaching new records. It’s a lob pass to call it a bubble. But is it really, or is this a period of elevated CapEx growth cycle in support of future revenue and profit expectations?

Charting source: Chip Stock Investor Research Dashboard, financial data powered by Fiscal.ai.

Is there a positive return on investment?

The primary concern for investors has been whether this “spend now, profit later” strategy is actually working. Based on the Q1 data, the return on investment is indeed still manifesting itself through revenue acceleration and expanding GAAP operating margins — albeit some of the Big 4 are performing better than others.

- Amazon: AWS revenue increased 28% year-over-year growth to $37.6 billion, driving total Amazon operating margins to 13.1% (up from 11.8% and 10.7% in Q1 2025 and Q1 2024, respectively).

- Microsoft: “Intelligent Cloud” (including Azure) revenue grew 29%, with total Microsoft operating margins hitting a massive 46.3% (up from 45.7% and 44.6% in Q1 2025 and Q1 2024, respectively).

- Alphabet: Google Cloud revenue surged 63% year-over-year. Overall Alphabet operating margins reached 36.1% (up from 33.9% and 31.6% in Q1 2025 and Q1 2024, respectively).

- Meta: Revenue accelerated 33%; operating margin dipped year-over-year due to high depreciation from Meta’s more aggressive CapEx outlay (40.6%, vs 41.5% in Q1 2025, but still up from 37.9% in Q1 2024).

The Takeaway: These companies have a vertically integrated business advantage. They “eat first” by using their own infrastructure to improve internal workloads and software products; Amazon, Microsoft, and Alphabet Google Cloud then rent capacity to the AI labs, enterprise software companies, and other customers.

The road to 2027

It’s still early, but this CapEx growth momentum is generally expected to carry through into 2027 and keep reaching new highs. However, three years in a row of 60%+ CapEx growth is not sustainable. The growth rate of this spending should moderate by 2027. At any rate, the cycle is a cash-printing machine for semiconductor leaders.

For shareholders, the volatility is a byproduct of cash flow expectations. If you can look past the short-term stock swings, you’ll see some of the most profitable businesses in history doubling down on a technological shift that shows no signs of slowing. A fundamental rebuilding of the world is in full swing.

Chip Stock Investor is building a Research Dashboard and an expanding portfolio of investing tools based on the CSI investing process and research articles. Get in the game early and be part of the journey! Access the tools and full research articles here: chipstockinvestor.com/pricing/

One Response

Fire!!